Download presentation

Presentation is loading. Please wait.

1

experience support // CPAs & ADVISORS TAX UPDATE TAHFA April 18, 2014

2

AGENDA 501(r) Update Camp Tax Reform Legislation 2013 Form 990 Update Unrelated Business Income issues for health care organizations Foreign reporting issues for health care organizations 2

Update Camp Tax Reform Legislation 2013 Form 990 Update Unrelated Business Income issues for health care organizations Foreign reporting issues for health care organizations 2")

3

Section 501(r)(4)-(6) Update 3

(4)-(6) Update 3")

4

BACKGROUND 501(r) enacted March 23, 2010 Notice 2010-39 – IRS requested comments regarding new 501(r) requirements (May 27, 2010) Notice 2011-52 – IRS addressed CHNA requirement (July 8, 2011) Proposed Regulations on requirements described in 501(r)(4) – (r)(6) (June 22, 2012)

enacted March 23, 2010 Notice – IRS requested comments regarding new 501(r) requirements (May 27, 2010) Notice – IRS addressed CHNA requirement (July 8, 2011) Proposed Regulations on requirements described in 501(r)(4) – (r)(6) (June 22, 2012)")

5

BACKGROUND Proposed Regulations on requirements described in 501(r)(3) (April 5, 2013) Notice 2014-2 – IRS confirms that tax-exempt hospital organizations can rely on proposed regulations contained in notices of proposed rulemaking published June 26, 2012 and April 5, 2013 (December 30, 2013) Notice 2014-3 – IRS addressed procedures for hospital organizations to disclose and fix failures (December 30, 2013)

(3) (April 5, 2013) Notice – IRS confirms that tax-exempt hospital organizations can rely on proposed regulations contained in notices of proposed rulemaking published June 26, 2012 and April 5, 2013 (December 30, 2013) Notice – IRS addressed procedures for hospital organizations to disclose and fix failures (December 30, 2013)")

6

HOSPITAL FACILITIES Licensed, registered or similarly recognized by state as hospital May treat multiple buildings operated under single state license as single hospital facility Facilities outside U.S. are not required to comply Disregarded entities operating hospitals must comply Governmental hospitals with 501(c)(3) status must comply (several comments regarding applicability in public hearing) 6

(3) status must comply (several comments regarding applicability in public hearing) 6.")

7

IRC SECTION 501(R)(4) Financial Assistance Policy (FAP) Eligibility criteria Basis for calculating amounts charged Method for applying If no separate billing & collection policy exists, actions organization may take in event of nonpayment Measures to widely publicize policy Policy relating to emergency medical care 7

(4) Financial Assistance Policy (FAP) Eligibility criteria Basis for calculating amounts charged Method for applying If no separate billing & collection policy exists, actions organization may take in event of nonpayment Measures to widely publicize policy Policy relating to emergency medical care 7")

8

IRC SECTION 501(R)(4) Financial Assistance Policy (FAP) May publicize summary of FAP as certain information may change regularly (such as federal poverty references) No mandate for particular eligibility criteria Must state amounts, such as gross charges, to which any discount percentages will be applied 8

(4) Financial Assistance Policy (FAP) May publicize summary of FAP as certain information may change regularly (such as federal poverty references) No mandate for particular eligibility criteria Must state amounts, such as gross charges, to which any discount percentages will be applied 8")

9

SCHEDULE H, PART V-FINANCIAL ASSISTANCE POLICY

10

SCHEDULE H, PART V-EMERGENCY MEDICAL CARE

11

ELIGIBILITY CRITERIA & BASIS CALCULATING AMOUNTS CHARGED Must state that FAP eligible patient will not be charged more than amounts generally billed (AGB) for emergency or other medically necessary care Must state which of IRS permitted methods will be used to determine AGB Must either state % of gross charges hospital facility applies to determine AGB & how these AGB percentages were calculated or how members of public may readily obtain this information in writing free of charge 11

for emergency or other medically necessary care Must state which of IRS permitted methods will be used to determine AGB Must either state % of gross charges hospital facility applies to determine AGB & how these AGB percentages were calculated or how members of public may readily obtain this information in writing free of charge 11")

12

METHOD FOR APPLYING & ACTIONS TAKEN FOR NONPAYMENT Financial assistance may not be denied based on omission of information not specifically required by FAP or FAP application form Must describe actions that may be taken in event of nonpayment if no separate billing &collections policy exists Must describe process & time frames hospital will use in taking these actions, including reasonable efforts to determine if individual is FAP eligible Must describe who has final authority for determining hospital has made reasonable efforts 12

13

WIDELY PUBLICIZING Four types of measures required Measures taken to make paper copies of FAP, FAP application & plain language summary available (in English & language of minority populations comprising > 10% of hospital’s community) One commenter suggested a 5% or 500 patient threshold Public display measures Measures to inform & notify members of hospital’s community Measures to make FAP, application form & plain language summary available on website 13

One commenter suggested a 5% or 500 patient threshold Public display measures Measures to inform & notify members of hospital’s community Measures to make FAP, application form & plain language summary available on website 13")

14

ESTABLISHING FAP Authorized body must adopt policy & hospital must implement the policy Authorized body includes Governing body Committee of governing body permitted under state law to act on behalf of governing body Other parties authorized by governing body of hospital to act on its behalf 14

15

IRC SECTION 501(R)(5) 501(r)(5) – Limitation on Charges Limits amounts charged for emergency or other medically necessary care provided to individuals eligible for assistance under FAP to not more than amounts generally billed to individuals having insurance covering such care Prohibits use of gross charges 15

