Download presentation

Presentation is loading. Please wait.

1

PRINCIPLES OF MONEY-TIME RELATIONSHIPS

2

MONEY Medium of Exchange -- Means of payment for goods or services; What sellers accept and buyers pay ; Store of Value -- A way to transport buying power from one time period to another; Unit of Account -- A precise measurement of value or worth; Allows for tabulating debits and credits; Medium of Exchange -- Means of payment for goods or services; What sellers accept and buyers pay ; Store of Value -- A way to transport buying power from one time period to another; Unit of Account -- A precise measurement of value or worth; Allows for tabulating debits and credits;

3

CAPITAL Wealth in the form of money or property that can be used to produce more wealth.

4

CAPITAL The majority of engineering economy studies involve commitment of capital for extended period of time, so the effect of time must be considered. A dollar today is worth more than a dollar one or more years from now because of the interest (or profit) it can earn. Therefore, money has a time value. The majority of engineering economy studies involve commitment of capital for extended period of time, so the effect of time must be considered. A dollar today is worth more than a dollar one or more years from now because of the interest (or profit) it can earn. Therefore, money has a time value.

it can earn. Therefore, money has a time value. The majority of engineering economy studies involve commitment of capital for extended period of time, so the effect of time must be considered. A dollar today is worth more than a dollar one or more years from now because of the interest (or profit) it can earn. Therefore, money has a time value..")

5

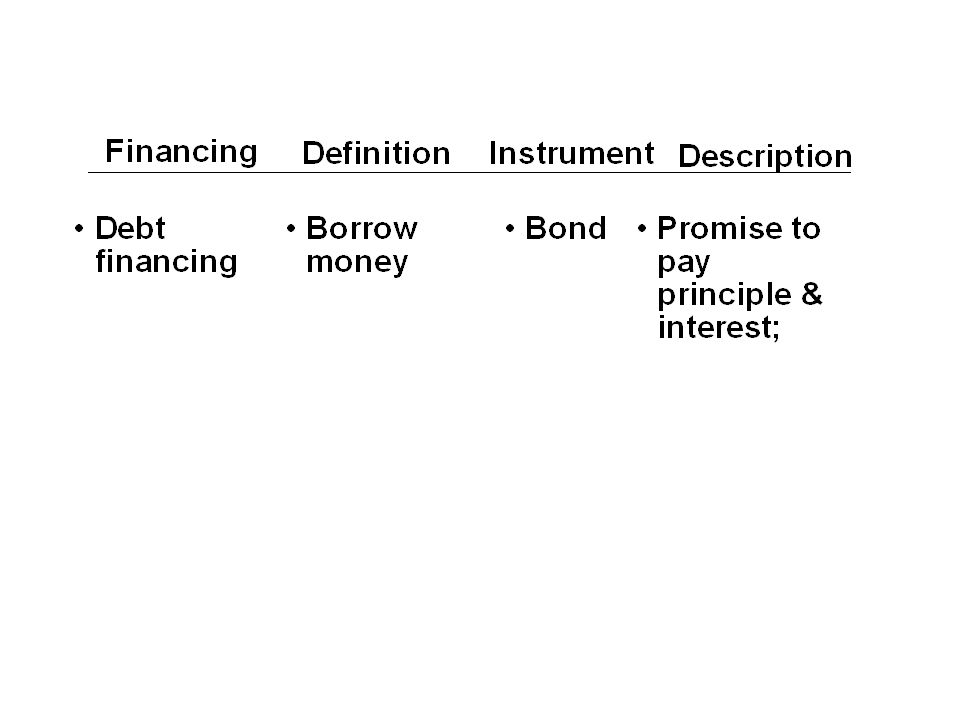

KINDS OF CAPITAL Capital in the form of money for the people, machines, materials, energy, and other things needed in the operation of an organization may be classified into two basic categories: Equity capital is that owned by individuals who have invested their money or property in a business project or venture in the hope of receiving a profit. Debt capital, often called borrowed capital, is obtained from lenders (e.g., through the sale of bonds) for investment. In return the lenders receive interest from the borrowers. Capital in the form of money for the people, machines, materials, energy, and other things needed in the operation of an organization may be classified into two basic categories: Equity capital is that owned by individuals who have invested their money or property in a business project or venture in the hope of receiving a profit. Debt capital, often called borrowed capital, is obtained from lenders (e.g., through the sale of bonds) for investment. In return the lenders receive interest from the borrowers.

for investment. In return the lenders receive interest from the borrowers. Capital in the form of money for the people, machines, materials, energy, and other things needed in the operation of an organization may be classified into two basic categories: Equity capital is that owned by individuals who have invested their money or property in a business project or venture in the hope of receiving a profit. Debt capital, often called borrowed capital, is obtained from lenders (e.g., through the sale of bonds) for investment. In return the lenders receive interest from the borrowers..")

8

Exchange money for shares of stock as proof of partial ownership

9

INTEREST The fee that a borrower pays to a lender for the use of his or her money. INTEREST RATE The percentage of money being borrowed, that is paid to the lender on some time basis. Is the rate of gain received from an investment. The fee that a borrower pays to a lender for the use of his or her money. INTEREST RATE The percentage of money being borrowed, that is paid to the lender on some time basis. Is the rate of gain received from an investment.

