Download presentation

Presentation is loading. Please wait.

1

Mobile technologies and innovation within Sub-Saharan Africa; a case of the M-Pesa mobile payment system Roseline Wanjiru Newcastle Business School Northumbria University Newcastle upon Tyne, UK

2

Adoption of ICT in Sub-Saharan Africa

Rapid adoption Leapfrogging existing gaps M-Pesa an interesting case of ICT adoption in peripheral contexts Some challenges widespread lack of regional and national infrastructures to support reliable connectivity challenging regulatory and policy environments Inequality and marginalisation Development context

3

Mobile technologies and growth

Broad academic consensus on the sources of economic growth Capital accumulation for investment, commercial expansion from specialization and trade, scale and size effects from increases in output or population growth, and increases in the stock of human knowledge as a result of technological and institutional changes , Solow, 1957; Schumpeter 1942; Abramovitz 1993; Nelson 1995; Romer 1990). Solow’s growth model - growth as arising from two sources; the rate of technological progress and convergence (Solow 1957). Schumpeterian notion of creative destruction and links to African innovation - endogenous growth Technology transfer can lead to changes in total factor productivity, which in turn contributes to economic growth and eventually economic development Positive relationship between a country’s output and mobile phone density ? Caution when making predictions on African countries’ growth rates based on ICT pre

. Solow’s growth model - growth as arising from two sources; the rate of technological progress and convergence (Solow 1957). Schumpeterian notion of creative destruction and links to African innovation. - endogenous growth. Technology transfer can lead to changes in total factor productivity, which in turn contributes to economic growth and eventually economic development. Positive relationship between a country’s output and mobile phone density Caution when making predictions on African countries’ growth rates based on ICT. pre.")

4

Sub-Saharan Africa Widely acknowledged challenges in the ability to attract investment into infrastructure, esp. in the four key sectors of transport, energy, water and ICT. A World Bank study into the state of infrastructure in 24 African countries. Conclusion; poor state of electricity, roads, ICT and water infrastructure effectively reduced national economic growth by two percentage points annually, while cutting productivity by 40 percent (World Bank, 2009). Two common challenges recognized particularly within the African ICT sectors; namely; (a) the lack of regional or national backbone infrastructure to support connectivity, and secondly (b) the challenging regulatory and policy environments that influence African countries’ ability to attract investment.

. Two common challenges recognized particularly within the African ICT sectors; namely; (a) the lack of regional or national backbone infrastructure to support connectivity, and secondly (b) the challenging regulatory and policy environments that influence African countries’ ability to attract investment.")

5

Connect Africa goals Key success factors critical for African ICT development a. The expansion of broadband backbone infrastructures and access networks, including national and regional interconnectivity initiatives, internet exchange points and rural connectivity b). The enhancement of workforce training to engender employment and growth of the ICT sectors c). Stimulating the development of locally relevant ICT content, services and applications d). Developing enabling policy and regulatory environments for investment, including regional harmonization.

. The enhancement of workforce training to engender employment and growth of the ICT sectors. c). Stimulating the development of locally relevant ICT content, services and applications. d). Developing enabling policy and regulatory environments for investment, including regional harmonization.")

6

Kenya Typical low-income developing country in Sub-Saharan Africa

GNI per capita $860 Over 40% of Kenya’s estimated 44 million population of 44million are very poor, living on less than $1.25 per day, while over 60% are classed as poor, living on below $2 per day. About a quarter of the country’s population live in urban areas while the rest are rural-based (World Bank development Indicators, 2014).

.")

