Download presentation

Presentation is loading. Please wait.

1

International Business, Diversity and Comparative Accounting

2

International Business

All business transactions that involve two or more countries Reasons Expand sales due to excess capacity or small domestic markets Gain access to production factors including Raw materials Cheaper labor Knowledge Protect domestic markets Protect foreign markets

3

Forms of International Involvement

Exports and Imports Largest Importers and exporters - U.S., China, Germany, Japan, France, U.K., Netherlands Tennessee Trade Strategic Alliances - Licensing agreements Franchising Joint Ventures Foreign Direct Investment Portfolio Investment

4

Characteristics of National Economies

Gross Domestic Product (GDP) – Value of new goods and services produced within a country (produced by its citizens and non-residents) GDP per capita – Crude measure of the standard of living in a country; ratio of that country’s GDP to its population.

– Value of new goods and services produced within a country (produced by its citizens and non-residents) GDP per capita – Crude measure of the standard of living in a country; ratio of that country’s GDP to its population.")

5

Gross Domestic Product per Capita (est. 2013)

Qatar $102,100 United States (14th) $52,800 Canada $43,100 Germany $39,500 United Kingdom $37,300 Japan $37,100 Russia $18,100 Mexico $15,600 China $ 9,800

$52,800. Canada $43,100. Germany $39,500. United Kingdom $37,300. Japan $37,100. Russia $18,100. Mexico $15,600. China $ 9,800.")

6

Gross Domestic Product (GDP) (est. 2013)

U.S. – $16.72 trillion (319 million population) China - $13.39 trillion (1.4 billion population) India – $4.99 trillion (1.2 billion population) Japan - $4.73 trillion (127 million population) Germany - $3.23 trillion (81 million population) Russia – $2.55 trillion (143 million population) Brazil - $2.42 trillion (203 million population) U.K. - $2.38 trillion (64 million population) France - $2.28 trillion (66 million population)

China - $13.39 trillion (1.4 billion population) India – $4.99 trillion (1.2 billion population) Japan - $4.73 trillion (127 million population) Germany - $3.23 trillion (81 million population) Russia – $2.55 trillion (143 million population) Brazil - $2.42 trillion (203 million population) U.K. - $2.38 trillion (64 million population) France - $2.28 trillion (66 million population)")

7

Global Corporate Strategy

Polycentric attitude All operating policies and procedures must be adjusted to the local environment Accounting is more decentralized. Ethnocentric attitude Everything the multinational enterprise does in the home country can be transferred to the foreign country, in spite of the environmental differences Accounting is more centralized.

8

Accounting Diversity Differences exist everywhere!

Language Currency Terminology Reports required – group/parent Report formats Measurement practices Disclosure practices Level of detail Relevance of statements Balance sheet more important Income sheet more important

9

Reasons for Accounting Diversity

Accounting reflects characteristics of its national environment Environmental variables influence and help explain why business is conducted differently in different countries Cultural relativism: the rationality of any behavior should be judged in terms of its own cultural context

10

Environmental Influences

Legal system Civil versus common law Rules based or judgment/precedent oriented How it affects accounting regulation Standard setting in public or private sector Accounting Profession How influential the profession is in the business world Formalization of accounting standards Economics Providers of Financing Banks and family members versus public debt and equity Degree of capital market development Institutional versus individual investors

11

Environmental Influences

Taxation Requirements that financial income must equal taxable income Inflation Must be accounted for if it is a problem Will influence financial reporting if present Political and Economic Ties Political systems Central planning versus private enterprise Accounting regulation Enforcement of standards

12

Environmental Influences

International factors Trade Influences Colonial influences Regional trade blocs Social climate Attitudes toward work, management, employee involvement, wealth, religion Value systems and attitudes often measured by Hofstede’s Cultural values Study conducted in 1980s Looked at the structural elements of culture that affect behavior in work Evaluated values of IBM employees in 50 countries

13

Cultural Influences - Hofstede’s Studies

Basic Value Systems Individualism vs. Collectivism Power Distance (Large vs. Small) Uncertainty Avoidance (Strong vs. weak) Masculinity vs. Femininity Short-term vs. Long-term orientation

Uncertainty Avoidance (Strong vs. weak) Masculinity vs. Femininity. Short-term vs. Long-term orientation.")