(5) 501(r)(5) – Limitation on Charges Limits amounts charged for emergency or other medically necessary care provided to individuals eligible for assistance under FAP to not more than amounts generally billed to individuals having insurance covering such care Prohibits use of gross charges 15")

16

SCHEDULE H, PART V-LIMITATIONS ON CHARGES

17

GROSS CHARGES May use gross charges as starting point to which discounts are applied Safe harbor provided for situations where individual does not complete FAP application before time of charges 17

18

LIMITATIONS ON CHARGES Must limit charges to FAP-eligible patients to not more than AGB to individuals with insurance covering that care & charges must be less than gross charges Two methods for computing AGB Look-back method Prospective method A hospital facility may use only one of the methods to determine AGB After choosing a particular method, a hospital facility must continue to use that method Claims paid under Medicare Advantage are treated as claims paid by private insurance 18

19

LOOK-BACK METHOD Based on actual claims paid (in full) to hospital by either Medicare fee-for-service only or Medicare fee-for-service together with all private health insurers paying claims Must calculate AGB percentages no less than annually by dividing sum of certain claims paid by sum of associated gross charges Calculated by multiplying gross charges by one or more AGB percentages 19

to hospital by either Medicare fee-for-service only or Medicare fee-for-service together with all private health insurers paying claims Must calculate AGB percentages no less than annually by dividing sum of certain claims paid by sum of associated gross charges Calculated by multiplying gross charges by one or more AGB percentages 19")

20

LOOK-BACK METHOD Must begin applying AGB percentages by 45 th day after end of 12-month period used in calculation (one commenter suggested a 75 – 90 day window to more closely coincide with revenue cycle) May calculate one average AGB percentage for all emergency and medically necessary care or multiple AGB percentages for separate categories of care as long as the hospital facility calculates an AGB percentages for all emergency and other medically necessary care 20

May calculate one average AGB percentage for all emergency and medically necessary care or multiple AGB percentages for separate categories of care as long as the hospital facility calculates an AGB percentages for all emergency and other medically necessary care 20")

21

PROSPECTIVE METHOD Determine AGB by using same billing & coding process hospital would use if individual were Medicare fee-for-service beneficiary 21

22

LIMITATION ON CHARGES Example On September 20 of year 1, X, a hospital facility, generates data on all claims paid to it in full for emergency or other medically necessary care by Medicare fee-for-service as the primary payer over the 12 months ending on August 31 of year 1. X determines that, of these claims for inpatient services, it received a total of $80 million from Medicare and another $20 million from Medicare beneficiaries in the form of co-insurance or deductibles. X’s gross charges for these inpatient claims totaled $250 million. Of the claims for outpatient services, X received a total of $100 million from Medicare and another $25 million from Medicare beneficiaries. X’s gross charges for these outpatient claims totaled $200 million. X calculates that its AGB percentage for inpatient services is 40 percent of gross charges ($100 million/$250 million) and its AGB percentage for outpatient services is 62.5 percent of gross charges ($125 million/$200 million). Between October 15 of year 1 (45 days after the end of the 12-month claim period ) and October 14 of year 2, X determines AGB for any emergency or other medically necessary inpatient care it provides to the FAP-eligible individual by multiplying the gross charges for the inpatient care it provides to the individual by 40% and AGB for any emergency or other medically necessary outpatient care it provides to a FAP-eligible individual by multiplying the gross charges for the outpatient care it provides to the individual by 62.5%.

and its AGB percentage for outpatient services is 62.5 percent of gross charges ($125 million/$200 million). Between October 15 of year 1 (45 days after the end of the 12-month claim period ) and October 14 of year 2, X determines AGB for any emergency or other medically necessary inpatient care it provides to the FAP-eligible individual by multiplying the gross charges for the inpatient care it provides to the individual by 40% and AGB for any emergency or other medically necessary outpatient care it provides to a FAP-eligible individual by multiplying the gross charges for the outpatient care it provides to the individual by 62.5%..")

23

IRC SECTION 501(R)(6) 501(r)(6) – Billing &Collection Requirement May not engage in extraordinary collection actions before organization has made reasonable efforts to determine whether individual is eligible for assistance 23

(6) 501(r)(6) – Billing &Collection Requirement May not engage in extraordinary collection actions before organization has made reasonable efforts to determine whether individual is eligible for assistance 23")

