Download presentation

Presentation is loading. Please wait.

1

For Producer Use Only. Not For Use with the Public Principal Life Insurance Company Why Principal Life for Individual Disability Insurance? & Disability Center Disability Center is your “one stop shop” for DI. - Full back office support - Top DI products and compensation - Discounted plans available - Free training, Marketing materials, Personal web portals for DI - Niche products and occupations 888-677-6575 www.DisabilityCenter.com Office@DisabilityCenter.comwww.DisabilityCenter.comOffice@DisabilityCenter.com

2

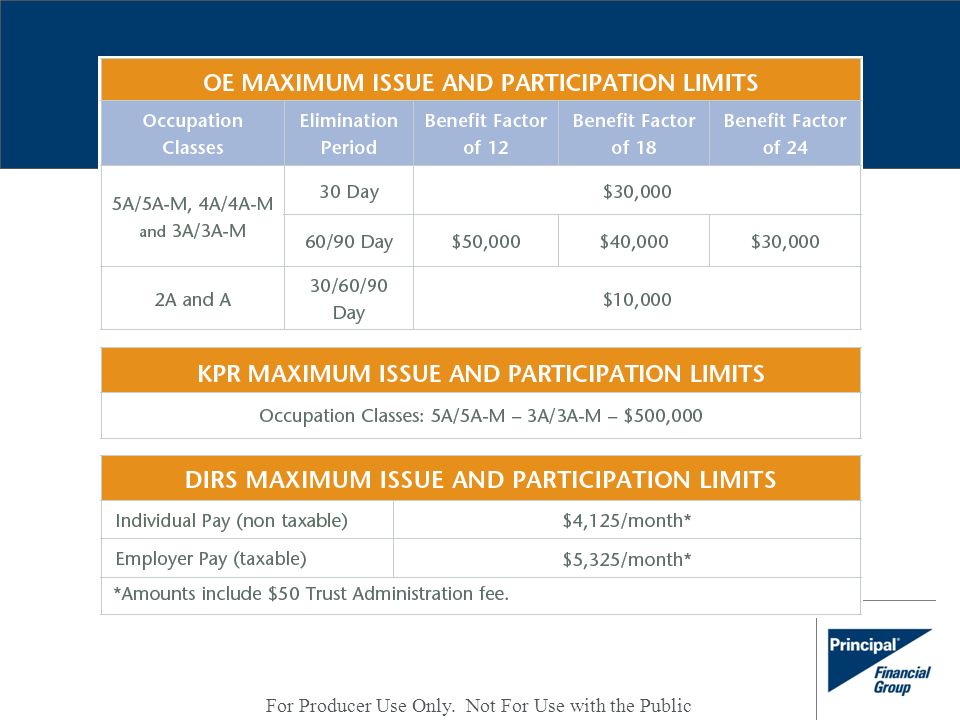

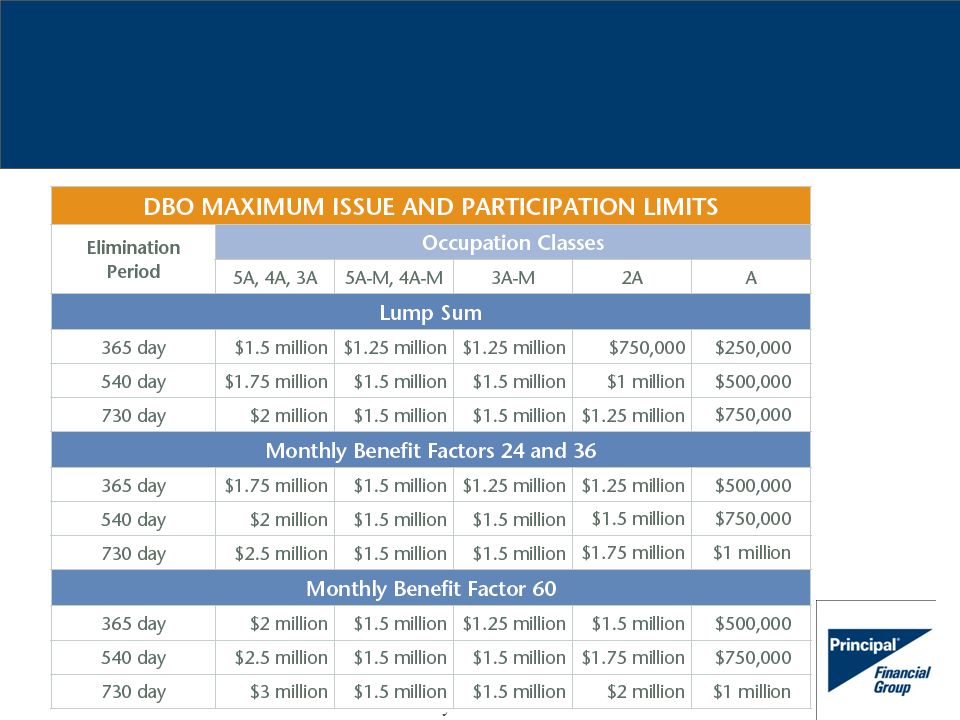

For Producer Use Only. Not For Use with the Public Competitive Product Offering Individual Disability Income Insurance –To $15,000 MB Individual 1 ; Up to $25,000 MB Multi-Life 1 Overhead Expense Insurance –To $50,000 MB reimbursement 1 –Business Loan Protector Rider (new); for HH702 OE 2 Up to $10,000 MB; $1 million Aggregate P&I Loan repayment Disability Buy-Out Insurance –To $3 million* reimbursement for purchase of disabled owner’s interest Key Person Replacement Insurance (new) 2 –2x times key employee’s earned income to $500,000 1 DI Retirement Security Insurance 3 –These benefits are in addition to other coverage. Benefits paid to an irrevocable trust which are invested according to the investment option chosen by the client. 15% of annual income to $4,125 per month individual pay, $5,325 employer paid. 1 MB = Maximum Benefit 1 – Additional guidelines apply. 2 – Not approved in all states. For listing of state approvals, go to: principal.com/distateapprovas 3 – Not available in California.

; for HH702 OE 2 Up to $10,000 MB; $1 million Aggregate P&I Loan repayment Disability Buy-Out Insurance –To $3 million* reimbursement for purchase of disabled owner’s interest Key Person Replacement Insurance (new) 2 –2x times key employee’s earned income to $500,000 1 DI Retirement Security Insurance 3 –These benefits are in addition to other coverage. Benefits paid to an irrevocable trust which are invested according to the investment option chosen by the client. 15% of annual income to $4,125 per month individual pay, $5,325 employer paid. 1 MB = Maximum Benefit 1 – Additional guidelines apply. 2 – Not approved in all states. For listing of state approvals, go to: principal.com/distateapprovas 3 – Not available in California..")

