Download presentation

Presentation is loading. Please wait.

1

A Model for Lowering Inter-Annual Revenue Variability for the Cotton Chain in WCA Countries by Jean Cordier Professor, Agrocampus Rennes ITF CRM annual meeting, Pretoria, May 16, 2006 A model developed with the support of the French Foreign Ministry and the Agence Française de Développement (AFD)

")

2

–Introduction : the « producer » problem –The model and its assumptions –Results –Advantages and limits ITF CRM annual meeting, TUT, Pretoria, May 16, 2006 A Model for Lowering Inter-Annual Revenue Variability for the Cotton Chain in WCA Countries

3

INTRODUCTION : THE « PRODUCER* » PROBLEM Reference market price F t FOB price (basis = 50) … Revenue = P.Q decrease increase Cost of production FtFt F t - 50 * « Producer » = ginner + farmer - Risk concern of the producer : price and quantity - Risk concern of the ginner : quantity and price f(relationship P - G) Risk on revenue

… Revenue = P.Q decrease increase Cost of production FtFt F t - 50 * « Producer » = ginner + farmer - Risk concern of the producer : price and quantity - Risk concern of the ginner : quantity and price f(relationship P - G) Risk on revenue")

4

INTRODUCTION : THE « PRODUCER » PROBLEM Risk perception : - Revenue variability … σ - Value at Risk : Prob 5 % Revenue(t) < 174 F.CFA Impact on : - Short Term invest. choices - Long Term invest. choices Impact on chain competitivity σ

5

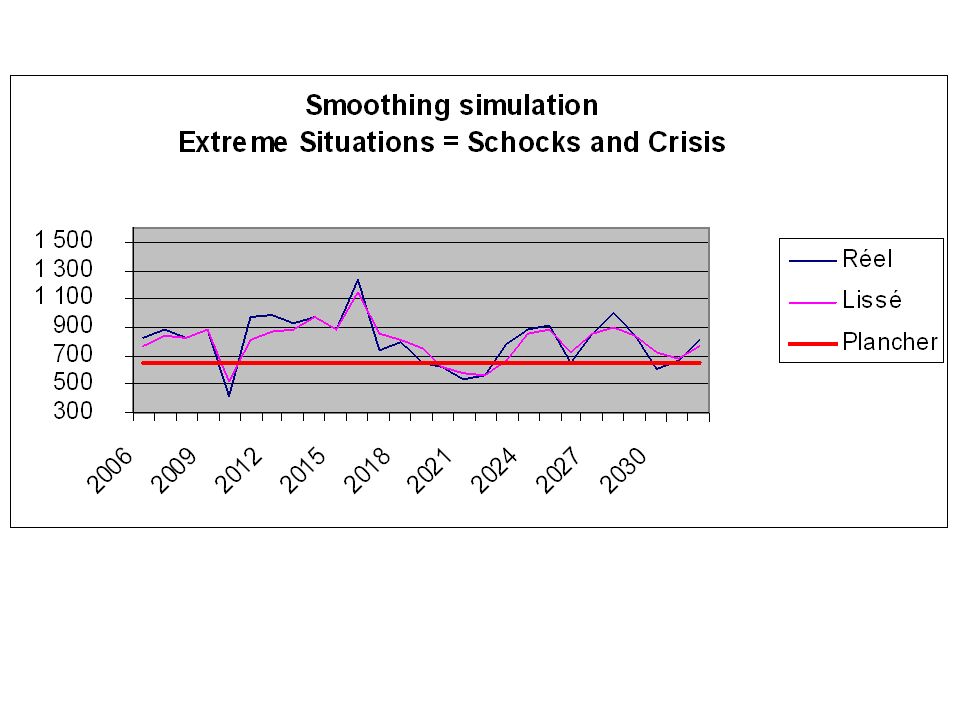

ShockCrisis INTRODUCTION : THE « PRODUCER » PROBLEM Productivity gains In a competitive market, price is fluctuating through time above and below cost of production

6

THE « PRODUCER » PROBLEM AND ITS « ANSWER » 700 Reference market price F t 650 FOB price (basis = 50) And with the benefit of a price lift With a floor price decrease increase Cost of production FtFt F t - 50 Being profitable

And with the benefit of a price lift With a floor price decrease increase Cost of production FtFt F t - 50 Being profitable")

7

OBJECTIVE OF THE MODEL 1.Reduce the revenue variability of the global Cotton Chain in WCA countries oDirectly from price risk management oIndirectly from cultivated surface management o… nothing, to the present time, on crop yield/weather risk management 2.Improve the VaR(5%) of the cotton producer 3.Share the residual risk between ginners and producers

of the cotton producer 3.Share the residual risk between ginners and producers")

8

CONTEXT OF THE MODEL = WCA COUNTRIES Unicity of farmer cotton price through space Unicity of price through time (within a crop year) March(t) Posted Price for Oct-November delivery t Posted price payment at delivery (Oct-Nov) and price bonus at the end of the crop year Organisation of (most) WCA cotton chains

