Download presentation

Presentation is loading. Please wait.

1

Week-3 Into to Interest Rates Money and Banking Econ 311 Tuesdays 7 - 9:45 Instructor: Thomas L. Thomas

2

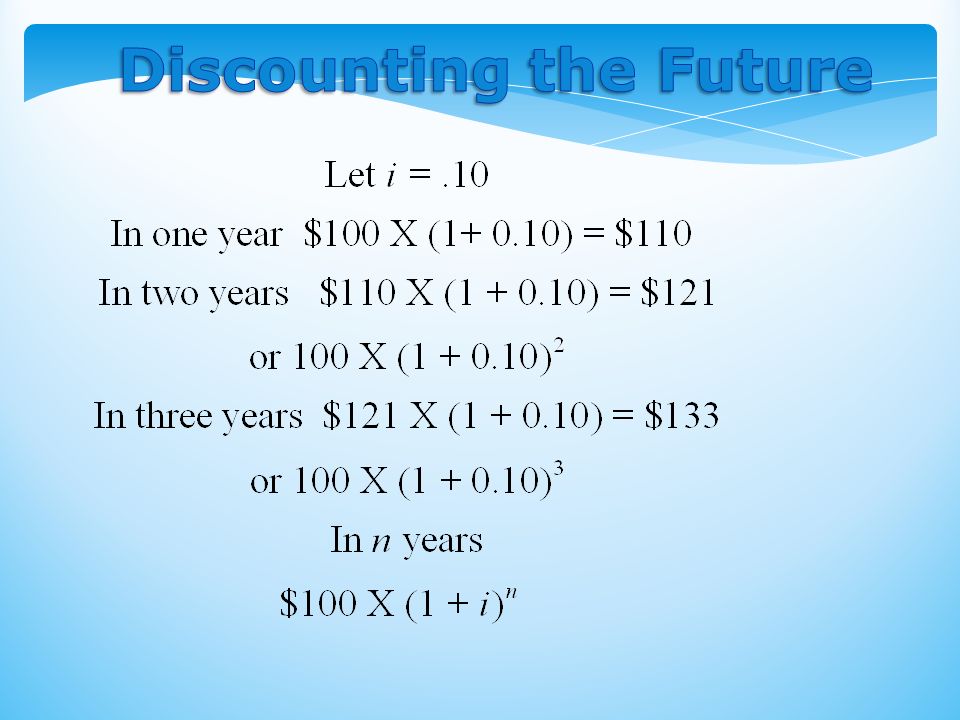

o Present Value: o A dollar paid to you one year from now is less valuable than a dollar paid to you today o Why? o A dollar deposited today can earn interest and become $1 x (1+i) one year from today.

one year from today..")