3

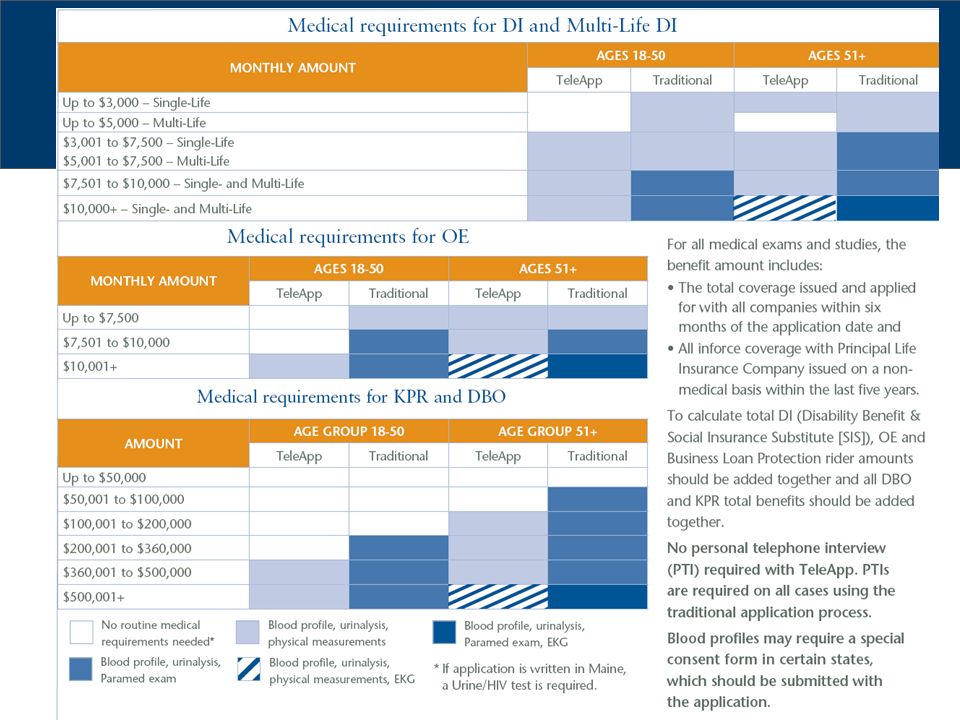

For Producer Use Only. Not For Use with the Public What is TeleApp? TeleApp means: Improved policy issue time Less paperwork and follow-up Fewer APSs, full paramedical exams, PTIs, and inspection reports. Client answers questions only once Producer stays fully informed throughout the application process Direct access to Underwriters

4

For Producer Use Only. Not For Use with the Public TeleApp Process Complete the initial application Explain the interview process to your client Schedule the TeleApp interview by calling 1-888-TeleApp (1-888-835-3277) from 7 a.m. to 10 p.m. Monday through Thursday, or 7 a.m. to 7 p.m. on Friday. (Central Time Zone) Provide broker and client contact information Submit initial application and additional necessary forms to new business coordinator in your office Deliver policy to client and secure signatures to verify application information Return one set of signed applications to the home office

from 7 a.m. to 10 p.m. Monday through Thursday, or 7 a.m. to 7 p.m. on Friday. (Central Time Zone) Provide broker and client contact information Submit initial application and additional necessary forms to new business coordinator in your office Deliver policy to client and secure signatures to verify application information Return one set of signed applications to the home office.")

