Download presentation

Presentation is loading. Please wait.

1

The Affordable Care Act: 2.0 Misty Baker 512-493-2432 office 512-797-3631 cell/text mbaker@iiat.org Twitter: @mistybaker Facebook: misty merkel baker

2

Marketplace Model Notice

3

Due to each new hire within 14 days of hire. NOT required annually, only at hire.

4

Rehire Rules Simplified Rule: –Gone from work more than 13 weeks = new employee –Gone from work less than 13 weeks = continuing employee No new waiting period, no initial measurement period –Exception: Educational institutions use a 26 week standard 4

5

Cadillac Tax Plan and discuss the Cadillac Tax with your clients as if it is 100% certain to happen. How it works: Examples based on current threshold amounts Self-only coverage A $12,000 individual plan would pay an excise tax of $720 per covered employee : $12,000 - $10,200 = $1,800 above the $10,200 threshold $1,800 x 40% = $720 Family coverage A $32,000 family plan would pay an excise tax of $1,800 per covered employee: $32,000 - $27,500 = $4,500 above the $27,500 threshold $4,500 x 40% = $1,800 5

6

Controlled Group Rules In companies with common ownership, the IRS controlled group rules apply and all employees of controlled group are counted to determine mandate applicability. Determining controlled group status is very complicated and a broker cannot legally do this for an employer. A summary of the rule for reference is it is two or more corporations generally connected through common control/stock ownership in any of the following ways: Parent-subsidiary group Brother-sister group Combined group Normal shared ownership percentage is 80% but it can vary! For reference, the IRS attempts to explain it all in this 108-page publication! http://www.irs.gov/pub/irs-tege/epchd704.pdf Important Points to Know The group’s CPA /tax counsel should already know what they are and this is not something a broker can legally determine for a company. The controlled group rules apply for 401Ks too.

7

Three Affordability Safe Harbors W-2 Safe Harbor: Affordability is based on: Employee is paying less than 9.56% of the employee’s W-2 (Box 1) income Box 1 income is the “adjusted gross income” or after pre-tax withholdings Monthly Pay Safe Harbor: Affordability is based on: How calculated: For salaried employees: monthly salary, for hourly employees: the hourly rate of pay x 130 hours/month If the employee's required monthly contribution for self-only coverage does not exceed 9.56% of the monthly wages, the employer coverage would be affordable FPL Safe Harbor: Affordability is based on: the federal poverty level for a single individual If the employee contribution for self-only coverage does not exceed 9.56% of the FPL, the employer coverage would be deemed affordable for all employees.

income Box 1 income is the adjusted gross income or after pre-tax withholdings Monthly Pay Safe Harbor: Affordability is based on: How calculated: For salaried employees: monthly salary, for hourly employees: the hourly rate of pay x 130 hours/month If the employee s required monthly contribution for self-only coverage does not exceed 9.56% of the monthly wages, the employer coverage would be affordable FPL Safe Harbor: Affordability is based on: the federal poverty level for a single individual If the employee contribution for self-only coverage does not exceed 9.56% of the FPL, the employer coverage would be deemed affordable for all employees.")

8

Flow of Information 8 IRS / Government Employer Employee / Individual Insurer / Carrier Exchange TPA What was offered to employees? (1094-C & 1095-C) What the ER offered on 1095-C 1095-A: premium tax credits received What ER or insurer offered on Form 1095-B or C 1095-B & 1094-B (transmittal) Actual Coverage info 1095-B Employer Sponsored Insurance offered? Proof of coverage

What the ER offered on 1095-C 1095-A: premium tax credits received What ER or insurer offered on Form 1095-B or C 1095-B & 1094-B (transmittal) Actual Coverage info 1095-B Employer Sponsored Insurance offered. Proof of coverage.")

9

Large Employers: Report in 2016 for 2015 Plan Year Section 6056 Annually submit: –1094-C to IRS by either March 1, 2016 (typically Feb 28) or March 31 if filing electronically –1095-C to the employees on or by January 31 No filing requirement if the employer has no full time employees 9

or March 31 if filing electronically –1095-C to the employees on or by January 31 No filing requirement if the employer has no full time employees 9")

10

The 1094-C Form: The “Cover Sheet”

11

For groups of 50 or more Your company information Make sure contact person speaks “ACA” Almost always YES, think of this as an attestation Also known as a control group Remember that this form determines your Employer penalty to the IRS. You MUST get this right!

