Download presentation

Presentation is loading. Please wait.

1

Fiduciary Services in a continuously changing global tax environment. Pitfalls and recommendations for best practices Pieris Markou Head of Tax Services Deloitte, Cyprus

2

Recent Global Developments Cadbury Schweppes

3

Recent Global Developments Vodafone

5

Recent Global Developments German Anti-abuse rules (1-1-2012)

")

6

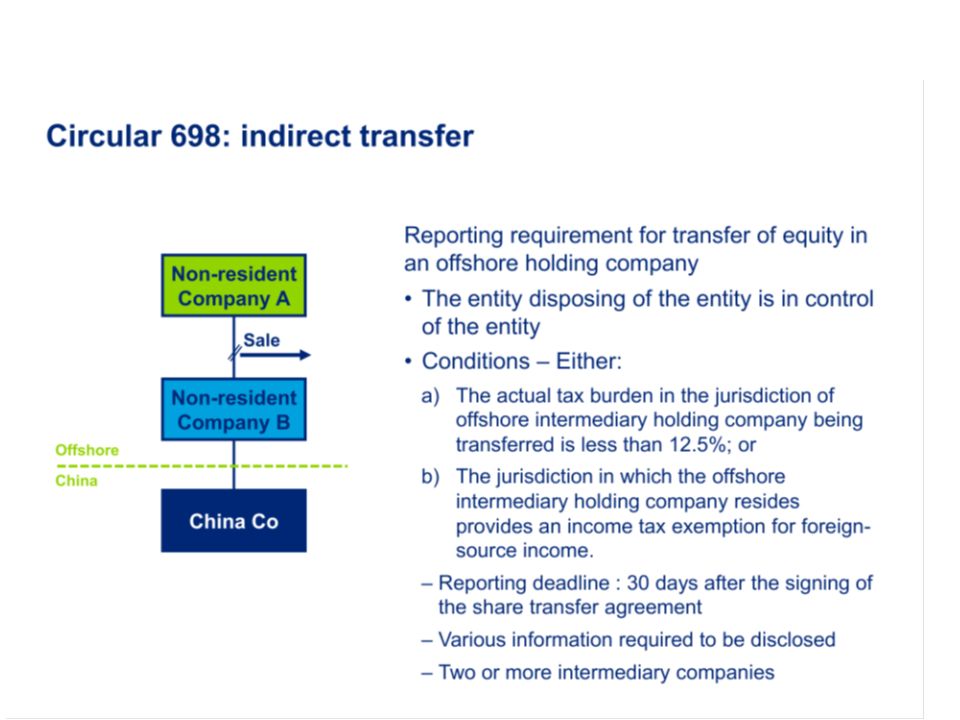

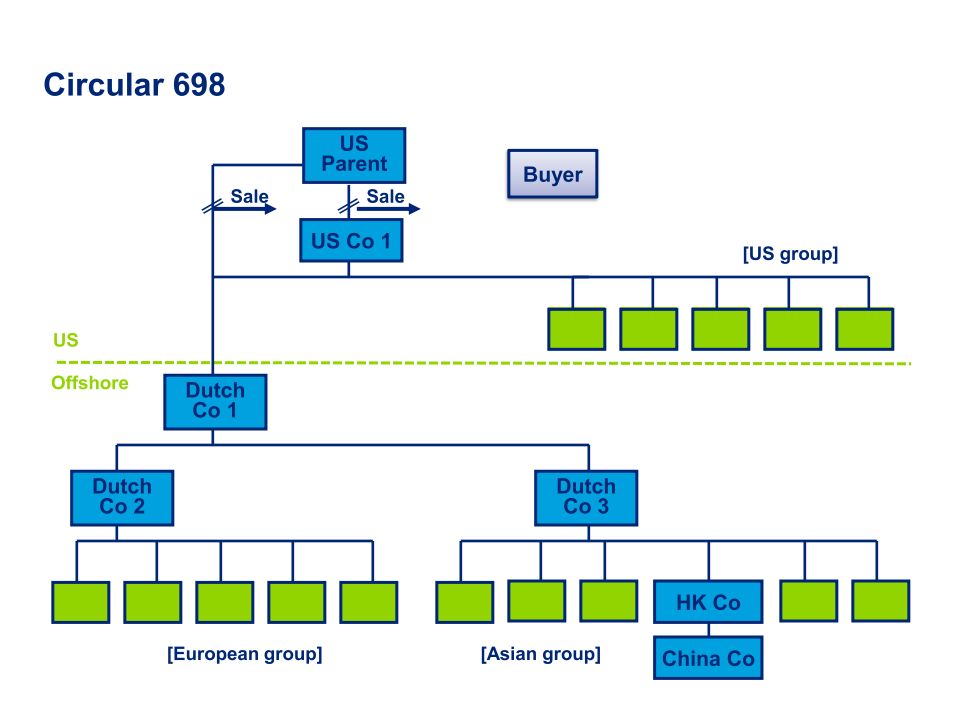

Recent Global Developments Chinese Circulars, 698 and 601

9

Recent Global Developments Indian GAAR

10

Recent Global Developments Monetka Case

11

11 Prior to 2006 the Russian Retail companies enjoyed free of charge use of the trademark. In 2006 the trademark was sold by a Russian individual to a BVI company for USD 8mln. IP holder then entered into a license agreement with the Cypriot company. The Cypriot company then signed sub- license agreements with the Russian retails companies. Based on the tax audit of one of the companies the Russian tax authorities challenged the deduction of USD 15mln of royalties related to 2006 – 2008. IP Co Cyprus Foreign HoldCo RusCo BVI Company Royalties Monetka Case

12

Recent Global Developments Cadbury Schweppes Vodafone German Anti-abuse rules (1-1-2012) Chinese Circulars, 601 and 698 Indian GAAR Monetka Case

Chinese Circulars, 601 and 698 Indian GAAR Monetka Case")

13

Threats Russia - Proposals target treaty shopping and payments to blacklisted jurisdictions India - Gains on sale of compulsory convertible debentures treated as interest Liaison offices in India under the taxman's scanner – mandatory reporting

14

Threats China - Guidance issued on determination of beneficial owner French court decision could trigger imposition of tax on all cross-border restructurings

