Download presentation

Presentation is loading. Please wait.

1

Financial Reports

2

LEARNING OBJECTIVES 1. Compare and contrast the fundamental objectives of a balance sheet and an income statement. 2. Demonstrate the relationship between a balance sheet and an income statement for a given year. 3. Describe the utility of financial ratios and interpret basic financial ratios used in community pharmacy practice. 4. Describe and integrate the financial information depicted in a balance sheet and an income statement in community pharmacy practice. 5. Define the flow of funds involved in community pharmacy practice, including expenses, prescription adjudication, receipt of payment, and revenue generation.

3

Assets = owner’s equity + liabilities

Accounting is the language of business Accounting : “a service activity, whose function is to provide quantitative information, primarily financial in nature, about economic entities that is intended to be useful in making economic decisions.” A major use of accounting is to track the flow of money (cash or credit) between financing and investing activities Assets = owner’s equity + liabilities

between financing and investing activities. Assets = owner’s equity + liabilities.")

4

ACCOUNTING PRINCIPLES

pharmacy, just as any other type of organization, engages in three fundamental activities: Obtaining financing Making investments Conducting a profitable operation

5

Obtaining Financing Financing activities to acquire assets involve obtaining funds from 1- owners 2- creditors (i.e., banks). When owners fund the activities of a corporation, they become shareholders of the corporation.

. When owners fund the activities of a corporation, they become shareholders of the corporation.")

6

Making Investments In pharmacy settings, funds are invested in acquisition of inventory, computer software and hardware, robotics, buildings, and land. Acquiring the resources necessary to employ the appropriate number of pharmacists, pharmacy technicians, and other staff also can be viewed as an investment activity

7

Conducting a Profitable Operation

Generally, the operating activities of pharmacy settings include: Purchasing Distribution (i.e., prescription-filling activities), Clinical activities Administration Marketing is also a significant operation activity, in that it is required so that others can learn of the goods and services that the pharmacy offers

, Clinical activities. Administration. Marketing is also a significant operation activity, in that it is required so that others can learn of the goods and services that the pharmacy offers.")

8

THREE ESSENTIAL FINANCIAL STATEMENTS

9

The fiscal year is a unit of time—a year as the term implies—that businesses use to record their financial interactions.

10

The Balance Sheet Provides a snapshot of an organization’s assets, liabilities, and shareholder equity at any particular point in time Balance sheet’s total assets must equal the total liabilities plus shareholders’ equity at all times. It does not reveal much about what caused these values to change over the course of the year does not tell us how income was generated and what types of expenses during the accounting period.

11

The Income Statement Income statement is a dynamic document that provides information about money coming into an organization (income) and money necessary to obtain that income (expenses). The difference between income and expenses is commonly referred to as net income

and money necessary to obtain that income (expenses). The difference between income and expenses is commonly referred to as net income.")

12

The Statement of Cash Flows

Throughout the fiscal year, the inflows and outflows of cash are recorded in the statement of cash flows These recorded values generally fall into three categories: Operating Investing Financing ment.asp

13

FINANCIAL RATIOS Organizations, investors, creditors, and even individuals use financial ratios to examine an organization’s financial performance. Financial ratio is a financial analysis comparison in which certain financial statement items are divided by one another to reveal their logical interrelationships. Data are taken from the balance sheet and income statement for calculating most ratios. They should not be used in isolation from other financial reports

14

In general, financial ratios allow users of financial information to make comparisons between:

A single organization and the entire industry average Differences within an organization over time (e.g., months, quarters, years) Two or more units with a single organization (e.g., pharmacies within the same chain) Two or more organizations with each other (e.g., comparisons between chain pharmacy corporations) Financial ratio analysis is only as valid as the financial information on which it is based.

Two or more units with a single organization (e.g., pharmacies within the same chain) Two or more organizations with each other (e.g., comparisons between chain pharmacy corporations) Financial ratio analysis is only as valid as the financial information on which it is based.")

