Download presentation

Presentation is loading. Please wait.

1

C HAPTER 9 CONTINUED : HEALTH CARE

2

IS THERE A WAY FOR PRIVATE MARKETS TO DEAL WITH ASYMMETRIC INFORMATION WITHOUT GOVERNMENT ? Use of “ experience ratings ” can reduce or eliminate problems associated with asymmetric information. Experience rating Commonly done for life insurance where a battery of blood tests must be undertaken in addition to questionnaire regarding use of tobacco, alcohol, etc. Experience ratings are common practice in auto insurance.

3

P ROBLEM WITH HEALTH CARE AND EXPERIENCE RATINGS Improving efficiency by reducing problems associated with asymmetric information has serious equity consequences. Those people who are genetically at a higher risk for adverse health events will pay higher premiums and may be priced out of the market. Potential solution of “community rating”—pooling a community of people into one plan. employer-mandated coverage in which large employers with a pool of many people with different risks are combined into one insurance plan with uniform premium rates. Government provided mandatory health care coverage for the entire population setting uniform rates for premiums.

4

A DVANTAGES AND DISADVANTAGES OF COMMUNITY RATINGS Advantage: Disadvantage: this “community rating” means that some people may have to pay premiums above the plan’s worth to them individually (not rewarding those with healthy lifestyles that have little or no need for insurance), while others would prefer to pay more money in order to buy more insurance.

, while others would prefer to pay more money in order to buy more insurance.")

5

H EALTH I NSURANCE AND M ORAL H AZARD Another consequence of insurance is moral hazard or the tendency to engage in risky or costly behavior because you are insured against adverse events. With health insurance plans, the more a plan smoothes the risk to individuals of lost income by covering health care costs, the more it leads to inefficient overconsumption of health care through an increase in risky behavior. Risky behavior includes Costly behavior includes

6

D EGREE OF MORAL HAZARD AND TYPE OF INSURANCE The degree of moral hazard depends on the type of insurance. Insurance with a copayment Co-insurance:

7

M ORAL HAZARD GRAPHING

8

M ORAL HAZARD GRAPHING CONTINUED

9

US HEALTH EXPENDITURES --% GDP

10

US SPENDING PER CAPITA IS MUCH HIGHER THAN OTHER COUNTRIES

11

R ICH COUNTRIES SPEND MORE — BUT US SPENDS PROPORTIONATELY MORE !

12

R EADING C HART 3 ABOVE : ( TAKEN DIRECTLY FROM OECD PUBLICATION ) If per capita income is around $20,000, a country is ‘expected’ to spend about $1,500 per person on health (and indeed this is the case for countries like Slovakia and Hungary), whereas if per capita income is $40,000, health spending of a bit more than $3,500 would be predicted. The relationship is simply an empirical observation: it does not imply that a country should be spending at or near the line, but it is a convenient way of thinking about national health spending levels. There are significant differences across countries: Canada spends a lot more than Australia, for example, though income levels are similar. But the United States is the biggest outlier, by a wide margin. A country with the income level of the United States would be expected to spend around $2,500 less per capita than it actually does – equivalent to $750billion per year.