14

Hofstede’s Cultural Variables

Country US Canada UK Mexico Japan Germany Individualism/ Collectivism 1 4 3 32 22 15 Large Power Distance 38 39 42 5 33 Strong Uncertainty Avoidance 43 41 47 18 7 29 Masculinity vs. Femininity 24 9 6 Short-term /Long-term orientation 14 17 N/A 11

15

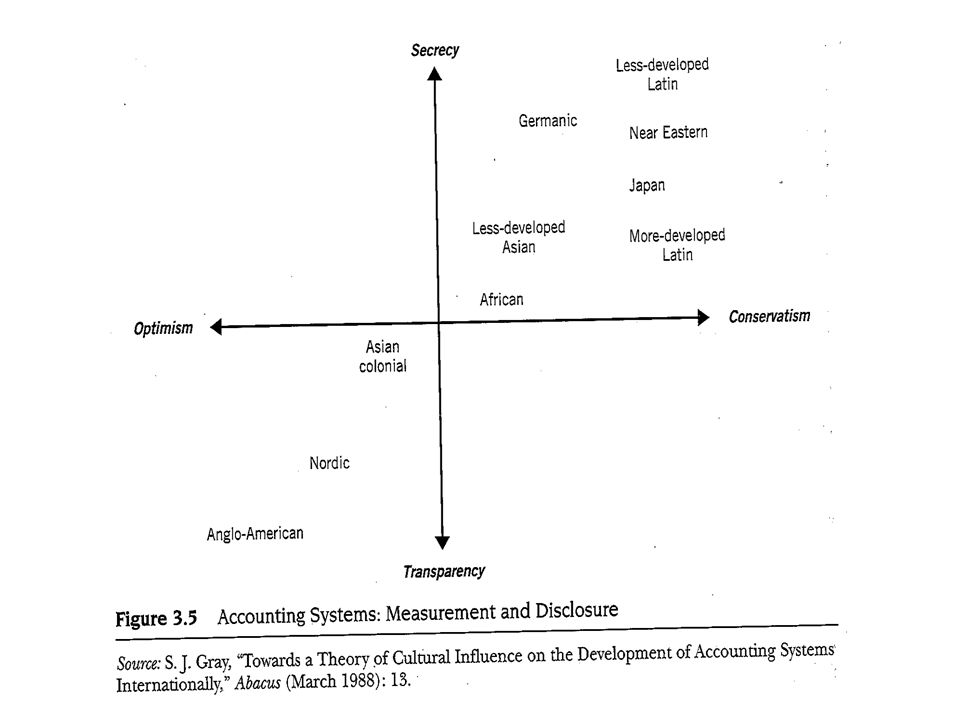

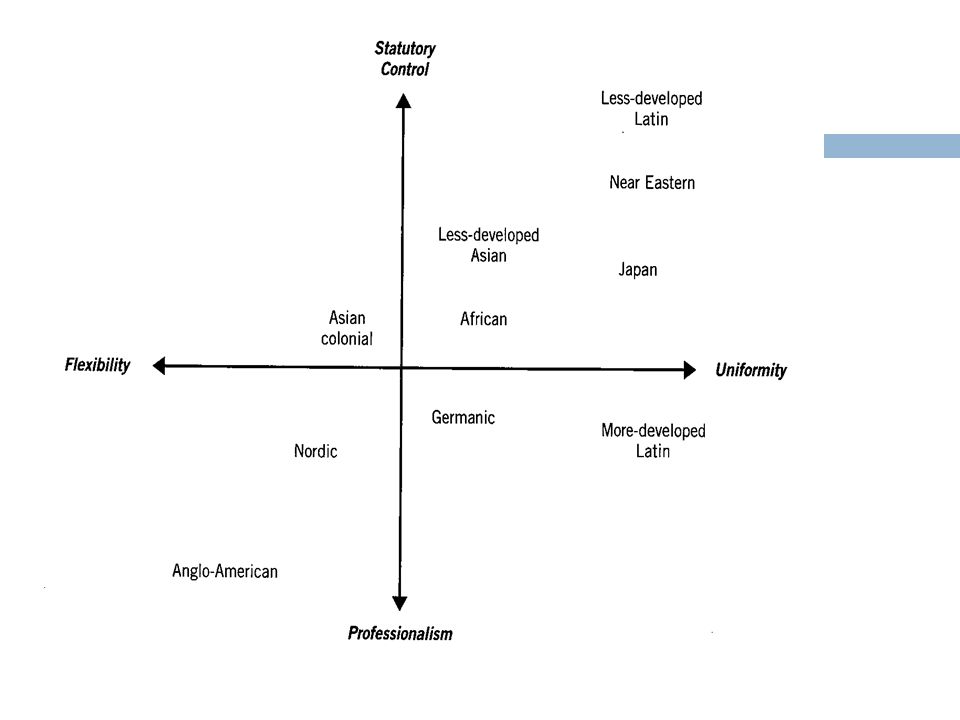

Cultural Influences Gray’s Accounting Values

Professionalism vs. statutory control Uniformity vs. flexibility Conservatism vs. optimism Secrecy vs. transparency Figure Conservatism and secrecy Next slide (Flexibility and professionalism) There is support for culture as an influential factor in the development of accounting.

There is support for culture as an influential factor in the development of accounting.")

18

Divisions of International Classifications

More-developed Latin - France, Italy, Brazil, Spain Less-developed Latin – Mexico, Chile, Venezuela More-developed Asian - Japan Less-developed Asian – Indonesia, Pakistan, India Near Eastern – Arab countries, Greece, Turkey, Iran African – East Africa, West Africa Asian Colonial – Hong Kong, Singapore Germanic – Germany, Austria, Israel and Switzerland Anglo-American - U.S., U.K., Canada, Australia Nordic – Netherlands, Denmark, Finland, Sweden

19

Comparisons for Six Countries – Environmental Influences

Legal Std. Setting Financing Tax Rules Political Germany Civil Code Private/Public Debt Tax=book E.U. U.K. Common Private Equity Minimal Canada NAFTA U.S. Mexico Both Japan Trade

20

