Download presentation

Presentation is loading. Please wait.

1

2005 Annual Results

3

2005 Results Summary Turnover £1,522m (2004 – £1,159m) EBITDA £71.4m (2004 – £49.5m) Profit from Operations £44.9m (2004 – £20.8m) Profit before tax £40.9m (2004 – £16.5m) Tax charge 35.6% (2004 – 32.8%) Basic EPS 21.2p (2004 – 7.9p) Dividend 6.0p (2004 – 4.5p) +31% +44% +116% +148% +168% +33%

EBITDA £71.4m (2004 – £49.5m) Profit from Operations £44.9m (2004 – £20.8m) Profit before tax £40.9m (2004 – £16.5m) Tax charge 35.6% (2004 – 32.8%) Basic EPS 21.2p (2004 – 7.9p) Dividend 6.0p (2004 – 4.5p) +31% +44% +116% +148% +168% +33%")

4

Turnover and Profit from Operations Year End December 2005 December 2004 Turnover £m Profit from Operations £m Operating MarginTurnover £m Profit from Operations £m Operating Margin Gibson Energy - Marketing - Other Hunting Energy Tenkay Others 1,016.7 197.7 202.3 12.3 92.9 10.7 11.1 18.9 5.3 1.5 1% 6% 9% 43% 2% 747.2 165.9 159.1 8.5 78.7 7.0 8.5 8.3 3.1 2.7 1% 5% 36% 3% 1,521.947.53%1,159.429.63%

5

Financial Net Borrowings Gearing Interest Cover December 2005 £97.0m 53% 7.1x December 2004 £130.6m 117% 5.7x

6

Capital Expenditure 2005 £m 2004 £m Gibson Energy Hunting Energy Tenkay Other Activities 16.1 9.2 5.6 2.0 8.4 5.0 6.4 2.1 32.921.9 Split: Maintenance New business 15.0 17.9 32.9 13.1 8.8 21.9

7

Cash Flow 2005 £m 2004 £m Cash from operations Capital Expenditure Interest etc. FREE CASH FLOW Acquisitions Disposals Equity dividends Rights Issue/ Preference Shares Repaid Other Decrease(increase) in Debt 54.8 (32.9) (4.0) 17.9 (11.9) 6.1 (5.6) 43.6 (16.5) 33.6 46.0 (21.9) (8.7) 15.4 (1.5) 28.3 (3.8) (47.9) 5.5 (4.0)

in Debt 54.8 (32.9) (4.0) 17.9 (11.9) 6.1 (5.6) 43.6 (16.5) (21.9) (8.7) 15.4 (1.5) 28.3 (3.8) (47.9) 5.5 (4.0).")

9

Hunting PLC Corporate Strategy Geographic Position Market Share Strength Proprietary Technologies Asset Utilisation

11

Hunting PLC Market Share Strength Gibson Energy – Canwest and Truck Transportation Gibson Shipbrokers – Tanker Broking Hunting Energy – Accessory Manufacturing Hunting Performance – Mud Motors Hunting Iberia – Drill Rod and Accessories Huaxin – Premium Connections (China)

")

12

Hunting PLC Proprietary Technologies Gibson Energy: Next Generation Transportation Methods State of the Art Terminals Well Site Fluid Products Hunting Energy: SWB Technologies Patented Premium Connection Technology Patented Environmental Running / Storage Compounds Patented Mud Motor Technologies Hunting Energy France: New Valve Development Automated Depot Management

13

Hunting PLC Asset Utilization Gibson Energy: Leveraging strategically located pipelines, storage tanks, terminals and truck transportation to combine crude oil of a lesser value with diluent to blend into products of higher value. Hunting Energy: Leveraging strategically located facilities, proprietary technologies and manufacturing expertise, providing products and services for well construction and well completion phases of E&P operations.