13

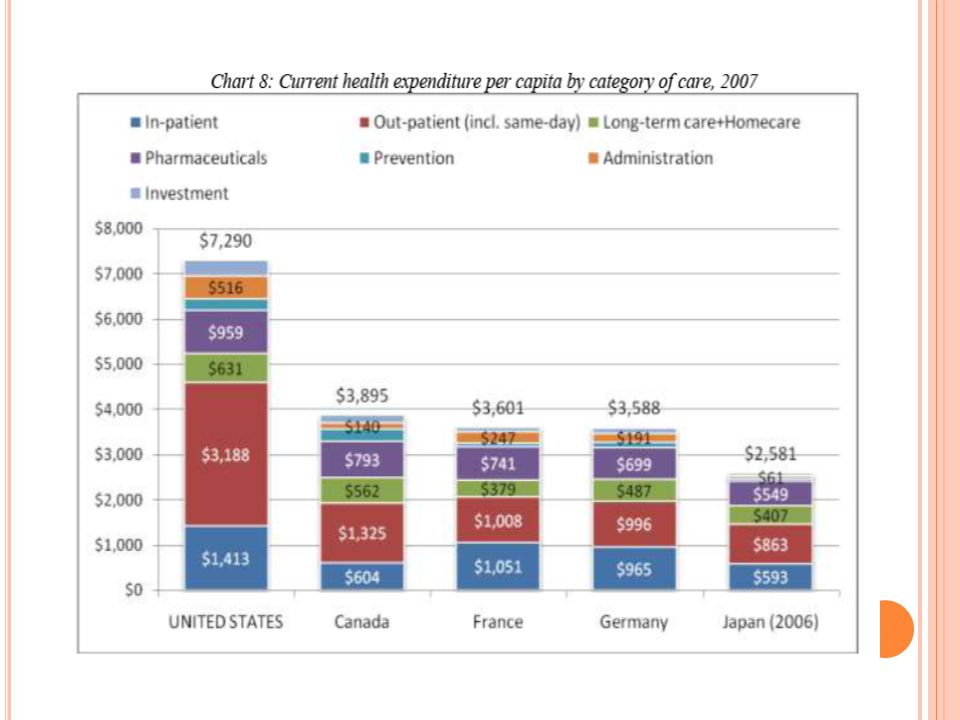

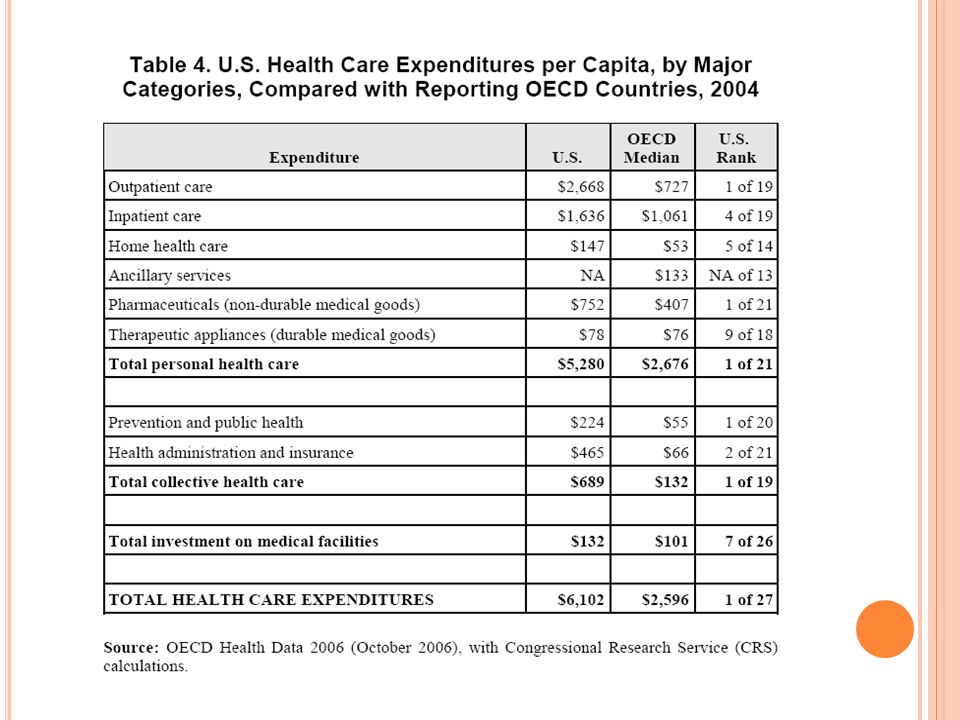

C ATEGORIES OF HEALTH SPENDING In what categories of cost is the US relatively high relative to OECD countries? (taken from “Written Statement to the Senate Committee on Aging” by Mark Pearson) 1. ___________________ is higher than in other OECD countries, but not by as much as might be expected, given differences in GDP. This reflects in part a data problem – some spending which would be classified as in-patient care in other countries is classified in out-patient care in the United States. It has been growing somewhat less rapidly than other categories of spending. 2. ___________________ is also highest in the United States, being more than three-times greater than in France, Germany and Japan, and growing very rapidly indeed. The growth rate is high in other countries as well, but from a lower basis.