12

22 A. Qualifying Offer Method All months, FPL method MEC EE, SP and Dependents 22 A. Qualifying Offer Method All months, FPL method MEC EE, SP and Dependents 22 B. Qualifying Offer Method Transitional Relief One or month months Offer to 95% of EEs (70% in 2015) 22 B. Qualifying Offer Method Transitional Relief One or month months Offer to 95% of EEs (70% in 2015) 22 C. Section 4980H Transitional Relief 50-99 EEs Not subject to 4980H in 2015 (USE THIS BOX) 100+ ERs who are eliminating first 80 (30 in 2016) 22 C. Section 4980H Transitional Relief 50-99 EEs Not subject to 4980H in 2015 (USE THIS BOX) 100+ ERs who are eliminating first 80 (30 in 2016) 22 D. 98% Offer Method ALL calendar months MEC Using any Affordability Safe Harbor 98% EEs covered 22 D. 98% Offer Method ALL calendar months MEC Using any Affordability Safe Harbor 98% EEs covered

22 B. Qualifying Offer Method Transitional Relief One or month months Offer to 95% of EEs (70% in 2015) 22 C. Section 4980H Transitional Relief EEs Not subject to 4980H in 2015 (USE THIS BOX) 100+ ERs who are eliminating first 80 (30 in 2016) 22 C. Section 4980H Transitional Relief EEs Not subject to 4980H in 2015 (USE THIS BOX) 100+ ERs who are eliminating first 80 (30 in 2016) 22 D. 98% Offer Method ALL calendar months MEC Using any Affordability Safe Harbor 98% EEs covered 22 D. 98% Offer Method ALL calendar months MEC Using any Affordability Safe Harbor 98% EEs covered.")

13

TOTAL EE count Indicate, per month the amount of FT EEs Check if this is part of a controlled group A – If 50-99 EEs B – if over 100 EEs/1 st 80 free A – If 50-99 EEs B – if over 100 EEs/1 st 80 free

14

List the members of your control group here

15

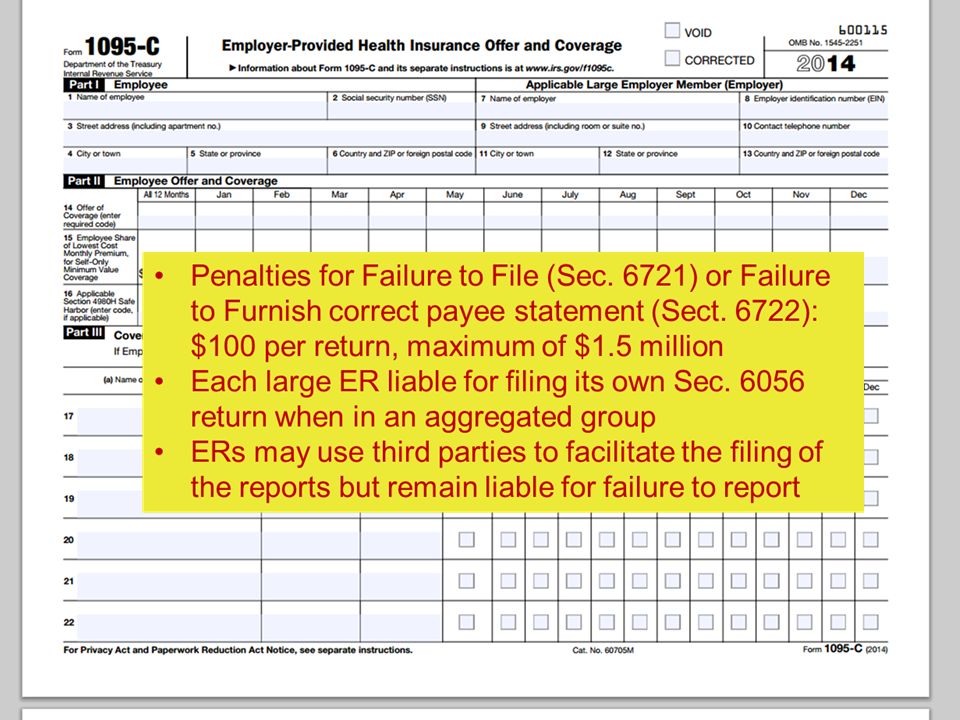

The 1095-C Form: The Employee Form

16

This is employee specific, think of it as another W-2 Every full time employee One copy to the Employee One copy to the IRS One copy to the Employee One copy to the IRS Make sure your contact phone number speaks ACA Carriers complete 1095-B and 1094-B forms and send them to the IRS Make three reasonable attempts to get a social security number for dependents ONLY complete Part III if you are self funded