24

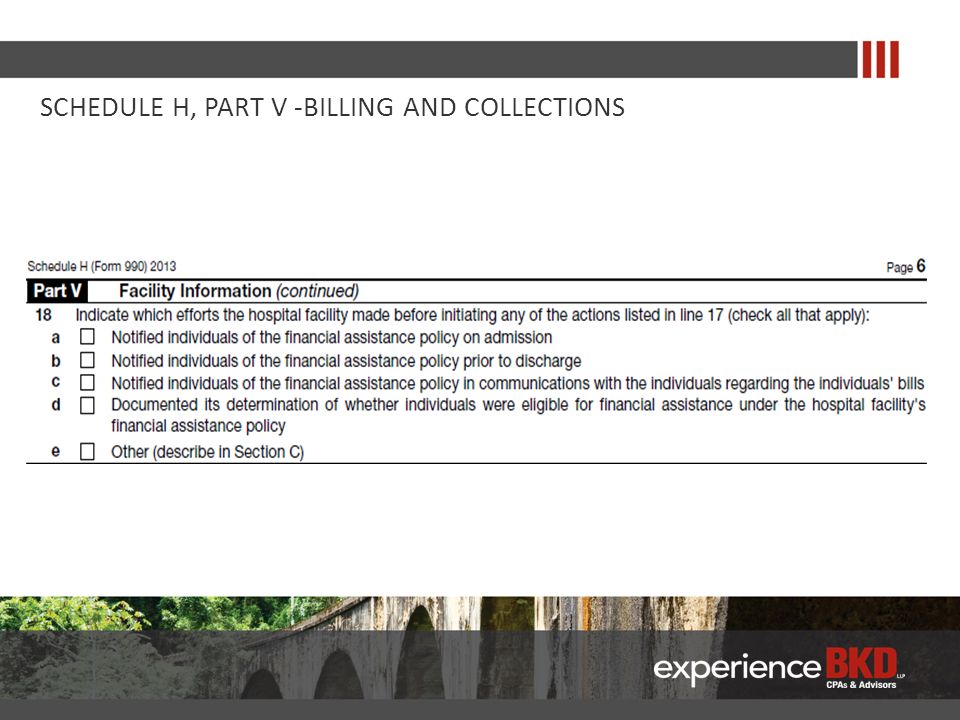

SCHEDULE H, PART V-BILLING AND COLLECTIONS

26

BILLING & COLLECTION Must engage in reasonable efforts to determine FAP eligibility before engaging in extraordinary collections actions (ECA) ECAs include Any action that requires legal or judicial process Reporting to credit agencies Sale of individual’s debt to another party 26

ECAs include Any action that requires legal or judicial process Reporting to credit agencies Sale of individual’s debt to another party 26")

27

REASONABLE EFFORTS Notify individual about FAP If individual provides incomplete application, provide them with information relevant to complete application Make & document determination as to whether individual is FAP-eligible 27

28

NOTIFICATION PERIOD Period in which hospital must notify individual about FAP Begins on date care is provided & ends on 120 th day after hospital provides first billing statement 28

29

APPLICATION PERIOD Must accept & process FAP applications during longer period that ends on 240 th day after hospital provides individual with first billing statement Many comments suggest this is too long 29

30

NOTIFICATION ABOUT FAP Must distribute plain language summary of FAP & offer an application before discharge Must distribute plain language summary of FAP with all (& at least 3) billing statements during notification period Must inform individual of FAP in all oral communications during notification period Must provide at least one written notice about ECAs hospital may initiate if individual does not submit FAP application or pay amount due by last day of notification period 30

billing statements during notification period Must inform individual of FAP in all oral communications during notification period Must provide at least one written notice about ECAs hospital may initiate if individual does not submit FAP application or pay amount due by last day of notification period 30")

31

PLAIN LANGUAGE SUMMARY Brief description of eligibility requirements & assistance offered Direct website address & physical location copies may be obtained Instructions on how to obtain free copy by mail Contact information Statement of availability of translations if applicable Statement that no FAP-eligible patient will be charged more than AGB 31

32

INCOMPLETE FAP APPLICATIONS If received during application period, hospital must Suspend ECAs when received Provide written notice that describes additional information needed Provide at least one written notice describing ECAs that may be initiated or resumed if individual does not complete by deadline that is no earlier than later of 30 days from written notice or last day of application period 32

33

COMPLETE FAP APPLICATIONS If received during application period, hospital must Provide billing statement indicating amount owed Refund any excess payments made by individual Take all reasonably available measures to reverse any ECA 33

34

BILLING AND COLLECTION Example Individual A receives care from hospital facility T on February 1 and February 2. When A is discharged from T on February 2, T gives A its FAP application form and a plain language summary of its FAP. On March 1, April 15, and May 30, T sends A billing statements that include a one-page insert that provides a plain language summary of the FAP. With the May 30 billing statement, T also includes a letter that informs A that if she does not pay the amount owed or submit a FAP application form by June 29 (120 days after the first billing statement was provided on March 1), T may report A’s delinquency to credit reporting agencies, seek to obtain a judgment against A, and, if such a judgment is obtained, seek to attach and seize A’s bank account or other personal property, which are the only ECAs that T (or any party to which T refers A’s debt) may take in accordance with T’s billing and collections policy. T does not have any other written or oral communications with A about her bill before June 29. T keeps electronic records showing that it provided a plain language summary and FAP application to A on discharge and included the letter regarding ECAs and the plain language summaries with the billing statements sent to A. A does not submit a FAP application form by June 29. T has made reasonable efforts to determine whether A is FAP-eligible, and thus may engage in ECAs against A, as of June 30.

, T may report A’s delinquency to credit reporting agencies, seek to obtain a judgment against A, and, if such a judgment is obtained, seek to attach and seize A’s bank account or other personal property, which are the only ECAs that T (or any party to which T refers A’s debt) may take in accordance with T’s billing and collections policy. T does not have any other written or oral communications with A about her bill before June 29. T keeps electronic records showing that it provided a plain language summary and FAP application to A on discharge and included the letter regarding ECAs and the plain language summaries with the billing statements sent to A. A does not submit a FAP application form by June 29. T has made reasonable efforts to determine whether A is FAP-eligible, and thus may engage in ECAs against A, as of June 30..")