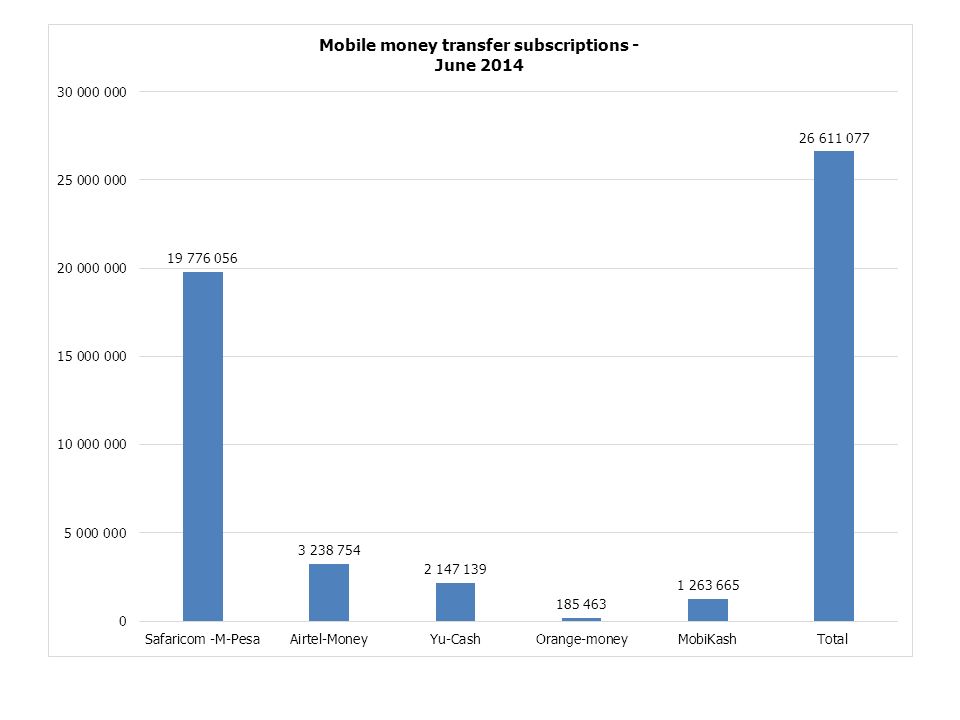

7

Kenya’s telecommunications profile:

April - June 2014 Subscriptions Penetration Mobile phone subscriptions 32.2 million 79.2 % Fixed line subscriptions 201, 233 0.1% Communications Authority of Kenya (2014) By end 1990s, 1 in every 1000 adult Kenyans owned a mobile phone. By 2010, 90 mobile phones in every 100 Kenyan adults (World Bank 2010) Traditional technologies remain relevant: radio still has wide coverage, with nearly 80% of the population having access to radio terminals. Two out of every five people have access to televisions (Kenya National ICT survey 2010)

By end 1990s, 1 in every 1000 adult Kenyans owned a mobile phone. By 2010, 90 mobile phones in every 100 Kenyan adults (World Bank 2010) Traditional technologies remain relevant: radio still has wide coverage, with nearly 80% of the population having access to radio terminals. Two out of every five people have access to televisions (Kenya National ICT survey 2010)")

8

Mobile phones in Kenya Most popular new form of ICT within a peripheral African economy Traditional technologies such as radio still very relevant Trends in Kenyan mobile phone usage

9

M-PESA popular mobile money in Kenya

transcending simple e-payment system to wider development applications attention linked to potential development possibilities Insight into diverse Africa? distinctive ways in which mobile technologies used and appropriated in peripheral, African contexts beyond dominant models informed by outsider, elite or Western priorities. - How replicable ?

10

Some local uses of M-Pesa in Kenya

Person to person transfers: Transfers of small amounts between family, friends or for SMEs. Petty traders typically take payment via M-Pesa and can also pay customers’ change back into customers’ M-pesa account. ATM Withdrawals: alternative access to M-Pesa funds as cash Lipa Karo: learning institutions with M-Pesa account and a Paybill number receive school fees Lipa na M-Pesa: walk-in customers paying over the counter for goods /services M-Pesa Pay Bill: remote payments of electricity or water bills, loan repayments Company Bulk payments: paying wages to workers without bank accounts into their M-Pesa accounts using a bulk payment service. M-Pesa Safari Card: local users can load money via their M-Pesa account into a pre-payment card to make local and international transactions

12

Additional mobile products in Kenya

Providers Mobile money Airtime credit Airtime sharing Safaricom M-Pesa OkoaJahazi Sambaza Essar (Yu) Yu-Cash YuCredo Share Airtime Airtel Networks Airtel Money Kopa Credo Advance Me2u Orange Telkom Orange Cash Pewa Credit transfer

Yu-Cash. YuCredo. Share Airtime. Airtel Networks. Airtel Money. Kopa Credo Advance. Me2u. Orange Telkom. Orange Cash. Pewa. Credit transfer.")