5

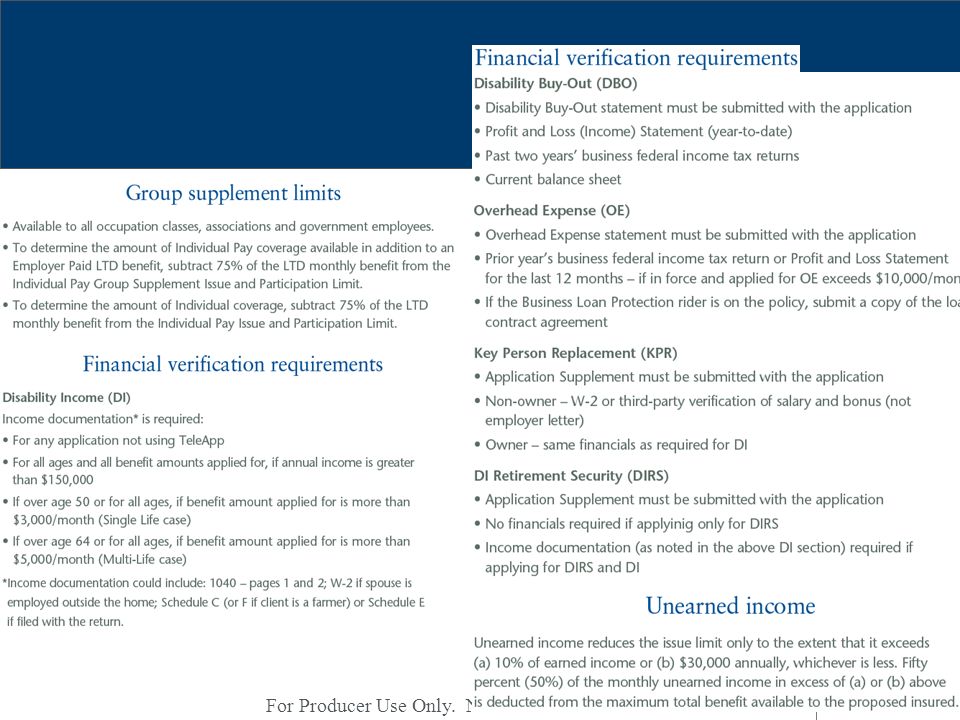

For Producer Use Only. Not For Use with the Public Sales Concepts and Programs Select Professionals 4 Need to have business ownership to qualify.

6

For Producer Use Only. Not For Use with the Public Sales Concepts and Programs Select Professionals 4 Need to have business ownership to qualify.

7

For Producer Use Only. Not For Use with the Public Sales Concepts and Programs Select Professionals (cont.) Underwriting considerations: A blood profile and urinalysis are required if the Benefit Update rider is selected for the following doctor occupations: first through last year resident/intern or medical student third and fourth year. | A blood profile and urinalysis are required if the monthly benefit amount is greater than $3,000.| Additional application paperwork for Overhead Expense and DI Retirement Security is required.

Underwriting considerations: A blood profile and urinalysis are required if the Benefit Update rider is selected for the following doctor occupations: first through last year resident/intern or medical student third and fourth year. | A blood profile and urinalysis are required if the monthly benefit amount is greater than $3,000.| Additional application paperwork for Overhead Expense and DI Retirement Security is required..")

8

For Producer Use Only. Not For Use with the Public Sales Concepts and Programs 10% 5A Select Occupation Discount –Actuaries, Architects, Attorneys, Certified Public Accountants (CPAs), Engineers, Executives (earning over $60,000), and Pharmacists –Can be “stacked” with Principal Life’s other discount offerings of the 20% Multi-Life or 10% Association –The Select Occupation discount applies to Individual Disability, Business Overhead, Disability Buy-Out, Key Person Replacement and DI Retirement Security insurance

, Engineers, Executives (earning over $60,000), and Pharmacists –Can be stacked with Principal Life’s other discount offerings of the 20% Multi-Life or 10% Association –The Select Occupation discount applies to Individual Disability, Business Overhead, Disability Buy-Out, Key Person Replacement and DI Retirement Security insurance.")

9

For Producer Use Only. Not For Use with the Public Sales Concepts and Programs 20% Multi-life Discount –20% discount for three or more lives with a common employer* –Unisex rates where available for Individual DI –Discount is fully portable, and no list bill required * 5 or more lives required in Ohio.

10

For Producer Use Only. Not For Use with the Public Sales Concepts and Programs Association BenefitsMember BenefitsProducer Benefits Valuable benefit for existing members at a discount An incentive for enticing new members No cost to the association No administrative work required Materials and marketing support to promote program 10% Association Discount available Financial needs analysis by trained representative Quality coverage Access to From Here to Security SM educational materials Access to multiple prospects in one setting Credibility afforded by an association’s endorsement Networking an relationship building potential Opportunities for new business and cross- sales 10% Association Discount Association offering may not be available in all states, for all products. For state approvals, go to: principal.com/distateapprovals. Not available in California.

11

For Producer Use Only. Not For Use with the Public Sales Concepts and Programs Simplified Sales Programs –Streamlined underwriting decision in 48 hours once the applications and TeleApp interviews are completed and received – without income verification (for incomes less than $150,000/year; for most occupations) or routine medical requirements*. –Up to $3,000/month benefit – Single Life –Up to $5,000/month benefit – Multi-Life –Up to $10,000/month benefit – Simplified OE –Up to $360,000 aggregate benefit – Simplified DBO *Unless a significant and undisclosed medical condition is reported by MIB, significant medical information is derived from the TeleApp, or any other disability coverage has been issued or applied for on a non-medical basis. Urine/HIV test is required in Maine. This is not a guaranteed issue program; applications could be rated, ridered or declined. Subject to Issue & Participation limits and minimum premium requirement. Combined Simplified DI and Simplified OE benefits cannot exceed $10,000/month.