35

BILLING AND COLLECTION Example Assume the same facts in previous example but A submits an incomplete FAP application to T on October 13, two weeks before the last day of the application period on October 27 (240 days after the first billing statement was provided on March 1). Eligibility for assistance under T’s FAP is based solely on an individual’s family income and the instructions to T’s FAP application form require applicants to attach certain documentation verifying family income to their application form. The FAP application form that A submits to T on October 14 includes all of the required income information, but A fails to attach the required documentation verifying her family income. After receiving A’s incomplete FAP application on October 13, T does not initiate any new ECAs against A and does not take any further action on the ECAs T previously initiated against A. On October 15, a member of T’s staff calls A to inform her that she failed to attach any of the required documentation of her family income and explain what kind of documentation A needs to submit and how she can submit it. On October 16, T sends a letter to A explaining the kind of documentation of family income that A must provide to T to complete her application and informing A about the ECAs that T (or any other authorized party) may initiate or resume against A if A does not submit the missing documentation or pay the amount due by November 15 (30 days after October 16). T includes a plain language summary of the FAP with the letter.

may initiate or resume against A if A does not submit the missing documentation or pay the amount due by November 15 (30 days after October 16). T includes a plain language summary of the FAP with the letter..")

36

ISSUES Guidance before release of Proposed Regulations was vague Requirements have been in place since March 23, 2010 May rely on, but not required to comply with the Proposed Regulations No word on anticipated release date for Final Regulations 36

37

Section 501(r) CHNA Update 37

CHNA Update 37")

38

Affordable Care Act Section 501(r) IRS Notice 2011-52 Creates Section 501(r) Creates Section 4959 CHNA Required Once Every Three Years Community Input Required $50,000 Excise Tax for Non-Compliance ACA Requirements –> CHNA–> Notice 2011-52 –>Proposed Regulations 38 Notice 2011- 52 Proposed Regulations Provides more detailed guidance May rely upon currently Some transitional relief Provides initial guidance May rely upon for reports widely available before 10/5/2013

IRS Notice Creates Section 501(r) Creates Section 4959 CHNA Required Once Every Three Years Community Input Required $50,000 Excise Tax for Non-Compliance ACA Requirements –> CHNA–> Notice –>Proposed Regulations 38 Notice Proposed Regulations Provides more detailed guidance May rely upon currently Some transitional relief Provides initial guidance May rely upon for reports widely available before 10/5/2013")

39

TIMING CHNA must be conducted once every three years for community served by each hospital – first must be completed by end of tax year beginning after March 23, 2012 39 Summary of Initial Cycle for CHNA Year End Beginning of Fiscal Year Due Date for Initial CHNA 03/31/201204/01/201203/31/2013 06/30/201207/01/201206/30/2013 09/30/201210/01/201209/30/2013 12/31/201201/01/201312/31/2013 01/31/201302/01/201401/31/2014

40

TIMING/TRANSITIONAL RELIEF Implementation Strategy Required document addressing the needs identified in the CHNA Must be adopted by the governing board (or body authorized by the governing board) before the end of the year in which the CHNA is adopted Must be attached to Form 990 filed for the same year Proposed Regulations Allows organizations to delay adoption of the Implementation Strategy to the ORIGINAL due date of the organization’s Form 990 Applies only to the first year of the CHNA cycle/Does not apply to future CHNA years Allows for organizations to provide the URL of the web page on which the Implementation Strategy was widely available in lieu of attaching the Implementation Strategy to Form 990 (form instructions does not address this) 40

before the end of the year in which the CHNA is adopted Must be attached to Form 990 filed for the same year Proposed Regulations Allows organizations to delay adoption of the Implementation Strategy to the ORIGINAL due date of the organization’s Form 990 Applies only to the first year of the CHNA cycle/Does not apply to future CHNA years Allows for organizations to provide the URL of the web page on which the Implementation Strategy was widely available in lieu of attaching the Implementation Strategy to Form 990 (form instructions does not address this) 40")

41

DEFINITION OF COMMUNITY Consistent with Notice 2011-52 Provide flexibility to take into account all of the relevant facts and circumstances in defining the community served, including the geographic area served, target populations served, and principal functions May include areas outside of those in which the organization’s patient populations reside May NOT define the organization’s community in a way that excludes medically underserved, low-income, or minority populations who are part of the organization’s patient population, live in geographic areas in which the patient population resides, or otherwise should be included based on the method used to determine the organization’s community 41

42

IDENTIFICATION AND PRIORITIZATION OF IDENTIFIED NEEDS Regulations clarify that CHNAs: Need only to identify significant health needs Need only to prioritize, and otherwise assess, those significant needs identified Needs are significant based on facts and circumstances present in the community served by the hospital No particular method prescribed to prioritize needs, but IRS suggests: Burden, scope, severity or urgency of the health need Estimated feasibility and effectiveness of possible interventions Health disparities associated with the need Importance the community places on addressing the need 42

43

BROAD INTEREST OF THE COMMUNITY INPUT Regulations specifically require hospitals take into account input (at a minimum) from: At least one state, local, tribal or regional governmental public health department with knowledge or expertise relevant to the health needs of the community Members of medically underserved, low-income, and minority populations in the community or individuals or organizations serving or representing the interests of such populations Written comments received on the hospital facility’s most recently conducted CHNA and most recently adopted implementation strategy (no requirement to post a draft CHNA for public comment) Notice 2011-52 Includes an addition requirement to include input from persons with special knowledge or expertise in public health 43

from: At least one state, local, tribal or regional governmental public health department with knowledge or expertise relevant to the health needs of the community Members of medically underserved, low-income, and minority populations in the community or individuals or organizations serving or representing the interests of such populations Written comments received on the hospital facility’s most recently conducted CHNA and most recently adopted implementation strategy (no requirement to post a draft CHNA for public comment) Notice Includes an addition requirement to include input from persons with special knowledge or expertise in public health 43")