1. ___________________ is higher than in other OECD countries, but not by as much as might be expected, given differences in GDP. This reflects in part a data problem – some spending which would be classified as in-patient care in other countries is classified in out-patient care in the United States. It has been growing somewhat less rapidly than other categories of spending. 2. ___________________ is also highest in the United States, being more than three-times greater than in France, Germany and Japan, and growing very rapidly indeed. The growth rate is high in other countries as well, but from a lower basis..")

14

S PENDING CATEGORIES CONTINUED 3. _____________________ are high. 4. ______________________ is higher in the US than in any other country, but it accounts for a smaller share of total health spending than in other countries. 5. _____________________ is a little higher than in other countries, but proportionally accounts for less spending than elsewhere.

17

US RANKING ON EXPENSIVE PROCEDURES

18

US HEALTH OUTCOMES — LIFE EXPECTANCY AND INFANT MORTALITY RATES

19

C URRENT HEALTH CARE REFORM BILL Mandatory Health Care will expand coverage to approximately 32 million Americans currently uninsured. Additionally, insurance companies will not be allowed to deny children coverage based on pre- existing conditions (begins 6 months from now) Insurance providers will no longer anyone coverage based on pre-existing conditions (beginning in 2014) Children may stay on their parent’s health plan until the age of 26.

Insurance providers will no longer anyone coverage based on pre-existing conditions (beginning in 2014) Children may stay on their parent’s health plan until the age of 26..")

20

“ MANDATES ” OF THE BILL Individual mandate: everyone must purchase health insurance or face a $695 annual fine (there are some exceptions for low-income people). This does not apply to illegal immigrants (approximately 11 million people). Effective January 2014. Employer-mandate: “medium sized businesses” are employers with more than 50 employees and must provide health insurance or pay a fine of $750 per worker, per year. If employees receive federal subsidies for purchase of health insurance this fine may be increased to $2,000 per worker, per year. “small businesses” with 25 or fewer employees will earn a tax credit up to 50% of their employees health care coverage expenses. Otherwise, these employees may buy into the Health Exchange in their state.

. Effective January Employer-mandate: medium sized businesses are employers with more than 50 employees and must provide health insurance or pay a fine of $750 per worker, per year. If employees receive federal subsidies for purchase of health insurance this fine may be increased to $2,000 per worker, per year. small businesses with 25 or fewer employees will earn a tax credit up to 50% of their employees health care coverage expenses. Otherwise, these employees may buy into the Health Exchange in their state..")

21

W HAT IS A HEALTH EXCHANGE ? Each state will create a health exchange in which those uninsured citizens and self- employed citizens can purchase health insurance. A separate exchange is to be created for small businesses to purchase coverage. Subsidies will be available for those qualifying based on income. General rule will be that individuals and families with income between 133% and 400% of the poverty level will receive subsidies to reduce the cost of health insurance. For those families earning below the 133% poverty level ($29,327 for a family of four), Medicaid will provide coverage.

, Medicaid will provide coverage..")

22

F UNDING FOR THE BILL -- TAXES A new Medicare payroll tax on investment income (unearned income) starting in 2010. 3.8% tax on investment income for families earning more than $250,000 per year. New Medicare tax on the wealthy earning over $250,000. Medicare tax of 0.9%. Excise tax on “Cadillac insurance plans” –high end insurance plans worth over $27,500 for families will result in a 40% tax on insurance companies. Excise tax of 10% on indoor tanning.

23

O THER SOURCES OF FUNDING Annual fee on manufacturers and importers of some medical devices. Annual fee on certain makers of branded prescription drugs. Increases medical tax deduction threshold from 7.5% to 10% of adjusted gross income.

Similar presentations