15

Gibson Energy Profit from Operations December 2005 Operating Margin December 2004 Operating Margin Marketing Truck Transportation Terminals and Pipelines Canwest Propane and Natural Gas Liquids Moose Jaw Asphalt 10.7 4.9 5.7 3.0 (2.5) 21.8 1% 7% 40% 6% 7.0 2.6 5.3 1.6 (1.0) 15.5 1% 5% 44% 3%

% 7% 40% 6% (1.0) % 5% 44% 3%")

17

Purchase and Sale of Crude Oil and Condensate 250K BBLs/Day 50 Employees Quality Management Risk Management and Arbitrage Purchase and Sale of Natural Gas Management of Crude Flow Through Owned Assets Gibson Energy: Marketing Activities

18

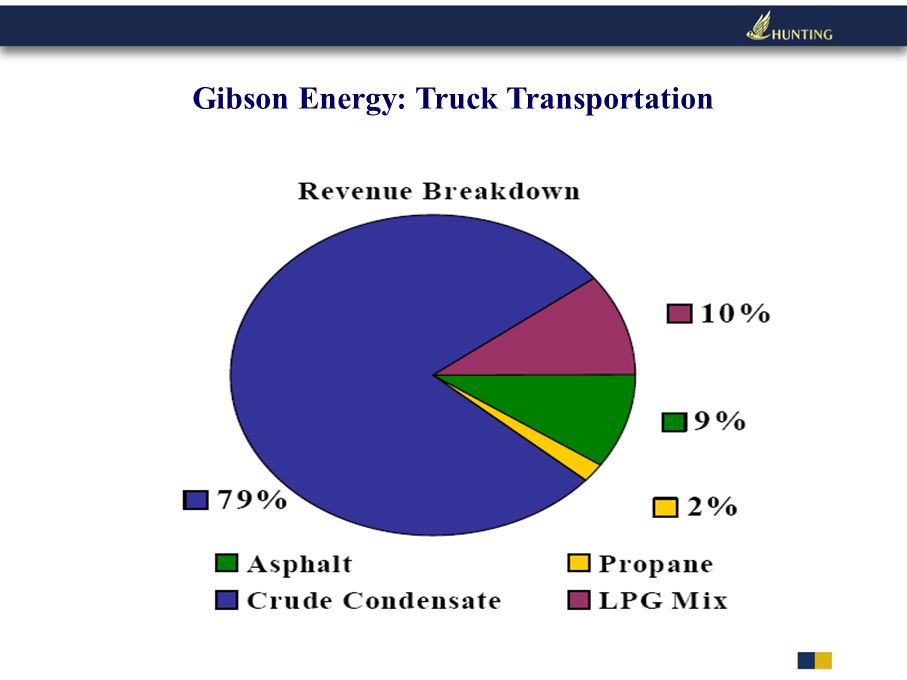

Gibson Energy: Truck Transportation

20

530 Tractor Units, 1000 Trailer Units, 186 Employees Athabasca Tar Sands Ft. McMurray is world’s second largest reserves of oil next to Saudi Arabia 75 billion dollars of investment over the next ten years Gibson Trucking hauls 100% of Bitumen in Ft. McMurray, Alberta New projects provide continued opportunities to haul Bitumen and Froth until projects reach commercial status Gibson Energy: Truck Transportation Growth and Opportunity

21

Gibson Energy: Terminals and Pipelines Hardisty Terminal Largest of the Gibson Terminal Facilities 1.6 Million Barrels of Storage 200K bpd Throughput Strategic Location

22

Refined Product and Crude Oil Terminal Strategic position in the Heart of Edmonton “Refinery Row” and “Pipeline Alley” 450k Barrel Capacity Rail Car Loading and Unloading Capabilities Handles 100% of Diesel Fuel produced by Suncor Facility in Ft. McMurray Receives Product via pipelines and transfers to Rail and Truck Receives Crude Oil and Condensate by Truck and Rail supporting Gibson Marketing Blending Operations Gibson Energy: Edmonton South Terminal