10

HOW INTEREST RATE IS DETERMINED Interest Rate Quantity of Money

11

HOW INTEREST RATE IS DETERMINED Interest Rate Quantity of Money Money Demand

12

HOW INTEREST RATE IS DETERMINED Interest Rate Quantity of Money Money Demand Money Supply MS 1

13

HOW INTEREST RATE IS DETERMINED Interest Rate Quantity of Money ieie Money Demand Money Supply MS 1

14

HOW INTEREST RATE IS DETERMINED Interest Rate Quantity of Money ieie Money Demand Money Supply MS 1 MS 2 i2i2

15

HOW INTEREST RATE IS DETERMINED Interest Rate Quantity of Money ieie Money Demand Money Supply MS 1 MS 2 i2i2 MS 3 i3i3

16

SIMPLE INTEREST The total interest earned or charged is linearly proportional to the initial amount of the loan (principal), the interest rate and the number of interest periods for which the principal is committed. When applied, total interest “I” may be found by I = ( P ) ( N ) ( i ), where –P = principal amount lent or borrowed –N = number of interest periods ( e.g., years ) –i = interest rate per interest period The total interest earned or charged is linearly proportional to the initial amount of the loan (principal), the interest rate and the number of interest periods for which the principal is committed. When applied, total interest “I” may be found by I = ( P ) ( N ) ( i ), where –P = principal amount lent or borrowed –N = number of interest periods ( e.g., years ) –i = interest rate per interest period

( N ) ( i ), where –P = principal amount lent or borrowed –N = number of interest periods ( e.g., years ) –i = interest rate per interest period The total interest earned or charged is linearly proportional to the initial amount of the loan (principal), the interest rate and the number of interest periods for which the principal is committed. When applied, total interest I may be found by I = ( P ) ( N ) ( i ), where –P = principal amount lent or borrowed –N = number of interest periods ( e.g., years ) –i = interest rate per interest period.")

17

COMPOUND INTEREST Whenever the interest charge for any interest period is based on the remaining principal amount plus any accumulated interest charges up to the beginning of that period. Period Amount Owed Interest Amount Amount Owed Beginning of for Period at end of period ( @ 10% ) period 1$1,000$100$1,100 2$1,100$110$1,210 3$1,210$121$1,331 Whenever the interest charge for any interest period is based on the remaining principal amount plus any accumulated interest charges up to the beginning of that period. Period Amount Owed Interest Amount Amount Owed Beginning of for Period at end of period ( @ 10% ) period 1$1,000$100$1,100 2$1,100$110$1,210 3$1,210$121$1,331

period 1$1,000$100$1,100 2$1,100$110$1,210 3$1,210$121$1,331 Whenever the interest charge for any interest period is based on the remaining principal amount plus any accumulated interest charges up to the beginning of that period. Period Amount Owed Interest Amount Amount Owed Beginning of for Period at end of period 10% ) period 1$1,000$100$1,100 2$1,100$110$1,210 3$1,210$121$1,331.")

18

ECONOMIC EQUIVALENCE Established when we are indifferent between a future payment, or a series of future payments, and a present sum of money. Considers the comparison of alternative options, or proposals, by reducing them to an equivalent basis, depending on: –interest rate; –amounts of money involved; –timing of the affected monetary receipts and/or expenditures; –manner in which the interest, or profit on invested capital is paid and the initial capital is recovered. Established when we are indifferent between a future payment, or a series of future payments, and a present sum of money. Considers the comparison of alternative options, or proposals, by reducing them to an equivalent basis, depending on: –interest rate; –amounts of money involved; –timing of the affected monetary receipts and/or expenditures; –manner in which the interest, or profit on invested capital is paid and the initial capital is recovered.

19

ECONOMIC EQUIVALENCE FOR FOUR REPAYMENT PLANS OF AN $8,000 LOAN Plan #1: $2,000 of loan principal plus 10% of BOY principal paid at the end of year; interest paid at the end of each year is reduced by $200 (i.e., 10% of remaining principal) YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$2,000 $2,800 2$6,000$600 $6,600$2,000 $2,600 3$4,000$400 $4,400$2,000 $2,400 4$2,000$200 $2,200$2,000 $2,200 Total interest paid ($2,000) is 10% of total dollar-years ($20,000) Plan #1: $2,000 of loan principal plus 10% of BOY principal paid at the end of year; interest paid at the end of each year is reduced by $200 (i.e., 10% of remaining principal) YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$2,000 $2,800 2$6,000$600 $6,600$2,000 $2,600 3$4,000$400 $4,400$2,000 $2,400 4$2,000$200 $2,200$2,000 $2,200 Total interest paid ($2,000) is 10% of total dollar-years ($20,000)

YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$2,000 $2,800 2$6,000$600 $6,600$2,000 $2,600 3$4,000$400 $4,400$2,000 $2,400 4$2,000$200 $2,200$2,000 $2,200 Total interest paid ($2,000) is 10% of total dollar-years ($20,000) Plan #1: $2,000 of loan principal plus 10% of BOY principal paid at the end of year; interest paid at the end of each year is reduced by $200 (i.e., 10% of remaining principal) YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$2,000 $2,800 2$6,000$600 $6,600$2,000 $2,600 3$4,000$400 $4,400$2,000 $2,400 4$2,000$200 $2,200$2,000 $2,200 Total interest paid ($2,000) is 10% of total dollar-years ($20,000)")

20

Plan #2: $0 of loan principal paid until end of fourth year; $800 interest paid at the end of each year YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$0 $800 2$8,000$800 $8,800$0 $800 3$8,000$800 $8,800$0 $800 4$8,000$800 $8,800$8,000 $8,800 Total interest paid ($3,200) is 10% of total dollar-years ($32,000) Plan #2: $0 of loan principal paid until end of fourth year; $800 interest paid at the end of each year YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$0 $800 2$8,000$800 $8,800$0 $800 3$8,000$800 $8,800$0 $800 4$8,000$800 $8,800$8,000 $8,800 Total interest paid ($3,200) is 10% of total dollar-years ($32,000) ECONOMIC EQUIVALENCE FOR FOUR REPAYMENT PLANS OF AN $8,000 LOAN

end of Year 1$8,000$800 $8,800$0 $800 2$8,000$800 $8,800$0 $800 3$8,000$800 $8,800$0 $800 4$8,000$800 $8,800$8,000 $8,800 Total interest paid ($3,200) is 10% of total dollar-years ($32,000) Plan #2: $0 of loan principal paid until end of fourth year; $800 interest paid at the end of each year YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$0 $800 2$8,000$800 $8,800$0 $800 3$8,000$800 $8,800$0 $800 4$8,000$800 $8,800$8,000 $8,800 Total interest paid ($3,200) is 10% of total dollar-years ($32,000) ECONOMIC EQUIVALENCE FOR FOUR REPAYMENT PLANS OF AN $8,000 LOAN")

