Download presentation

Presentation is loading. Please wait.

1

Lecture #7

2

Lecture Outline Review Go over Exam #1 Continue production economic theory

3

Maximizing Profit Using the previous example, let’s now solve for the input levels which maximize profits. Maximizing profit

4

Maximizing Profit 1 st order conditions:

5

Maximizing Profit For the first partial derivative: For the second partial derivative:

6

Maximizing Profit 2 nd order conditions: and Profits are maximized when

7

Maximizing Profit Summary: Least cost combinations and profit maximization.

8

Maximizing Profit Summary: Least cost combinations and profit maximization. Maximizing output subject to a cost constraint:

9

Minimizing Cost Minimizing cost subject to an output constraint: Profit maximization:

10

Expansion Path An expansion path is a locus of points which represent the tangencies between isoquant and isocost lines assuming that input prices are constant. Note that these tangencies are least cost combinations. Since the tangencies represent points where slopes of isoquant and isocost lines are equal, we can solve for the equation of the expansion path: Slope of isoquant:

11

Expansion Path Slope of isocost line: Using our previous production example:

12

Expansion Path equation of the expansion path Points of the expansion path are least cost combinations of inputs.

13

Expansion Path (so the least cost solutions lie on the expansion path)

")

14

Expansion Path So the profit max solution is a least cost solution which lies on the firm’s expansion path. What about the profit max solution?

15

Duality The two constrained optimization methods, constrained output maximization and constrained cost minimization, yield a unique relationship called duality. It implies the possibility of deriving cost functions from production functions and vice versa. Given the same cost and production constraints, we see that both problems (constrained output maximization and constrained cost minimization) can yield the same optimal combinations of inputs

can yield the same optimal combinations of inputs.")

16

Lagrange Multiplier However, the other bit of information – the Lagrange multiplier is different yet related. For the constrained output maximization problem, In the constrained minimization problem,

17

Problem The following production function, based on actual Iowa experimental data, has been altered slightly to simplify computations:

18

Problem Given the above production function and input prices, what is the least cost combination to produce a 240 pound hog?

19

Problem This is a problem of constrained cost minimization. Why? Because costs are in cwt and 240 lbs = 2.4cwt 1 st order conditions:

20

Problem Solve for λ: From the first equation:

21

Problem From the second equation:

22

Problem Plug this relationship between into the third equation.

23

Problem or

24

Problem Least cost combination: Feed 448 lbs of corn and 80 lbs of soybean meal to produce a 240 lb hog (2.4 cwt)

")

25

Homogeneous Functions The function is said to be homogeneous of degree k if each independent variable (the x’s for this function) is multiplied by a scalar λ, and the dependent variable (in this case y) changes by λ k. So the function is homogeneous of degree k if:

26

Example Find the degree of homogeneity for this function. If the function is homogeneous then we can write: the function is homogeneous of degree 2 (HD2)

.")

27

Example What does this mean? If inputs x 1 and x 2 are increased by a factor λ, then output (y) will increase by λ 2.

will increase by λ 2..")

28

Cobb-Douglas Form Another example: case of Cobb- Douglas form Find the degree of homogeneity for this function.

29

Cobb-Douglas Form Linearly homogeneous production functions are HD1 or HD = 1 General Cobb-Douglas production function: is homogeneous of degree Another example:

30

Cobb-Douglas Form Is this function homogeneous and of what degree? However, we can not get back to λ k y. So this function is not homogeneous.

31

Factor (Input) Demand Functions The demand for final products is derived from constrained utility maximization (objective function of consumers). The demand for inputs is derived from profit maximization (objective function of producers). Take the case of production with one variable input:

. Take the case of production with one variable input:.")

32

Factor (Input) Demand Functions Recall first order conditions for profit maximization: We can write the factor demand for input x 1 as:

Demand Functions Recall first order conditions for profit maximization: We can write the factor demand for input x 1 as:")

33

Factor (Input) Demand Functions Changes in r 1 can be represented as movements along the input demand function. Changes in p can be represented as shifts of the input demand function. Generally, output price is a positive shifter of the input demand function.