23

New Facility – commissioned in January 2006 310k Barrel Capacity Pipeline Connects to Pembina and Rainbow Pipeline Systems Receipt of Crude Oil and Condensate in facilities to support Gibson Marketing activities Connected to Enbridge Mainline and Terasen Pipelines Gibson Energy: Edmonton North Terminal

24

Second Largest Propane Company in Canada Operations in BC, AB, SK, WA State 12 Branches and 27 Storage Facilities 145 Fully Equipped, Delivery and Service Vehicles 128 Branch, Operational and Sales People 21 Owner Operators 12 Field and Corporate Management People Gibson Energy: Canwest Operations

25

Gibson Energy Canwest Operations

26

Vision Acquire under-utilised plant Expand utilisation – Increase volume via year-round operation Upgrade value received on top of barrel Experience Constant asphalt prices Increasing feedstock costs Expanding markets for high value products grew slower than increased crude costs. Gibson Energy: Moose Jaw Asphalt

28

Hunting Energy Profit from Operations: December 2005 £m Operating Margin £m December 2004 £m Operating Margin £m Well Construction Well Completion 6.7 12.2 ____ 18.9 10% 9% 4.8 3.5 ____ 8.3 11% 3% 5%

29

Hunting Energy: Business Platforms Well Construction Products and Accessories to Increase Drilling Rates for Oil and Gas Applications Mud Motors Shock Tools Support Equipment and Services Products and Accessories for Commercial Applications “Firestick” Drill Stem Supporting Telecommunication Industry SWB in Support of UCT Engineered Connections: Premium Connections for OCTG Casing and Tubing Annular Pressure Relief System

30

Hunting Energy: Business Platforms Well Completion Manufacturing: Downhole Completion Accessories OEM Licensed Manufacturing Specialty Manufacturing Pressure Control Equipment Slickline / Wireline Equipment Tubular Products: Chrome OCTG Casing and Tubing 2 Step Tubing Clear Run

31

Hunting Energy: New Technologies Well Construction: Coiled Tubing and Disposable Mud Motors Large O. D. Premium Connections “Near Bit” Sensor for SWB Well Completion: State of the Art Manufacturing Equipment “Clam” Pressure Control Equipment Environmentally Sound Thread Protection

33

Tenkay Resources December 2005 £m Operating Margin December 2004 £m Operating Margin Oil and Gas Drilling Activities5.343%3.136% Profit from Operations: Highlights: 17 Wells and 13 Successes Oil: 3 Gas: 10 105% Reserve Replacement (2.42m) (Net Equivalent Barrels) Production: 364,403 (Net Equivalent Barrels)

(Net Equivalent Barrels) Production: 364,403 (Net Equivalent Barrels)")

34

Ownership Position Working interests vary from 25% to less than 1%, with the majority around 9% to 10%. About 75 profit centres of wells/facilities/well units. 49 offshore, 26 onshore 276 individual wells.

36

Gibson Shipbrokers Highlights: Sustained high levels of activity in traditional tanker markets Increased share in Dry Cargo and Gas segments Expanded London base and growth overseas in Middle East and Far East Profit from Operations: December 2005 £m Operating Margin December 2004 £m Operating Margin Broking Activities2.511%1.69%

38

Hunting Energy France Highlights: Roforge– New product development Interpec– Added value engineering from cogeneration Larco– Acquisition of Setmat for automated depot management Profit from Operations December 2005 £m Operating Margin December 2004 £m Operating Margin Petroleum Equipment1.19%1.08%

39

Source: Spears and Associates

40

Average Oil and Gas Prices fcst Source : EIA

41

Conclusion: Continued Strong Commodity Fundamentals Increasing E & P Spend and Project Development Geopolitical Uncertainty Challenged production capability Reserve Replacements / Depletion Rates Demand Will Continue to Rise

42

Outlook Hunting in 2006 will: Maximise Asset Utilisation Increase Capacity with Customer Assurances Push New Technologies, Products and Services Further Afield Examine Acquisition Opportunities that meet Financial Criteria Deliver Results

43

2005 Annual Results

Similar presentations