March(t) Posted Price for Oct-November delivery t Posted price payment at delivery (Oct-Nov) and price bonus at the end of the crop year Organisation of (most) WCA cotton chains")

9

CONTEXT OF THE MODEL = WCA COUNTRIES - A fixed exchange rate EUR/F.CFA - A devaluation between EUR/F.CFA in 1994

10

THE PROPOSED MODEL AS A SECOND BEST Reference market price F t FOB price (basis = 50) decrease increase Cost of production

decrease increase Cost of production")

11

THE MODEL 1.Use of reference markets (NYBOT/Cotlook A and exchange rate USD/EUR to define a « fair » CIF-FCFA reference price 2.Define the basis B t for eliciting the WCA FOB-FCFA price B t = transportation cost minus quality premium 3. Design « price layers » with respect to probability of occurrence →Layer A : Risk retention layer Prob(Layer A) ≈ 90 % –Layer B : Market instrum. layer Prob(Layer A) ≈ 10 % –Layer C : Market failure layer Prob(Layer A) ≈ 1-5 % 4.Design tools matching each layer with portfolio consistency and governance potential 5.Define a formula pricing for sharing cotton value between ginners and producers

≈ 90 % –Layer B : Market instrum. layer Prob(Layer A) ≈ 10 % –Layer C : Market failure layer Prob(Layer A) ≈ 1-5 % 4.Design tools matching each layer with portfolio consistency and governance potential 5.Define a formula pricing for sharing cotton value between ginners and producers.")

12

THE PROPOSED MODEL Reference market price F t FOB price (basis = 50) decrease increase Cost of production A BC

decrease increase Cost of production A BC")

13

TOOLS ORGANIZATION IN THE MODEL « Risk retention layer » = Layer A Intra-annual smoothing : selling diversification using futures and forward contracts (private basis) Inter-annual smoothing : price and revenue smoothing using a Buffer Fund and a Withdrawal Right (private professional basis) « Market insurance layer » = Layer B Risk transfer to market : price derivative contract (« bear put spread ») « Market failure layer » = Layer C External support : local covered eventually by international Governance of crisis (early signals, crisis procedure implementation)

Inter-annual smoothing : price and revenue smoothing using a Buffer Fund and a Withdrawal Right (private professional basis) « Market insurance layer » = Layer B Risk transfer to market : price derivative contract (« bear put spread ») « Market failure layer » = Layer C External support : local covered eventually by international Governance of crisis (early signals, crisis procedure implementation)")

14

ASSUMPTIONS OF MODEL SIMULATION FOR BURKINA FASO Lognormal price distribution for the world cotton price in cts/lb (NYBOT or Cotlook A) LN(St) has a normal distribution : N(0 ; 0,20) Normal distribution for the exchange rate USD/EURO : N(1,15 ; 0,22) Normal distribution for farm cotton yield : N(1063 ; 113) Normal distribution for cultivated area : N(700000 ; 70000) No current distribution on FOB-to-CIF cost or quality premium

LN(St) has a normal distribution : N(0 ; 0,20) Normal distribution for the exchange rate USD/EURO : N(1,15 ; 0,22) Normal distribution for farm cotton yield : N(1063 ; 113) Normal distribution for cultivated area : N( ; 70000) No current distribution on FOB-to-CIF cost or quality premium")

15

Moving Average smoothing

16

PARAMETRIZATION TESTED Pivot price calculated using first order exponential smoothing (4 years and α = 0,7) Price layers : A > 700, 600 > B > 700 and C < 600 Upper bound = 110 % of pivot price Lower bound = 90 % of pivot price Percentage of surplus given to the Buffer Fund (BF) = 100 % Maximum size of the Buffer Fund = 15 % of pivot price Maximum size of the Withdrawal Right (WR) = 15 % of pivot price Formula for sharing cotton FOB value between the ginner and the producer : Ginner margin : M = 200 + 0,1*P Producer price : P Prod. = (P FOB – M)* 0,42

* 0,42.")