21

Plan #3: $2,524 paid at the end of each year; interest paid at the end of each year is 10% of amount owed at the beginning of the year. YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$1,724 $2,524 2$6,276$628 $6,904$1,896 $2,524 3$4,380$438 $4,818$2,086 $2,524 4$2,294$230 $2,524$2,294 $2,524 Total interest paid ($2,096) is 10% of total dollar-years ($20,950) Plan #3: $2,524 paid at the end of each year; interest paid at the end of each year is 10% of amount owed at the beginning of the year. YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$1,724 $2,524 2$6,276$628 $6,904$1,896 $2,524 3$4,380$438 $4,818$2,086 $2,524 4$2,294$230 $2,524$2,294 $2,524 Total interest paid ($2,096) is 10% of total dollar-years ($20,950)

end of Year 1$8,000$800 $8,800$1,724 $2,524 2$6,276$628 $6,904$1,896 $2,524 3$4,380$438 $4,818$2,086 $2,524 4$2,294$230 $2,524$2,294 $2,524 Total interest paid ($2,096) is 10% of total dollar-years ($20,950) Plan #3: $2,524 paid at the end of each year; interest paid at the end of each year is 10% of amount owed at the beginning of the year. YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$1,724 $2,524 2$6,276$628 $6,904$1,896 $2,524 3$4,380$438 $4,818$2,086 $2,524 4$2,294$230 $2,524$2,294 $2,524 Total interest paid ($2,096) is 10% of total dollar-years ($20,950).")

22

ECONOMIC EQUIVALENCE FOR FOUR REPAYMENT PLANS OF AN $8,000 LOAN Plan #4: No interest and no principal paid for first three years. At the end of the fourth year, the original principal plus accumulated (compounded) interest is paid. YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$0 $0 2$8,800$880 $9,680$0 $0 3$9,680$968 $10,648$0 $0 4$10,648$1,065 $11,713$8,000 $11,713 Total interest paid ($3,713) is 10% of total dollar-years ($37,128) Plan #4: No interest and no principal paid for first three years. At the end of the fourth year, the original principal plus accumulated (compounded) interest is paid. YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$0 $0 2$8,800$880 $9,680$0 $0 3$9,680$968 $10,648$0 $0 4$10,648$1,065 $11,713$8,000 $11,713 Total interest paid ($3,713) is 10% of total dollar-years ($37,128)

interest is paid. YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$0 $0 2$8,800$880 $9,680$0 $0 3$9,680$968 $10,648$0 $0 4$10,648$1,065 $11,713$8,000 $11,713 Total interest paid ($3,713) is 10% of total dollar-years ($37,128) Plan #4: No interest and no principal paid for first three years. At the end of the fourth year, the original principal plus accumulated (compounded) interest is paid. YearAmount Owed Interest Accrued Total Principal Total end at beginning for Year Money Payment of Year of Year owed at Payment ( BOY ) end of Year 1$8,000$800 $8,800$0 $0 2$8,800$880 $9,680$0 $0 3$9,680$968 $10,648$0 $0 4$10,648$1,065 $11,713$8,000 $11,713 Total interest paid ($3,713) is 10% of total dollar-years ($37,128).")

23

CASH FLOW DIAGRAMS / TABLE NOTATION i = effective interest rate per interest period N = number of compounding periods (e.g., years) P = present sum of money; the equivalent value of one or more cash flows at the present time reference point F = future sum of money; the equivalent value of one or more cash flows at a future time reference point A = end-of-period cash flows (or equivalent end-of- period values ) in a uniform series continuing for a specified number of periods, starting at the end of the first period and continuing through the last period G = uniform gradient amounts -- used if cash flows increase by a constant amount in each period i = effective interest rate per interest period N = number of compounding periods (e.g., years) P = present sum of money; the equivalent value of one or more cash flows at the present time reference point F = future sum of money; the equivalent value of one or more cash flows at a future time reference point A = end-of-period cash flows (or equivalent end-of- period values ) in a uniform series continuing for a specified number of periods, starting at the end of the first period and continuing through the last period G = uniform gradient amounts -- used if cash flows increase by a constant amount in each period

P = present sum of money; the equivalent value of one or more cash flows at the present time reference point F = future sum of money; the equivalent value of one or more cash flows at a future time reference point A = end-of-period cash flows (or equivalent end-of- period values ) in a uniform series continuing for a specified number of periods, starting at the end of the first period and continuing through the last period G = uniform gradient amounts -- used if cash flows increase by a constant amount in each period i = effective interest rate per interest period N = number of compounding periods (e.g., years) P = present sum of money; the equivalent value of one or more cash flows at the present time reference point F = future sum of money; the equivalent value of one or more cash flows at a future time reference point A = end-of-period cash flows (or equivalent end-of- period values ) in a uniform series continuing for a specified number of periods, starting at the end of the first period and continuing through the last period G = uniform gradient amounts -- used if cash flows increase by a constant amount in each period")

24

CASH FLOW DIAGRAM NOTATION 12345 = N 1 1 Time scale with progression of time moving from left to right; the numbers represent time periods (e.g., years, months, quarters, etc...) and may be presented within a time interval or at the end of a time interval.

and may be presented within a time interval or at the end of a time interval.")

25

CASH FLOW DIAGRAM NOTATION 12345 = N 1 1 Time scale with progression of time moving from left to right; the numbers represent time periods (e.g., years, months, quarters, etc...) and may be presented within a time interval or at the end of a time interval. P =$8,000 2 2 Present expense (cash outflow) of $8,000 for lender.

of $8,000 for lender..")

26

CASH FLOW DIAGRAM NOTATION 12345 = N 1 1 Time scale with progression of time moving from left to right; the numbers represent time periods (e.g., years, months, quarters, etc...) and may be presented within a time interval or at the end of a time interval. P =$8,000 2 2 Present expense (cash outflow) of $8,000 for lender. A = $2,524 3 3 Annual income (cash inflow) of $2,524 for lender.

of $8,000 for lender. A = $2, Annual income (cash inflow) of $2,524 for lender..")