or routine medical requirements*. –Up to $3,000/month benefit – Single Life –Up to $5,000/month benefit – Multi-Life –Up to $10,000/month benefit – Simplified OE –Up to $360,000 aggregate benefit – Simplified DBO *Unless a significant and undisclosed medical condition is reported by MIB, significant medical information is derived from the TeleApp, or any other disability coverage has been issued or applied for on a non-medical basis. Urine/HIV test is required in Maine. This is not a guaranteed issue program; applications could be rated, ridered or declined. Subject to Issue & Participation limits and minimum premium requirement. Combined Simplified DI and Simplified OE benefits cannot exceed $10,000/month..")

12

For Producer Use Only. Not For Use with the Public Sales Concepts and Programs The DI Solutions Center – Standard Issue Program –Your one stop resource for multi-life case assistance (15+ lives) –Provides standard coverage for an entire group –Available for employer-paid or voluntary employee paid cases –Discounts and coverage based on participating lives –This program gives employees an opportunity to obtain coverage without medical evidence of insurability. –If they leave their employer, the policy is portable with continued discounts

–Provides standard coverage for an entire group –Available for employer-paid or voluntary employee paid cases –Discounts and coverage based on participating lives –This program gives employees an opportunity to obtain coverage without medical evidence of insurability. –If they leave their employer, the policy is portable with continued discounts.")

13

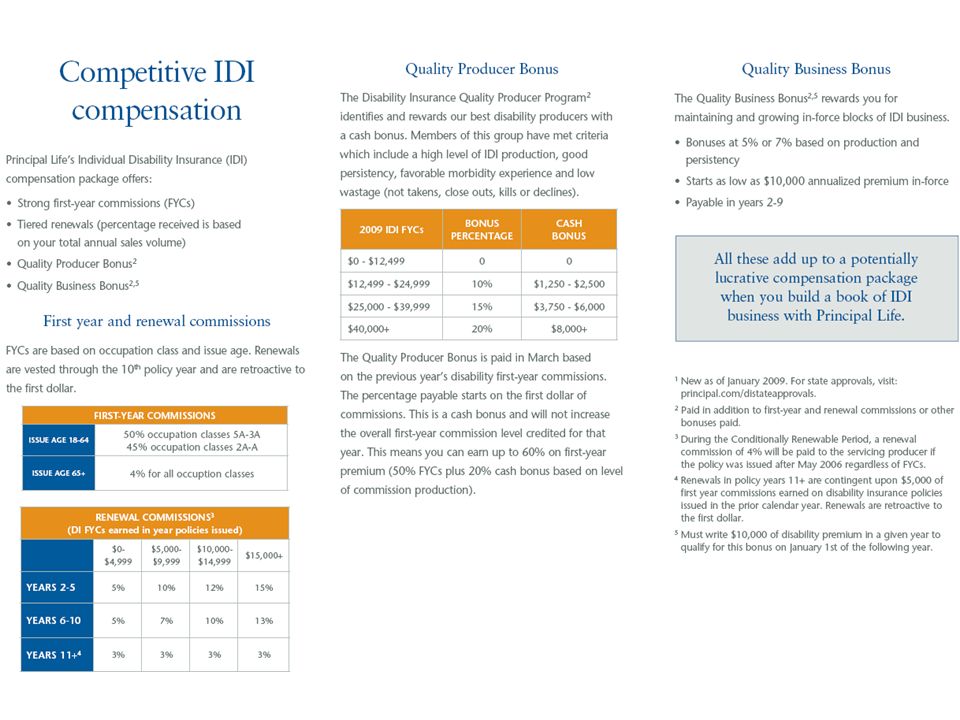

For Producer Use Only. Not For Use with the Public Attractive Compensation Series 700 Compensation Shown; Compensation Differs for Solutions II (California) 1 – For issue ages 65 and older, the first year commission rate is 4%. 2 – During the Conditionally Renewable Period, a renewal commission of 4% will be paid to the servicing producer if the policy was issued after May 2006 regardless of FYC. 3 – Renewals in years 11+ are contingent upon $5,000 of annualized disability commission in the prior year.