44

DOCUMENTATION CHNA must be documented in a report, adopted by an authorized body of the governing body, and must include: Definition of the community served by the hospital and a description of how the community was determined Description of the processes and methods used to conduct the CHNA Description of how the hospital took into account input from persons who represent the broad interest of the community it serves Prioritized listing of significant health needs of the community and a description of the process and criteria used in identifying certain needs as significant and prioritizing such significant needs Description of potential measures and resources identified through the CHNA process to address the significant health needs 44

45

DESCRIPTION OF PROCESS AND METHODS Requirements are met if the CHNA report: Describes the data and other information used in the assessment, as well as the methods of collecting and analyzing this data and information Identifies any parties with whom the hospital facility collaborated with, or with whom it contracted for assistance, in conducting the CHNA 45

46

DESCRIPTION OF COMMUNITY INPUT Proposed regulations clarify: Report may summarize how and over what time community input was gathered Report may include a general summary of input received Report does not need to name or otherwise individually identify any individuals participating in community forums, focus groups, survey samples or similar groups 46

47

COLLABORATION Every hospital facility must document its CNHA in a separate CHNA report If collaborating with other facilities or organizations in conducting its CHNA or basing its CHNA, in part, on a CHNA for all or part of its community conducted by another organization, portions of the hospital’s CHNA report may be substantially identical to the report of a collaborating facility or organization, if appropriate under the facts and circumstances Collaborating hospital facilities may produce a joint CHNA report as long as all of the facilities define their community to be the same and conduct a joint CHNA process. The joint report must clearly identify each hospital facility to which it applies and an authorized body of each collaborating hospital facility must adopt the joint CHNA as its own 47

48

MAKING THE CHNA WIDELY AVAILABLE To be made widely available the CHNA must be posted on the hospital facility’s website (or the hospital organization’s website) if the facility does not have a separate website Must be accessible for viewing and printing without the need for special software (software not generally available to the public without payment of any fee) Individuals asking how to access the CHNA online must be provided with the direct website address or URL of the webpage where the CHNA is posted Regulations add: Complete copy of the CHNA must be conspicuously posted on the website CHNA must remain on the website until two subsequent CHNA reports have been posted Individuals must not be required to create an account to access the CHNA Paper copy must be available without charge until the two subsequent CHNA copies are available 48

if the facility does not have a separate website Must be accessible for viewing and printing without the need for special software (software not generally available to the public without payment of any fee) Individuals asking how to access the CHNA online must be provided with the direct website address or URL of the webpage where the CHNA is posted Regulations add: Complete copy of the CHNA must be conspicuously posted on the website CHNA must remain on the website until two subsequent CHNA reports have been posted Individuals must not be required to create an account to access the CHNA Paper copy must be available without charge until the two subsequent CHNA copies are available 48")

49

IMPLEMENTATION STRATEGY Health needs covered in the implementation strategy are limited to the significant health needs identified in the CHNA Regulations do not require a hospital to address every significant health need identified With respect to each significant health need identified, the implementation strategy must either: Describe how the hospital facility plans to address the health need, or Identify the health need as one the hospital does not intend to address and explain why the hospital does not intend to address the need Implementation strategy must identify programs and resources the hospital facility plans to commit to address the health needs Implementation strategy must describe any planned collaboration between the hospital facility and other facilities addressing the health need 49

50

IMPLEMENTATION STRATEGY Implementation Strategy must also describe the anticipated impact of the actions the hospital plans to take and the hospital’s plan to evaluate such impact Hospital facilities must establish an ongoing feedback mechanism that requires a hospital facility to take into account written comments received on its most recently adopted implementation strategy when conducting a CHNA Implementation strategies may be developed in collaboration with other facilities and organizations. However, the hospital facility must document its Implementation Strategy in a separate written plan that is tailored to the hospital facility 50

51

IMPLEMENTATION STRATEGY Joint Implementation Strategies allowed if the report: Is clearly identified as applying to the hospital facility Clearly identifies the hospital facility’s particular role and responsibilities in taking the actions described in the implementation strategy and the programs and resources the hospital facility plans to commit in taking those actions Includes a summary or other tool that helps the reader easily locate those portions of the joint implementation strategy that relates to the hospital facility 51

52

NEWLY CREATED OR ACQUIRED HOSPITAL FACILITIES A Hospital facility that becomes subject to 501(r) because the hospital organization is newly recognized as described in section 501(c)(3) must conduct a CHNA and adopt an implementation strategy by the last day of the second taxable year beginning after the date the hospital facility is acquired or placed into service, or newly subject to 501(r) Short taxable years of less than twelve months are considered a tax year for purposes of section 501(r) 52

because the hospital organization is newly recognized as described in section 501(c)(3) must conduct a CHNA and adopt an implementation strategy by the last day of the second taxable year beginning after the date the hospital facility is acquired or placed into service, or newly subject to 501(r) Short taxable years of less than twelve months are considered a tax year for purposes of section 501(r) 52")

53

NEWLY CREATED OR ACQUIRED HOSPITAL FACILITIES Example Hospital A is organized as a new organization exempt from tax under IRC Section 501(c)(3) on May 1, 2012. Hospital A elects to have a September 30 year end for tax and financial reporting purposes. Short year May 1, 2012 – September 30, 2012 = First year Taxable year October 1, 2012 – September 30, 2013 = First year beginning after 5/1/2012 Taxable year October 1, 2013 – September 30, 2014 = Second year beginning after 5/1/2012 First CHNA and Implementation strategy are due on or before September 30, 2014 53

54

EXCISE TAX Excise Tax Computed under Section 4959 of the code $50,000 excise tax due for failure to comply with the CHNA and/or Implementation Strategy rules Applies each year the hospital facility is not in compliance Applies separately to each hospital facility that is not in compliance 54