27

CASH FLOW DIAGRAM NOTATION 12345 = N 1 1 Time scale with progression of time moving from left to right; the numbers represent time periods (e.g., years, months, quarters, etc...) and may be presented within a time interval or at the end of a time interval. P =$8,000 2 2 Present expense (cash outflow) of $8,000 for lender. A = $2,524 3 3 Annual income (cash inflow) of $2,524 for lender. i = 10% per year 4 4 Interest rate of loan.

of $8,000 for lender. A = $2, Annual income (cash inflow) of $2,524 for lender. i = 10% per year 4 4 Interest rate of loan..")

28

CASH FLOW DIAGRAM NOTATION 12345 = N 1 1 Time scale with progression of time moving from left to right; the numbers represent time periods (e.g., years, months, quarters, etc...) and may be presented within a time interval or at the end of a time interval. P =$8,000 2 2 Present expense (cash outflow) of $8,000 for lender. A = $2,524 3 3 Annual income (cash inflow) of $2,524 for lender. i = 10% per year 4 4 Interest rate of loan. 5 5 Dashed-arrow line indicates amount to be determined.

of $8,000 for lender. A = $2, Annual income (cash inflow) of $2,524 for lender. i = 10% per year 4 4 Interest rate of loan. 5 5 Dashed-arrow line indicates amount to be determined..")

29

INTEREST FORMULAS FOR ALL OCCASIONS relating present and future values of single cash flows; relating a uniform series (annuity) to present and future equivalent values; –for discrete compounding and discrete cash flows; –for deferred annuities (uniform series); equivalence calculations involving multiple interest; relating a uniform gradient of cash flows to annual and present equivalents; relating a geometric sequence of cash flows to present and annual equivalents; relating present and future values of single cash flows; relating a uniform series (annuity) to present and future equivalent values; –for discrete compounding and discrete cash flows; –for deferred annuities (uniform series); equivalence calculations involving multiple interest; relating a uniform gradient of cash flows to annual and present equivalents; relating a geometric sequence of cash flows to present and annual equivalents;

to present and future equivalent values; –for discrete compounding and discrete cash flows; –for deferred annuities (uniform series); equivalence calculations involving multiple interest; relating a uniform gradient of cash flows to annual and present equivalents; relating a geometric sequence of cash flows to present and annual equivalents; relating present and future values of single cash flows; relating a uniform series (annuity) to present and future equivalent values; –for discrete compounding and discrete cash flows; –for deferred annuities (uniform series); equivalence calculations involving multiple interest; relating a uniform gradient of cash flows to annual and present equivalents; relating a geometric sequence of cash flows to present and annual equivalents;")

30

INTEREST FORMULAS FOR ALL OCCASIONS relating nominal and effective interest rates; relating to compounding more frequently than once a year; relating to cash flows occurring less often than compounding periods; for continuous compounding and discrete cash flows; for continuous compounding and continuous cash flows; relating nominal and effective interest rates; relating to compounding more frequently than once a year; relating to cash flows occurring less often than compounding periods; for continuous compounding and discrete cash flows; for continuous compounding and continuous cash flows;

31

RELATING PRESENT AND FUTURE EQUIVALENT VALUES OF SINGLE CASH FLOWS Finding F when given P: Finding future value when given present value F = P ( 1+i ) N –(1+i) N single payment compound amount factor –functionally expressed as F = ( F / P, i%,N ) –predetermined values of this are presented in column 2 of Appendix C of text. Finding F when given P: Finding future value when given present value F = P ( 1+i ) N –(1+i) N single payment compound amount factor –functionally expressed as F = ( F / P, i%,N ) –predetermined values of this are presented in column 2 of Appendix C of text. P 0 N = F = ?

N –(1+i) N single payment compound amount factor –functionally expressed as F = ( F / P, i%,N ) –predetermined values of this are presented in column 2 of Appendix C of text. P 0 N = F = .")

32

Finding P when given F: Finding present value when given future value P = F [1 / (1 + i ) ] N – (1+i) -N single payment present worth factor – functionally expressed as P = F ( P / F, i%, N ) –predetermined values of this are presented in column 3 of Appendix C of text; Finding P when given F: Finding present value when given future value P = F [1 / (1 + i ) ] N – (1+i) -N single payment present worth factor – functionally expressed as P = F ( P / F, i%, N ) –predetermined values of this are presented in column 3 of Appendix C of text; RELATING PRESENT AND FUTURE EQUIVALENT VALUES OF SINGLE CASH FLOWS P = ? 0N = F

![Finding P when given F: Finding present value when given future value P = F [1 / (1 + i ) ] N – (1+i) -N single payment present worth factor – functionally expressed as P = F ( P / F, i%, N ) –predetermined values of this are presented in column 3 of Appendix C of text; Finding P when given F: Finding present value when given future value P = F [1 / (1 + i ) ] N – (1+i) -N single payment present worth factor – functionally expressed as P = F ( P / F, i%, N ) –predetermined values of this are presented in column 3 of Appendix C of text; RELATING PRESENT AND FUTURE EQUIVALENT VALUES OF SINGLE CASH FLOWS P = .](http://images.slideplayer.com/22/6393729/slides/slide_32.jpg "0N = F.")

33

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A:

TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A:")

34

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments

TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments")

35

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i

TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i")

36

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ]

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ]](http://images.slideplayer.com/22/6393729/slides/slide_36.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ]")

37

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N ) Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N )

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N ) Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N )](http://images.slideplayer.com/22/6393729/slides/slide_37.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N ) Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N )")

38

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N ) –predetermined values are in column 4 of Appendix C of text Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N ) –predetermined values are in column 4 of Appendix C of text

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N ) –predetermined values are in column 4 of Appendix C of text Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N ) –predetermined values are in column 4 of Appendix C of text](http://images.slideplayer.com/22/6393729/slides/slide_38.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N ) –predetermined values are in column 4 of Appendix C of text Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N ) –predetermined values are in column 4 of Appendix C of text")

39

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N ) –predetermined values are in column 4 of Appendix C of text Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N ) –predetermined values are in column 4 of Appendix C of text F = ? 1234567 8 A =

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N ) –predetermined values are in column 4 of Appendix C of text Finding F given A: Finding future equivalent income (inflow) value given a series of uniform equal Payments ( 1 + i ) N - 1 F = A i –uniform series compound amount factor in [ ] –functionally expressed as F = A ( F / A,i%,N ) –predetermined values are in column 4 of Appendix C of text F = .](http://images.slideplayer.com/22/6393729/slides/slide_39.jpg "A =.")