15

Competitors Malta - Parliament expands royalty and participation exemption Singapore tax authorities clarify non-taxation of companies' gains on disposal of equity investment Singapore: Home for billionaires and superstars Luxembourg rolls out the red carpet for alternative investment funds

16

Light at the end of the tunnel Denmark - Authorities rule EU parent is beneficial owner of deemed dividends Italy - Tax authorities loose beneficial ownership case

17

Opportunities China India Russia Brazil South Africa

18

Opportunities China India Russia Brazil South Africa

19

Opportunities China India Russia Brazil South Africa

20

Opportunities C I R B S

21

Structuring your tax affairs in the BRICS Strong focus on anti-avoidance Close collaboration to crack down on tax evasion Use of beneficial ownership concept and extended Black Lists Strict transfer pricing legislation Non-OECD members

22

Structuring your tax affairs in the BRICS Aggressive in tax enforcement and collection Taxation of indirect equity transfers (Vodafone & China’s circular 698) Non-OECD members – possible double taxation Shift from traditional holding company jurisdictions to jurisdictions with legitimate substance No one-size-fits-all

Non-OECD members – possible double taxation Shift from traditional holding company jurisdictions to jurisdictions with legitimate substance No one-size-fits-all")

23

The way forward Greater emphasis on Beneficial Ownership Increased economic and commercial substance Real decision making by directors

24

The way forward Continuous and proper compliance with local regulations Increased reporting obligation in operating locations Full transparency and exchange of information

25

Opportunities C I V E T s

26

Colombia Indonesia Vietnam Egypt Turkey

Similar presentations