Extent of Disclosure Disclosure internationally tends to be limited in these areas: Segments Asset valuation Foreign operations Interim statements Reserves Globalization of capital markets tends to enhance disclosure as companies attempt to attract investors.

21

Extent of Disclosure Largest multinationals set trends in disclosing information and tend to voluntarily disclose more information Disclosure varies by industry Companies from common law countries tend to disclose more information than civil code countries. Corruption decreased the likelihood of disclosure. European companies disclose a lot of nonfinancial information; especially environmental and employee information

22

Disclosure Regulation

New York Stock Exchange requires the most financial disclosures; London Stock Exchange second, Swiss Stock Exchange least disclosures (due to secrecy). More developed stock exchanges tend to require more financial disclosures

. More developed stock exchanges tend to require more financial disclosures.")

23

Timeliness Timeliness is one aspect of the relevance of information.

Filing deadlines differ. The U.S. and Canada are the most timely whereas continental European countries are the least. Few other countries demand quarterly reporting besides the U.S. and Canada. IAS 34 only requires interim reporting but does not state frequency. There is very little investors can do to overcome these problems.

24

American Depositary Receipts (ADRs)

American equivalent of shares of stock in a foreign company. 1 ADR share may equal 2-10 shares of the foreign company’s domestic stock. The amount is determined to equate stock exchange values.

Similar presentations

Steady Growth in.>")

Industry Presentation.>")