5

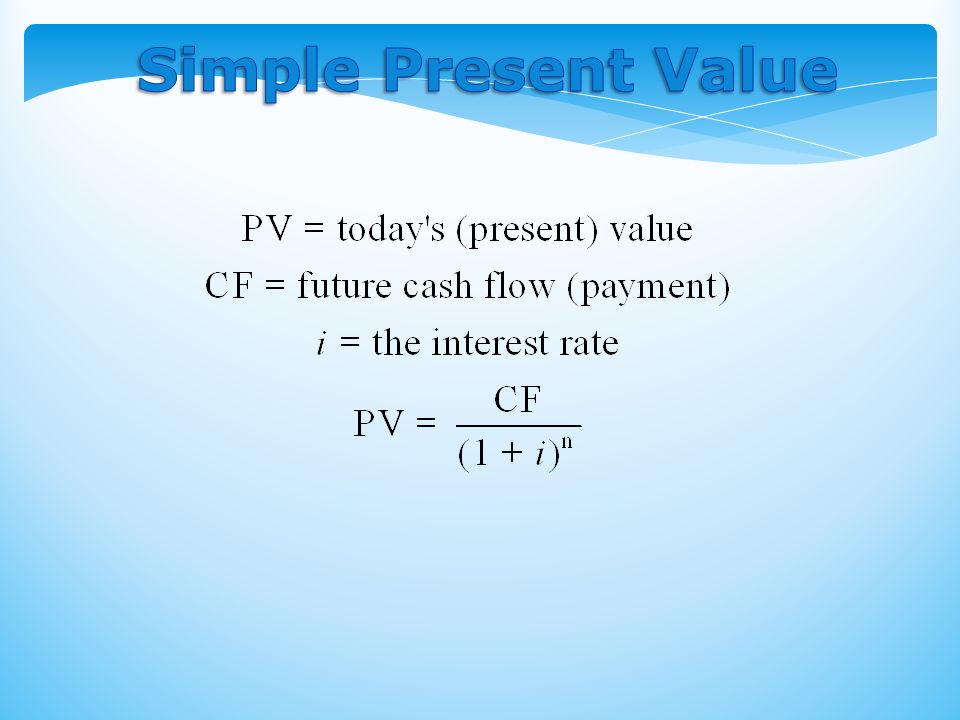

$100 Year01 PV100 2 $100 n 100/(1+i)100/(1+i) 2 100/(1+i) n Cannot directly compare payments scheduled in different points in the time line

100/(1+i) 2 100/(1+i) n Cannot directly compare payments scheduled in different points in the time line")