17

Line 14: What did I actually offer my employees? Use Series 1 codes 1A – MEC/MV offered to Fulltime employees that is affordable using FPL safe harbor and MEC offered to spouse and dependents (FPL 2014:$92.39, FPL 2015: $93.18) 1B - MEC/MV offered to employee only 1C - MEC/MV offered to employee and MEC offered to dependents but NOT the spouse 1D -MEC/MV offered to the employee and MEC to spouse but NOT dependents 1E – MEC/MV offered to employees and MEC offered to Spouse and Dependents 1F – MEC without MV offered to employee or employee plus any combination of spouse and dependents 1G – SELF FUNDED ONLY – offer of coverage to employee who was not full time employee for any month and who enrolled in self insurance coverage for one or more months 1H – No offer of MEC 1I – Qualifying Offer of Transitional Relief: employee(and spouse and dependents) receive no offer of coverage, OR an offer that is not qualifying offer, or qualifying offer for less than 12 months (use this when you offer coverage to at least 95% of EEs) Line 14: What did I actually offer my employees? Use Series 1 codes 1A – MEC/MV offered to Fulltime employees that is affordable using FPL safe harbor and MEC offered to spouse and dependents (FPL 2014:$92.39, FPL 2015: $93.18) 1B - MEC/MV offered to employee only 1C - MEC/MV offered to employee and MEC offered to dependents but NOT the spouse 1D -MEC/MV offered to the employee and MEC to spouse but NOT dependents 1E – MEC/MV offered to employees and MEC offered to Spouse and Dependents 1F – MEC without MV offered to employee or employee plus any combination of spouse and dependents 1G – SELF FUNDED ONLY – offer of coverage to employee who was not full time employee for any month and who enrolled in self insurance coverage for one or more months 1H – No offer of MEC 1I – Qualifying Offer of Transitional Relief: employee(and spouse and dependents) receive no offer of coverage, OR an offer that is not qualifying offer, or qualifying offer for less than 12 months (use this when you offer coverage to at least 95% of EEs) CodeExplanation 1AMEC/MV offered to full-time employee that is affordable using the FPL Safe Harbor (employee rate of $92.39 or less), and MEC offered to spouse and dependents 1BMEC/MV offered to employee only 1CMEC/MV offered to employee, and MEC offered to dependents (not spouse) 1DMEC/MV offered to employee, and MEC to spouse (not dependents) 1EMEC/MV offered to employee, and MEC to spouse and dependents 1FMEC without MV offered to employee or any combination of employee, spouse and dependents 1GOffer of coverage to employee who was not a full-time employee for any month and who enrolled in self- insured coverage for one or more months 1HNo offer of minimum essential coverage

1B - MEC/MV offered to employee only 1C - MEC/MV offered to employee and MEC offered to dependents but NOT the spouse 1D -MEC/MV offered to the employee and MEC to spouse but NOT dependents 1E – MEC/MV offered to employees and MEC offered to Spouse and Dependents 1F – MEC without MV offered to employee or employee plus any combination of spouse and dependents 1G – SELF FUNDED ONLY – offer of coverage to employee who was not full time employee for any month and who enrolled in self insurance coverage for one or more months 1H – No offer of MEC 1I – Qualifying Offer of Transitional Relief: employee(and spouse and dependents) receive no offer of coverage, OR an offer that is not qualifying offer, or qualifying offer for less than 12 months (use this when you offer coverage to at least 95% of EEs) Line 14: What did I actually offer my employees. Use Series 1 codes 1A – MEC/MV offered to Fulltime employees that is affordable using FPL safe harbor and MEC offered to spouse and dependents (FPL 2014:$92.39, FPL 2015: $93.18) 1B - MEC/MV offered to employee only 1C - MEC/MV offered to employee and MEC offered to dependents but NOT the spouse 1D -MEC/MV offered to the employee and MEC to spouse but NOT dependents 1E – MEC/MV offered to employees and MEC offered to Spouse and Dependents 1F – MEC without MV offered to employee or employee plus any combination of spouse and dependents 1G – SELF FUNDED ONLY – offer of coverage to employee who was not full time employee for any month and who enrolled in self insurance coverage for one or more months 1H – No offer of MEC 1I – Qualifying Offer of Transitional Relief: employee(and spouse and dependents) receive no offer of coverage, OR an offer that is not qualifying offer, or qualifying offer for less than 12 months (use this when you offer coverage to at least 95% of EEs) CodeExplanation 1AMEC/MV offered to full-time employee that is affordable using the FPL Safe Harbor (employee rate of $92.39 or less), and MEC offered to spouse and dependents 1BMEC/MV offered to employee only 1CMEC/MV offered to employee, and MEC offered to dependents (not spouse) 1DMEC/MV offered to employee, and MEC to spouse (not dependents) 1EMEC/MV offered to employee, and MEC to spouse and dependents 1FMEC without MV offered to employee or any combination of employee, spouse and dependents 1GOffer of coverage to employee who was not a full-time employee for any month and who enrolled in self- insured coverage for one or more months 1HNo offer of minimum essential coverage.")