34

Factor (Input) Demand Functions We can graph the input demand function for x 1 by assuming p is held constant. We call the input demand function the derived demand function since it is a result of (or derived from) profit maximization. So the input demand function is often called the derived demand function since it is derived from profit maximization. For the one variable input case (factor-product case), economic theory states that the factor demand function is that portion of the VMP or MVP curve in Stage II.

profit maximization. So the input demand function is often called the derived demand function since it is derived from profit maximization. For the one variable input case (factor-product case), economic theory states that the factor demand function is that portion of the VMP or MVP curve in Stage II..")

35

What is the law of demand? Does it hold for inputs? Yes. The law of demand underlies the negative relationship between own price and quantity demanded for final products as well as inputs.

36

What about input demands for the factor-factor case? Given the following production function:

37

Assume also that p is output price, r 1 is the per unit cost of x 1 and r 2 is the per unit cost of x 2. Derive the factor demand function for x 1. Input or factor demands are derived from profit maximization.

38

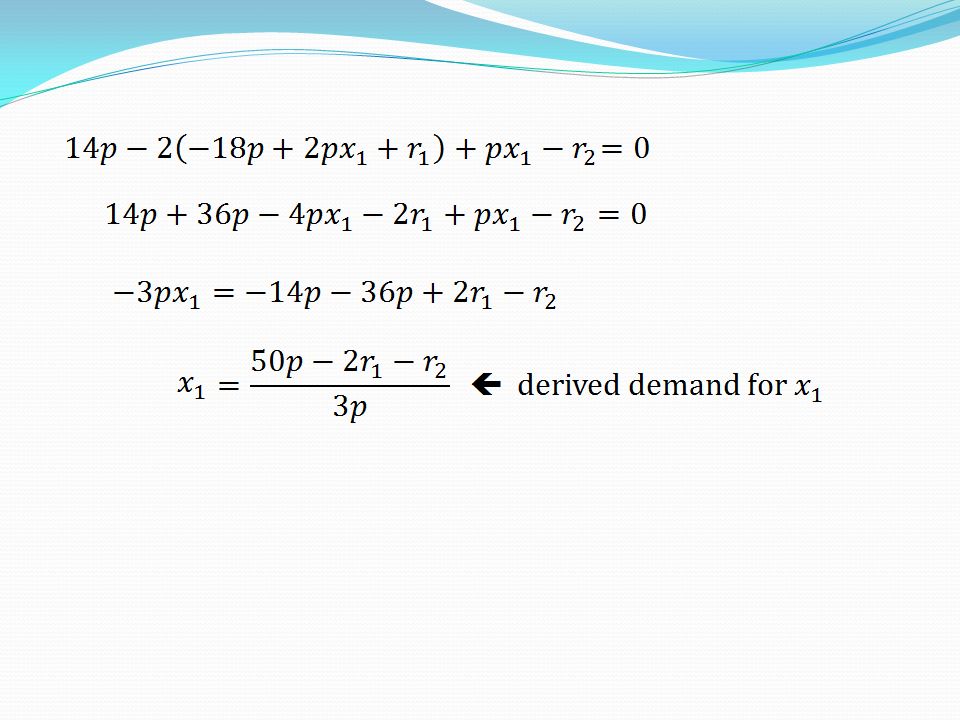

1 st order conditions: Solving for x 2 :

40

In a similar manner, one can derive the factor demand for x 2. Is the factor demand function for x 1 downward sloping?

41

Is output price, p, a positive shifter of the input demand function? So if output price increases demand for x 1 increases

42

What effect does changes in r 2 have on the input demand for x 1 ?

43

Own price elasticity of demand:

Similar presentations

w: wage rate (including fringe benefits, holidays, PRSI, etc) r: rental.>")

. Be able.>")