40

( F / A,i%,N ) = (P / A,i,N ) ( F / P,i,N ) ( F / A,i%,N ) = F / P,i,N-k ) N k = 1

= (P / A,i,N ) ( F / P,i,N ) ( F / A,i%,N ) = F / P,i,N-k ) N k = 1")

41

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A:

TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A:")

42

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts Finding P given A: Finding present equivalent value given a series of uniform equal receipts

TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts Finding P given A: Finding present equivalent value given a series of uniform equal receipts")

43

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N

TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N")

44

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ]

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ]](http://images.slideplayer.com/22/6393729/slides/slide_44.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ]")

45

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N ) Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N )

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N ) Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N )](http://images.slideplayer.com/22/6393729/slides/slide_45.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N ) Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N )")

46

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N ) –predetermined values are in column 5 of Appendix C of text Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N ) –predetermined values are in column 5 of Appendix C of text

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N ) –predetermined values are in column 5 of Appendix C of text Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N ) –predetermined values are in column 5 of Appendix C of text](http://images.slideplayer.com/22/6393729/slides/slide_46.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N ) –predetermined values are in column 5 of Appendix C of text Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N ) –predetermined values are in column 5 of Appendix C of text")

47

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N ) –predetermined values are in column 5 of Appendix C of text Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N ) –predetermined values are in column 5 of Appendix C of text P = ? 1234567 8 A =

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N ) –predetermined values are in column 5 of Appendix C of text Finding P given A: Finding present equivalent value given a series of uniform equal receipts ( 1 + i ) N - 1 P = A i ( 1 + i ) N –uniform series present worth factor in [ ] –functionally expressed as P = A ( P / A,i%,N ) –predetermined values are in column 5 of Appendix C of text P = .](http://images.slideplayer.com/22/6393729/slides/slide_47.jpg "A =.")

48

( P / A,i%,N ) = P / F,i,k ) N k = 1

= P / F,i,k ) N k = 1")

49

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F:

TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F:")

50

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value Finding A given F: Finding amount A of a uniform series when given the equivalent future value

TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value Finding A given F: Finding amount A of a uniform series when given the equivalent future value")

51

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1

TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1")

52

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ]

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ]](http://images.slideplayer.com/22/6393729/slides/slide_52.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ]")

53

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N )

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N )](http://images.slideplayer.com/22/6393729/slides/slide_53.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N )")

54

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) –predetermined values are in column 6 of Appendix C of text Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) –predetermined values are in column 6 of Appendix C of text

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) –predetermined values are in column 6 of Appendix C of text Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) –predetermined values are in column 6 of Appendix C of text](http://images.slideplayer.com/22/6393729/slides/slide_54.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) –predetermined values are in column 6 of Appendix C of text Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) –predetermined values are in column 6 of Appendix C of text")

55

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) –predetermined values are in column 6 of Appendix C of text Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) –predetermined values are in column 6 of Appendix C of text F = 1234567 8 A =?

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) –predetermined values are in column 6 of Appendix C of text Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) –predetermined values are in column 6 of Appendix C of text F = A =](http://images.slideplayer.com/22/6393729/slides/slide_55.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) –predetermined values are in column 6 of Appendix C of text Finding A given F: Finding amount A of a uniform series when given the equivalent future value i A = F ( 1 + i ) N -1 –sinking fund factor in [ ] –functionally expressed as A = F ( A / F,i%,N ) –predetermined values are in column 6 of Appendix C of text F = A =")

56

( A / F,i%,N ) = 1 / ( F / A,i%,N ) ( A / F,i%,N ) = ( A / P,i%,N ) - i

= 1 / ( F / A,i%,N ) ( A / F,i%,N ) = ( A / P,i%,N ) - i")

57

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P:

TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P:")

58

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value Finding A given P: Finding amount A of a uniform series when given the equivalent present value

TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value Finding A given P: Finding amount A of a uniform series when given the equivalent present value")

59

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1

TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1")

60

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ]

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ]](http://images.slideplayer.com/22/6393729/slides/slide_60.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ]")

61

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N )

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N )](http://images.slideplayer.com/22/6393729/slides/slide_61.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N )")

62

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) –predetermined values are in column 7 of Appendix C of text Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) –predetermined values are in column 7 of Appendix C of text

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) –predetermined values are in column 7 of Appendix C of text Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) –predetermined values are in column 7 of Appendix C of text](http://images.slideplayer.com/22/6393729/slides/slide_62.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) –predetermined values are in column 7 of Appendix C of text Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) –predetermined values are in column 7 of Appendix C of text")

63

RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) –predetermined values are in column 7 of Appendix C of text Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) –predetermined values are in column 7 of Appendix C of text P = 1234567 8 A =?

![RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) –predetermined values are in column 7 of Appendix C of text Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) –predetermined values are in column 7 of Appendix C of text P = A =](http://images.slideplayer.com/22/6393729/slides/slide_63.jpg "RELATING A UNIFORM SERIES (ORDINARY ANNUITY) TO PRESENT AND FUTURE EQUIVALENT VALUES Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) –predetermined values are in column 7 of Appendix C of text Finding A given P: Finding amount A of a uniform series when given the equivalent present value i ( 1+i ) N A = P ( 1 + i ) N -1 –capital recovery factor in [ ] –functionally expressed as A = P ( A / P,i%,N ) –predetermined values are in column 7 of Appendix C of text P = A =")

64

( A / P,i%,N ) = 1 / ( P / A,i%,N )

= 1 / ( P / A,i%,N )")