16

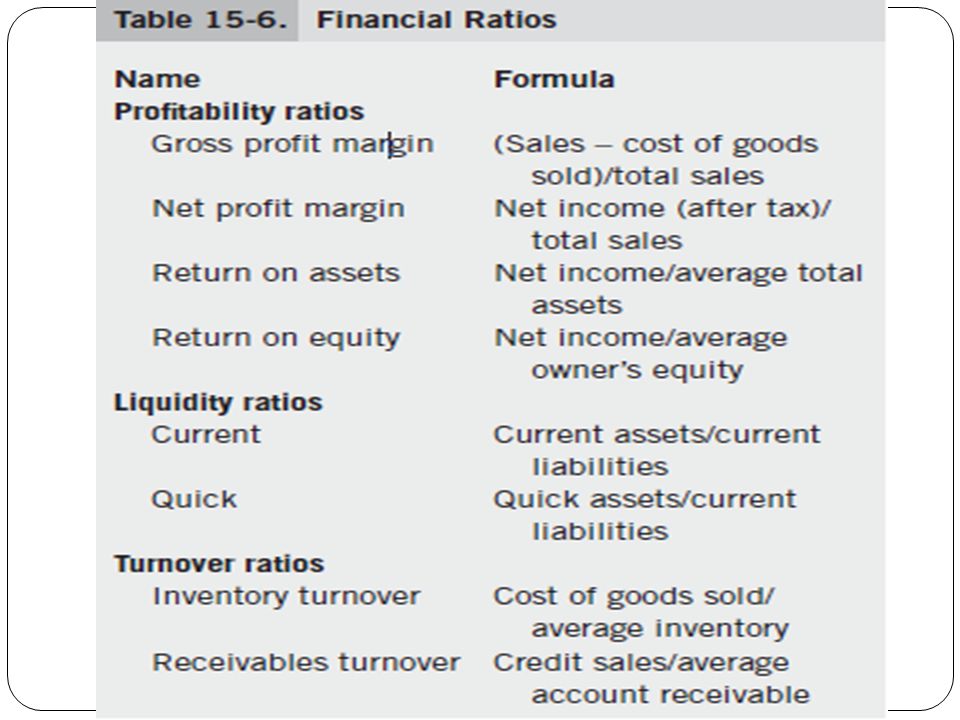

Profitability Ratios Profitability ratios provide a method to measure the overall financial success of a company The most commonly used profitability ratios are the gross profit margin and the net profit margin. Gross profit margin = (sales − cost of goods sold) ÷ total sales this ratio provides information on the company’s ability to generate gross profits Higher gross profit margin ratios are desirable because they indicate the availability of funds for the company’s other expenses

÷ total sales. this ratio provides information on the company’s ability to generate gross profits. Higher gross profit margin ratios are desirable because they indicate the availability of funds for the company’s other expenses.")

17

Net profit margin = net income (after taxes) ÷ total sales

Net profit margin indicates the fraction of net profit that is generated for every riyal of sales Return on assets (ROA) = net income ÷ average total assets provides information on the company’s ability to generate profits using the company’s assets profits can only be generated from the company’s assets. Therefore, effective use of assets results in a high ROA ratio

= net income ÷ average total assets. provides information on the company’s ability to generate profits using the company’s assets. profits can only be generated from the company’s assets. Therefore, effective use of assets results in a high ROA ratio.")

18

Return on equity (ROE) = net income ÷ average owner’s equity

Return on equity, also known as return on investment (ROI), is a measure of how well the company can make profits from funds provided by owners or investors High ROE levels are desirable because investors— similar to companies—are interested in maximizing their profits Managers who make better financial decisions are better able to produce higher ROA and ROE ratios for their organizations.

, is a measure of how well the company can make profits from funds provided by owners or investors. High ROE levels are desirable because investors— similar to companies—are interested in maximizing their profits. Managers who make better financial decisions are better able to produce higher ROA and ROE ratios for their organizations.")

19

Liquidity Ratios Provide information on the business’s ability to meet its short-term financial obligations The current ratio is the ratio of current assets to current liabilities. Current ratio = current assets ÷ current liabilities An organization with a high current ratio is taking fewer risks in meeting its financial obligation

20

High values greater than 5 This might be a sign of a company that is too conservative, leaving too much of its money in the bank rather than investing it in ways that could help the organization grow (e.g., building new pharmacies or expanding existing services). A low current ratio (<2.0) indicates that the organization has low current assets (especially cash) relative to its current liabilities (often bills that are due in 30 to 60 days).

indicates that the organization has low current assets (especially cash) relative to its current liabilities (often bills that are due in 30 to 60 days).")