55

EXCISE TAX CHNA under Notice 2011-52 CHNAs and implementation strategies following the guidance under Notice 2011-52 must be adopted on or before October 5, 2013 After October 5, 2013 Notice 2011-52 becomes obsolete CHNA under Proposed Regulations May rely upon the proposed regulations beginning April 3, 2013 and until 60 days after final or temporary regulations are published 55

56

Section 501(r) Other Matters 56

Other Matters 56")

57

NOTICE 2014-3 Proposed revenue procedure that is intended to allow hospital organizations to disclose and fix failures to meet 501(r) Only applies to failures that are not egregious and willful Proposed regulations added insight on enforcement Three types of failures Minor Not Minor/Not Willful Willful and Egregious

Only applies to failures that are not egregious and willful Proposed regulations added insight on enforcement Three types of failures Minor Not Minor/Not Willful Willful and Egregious")

58

NOTICE 2014-3 General A hospital organization may rely on proposed regulations to correct and disclose any failure that is not willful and egregious The hospital organization must have begun correcting the failure and disclosed the failure before the hospital organization has been contacted by the IRS concerning an examination

59

NOTICE 2014-3 A failure that is willful includes a failure due to gross negligence, reckless disregard, or willful neglect. A hospital organizations correction and disclosure of a failure does not create a presumption that the failure was not willful or egregious

60

NOTICE 2014-3 Restoration of affected persons Correction should be made with respect to each affected person Correction should restore the affected person(s) to the position they would have been if the failure had not occurred

to the position they would have been if the failure had not occurred")

61

NOTICE 2014-3 Reasonable and appropriate correction The correction should be reasonable and appropriate for the failure Depending on the failure there maybe more than one reasonable and appropriate correction Timing The correction should be made as promptly after discovery as possible given the nature of the failure

62

NOTICE 2014-3 Implementation/modification of safeguards If the hospital organization has not established practices and procedures that are designed to achieve compliance with 501(r), the hospital organization should establish practices and procedures as part of the correction process If the hospital organization has established practices and procedures that are designed to achieve compliance with 501(r) and failed to identify the failure, the hospital organization should determine what changes need to occur to reduce the likelihood of another failure

, the hospital organization should establish practices and procedures as part of the correction process If the hospital organization has established practices and procedures that are designed to achieve compliance with 501(r) and failed to identify the failure, the hospital organization should determine what changes need to occur to reduce the likelihood of another failure")

63

NOTICE 2014-3 Disclosure A description of the failure A description of the discovery A description of the correction made A description of the practices and procedures

64

Camp Tax Reform Legislation 64

65

CAMP DRAFT LEGISLATION Released February 2014 1,000 pages long Five topics of interest for tax exempt hospitals

66

CAMP DRAFT LEGISLATION Charitable Contributions Establishes 2% floor on individual tax returns Election to treat charitable contributions made after the close of the tax year but before due date of the return as made in the tax year Limits charitable contribution of appreciated property to the taxpayer’s basis Simplifies income limitations on deductible charitable contributions

67

CAMP DRAFT LEGISLATION Unrelated Business Income Tax Subjects all exempt entities (501(a)) to UBIT not withstanding exemption under another code section (115 for governmental organizations) Sale or licensing of the EO’s name or logo would be UBI (subjects royalties received to UBIT) Compute UBIT separately for each line of business (losses from one activity can not offset income from another activity) Limits exclusion for fundamental research to income derived from publicly available research Modifies exclusion for qualified sponsorship payments Accuracy related penalty for understatements imposed on any officer, director, trustee, employee or other individual whose duties relate to the underpayment

) to UBIT not withstanding exemption under another code section (115 for governmental organizations) Sale or licensing of the EO’s name or logo would be UBI (subjects royalties received to UBIT) Compute UBIT separately for each line of business (losses from one activity can not offset income from another activity) Limits exclusion for fundamental research to income derived from publicly available research Modifies exclusion for qualified sponsorship payments Accuracy related penalty for understatements imposed on any officer, director, trustee, employee or other individual whose duties relate to the underpayment")

68

CAMP DRAFT LEGISLATION Elimination of Rebuttable Presumption of Reasonableness Entity level excise tax of 10% on any excess benefit transaction where minimum levels of due diligence were not followed: Approval by an independent body Reliance on appropriate comparability data Concurrent documentation of the basis for approval Above steps no longer giver rise to a presumption of reasonableness Safe harbor for organization managers who rely on professional advise eliminated

69

CAMP DRAFT LEGISLATION Excise Tax on Excess Tax-Exempt Organization Executive Compensation Excise tax on employers equal to 25% of remuneration in excess of $1 million paid to a covered employee Applies to excess parachute payments (even if payment does not exceed $1 million) Covered employee is one of the five highest compensated employees of the organization (includes former employees) for the current or any preceding tax year

Covered employee is one of the five highest compensated employees of the organization (includes former employees) for the current or any preceding tax year")

70

CAMP DRAFT LEGISLATION Tax Exempt Bonds Repeals exclusion from gross income interest paid on: Private activity bonds Advance refunding bonds

71

Form 990 Update 2013 71

72

2013 FORM 990 Filed for years beginning in 2013 Calendar year end 12/31/2013 Fiscal years ending in 2014 Significant Changes No significant changes Mostly clarifications to instructions BKD webinar highlighting all changes http://www.bkd.com/webinars/2014/an-update-on-irs-form-990.htm Archived for viewing