13

M-Pesa and the competition

Mobile money product Company Mobile market share % Year launched M-Pesa Safaricom 69.89 March 2007 Airtel money Airtel Networks 15.20 November 2010 Yu-cash EssarTelcom 8.50 December 2009 Orange money Orange Telkom 6.37 (MobilePay) (Tangaza) *2014 (MobiKash) ..

(Tangaza) *2014. (MobiKash) ..")

14

Some insights from the M-Pesa experience so far

- Success at increasing financial inclusion of the unbanked population 2006, 2009 and 2013 FinAccess national survey results adoption by both poor and middle classes (potential to address exclusion; poor, rural, nomadic, gender, ethnicity) disrupting existing industries +potential for greater innovation potential for creative pro-poor development interventions Local context crucial: Existing Kenyan communication gaps arising from the widespread lack of fixed telephony infrastructure across the country, the increased availability of cheap handsets locally.

disrupting existing industries +potential for greater innovation. potential for creative pro-poor development interventions. Local context crucial: Existing Kenyan communication gaps arising from the widespread lack of fixed telephony infrastructure across the country, the increased availability of cheap handsets locally.")

15

Some M-Pesa impacts 2006, 2009 and 2013 FinAccess national survey results By 2013, nearly 31% of Kenyan GDP via mobile money including Mpesa M-Pesa users more inclined to save formally, encouraging their inclusion in formal banking. Poor Kenyans previously largely unbanked and excluded from various economic transactions, consigned to informal, unregulated mechanisms e.g. ‘merry-go-rounds’ or rotating savings and credit associations (ROSCAs). Increased sending and receiving transfer frequencies of smaller amounts - Morawcyznski&Pickens (2009) Lower revenues and profits for traditional banks and money transfer companies e.g. Western Union, MoneyGram

. Increased sending and receiving transfer frequencies of smaller amounts - Morawcyznski&Pickens (2009) Lower revenues and profits for traditional banks and money transfer companies e.g. Western Union, MoneyGram.")

16

Some challenges in Kenya

Kenyan mobile market – ‘winner-takes-most’ model, with significant profit inequality and extreme market shares Proportion of market share by subscriptions: Kenyan mobile operators 2014

17

2013 Kenya Mobile Revenue Shares

18

Further insights from M-Pesa

Regulatory capacity – intense lobbying by various interests (nods and winks), limits to CBK and CA formal regulation FDI impacts on local economy – varied Competition: monopoly profits vs consumer welfare Dominance of Safaricom – Vodafone in mobile market Limited interoperability of M-Pesa system and tight control over Safaricom Agent network (anti-competitive concerns) Recent changes 2014 – pressure to open up system, court cases, Equity Bank+Airtel partnership Policy and regulatory ambiguity surrounding M-Pesa (consumer protection and regulatory proportionality) Local context crucial in assessing applicability elsewhere

, limits to CBK and CA formal regulation. FDI impacts on local economy – varied. Competition: monopoly profits vs consumer welfare. Dominance of Safaricom – Vodafone in mobile market. Limited interoperability of M-Pesa system and tight control over Safaricom Agent network (anti-competitive concerns) Recent changes 2014 – pressure to open up system, court cases, Equity Bank+Airtel partnership. Policy and regulatory ambiguity surrounding M-Pesa. (consumer protection and regulatory proportionality) Local context crucial in assessing applicability elsewhere.")

19

Developing effective mobile financial services

Supportive institutional environment, including both consumer protection and regulatory proportionality. M-Pesa ; - regulation at the intersection between the financial and telecommunications sectors, with resulting policy uncertainty Other factors include market competitiveness the end-user environment including agent and distribution networks. Local context crucial in assessing applicability elsewhere

Similar presentations