21

Quick ratio quick assets are defined as assets that are easily converted to cash it provides a better picture of a company’s liquidity and its ability to meet its financial obligations. Quick ratio = (current assets − inventories − prepaid expenses) ÷ current liabilities The standard quick ratio that any organization strives to obtain is at least 1.0 less means not enough money to pay obligations

÷ current liabilities. The standard quick ratio that any organization strives to obtain is at least 1.0 less means not enough money to pay obligations.")

22

Turnover Ratios Turnover ratios measure the efficiency with which an organization uses its assets Inventory turnover ratio = cost of goods sold ÷ average inventory (at cost) The inventory turnover ratio measures how quickly, on average, an organization’s inventories are sold Low inventory turnover ratios (6.0 or below) indicate that the organization’s inventory is too large for its operations and that cash that could be better spent elsewhere is tied up in inventory

The inventory turnover ratio measures how quickly, on average, an organization’s inventories are sold. Low inventory turnover ratios (6.0 or below) indicate that the organization’s inventory is too large for its operations and that cash that could be better spent elsewhere is tied up in inventory.")

23

High inventory turnover ratios are generally desirable because this means that the organization was able to sell and replace its inventory with high efficiency and therefore generate higher revenues and profits

24

Receivables turnover ratio = credit sales ÷ average accounts receivable

This ratio measures how quickly receivables (money owed to the organization by others) are turned into cash

are turned into cash.")

25

Quiz What are the three types of financial statements .

26

Definition of 'Equity ' A stock or any other security representing an ownership interest. On a company's balance sheet, the amount of the funds contributed by the owners (the stockholders) plus the retained earnings (or losses). Also referred to as "shareholders' equity". In the context of margin trading, the value of securities in a margin account minus what has been borrowed from the brokerage. In the context of real estate, the difference between the current market value of the property and the amount the owner still owes on the mortgage. It is the amount that the owner would receive after selling a property and paying off the mortgage. In terms of investment strategies, equity (stocks) is one of the principal asset classes. The other two are fixed-income (bonds) and cash/cash-equivalents. These are used in asset allocation planning to structure a desired risk and return profile for an investor's portfolio.

plus the retained earnings (or losses). Also referred to as shareholders equity . In the context of margin trading, the value of securities in a margin account minus what has been borrowed from the brokerage. In the context of real estate, the difference between the current market value of the property and the amount the owner still owes on the mortgage. It is the amount that the owner would receive after selling a property and paying off the mortgage. In terms of investment strategies, equity (stocks) is one of the principal asset classes. The other two are fixed-income (bonds) and cash/cash-equivalents. These are used in asset allocation planning to structure a desired risk and return profile for an investor s portfolio.")

27

Definition of 'Liability‘ A company's legal debts or obligations that arise during the course of business operations. Liabilities are settled over time through the transfer of economic benefits including money, goods or services. Definition of 'Asset' A resource with economic value that an individual, corporation or country owns or controls with the expectation that it will provide future benefit. A balance sheet item representing what a firm owns.

28

Definition of 'Return On Assets - ROA'

An indicator of how profitable a company is relative to its total assets. ROA gives an idea as to how efficient management is at using its assets to generate earnings. Calculated by dividing a company's annual earnings by its total assets, ROA is displayed as a percentage. Sometimes this is referred to as "return on investment” Note: Some investors add interest expense back into net income when performing this calculation because they'd like to use operating returns before cost of borrowing.

29

ROA tells you what earnings were generated from invested capital (assets). ROA for public companies can vary substantially and will be highly dependent on the industry. This is why when using ROA as a comparative measure, it is best to compare it against a company's previous ROA numbers or the ROA of a similar company. The assets of the company are comprised of both debt and equity. Both of these types of financing are used to fund the operations of the company. The ROA figure gives investors an idea of how effectively the company is converting the money it has to invest into net income. The higher the ROA number, the better, because the company is earning more money on less investment. For example, if one company has a net income of $1 million and total assets of $5 million, its ROA is 20%; however, if another company earns the same amount but has total assets of $10 million, it has an ROA of 10%. Based on this example, the first company is better at converting its investment into profit. When you really think about it, management's most important job is to make wise choices in allocating its resources. Anybody can make a profit by throwing a ton of money at a problem, but very few managers excel at making large profits with little investment.

Similar presentations

. What is ratio analysis? A set of accounting ratios often used to help interested parties interpret ( make.>")