6

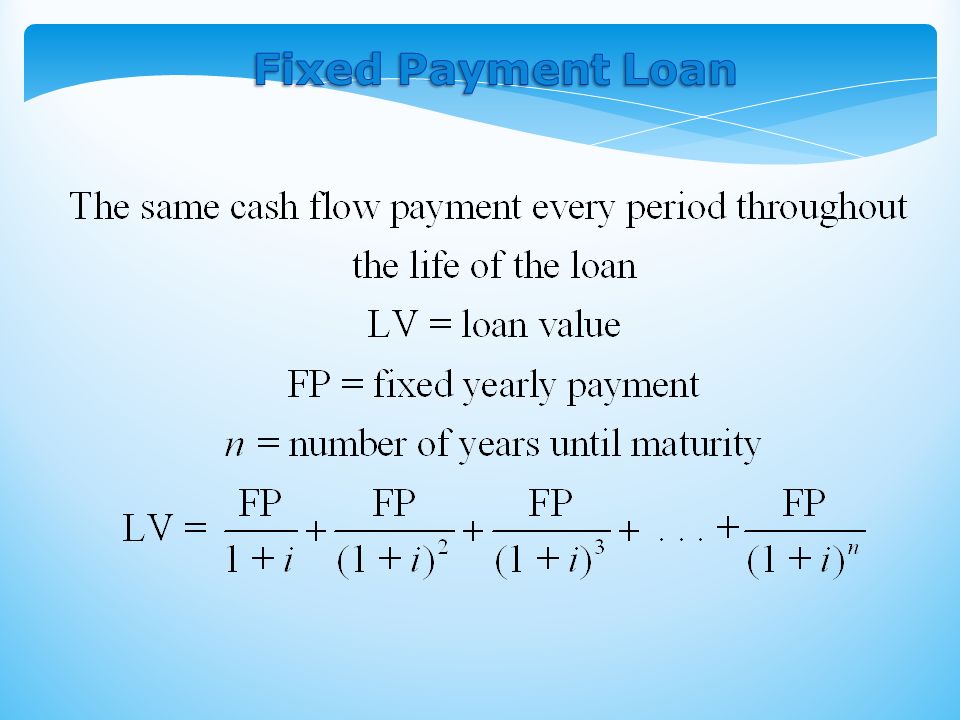

o Simple Loan o Fixed Payment Loan o Coupon Bond o Discount Bond

7

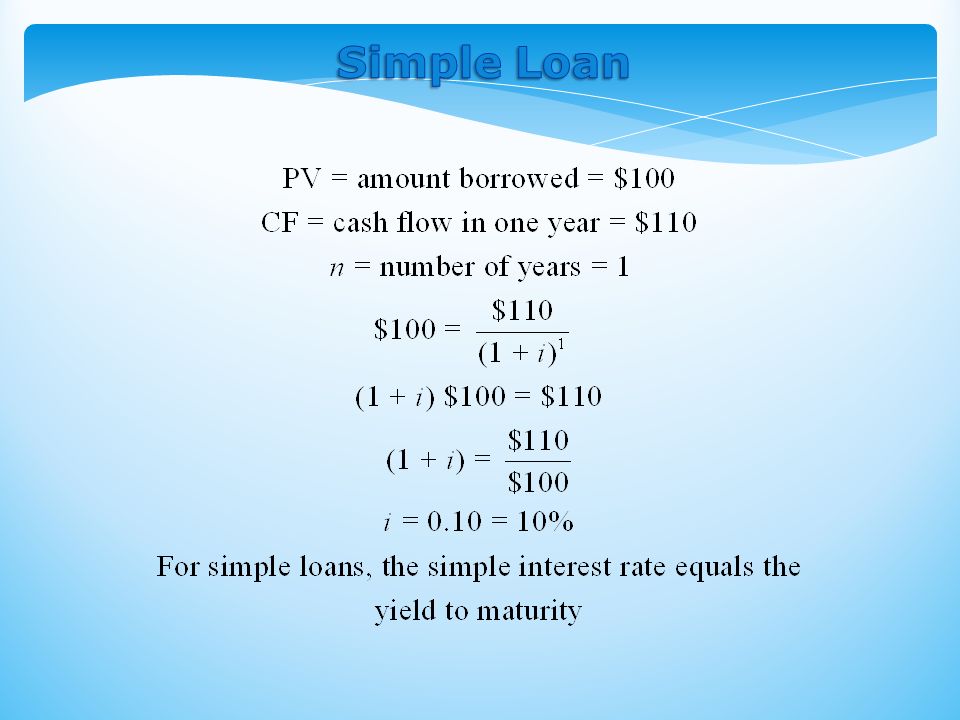

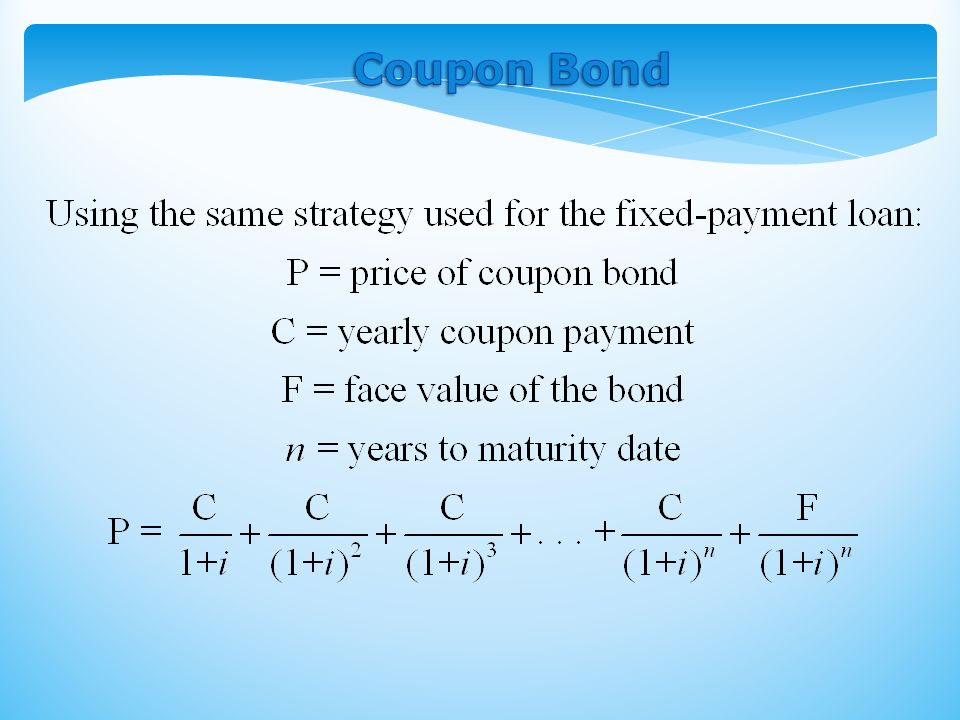

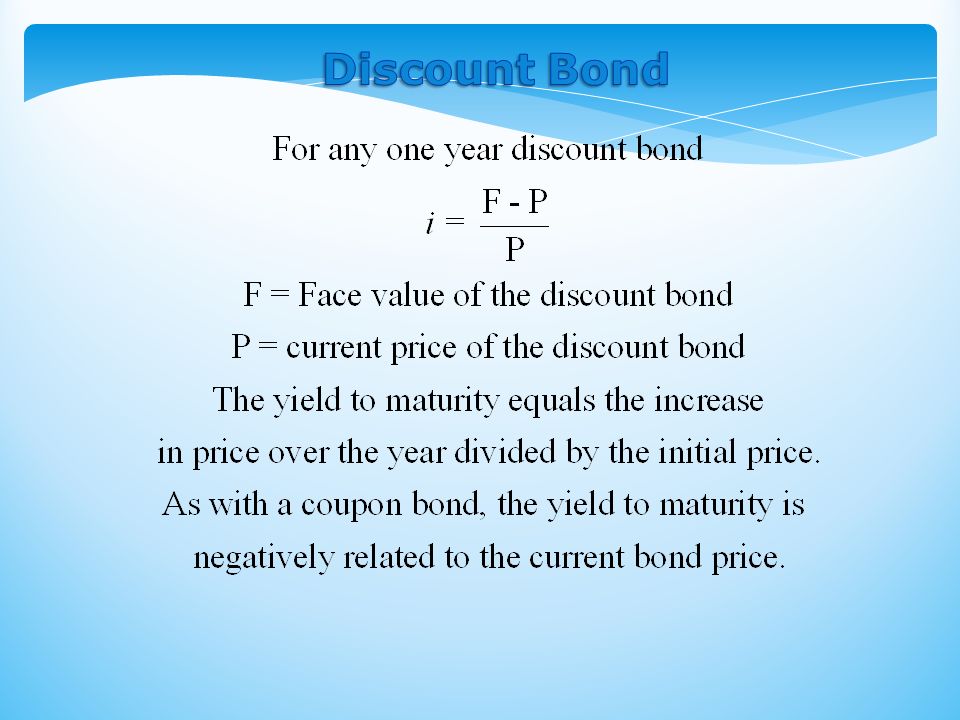

o The interest rate that equates the present value of cash flow payments received from a debt instrument with its value today

11

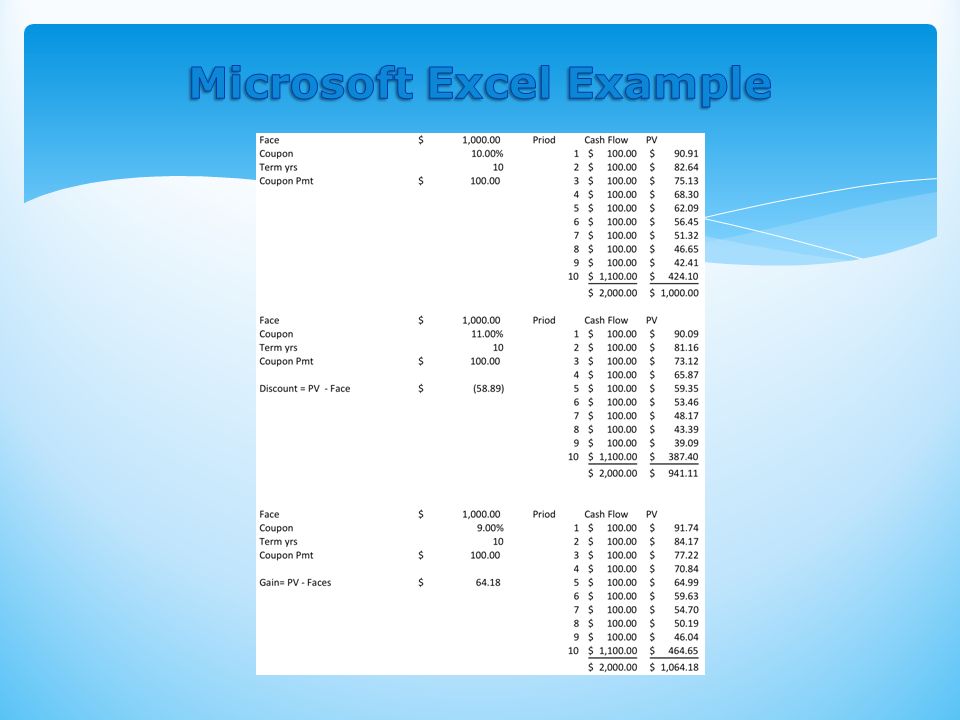

o When the coupon bond is priced at its face value, the yield to maturity equals the coupon rate o The price of a coupon bond and the yield to maturity are negatively related o The yield to maturity is greater than the coupon rate when the bond price is below its face value

13

o A bond with no maturity date that does not repay principal but pays fixed coupon payments forever For coupon bonds, this equation gives the current yield, an easy to calculate approximation to the yield to maturity

15

Rate of Return :