1 – For issue ages 65 and older, the first year commission rate is 4%. 2 – During the Conditionally Renewable Period, a renewal commission of 4% will be paid to the servicing producer if the policy was issued after May 2006 regardless of FYC. 3 – Renewals in years 11+ are contingent upon $5,000 of annualized disability commission in the prior year..")

14

Attractive Compensation Please remember to abide by the company's policy on disclosure of compensation. You can obtain more information, as well as a sample disclosure form, at www.principal.com Attractive Compensation

15

Your income potential over 10 years

17

For Producer Use Only. Not For Use with the Public We have one goal in mind…to help you sell more.

18

For Producer Use Only. Not For Use with the Public Disability’s Triple Threat Business owners face a triple threat Keeping a roof over their head Keeping their business’ doors open Keeping their business investment intact

19

For Producer Use Only. Not For Use with the Public Keeping a roof over their head – income protection Individual Disability Income insurance

20

For Producer Use Only. Not For Use with the Public Income $4,216,000 Home $242,700 Car $28,715 Keeping a roof over their head 1 – Auto Affordability Index, complied by Comerica Bank, February 2008 2 – Average sale price in United States, © 2009 National Association of REALTORS ® 3 –Projected cumulative income, 35-year-old earning $6,250/month assuming 4% annual increase to age 65.

21

For Producer Use Only. Not For Use with the Public Keeping a roof over their head Ask clients: What would happen to your income? How would you maintain your lifestyle? Where would the money come from to pay for bills? What happens to your retirement savings and other financial goals? Do you have Group Long-Term Disability insurance in place? Are the benefits taxable?

22

For Producer Use Only. Not For Use with the Public Can your clients live on 42% of their income? Chart based on $5,000 gross monthly income ($60,000 annually), with 60% Group Long Term Disability program, assuming a 30% tax bracket for Federal, State and FICA. Few could live on 42% of their income.

, with 60% Group Long Term Disability program, assuming a 30% tax bracket for Federal, State and FICA. Few could live on 42% of their income..")

23

For Producer Use Only. Not For Use with the Public Keeping a roof over their head Personal income protection so clients can: Provide for family if they become too sick or hurt to work Maintain their lifestyle without draining savings or business profits Protect a higher level of their income (in the event you have Group LTD insurance) Individual Disability Income (DI) insurance

Individual Disability Income (DI) insurance.")

24

For Producer Use Only. Not For Use with the Public Keeping the business’ door open – risk management Overhead Expense and Key Person Replacement Insurance

25

For Producer Use Only. Not For Use with the Public Keeping the business’ door open Ask your clients: If you are unable to work, would your business be able to keep the doors open? How would business expenses get paid (rent, salaries, utilities, etc....)? Would you have to turn clients away? What would happen to your business if a key employee became totally disabled?

. Would you have to turn clients away. What would happen to your business if a key employee became totally disabled .")

26

For Producer Use Only. Not For Use with the Public Chances of a Disability Lasting Three Months or Longer (Before Age 65) Age1 Owner2 Owners3 Owners 2745.3%70.0%83.6% 3740.4%64.5%78.8% 4732.8%54.8%69.6% 5719.6%35.4%48.1% Based on Commissioner’s Individual Disability Table A – Equally Weighted, All Occupation Classes, Unisex Keeping your business’ door open

Age1 Owner2 Owners3 Owners %70.0%83.6% %64.5%78.8% %54.8%69.6% %35.4%48.1% Based on Commissioner’s Individual Disability Table A – Equally Weighted, All Occupation Classes, Unisex Keeping your business’ door open.")