73

SCHEDULE H Part I, Line 7 Community Benefit Table Report restricted grants received to be used for community benefit as direct offsetting revenue in column d Part I, Line 7i and Worksheet 8 allow reporting of contributions for community benefit funded in whole or in part by a restricted grant from a related organization Instructions clarify that financial assistance does not include self- pay or prompt pay discounts

74

SCHEDULE H Part V, Section A requires state license number for each facility For each separate Part V, Section B completed Part V, Section C must be completed Part V, Section B adds residency as a possible factor considered in calculated amounts charged to patients

75

Unrelated Business Income Tax Issues for Heath Care Organizations 75

76

76 UNRELATED BUSINESS INCOME Exempt organizations face increasing pressure to raise revenue through alternative or innovative programs. Programs are often not directly related to the organization’s exempt purpose and may be subject to the unrelated business income tax. Unrelated business income must be reported on Form 990-T if there is $1,000 or more of gross unrelated business income. IRS continues to focus on loss activities

77

UNRELATED BUSINESS INCOME FOR ALTERNATIVE INVESTMENTS Alternative investments, such as distressed debt, natural resources and private equity are frequently held in a partnership type structure These investments generate Schedule K-1s to report a partner’s share of income or loss which also indicates unrelated business income generated by the underlying investments This income or loss is reported on Form 990-T and may also require filing in multiple states Additionally, Schedule K-1 may disclose information related to transfers to foreign entities which may require additional reporting requirements 77

78

RISK AREAS OF UNRELATED BUSINESS INCOME FOR HEALTH CARE ORGANIZATIONS The IRS continues to scrutinize operations of health care organizations. Common risk areas for unrelated business income include services performed for the benefit of nonpatients including: Pharmacy services Reference lab services Laundry services Catering and food services In addition, healthcare organizations should evaluate: Investments in alternative investments, such as private equity, limited partnerships or foreign corporations may be producing UBI. Allocation of the organization’s expenses against UBI. Annual losses being generated for activities classified as UBI may lack profit motive. 78

79

Foreign Reporting Issues for Health Care Organizations 79

80

80 FORM 990 SCHEDULE F STATEMENT OF ACTIVITIES OUTSIDE THE U.S. Office, employees or agents outside U.S. Aggregate revenue or expenses of more than $10,000 from or attributable to grantmaking, fundraising activities, business, investments & program service activities outside U.S. Schedule F Part I General Information Beginning in 2010, investment book value is reported Activities to report include travel to & from region for board meeting, seminars or site visits Schedule F Part IV Foreign Forms

81

81 FORM 990 SCHEDULE F STATEMENT OF ACTIVITIES OUTSIDE THE U.S. Added questions if forms are required to be filed for Transfer of property to foreign corporation (Form 926) Interest in foreign trust (Form 3520 &/or Form 3520-A) Ownership interest in foreign corporation (Form 5471) Direct or indirect shareholder of passive foreign investment company (Form 8621) Ownership interest in foreign partnership (Form 8865) Operations in or related to any boycotting countries (Form 5713)

Interest in foreign trust (Form 3520 &/or Form 3520-A) Ownership interest in foreign corporation (Form 5471) Direct or indirect shareholder of passive foreign investment company (Form 8621) Ownership interest in foreign partnership (Form 8865) Operations in or related to any boycotting countries (Form 5713).")

82

82 COMMON INTERNATIONAL TAX ISSUES AFFECTING EXEMPT ORGS Reporting requirements for foreign alternative investments & accounts Alternative investment choices involving foreign “blocker” corporations Withholding tax & reporting on payments to foreign persons Transfer pricing on transactions between related taxable & nontaxable entities [not discussed in this presentation] Foreign taxation of foreign entities/operations [not discussed in this presentation] Individual income tax & payroll taxes associated with foreign national employees & U.S. employees working outside U.S. [not discussed in this presentation]

![82 COMMON INTERNATIONAL TAX ISSUES AFFECTING EXEMPT ORGS Reporting requirements for foreign alternative investments & accounts Alternative investment choices involving foreign blocker corporations Withholding tax & reporting on payments to foreign persons Transfer pricing on transactions between related taxable & nontaxable entities [not discussed in this presentation] Foreign taxation of foreign entities/operations [not discussed in this presentation] Individual income tax & payroll taxes associated with foreign national employees & U.S.](http://images.slideplayer.com/18/6197807/slides/slide_82.jpg "employees working outside U.S. [not discussed in this presentation].")

83

83 REPORTING REQUIREMENTS FOR FOREIGN INVESTMENTS & ACCOUNTS All private foundations, hospitals & other exempt organizations should carefully review each of their direct & indirect investments to determine if reporting requirements apply Significant penalty (in some cases criminal) can apply for failure to report foreign investments & accounts

can apply for failure to report foreign investments & accounts")

84

84 REPORTING REQUIREMENTS FOR FOREIGN INVESTMENTS & ACCOUNTS Foreign corporations Form 926, Return by U.S. Transferor of Property to Foreign Corporation – Capital contributions of $100,000 or more cash or any property if own 10% or more of the foreign corporation Form 5471, Information Return of U.S. Person with Respect to Certain Foreign Corporations – Ownership of 10% or more of certain foreign corporations Form 8621, Return by Shareholder of Passive Foreign Investment Company or Qualified Electing Fund. Generally not required to be filed by tax-exempt organizations unless investment is debt financed resulting in dividends from PFIC that are unrelated business taxable income

85

85 REPORTING REQUIREMENTS FOR FOREIGN INVESTMENTS & ACCOUNTS Foreign partnerships Form 8865, Return of U.S. Persons with Respect to Certain Foreign Partnerships – Ownership of 10% or more of certain foreign partnerships and capital contributions of $100,000 or more cash to foreign partnerships Foreign bank accounts Form FinCEN 114 (formerly TDF 90-22.1), Report of Foreign Bank & Financial Accounts (FBAR) – Financial interest in, signatory authority or other authority over any financial account in foreign country & aggregate value of account exceeds $10,000 at any time during year

, Report of Foreign Bank & Financial Accounts (FBAR) – Financial interest in, signatory authority or other authority over any financial account in foreign country & aggregate value of account exceeds $10,000 at any time during year.")