17

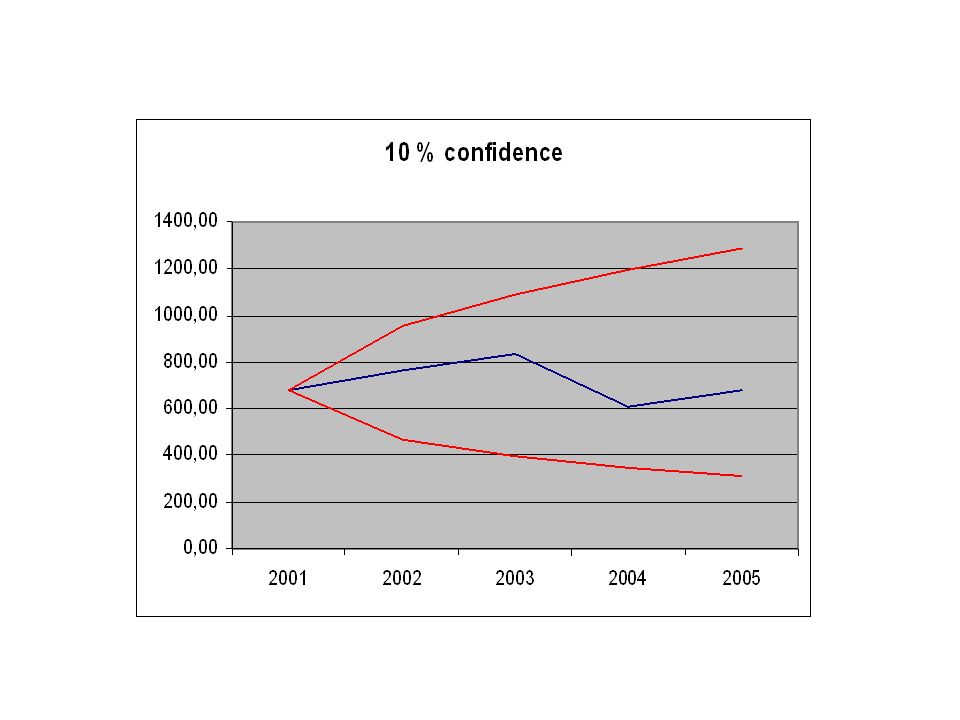

THE BUFFER FUND « AUGMENTED » WITH WITHDRAWAL RIGHT Example of simulation :

18

Current situation Impact of the model Example of simulation :

20

Crise Shock

21

RESULTS OF MONTE CARLO SIMULATION Robust model under current hypothesis (Monte Carlo simulation) Risk decrease for WCA cotton chains –35-40 % decrease of the coeff. of variation of the producer price –30-35 % decrease in standard deviation of the producer price Value at Risk (5%) improvement : 20-25 % Use of Layer C : 3 to 5 % for an average of 37 MM F.CFA (Burkina Faso – 700.000 ha), 1 or 2 times every 30 years (37 or 74 MM F.CFA)

improvement : % Use of Layer C : 3 to 5 % for an average of 37 MM F.CFA (Burkina Faso – ha), 1 or 2 times every 30 years (37 or 74 MM F.CFA).")

22

MODEL ADVANTAGES Effective risk reduction for WCA cotton chains VaR(5%) improvement Non-distorting mechanism « clear principles » and parametrization to reach local objectives Non manipulable therefore « sustainable » Linked to « market » through the use of market signals (exponential smoothing) and instruments (futures-forward, options) Cultural acceptability in merging « buffer funds » and « market instruments » therefore « locally acceptable » … in addition to parametrization

improvement Non-distorting mechanism « clear principles » and parametrization to reach local objectives Non manipulable therefore « sustainable » Linked to « market » through the use of market signals (exponential smoothing) and instruments (futures-forward, options) Cultural acceptability in merging « buffer funds » and « market instruments » therefore « locally acceptable » … in addition to parametrization")

23

MODEL LIMITS Jumps are not considered (FCFA devaluation, strong production cost changes – i.e. GMO – strong cotton area increase) … therefore additional « governance » mechanisms are required to handle jumps consequences Requirement of a national agreement for sharing the world cotton value and risk in between ginners and producers (formula margin and productivity targets) Unknown derivative market liquidity, inducing transaction costs on the knockout option through market intermediaries (banks, international trading firms, specialized intermediaries) Requirement of an agreement between the local Cotton Chain (Interprofession) and the Government for « Layer C management »

… therefore additional « governance » mechanisms are required to handle jumps consequences Requirement of a national agreement for sharing the world cotton value and risk in between ginners and producers (formula margin and productivity targets) Unknown derivative market liquidity, inducing transaction costs on the knockout option through market intermediaries (banks, international trading firms, specialized intermediaries) Requirement of an agreement between the local Cotton Chain (Interprofession) and the Government for « Layer C management ».")

24

… IMPLEMENTATION ISSUES Need to move from current national situations (objective and also constraint of pilot tests) Set theoretical and practical layers limits (A, B and C) Premium issue (perceived cost/benefit, how much, flexible/fixed) A need for normative costs (ginners) Adaptation to national ginners structure (one or several ginners) Institutional, legal, initial endowments issues THANKS FOR YOUR ATTENTION ITF CRM annual meeting, Pretoria, May 16, 2006

Set theoretical and practical layers limits (A, B and C) Premium issue (perceived cost/benefit, how much, flexible/fixed) A need for normative costs (ginners) Adaptation to national ginners structure (one or several ginners) Institutional, legal, initial endowments issues THANKS FOR YOUR ATTENTION ITF CRM annual meeting, Pretoria, May 16, 2006")

25

Besoin d’un « plan marketing » et d’un suivi Plan MKG : Fondement du suivi

26

Compatibilité des aides par rapport à l’O.M.C. Notion de choc et de crise Amélioration possible de la règle de « catastrophe naturelle » telle que rédigée en annexe 2 – paragraphe 7 de l’accord de Marrakech - Autor. OMC - Aide prévue

Similar presentations

would prefer to hedge their.>")

and borrowers.>")

Rationale and Lessons learnt Artur Runge-Metzger Head of International Climate Negotiations, European Commission.>")