27

For Producer Use Only. Not For Use with the Public Possible income sources Business partner Creditors Liquidate assets Personal savings Sell the business Keeping the business’ door open

28

For Producer Use Only. Not For Use with the Public With Overhead Expense insurance: Fixed business expenses are reimbursed No reliance on creditors Savings and investment plans aren’t jeopardized Foreclosure or liquidation can be avoided Premiums are tax-deductible Keeping the business’ door open

29

For Producer Use Only. Not For Use with the Public With Key Person Replacement insurance: Protects the business from the loss of a key employee Business pays for and is the owner of the policy Any benefits received can be used at the business’ discretion, but cannot be assigned to the key employee Helps demonstrate financial stability to creditors, shareholders and other stakeholders Keeping the business’ door open

30

For Producer Use Only. Not For Use with the Public Keeping the business investment intact – succession planning Disability Buy-Out Insurance

31

For Producer Use Only. Not For Use with the Public Keeping the business investment intact Would you want to sell your share of the business? Would you want to buy out your partner? How would the price be determined? Where would the money come from? Is it guaranteed to be there when it’s needed? Ask your clients, if you or one of your partners is disabled …

32

For Producer Use Only. Not For Use with the Public The disabled partner may: Become a drain on income while not contributing to the business Have different priorities for the business income and profits and may not want to reinvest profits Decide to let spouse or relative take over their role in the business Keeping the business investment intact The healthy partner may not: Be able to pay the disabled partner an income and maintain the business Have funds to buy the disabled partner out Want to share business decisions with the disabled partners family

33

For Producer Use Only. Not For Use with the Public Disabled owner advantages Assures a definite price and buyer Financial future is no longer contingent on the business’s success Keeping the business investment intact Healthy owner(s) advantages Avoids negotiation of price Assures complete and orderly transfer of ownership Retains control of the business Provides continuity and credibility for customers and creditors Establishing a buy-sell agreement

advantages Avoids negotiation of price Assures complete and orderly transfer of ownership Retains control of the business Provides continuity and credibility for customers and creditors Establishing a buy-sell agreement.")

34

For Producer Use Only. Not For Use with the Public Keeping the business investment intact Funding alternatives Current cash flow Establish a sinking fund Borrow the funds Disability Buy-Out insurance

35

For Producer Use Only. Not For Use with the Public Keeping the business investment intact Disability Buy-Out Insurance A written agreement that specifies when and for how much the buy-out will take place, and... is funded with the right amount of Disability Buy-Out insurance.

36

For Producer Use Only. Not For Use with the Public OE + DI + DI = 20% discount A business owner purchases OE and employees purchase their own DI = 20% discount! DBO + DBO + KPR = 20% discount Two business owners purchase DBO policies and pay premiums for an employee’s KPR policy = 20% discount! DI + DI + DI = 20% discount Three individuals with a common employer purchase DI policies = 20% discount! Provide peace of mind … at a multi-life discount OE = Overhead Expense | DBO = Disability Buy-Out | DI = Individual Disability Income | KPR = Key Person Replacement Multi-Life Discount may not be available in all states for all products. Ohio requires 5 lives.

37

For Producer Use Only. Not For Use with the Public

45

Disability Center Thank you! Questions? 888-677-6575 www.DisabilityCenter.com Office@DisabilityCenter.comwww.DisabilityCenter.comOffice@DisabilityCenter.com

Similar presentations

SI/SNY Guarantee Issue 101 For producer training. Not for use with consumers.>")

![Protect Yourself, Your Business and the People Who Rely on You: DI Strategies for [Business Owners] [Solo or Group Practitioners] Presented by: Your Name.](/13/4175620/big_thumb.jpg "Protect Yourself, Your Business and the People Who Rely on You: DI Strategies for [Business Owners] [Solo or Group Practitioners] Presented by: Your Name.>")

Buy/Sell Funding Disability Insurance at The Standard For producer training only. Not for use with consumers.>")

What they are and how to exercise them at The Standard Future Purchase Options For producer use only. Not for use with consumers.>")

?>")

(FL)MLIC-LD Disability Income : Helping You Build Financial Freedom.>")