16

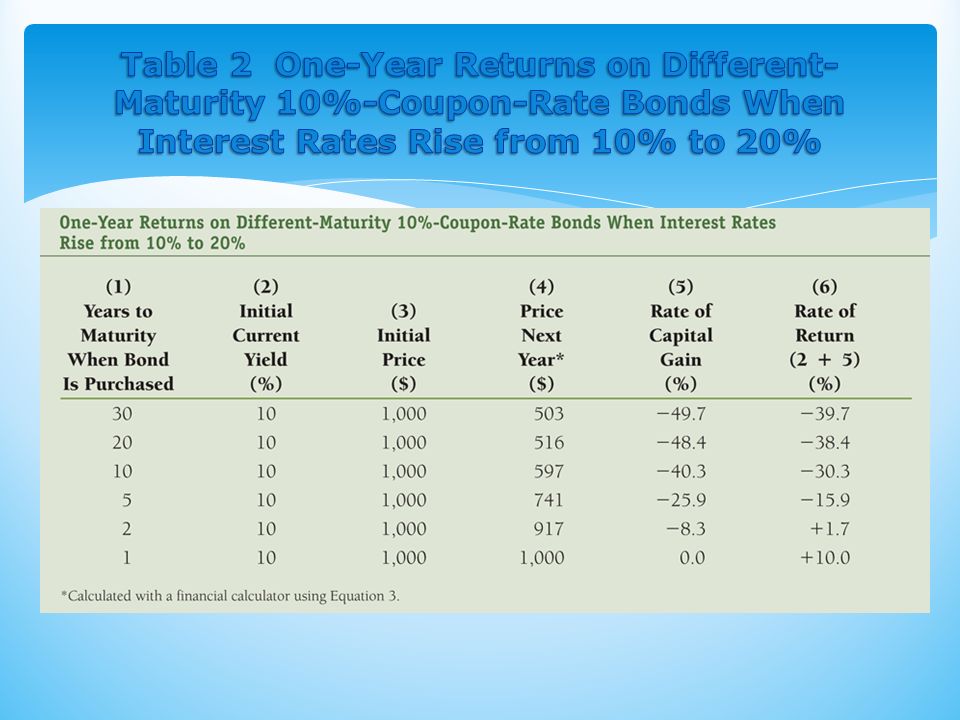

o The return equals the yield to maturity only if the holding period equals the time to maturity o A rise in interest rates is associated with a fall in bond prices, resulting in a capital loss if time to maturity is longer than the holding period o The more distant a bond’s maturity, the greater the size of the percentage price change associated with an interest-rate change (also referred to as duration)

")

18

o Prices and returns for long-term bonds are more volatile than those for shorter-term bonds o There is no interest-rate risk for any bond whose time to maturity matches the holding period

19

o Duration - is the weighted average time over which he cash flows form an investment are expected, where the weights are the relative present values of the cash flows. o Focusing on maturity ignore the fact that some cash benefits are received before maturity (can be reinvested) and the benefits may be substantial.

and the benefits may be substantial..")

20

o Higher yields lead to lower durations. As the yield increases the present value of the distant cash flows gets exponentially smaller thus the weight given to distant time periods in the numerator get smaller lowering the duration.

21

o The duration of any instrument is positively related to maturity, except for maturities in excess of 50 years. The duration of a bond increases as yield (coupon) increases.

increases..")

22

o Why is this important? The answer: for a given change in market yields, the percentage change in an asset’s price (PV) are proportional to the asset’s duration. o Hence longer duration instruments are subject to greater price changes (exhibit greater price elasticity). o This is expressed by the following formula: -Duration × [i ÷(1+i)] Examples:

are proportional to the asset’s duration. o Hence longer duration instruments are subject to greater price changes (exhibit greater price elasticity). o This is expressed by the following formula: -Duration × [i ÷(1+i)] Examples:.")