65

RELATING A UNIFORM SERIES (DEFERRED ANNUITY) TO PRESENT / FUTURE EQUIVALENT VALUES If an annuity is deferred j periods, where j < N And finding P given A for an ordinary annuity is expressed by: P = A ( P / A, i%,N ) This is expressed for a deferred annuity by: A ( P / A, i%,N - j ) at end of period j This is expressed for a deferred annuity by: A ( P / A, i%,N - j ) ( P / F, i%, j ) as of time 0 (time present) If an annuity is deferred j periods, where j < N And finding P given A for an ordinary annuity is expressed by: P = A ( P / A, i%,N ) This is expressed for a deferred annuity by: A ( P / A, i%,N - j ) at end of period j This is expressed for a deferred annuity by: A ( P / A, i%,N - j ) ( P / F, i%, j ) as of time 0 (time present)

TO PRESENT / FUTURE EQUIVALENT VALUES If an annuity is deferred j periods, where j < N And finding P given A for an ordinary annuity is expressed by: P = A ( P / A, i%,N ) This is expressed for a deferred annuity by: A ( P / A, i%,N - j ) at end of period j This is expressed for a deferred annuity by: A ( P / A, i%,N - j ) ( P / F, i%, j ) as of time 0 (time present) If an annuity is deferred j periods, where j < N And finding P given A for an ordinary annuity is expressed by: P = A ( P / A, i%,N ) This is expressed for a deferred annuity by: A ( P / A, i%,N - j ) at end of period j This is expressed for a deferred annuity by: A ( P / A, i%,N - j ) ( P / F, i%, j ) as of time 0 (time present)")

66

EQUIVALENCE CALCULATIONS INVOLVING MULTIPLE INTEREST All compounding of interest takes place once per time period (e.g., a year), and to this point cash flows also occur once per time period. Consider an example where a series of cash outflows occur over a number of years. Consider that the value of the outflows is unique for each of a number (i.e., first three) years. Consider that the value of outflows is the same for the last four years. Find a) the present equivalent expenditure; b) the future equivalent expenditure; and c) the annual equivalent expenditure All compounding of interest takes place once per time period (e.g., a year), and to this point cash flows also occur once per time period. Consider an example where a series of cash outflows occur over a number of years. Consider that the value of the outflows is unique for each of a number (i.e., first three) years. Consider that the value of outflows is the same for the last four years. Find a) the present equivalent expenditure; b) the future equivalent expenditure; and c) the annual equivalent expenditure

years. Consider that the value of outflows is the same for the last four years. Find a) the present equivalent expenditure; b) the future equivalent expenditure; and c) the annual equivalent expenditure All compounding of interest takes place once per time period (e.g., a year), and to this point cash flows also occur once per time period. Consider an example where a series of cash outflows occur over a number of years. Consider that the value of the outflows is unique for each of a number (i.e., first three) years. Consider that the value of outflows is the same for the last four years. Find a) the present equivalent expenditure; b) the future equivalent expenditure; and c) the annual equivalent expenditure.")

67

PRESENT EQUIVALENT EXPENDITURE Use P 0 = F( P / F, i%, N ) for each of the unique years: -- F is a series of unique outflow for year 1 through year 3; -- i is common for each calculation; -- N is the year in which the outflow occurred; -- Multiply the outflow times the associated table value; -- Add the three products together; Use A ( P / A,i%,N - j ) ( P / F, i%, j ) -- deferred annuity -- for the remaining (common outflow) years: -- A is common for years 4 through 7; -- i remains the same; -- N is the final year; -- j is the last year a unique outflow occurred; -- multiply the common outflow value times table values; -- add this to the previous total for the present equivalent expenditure. Use P 0 = F( P / F, i%, N ) for each of the unique years: -- F is a series of unique outflow for year 1 through year 3; -- i is common for each calculation; -- N is the year in which the outflow occurred; -- Multiply the outflow times the associated table value; -- Add the three products together; Use A ( P / A,i%,N - j ) ( P / F, i%, j ) -- deferred annuity -- for the remaining (common outflow) years: -- A is common for years 4 through 7; -- i remains the same; -- N is the final year; -- j is the last year a unique outflow occurred; -- multiply the common outflow value times table values; -- add this to the previous total for the present equivalent expenditure.

for each of the unique years: -- F is a series of unique outflow for year 1 through year 3; -- i is common for each calculation; -- N is the year in which the outflow occurred; -- Multiply the outflow times the associated table value; -- Add the three products together; Use A ( P / A,i%,N - j ) ( P / F, i%, j ) -- deferred annuity -- for the remaining (common outflow) years: -- A is common for years 4 through 7; -- i remains the same; -- N is the final year; -- j is the last year a unique outflow occurred; -- multiply the common outflow value times table values; -- add this to the previous total for the present equivalent expenditure..")

68

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO FUTURE EQUIVALENTS Find F when given G:

69

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO FUTURE EQUIVALENTS Find F when given G: Find the future equivalent value when given the uniform gradient amount Find F when given G: Find the future equivalent value when given the uniform gradient amount

70

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO FUTURE EQUIVALENTS Find F when given G: Find the future equivalent value when given the uniform gradient amount (1+i) N-1 -1 (1+i) N-2 -1 (1+i) 1 -1 F = G + +... + Find F when given G: Find the future equivalent value when given the uniform gradient amount (1+i) N-1 -1 (1+i) N-2 -1 (1+i) 1 -1 F = G + +... + i i i

N-1 -1 (1+i) N-2 -1 (1+i) 1 -1 F = G i i i.")

71

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO FUTURE EQUIVALENTS Find F when given G: Find the future equivalent value when given the uniform gradient amount (1+i) N-1 -1 (1+i) N-2 -1 (1+i) 1 -1 F = G + +... + Functionally represented as (G/ i) (F/A,i%,N) - (NG/ i) Find F when given G: Find the future equivalent value when given the uniform gradient amount (1+i) N-1 -1 (1+i) N-2 -1 (1+i) 1 -1 F = G + +... + Functionally represented as (G/ i) (F/A,i%,N) - (NG/ i) i i i

(F/A,i%,N) - (NG/ i) Find F when given G: Find the future equivalent value when given the uniform gradient amount (1+i) N-1 -1 (1+i) N-2 -1 (1+i) 1 -1 F = G Functionally represented as (G/ i) (F/A,i%,N) - (NG/ i) i i i.")