18

Line 15: Complete ONLY if code 1B, 1C, 1D or 1E is entered online 14 in either the ALL 12 months box, or ANY of the monthly boxes For line 15, enter the lowest-cost monthly premium for self-only minimum essential coverage providing minimum value that is offered to the employee. This amount may not be the amount the employee is paying for the coverage, for example, if the employee chose to enroll in more expensive coverage such as family coverage. If the employee share was the same for all 12 months, only enter the amount in the all 12 months box. Note: this will typically only be the case for a calendar year plan If the employer funds 100% of the health cost for the employee, enter $0.00 in the All 12 months box Line 15: Complete ONLY if code 1B, 1C, 1D or 1E is entered online 14 in either the ALL 12 months box, or ANY of the monthly boxes For line 15, enter the lowest-cost monthly premium for self-only minimum essential coverage providing minimum value that is offered to the employee. This amount may not be the amount the employee is paying for the coverage, for example, if the employee chose to enroll in more expensive coverage such as family coverage. If the employee share was the same for all 12 months, only enter the amount in the all 12 months box. Note: this will typically only be the case for a calendar year plan If the employer funds 100% of the health cost for the employee, enter $0.00 in the All 12 months box

19

Line 16 Series 2 Codes 2A - Employee NOT employed during the ENTIRE month 2B - Employee not full time that month and did not enroll in MEC, if offered that month. (coverage could have ended during the middle of the month) 2C - Employee enrolled in coverage offered (if so this is the ONLY code that needs to be entered in line 16 2D – Employee in a limited non assessment period (waiting period, measurement period, variable hour employee) 2E – Multi employee rule (NOT common) 2F - For W-2 Affordability Safe Harbor 2G – FPL Safe Harbor 2H – Rate of Pay Safe Harbor Line 16 Series 2 Codes 2A - Employee NOT employed during the ENTIRE month 2B - Employee not full time that month and did not enroll in MEC, if offered that month. (coverage could have ended during the middle of the month) 2C - Employee enrolled in coverage offered (if so this is the ONLY code that needs to be entered in line 16 2D – Employee in a limited non assessment period (waiting period, measurement period, variable hour employee) 2E – Multi employee rule (NOT common) 2F - For W-2 Affordability Safe Harbor 2G – FPL Safe Harbor 2H – Rate of Pay Safe Harbor

2C - Employee enrolled in coverage offered (if so this is the ONLY code that needs to be entered in line 16 2D – Employee in a limited non assessment period (waiting period, measurement period, variable hour employee) 2E – Multi employee rule (NOT common) 2F - For W-2 Affordability Safe Harbor 2G – FPL Safe Harbor 2H – Rate of Pay Safe Harbor Line 16 Series 2 Codes 2A - Employee NOT employed during the ENTIRE month 2B - Employee not full time that month and did not enroll in MEC, if offered that month. (coverage could have ended during the middle of the month) 2C - Employee enrolled in coverage offered (if so this is the ONLY code that needs to be entered in line 16 2D – Employee in a limited non assessment period (waiting period, measurement period, variable hour employee) 2E – Multi employee rule (NOT common) 2F - For W-2 Affordability Safe Harbor 2G – FPL Safe Harbor 2H – Rate of Pay Safe Harbor.")

21

Clients Mistakes to Avoid Questions Doing nothing Doing it wrong Not hiring help 21

22

Text, Instagram, FB with me! #IIATconf Misty Baker 800-880-7428 office 512-493-2432 direct 512-797-3631 cell/text mbaker@iiat.org Twitter: @mistybaker Facebook: misty merkel baker Instagram: misty.baker 22

Similar presentations

>")

Better known as ACA>")

Presented by the Asian American Hotel Owners Association (AAHOA)>")

Updates and Strategies What Employers Need to Know for 2015 and Beyond June 3, 2014.>")