86

86 PENALTIES Forms 8865 & Form 5471 - $10,000 per failure to file. Can toll statute of limitations for entire tax return Form 926 and 8865 Category 3 - 10% of fair market value of property contributed up to $100,000 for failure to report contribution to foreign corporation or foreign partnership FBAR - $10,000 for each non-willful negligent violation, $100,000 or 50% of account value for each willful violation, criminal penalties of up to $500,000 & 10 years in prison or both Penalties can generally be waived for reasonable cause

87

87 EXPANSION OF PFIC REPORTING UNDER HIRE ACT Hiring Incentives to Restore Employment (HIRE) Act signed into law on March 18, 2010 New IRC Section 1298(f) requires U.S. persons owning shares in a PFIC to file an annual information return disclosing their ownership of the PFIC Alternative investments that are foreign “blocker” corporations are most likely considered PFICs Provision effective March 18, 2010, but IRS has suspended Section 1298(f) reporting until regulations are issued and a revised Form 8621 is released.

reporting until regulations are issued and a revised Form 8621 is released..")

88

88 ALTERNATIVE INVESTMENT CHOICES INVOLVING FOREIGN “BLOCKER” CORPS Frequently an alternative investment will set up two types of investment vehicles for its investors: A partnership designed mainly for its U.S. taxable investors to avoid the PFIC rules and to reduce withholding taxes on investment income A foreign “blocker” corporation or LP incorporated in a tax- haven country such as Cayman Islands, Bermuda, or British Virgin Islands designed for its U.S. tax exempt investors to “block” UBI and also designed for its non-U.S. investors to block ECI.

89

89 ALTERNATIVE INVESTMENT CHOICES INVOLVING FOREIGN “BLOCKER” CORPS While blocking UBI may sound like a good idea, it may not always be the best investment choice because of the additional tax burden that is imposed on tax-haven entities: Generally no reduction of foreign withholding taxes on foreign source interest and dividend income is available to a tax-haven entity or any of its investors under any income tax treaty 30% U.S. withholding tax imposed on a tax-haven entity on U.S. source interest and dividend income A tax-haven corporation’s income that is effectively connected to a U.S. trade or business is subject to U.S. corporate income and branch profits taxes

90

90 ALTERNATIVE INVESTMENT CHOICES INVOLVING FOREIGN “BLOCKER” CORPS A U.S. partnership, on the other hand, is not subject to U.S. corporate income taxes and is not subject to U.S. withholding taxes on U.S. source investment income allocated to its U.S. partners. A U.S. partnership also may be able to claim reduced rates of foreign withholding taxes on foreign source investment income under income tax treaties to the extent the income is allocated to its U.S. partners. The obvious down-side is that a U.S. partnership can allocate UBI to its U.S. tax-exempt partners on Schedule K-1

91

91 ALTERNATIVE INVESTMENT CHOICES INVOLVING FOREIGN “BLOCKER” CORPS The financial burden of the additional taxes imposed on a tax-haven entity’s investment income as compared to a U.S. partnership generally will be borne by the investors of the tax-haven entity via reduced returns on investment. Rather than always going with the foreign “blocker” alternative investment choice, a tax-exempt organization should weigh the effects of having UBI flow through on a Schedule K-1 under the U.S. partnership investment regime against the effects of reduced returns on investment from additional withholding taxes imposed under the foreign blocker investment regime. For example, if a tax-exempt organization has significant NOL carryovers for UBIT purposes, a U.S. partnership investment is likely the better investment choice over the foreign blocker investment.

92

92 WITHHOLDING TAX & REPORTING ON PAYMENTS TO FOREIGN PERSONS Certain payments by U.S. persons to foreign persons are required to be reported on Forms 1042, 1042-S, and 1042-T, and may be subject to U.S. withholding tax Payments to foreign persons subject to reporting and possible U.S. withholding tax include interest, rents, royalties, compensation for independent services performed in the U.S., annuities, pension distributions, gambling winnings, prizes and awards, etc.

93

DISCLOSURES These discussions and conclusions are based on the facts as stated and existing authorities as of the date of this communication. Our advice could change as a result of changes in applicable laws and regulations. We are under no obligation to update this communication if such changes occur. Any advice should be based on your unique facts and circumstances as you communicated them to us and should not be used or relied on by anyone else. Tax professionals that practice before the IRS are required to adhere to certain professional standards prescribed by the Department of Treasury and the IRS. These standards require us to include the following statement in certain written federal tax advice: This advice is not intended or written to be used, and it cannot be used, for the purpose of avoiding penalties that may be imposed. 93

94

THANK YOU FOR MORE INFORMATION // For a complete list of our offices and subsidiaries, visit bkd.com or contact: Paige Gerich, CPA// Partner pgerich@bkd.com // 713-499-4639

Similar presentations

Regulations Pete Gautreau, CPA Partner Danielle Witten, CPA Senior Manager.>")

298-5804>")

Regulations and.>")

Final Regulations.>")