72

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO FUTURE EQUIVALENTS Find F when given G: Find the future equivalent value when given the uniform gradient amount (1+i) N-1 -1 (1+i) N-2 -1 (1+i) 1 -1 F = G + +... + Functionally represented as (G/ i) (F/A,i%,N) - (NG/ i) Usually more practical to deal with annual and present equivalents, rather than future equivalent values Find F when given G: Find the future equivalent value when given the uniform gradient amount (1+i) N-1 -1 (1+i) N-2 -1 (1+i) 1 -1 F = G + +... + Functionally represented as (G/ i) (F/A,i%,N) - (NG/ i) Usually more practical to deal with annual and present equivalents, rather than future equivalent values i i i

(F/A,i%,N) - (NG/ i) Usually more practical to deal with annual and present equivalents, rather than future equivalent values Find F when given G: Find the future equivalent value when given the uniform gradient amount (1+i) N-1 -1 (1+i) N-2 -1 (1+i) 1 -1 F = G Functionally represented as (G/ i) (F/A,i%,N) - (NG/ i) Usually more practical to deal with annual and present equivalents, rather than future equivalent values i i i.")

73

Cash Flow Diagram for a Uniform Gradient Increasing by G Dollars per period 1234N-2N-1N G 2G 3G (N-3)G (N-2)G (N-1)G i = effective interest rate per period End of Period

G (N-2)G (N-1)G i = effective interest rate per period End of Period")

74

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find A when given G:

75

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find A when given G: Find the annual equivalent value when given the uniform gradient amount Find A when given G: Find the annual equivalent value when given the uniform gradient amount

76

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find A when given G: Find the annual equivalent value when given the uniform gradient amount 1 N A = G - i(1 + i ) N - 1 Find A when given G: Find the annual equivalent value when given the uniform gradient amount 1 N A = G - i(1 + i ) N - 1

N - 1 Find A when given G: Find the annual equivalent value when given the uniform gradient amount 1 N A = G - i(1 + i ) N - 1")

77

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find A when given G: Find the annual equivalent value when given the uniform gradient amount 1 N A = G - i(1 + i ) N - 1 Functionally represented as A = G ( A / G, i%,N ) Find A when given G: Find the annual equivalent value when given the uniform gradient amount 1 N A = G - i(1 + i ) N - 1 Functionally represented as A = G ( A / G, i%,N )

N - 1 Functionally represented as A = G ( A / G, i%,N ) Find A when given G: Find the annual equivalent value when given the uniform gradient amount 1 N A = G - i(1 + i ) N - 1 Functionally represented as A = G ( A / G, i%,N )")

78

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find A when given G: Find the annual equivalent value when given the uniform gradient amount 1 N A = G - i(1 + i ) N - 1 Functionally represented as A = G ( A / G, i%,N ) The value shown in [ ] is the gradient to uniform series conversion factor and is presented in column 9 of Appendix C (represented in the above parenthetical expression). Find A when given G: Find the annual equivalent value when given the uniform gradient amount 1 N A = G - i(1 + i ) N - 1 Functionally represented as A = G ( A / G, i%,N ) The value shown in [ ] is the gradient to uniform series conversion factor and is presented in column 9 of Appendix C (represented in the above parenthetical expression).

![RELATING A UNIFORM GRADIENT OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find A when given G: Find the annual equivalent value when given the uniform gradient amount 1 N A = G - i(1 + i ) N - 1 Functionally represented as A = G ( A / G, i%,N ) The value shown in [ ] is the gradient to uniform series conversion factor and is presented in column 9 of Appendix C (represented in the above parenthetical expression).](http://images.slideplayer.com/22/6393729/slides/slide_78.jpg "Find A when given G: Find the annual equivalent value when given the uniform gradient amount 1 N A = G - i(1 + i ) N - 1 Functionally represented as A = G ( A / G, i%,N ) The value shown in [ ] is the gradient to uniform series conversion factor and is presented in column 9 of Appendix C (represented in the above parenthetical expression)..")

79

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find P when given G:

80

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find P when given G: Find the present equivalent value when given the uniform gradient amount Find P when given G: Find the present equivalent value when given the uniform gradient amount

81

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find P when given G: Find the present equivalent value when given the uniform gradient amount 1(1 + i ) N -1N P = G- ii (1 + i ) N (1 + i ) N Find P when given G: Find the present equivalent value when given the uniform gradient amount 1(1 + i ) N -1N P = G- ii (1 + i ) N (1 + i ) N

N -1N P = G- ii (1 + i ) N (1 + i ) N Find P when given G: Find the present equivalent value when given the uniform gradient amount 1(1 + i ) N -1N P = G- ii (1 + i ) N (1 + i ) N")

82

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find P when given G: Find the present equivalent value when given the uniform gradient amount 1(1 + i ) N -1N P = G- ii (1 + i ) N (1 + i ) N Functionally represented as P = G ( P / G, i%,N ) Find P when given G: Find the present equivalent value when given the uniform gradient amount 1(1 + i ) N -1N P = G- ii (1 + i ) N (1 + i ) N Functionally represented as P = G ( P / G, i%,N )

N -1N P = G- ii (1 + i ) N (1 + i ) N Functionally represented as P = G ( P / G, i%,N ) Find P when given G: Find the present equivalent value when given the uniform gradient amount 1(1 + i ) N -1N P = G- ii (1 + i ) N (1 + i ) N Functionally represented as P = G ( P / G, i%,N )")

83

RELATING A UNIFORM GRADIENT OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find P when given G: Find the present equivalent value when given the uniform gradient amount 1(1 + i ) N -1N P = G- ii (1 + i ) N (1 + i ) N Functionally represented as P = G ( P / G, i%,N ) The value shown in{ } is the gradient to present equivalent conversion factor and is presented in column 8 of Appendix C (represented in the above parenthetical expression). Find P when given G: Find the present equivalent value when given the uniform gradient amount 1(1 + i ) N -1N P = G- ii (1 + i ) N (1 + i ) N Functionally represented as P = G ( P / G, i%,N ) The value shown in{ } is the gradient to present equivalent conversion factor and is presented in column 8 of Appendix C (represented in the above parenthetical expression).