23

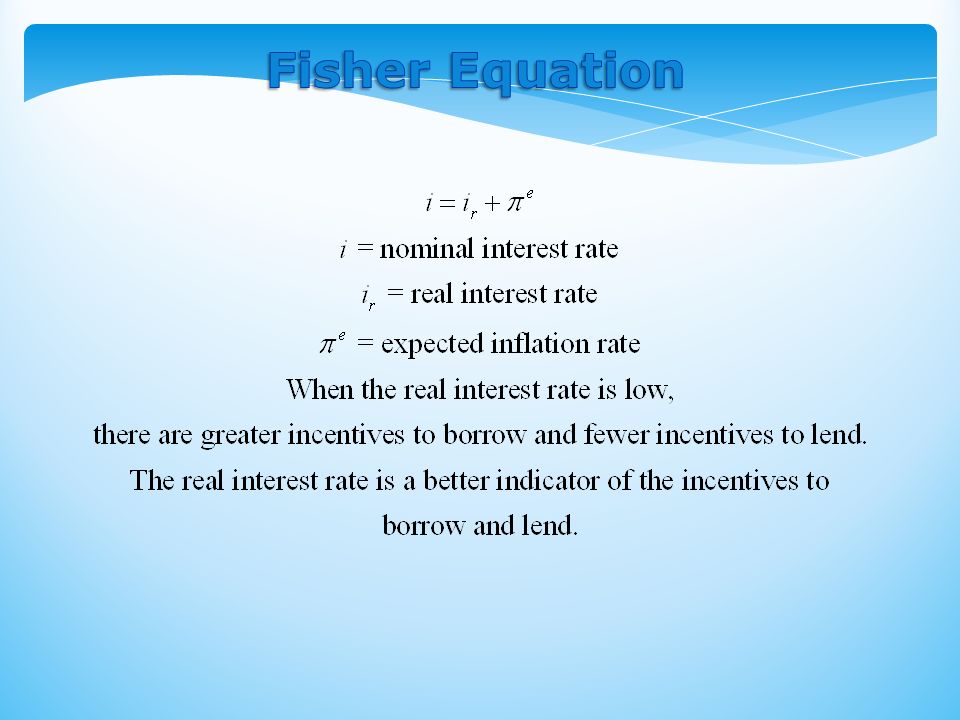

o Nominal interest rate makes no allowance for inflation o Real interest rate is adjusted for changes in price level so it more accurately reflects the cost of borrowing o Ex ante real interest rate is adjusted for expected changes in the price level o Ex post real interest rate is adjusted for actual changes in the price level

25

Sources: Nominal rates from www.federalreserve.gov/releases/H15 and inflation from ftp://ftp.bis.gov/special.requests/cpi/cpia.txt. The real rate is constructed using the procedure outlined in Frederic S. Mishkin, “The Real Interest Rate: An Empirical Investigation,” Carnegie-Rochester Conference Series on Public Policy 15 (1981): 151–200. This procedure involves estimating expected inflation as a function of past interest rates, inflation, and time trends and then subtracting the expected inflation measure from the nominal interest rate.ftp://ftp.bis.gov/special.requests/cpi/

: 151–200. This procedure involves estimating expected inflation as a function of past interest rates, inflation, and time trends and then subtracting the expected inflation measure from the nominal interest rate.ftp://ftp.bis.gov/special.requests/cpi/.")

26

Determinants of Asset Demand Wealth: the total resources owned by the individual, including all assets Expected Return: the return expected over the next period on one asset relative to alternative assets Risk: the degree of uncertainty associated with the return on one asset relative to alternative assets Liquidity: the ease and speed with which an asset can be turned into cash relative to alternative assets

27

Theory of Portfolio Choice Holding all other factors constant: 1.The quantity demanded of an asset is positively related to wealth 2.The quantity demanded of an asset is positively related to its expected return relative to alternative assets 3.The quantity demanded of an asset is negatively related to the risk of its returns relative to alternative assets 4.The quantity demanded of an asset is positively related to its liquidity relative to alternative assets

28

Supply and Demand in the Bond Market At lower prices (higher interest rates), ceteris paribus, the quantity demanded of bonds is higher: an inverse relationship At lower prices (higher interest rates), ceteris paribus, the quantity supplied of bonds is lower: a positive relationship

, ceteris paribus, the quantity demanded of bonds is higher: an inverse relationship At lower prices (higher interest rates), ceteris paribus, the quantity supplied of bonds is lower: a positive relationship")

29

Supply and Demand for Bonds

30

Changes in Equilibrium Interest Rates Shifts in the demand for bonds: Wealth: in an expansion with growing wealth, the demand curve for bonds shifts to the right Expected Returns: higher expected interest rates in the future lower the expected return for long-term bonds, shifting the demand curve to the left Expected Inflation: an increase in the expected rate of inflations lowers the expected return for bonds, causing the demand curve to shift to the left Risk: an increase in the riskiness of bonds causes the demand curve to shift to the left Liquidity: increased liquidity of bonds results in the demand curve shifting right

31

Factors That Shift the Demand Curve for Bonds

32

Shifts in the Supply of Bonds Expected profitability of investment opportunities: in an expansion, the supply curve shifts to the right Expected inflation: an increase in expected inflation shifts the supply curve for bonds to the right Government budget: increased budget deficits shift the supply curve to the right

33

Factors That Shift the Supply of Bonds

Similar presentations