N -1N P = G- ii (1 + i ) N (1 + i ) N Functionally represented as P = G ( P / G, i%,N ) The value shown in{ } is the gradient to present equivalent conversion factor and is presented in column 8 of Appendix C (represented in the above parenthetical expression)..")

84

RELATING GE0METRIC SEQUENCE OF CASH FLOWS TO PRESENT AND ANNUAL EQUIVALENTS Projected cash flow patterns changing at an average rate of f each period;

85

RELATING GE0METRIC SEQUENCE OF CASH FLOWS TO PRESENT AND ANNUAL EQUIVALENTS Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series;

86

RELATING GE0METRIC SEQUENCE OF CASH FLOWS TO PRESENT AND ANNUAL EQUIVALENTS Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1

87

RELATING GE0METRIC SEQUENCE OF CASH FLOWS TO PRESENT AND ANNUAL EQUIVALENTS Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N

( 1 +f ),2 < k < N Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N")

88

RELATING GE0METRIC SEQUENCE OF CASH FLOWS TO PRESENT AND ANNUAL EQUIVALENTS Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1 Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1

( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1 Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1")

89

RELATING GE0METRIC SEQUENCE OF CASH FLOWS TO PRESENT AND ANNUAL EQUIVALENTS Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1 f = (A k - A k-1 ) / A k-1 Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1 f = (A k - A k-1 ) / A k-1

( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1 f = (A k - A k-1 ) / A k-1 Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1 f = (A k - A k-1 ) / A k-1")

90

RELATING GE0METRIC SEQUENCE OF CASH FLOWS TO PRESENT AND ANNUAL EQUIVALENTS Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1 f = (A k - A k-1 ) / A k-1 convenience rate = i cr = [ ( 1 + i ) / ( 1 + f ) ] - 1 = ( i - f ) / ( 1 + f ) Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1 f = (A k - A k-1 ) / A k-1 convenience rate = i cr = [ ( 1 + i ) / ( 1 + f ) ] - 1 = ( i - f ) / ( 1 + f )

![RELATING GE0METRIC SEQUENCE OF CASH FLOWS TO PRESENT AND ANNUAL EQUIVALENTS Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1 f = (A k - A k-1 ) / A k-1 convenience rate = i cr = [ ( 1 + i ) / ( 1 + f ) ] - 1 = ( i - f ) / ( 1 + f ) Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1 f = (A k - A k-1 ) / A k-1 convenience rate = i cr = [ ( 1 + i ) / ( 1 + f ) ] - 1 = ( i - f ) / ( 1 + f )](http://images.slideplayer.com/22/6393729/slides/slide_90.jpg "RELATING GE0METRIC SEQUENCE OF CASH FLOWS TO PRESENT AND ANNUAL EQUIVALENTS Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1 f = (A k - A k-1 ) / A k-1 convenience rate = i cr = [ ( 1 + i ) / ( 1 + f ) ] - 1 = ( i - f ) / ( 1 + f ) Projected cash flow patterns changing at an average rate of f each period; Resultant end-of-period cash-flow pattern is referred to as a geometric gradient series; A 1 is cash flow at end of period 1 A k = (A k-1 ) ( 1 +f ),2 < k < N A N = A 1 ( 1 + f ) N-1 f = (A k - A k-1 ) / A k-1 convenience rate = i cr = [ ( 1 + i ) / ( 1 + f ) ] - 1 = ( i - f ) / ( 1 + f )")

91

01234N A1A1 A 2 =A 1 (1+f ) A 3 =A 1 (1+f ) 2 A N =A 1 (1+f ) N - 1 End of Period Cash-flow diagram for a Geometric Sequence of Cash Flows

A 3 =A 1 (1+f ) 2 A N =A 1 (1+f ) N - 1 End of Period Cash-flow diagram for a Geometric Sequence of Cash Flows")

92

RELATING A GEOMETRIC SEQUENCE OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find P when given A:

93

RELATING A GEOMETRIC SEQUENCE OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find P when given A: Find the present equivalent value when given the annual equivalent value ( i = f )and ( i cr = 0 ) Find P when given A: Find the present equivalent value when given the annual equivalent value ( i = f )and ( i cr = 0 )

and ( i cr = 0 ) Find P when given A: Find the present equivalent value when given the annual equivalent value ( i = f )and ( i cr = 0 )")

94

RELATING A GEOMETRIC SEQUENCE OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find P when given A: Find the present equivalent value when given the annual equivalent value ( i = f )and ( i cr = 0 ) A 1 P = ( P / A, i CR %, N ) ( 1 + f ) Find P when given A: Find the present equivalent value when given the annual equivalent value ( i = f )and ( i cr = 0 ) A 1 P = ( P / A, i CR %, N ) ( 1 + f )

and ( i cr = 0 ) A 1 P = ( P / A, i CR %, N ) ( 1 + f ) Find P when given A: Find the present equivalent value when given the annual equivalent value ( i = f )and ( i cr = 0 ) A 1 P = ( P / A, i CR %, N ) ( 1 + f )")

95

RELATING A GEOMETRIC SEQUENCE OF CASH FLOWS TO ANNUAL AND PRESENT EQUIVALENTS Find P when given A: Find the present equivalent value when given the annual equivalent value ( i = f )and ( i cr = 0 ) A 1 P = ( P / A, i CR %, N ) 1 + f Functionally represented as A = P (A / P, i%,N ) Find P when given A: Find the present equivalent value when given the annual equivalent value ( i = f )and ( i cr = 0 ) A 1 P = ( P / A, i CR %, N ) 1 + f Functionally represented as A = P (A / P, i%,N )

and ( i cr = 0 ) A 1 P = ( P / A, i CR %, N ) 1 + f Functionally represented as A = P (A / P, i%,N ) Find P when given A: Find the present equivalent value when given the annual equivalent value ( i = f )and ( i cr = 0 ) A 1 P = ( P / A, i CR %, N ) 1 + f Functionally represented as A = P (A / P, i%,N )")

96