Download presentation

Presentation is loading. Please wait.

1

1 Bruce Bowhill University of Portsmouth ISBN: 978-0-470-06177-0 © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

2

Chapter 2 Pricing and Costing in a Competitive Environment © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

3

3 ALTERNATIVE APPROACHES Traditional approach. Full cost plus mark- up. Approaches to pricing that take into consideration market factors –Contribution approach –Demand based approach –Target pricing and costing –Pricing strategies e.g. -price skimming- market based pricing © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

4

4 Full cost plus mark-up (product M) Budgeted fixed cost £180,000 Budgeted production 12,000 units Budgeted fixed cost per unit = £15 £ Material 21.00 Labour 15.00 Fixed cost per unit 15.00 Total cost per unit 51.00 Add 20% mark-up 10.20 Selling price 61.20 © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

5

5 Criticisms of full costing approach to pricing May lead to uncompetitive pricing as it does not take into account market demand. This can lead to a spiral effect of falling sales and production Method of assigning overheads may not reflect use or cause. The budget may be out of date (expected costs or sales volumes have changed ). © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

. © 2008 John Wiley & Sons Ltd.")

6

6 Approaches to pricing that take into consideration market factors Contribution approach Demand based pricing Target pricing and costing Pricing strategies e.g. price skimming, market penetration © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

7

7 Contribution approach Product M £ Selling price 50 Variable cost: Material 21 Labour 15 Total variable cost 36 Contribution to overheads 14 © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

8

8 Benefits of contribution approach When there is spare capacity No commitment to long-term business For a large order Strategic reasons: –Means of gaining market entry –An important customer © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

9

9 Dangers of contribution approach Future customer reaction Future competitor reaction Incorrect cost assumptions © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

10

10 Demand based pricing Selling price/ unit £ 67.561.255504540 Sales volume (units) 2,70040006,000750085009500 © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

11

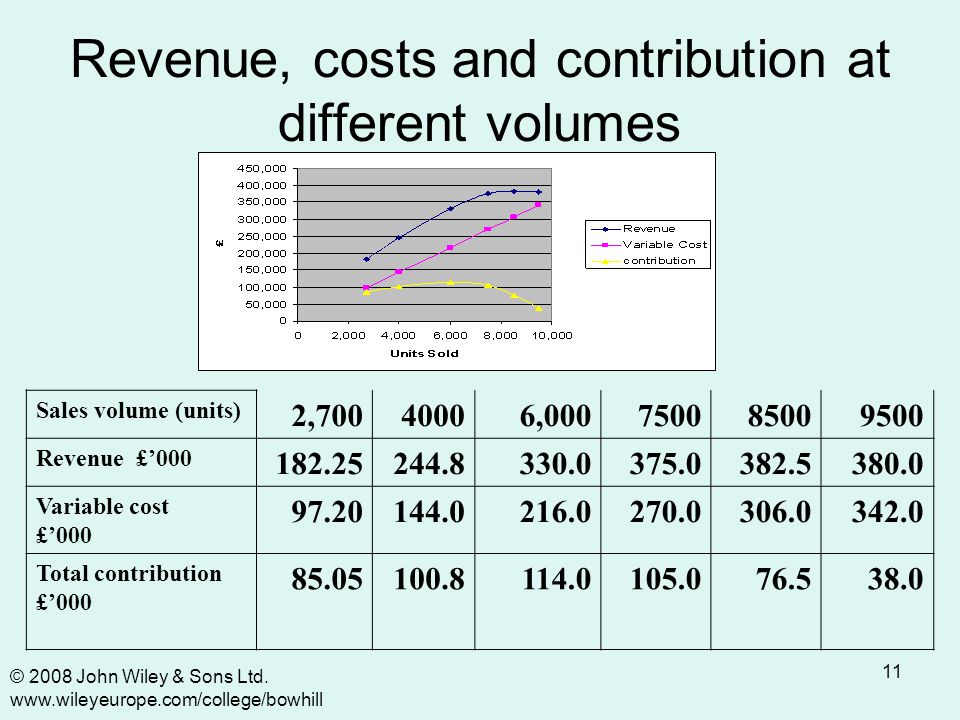

11 Revenue, costs and contribution at different volumes Sales volume (units) 2,70040006,000750085009500 Revenue £’000 182.25244.8330.0375.0382.5380.0 Variable cost £’000 97.20144.0216.0270.0306.0342.0 Total contribution £’000 85.05100.8114.0105.076.538.0 © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

12

12 Traditional v target costing (1) Target costing Step 1 - Target selling price is identified. Step 2 - Target costs are identified. –Target profit is deducted from target selling price to identify the target cost. Traditional costing Step 1 - Market research to identify customer requirement, Step 2 - Product specification and design –Product to meet customer needs is specified. –Designers produce a product design to specification –Production engineers provided with the design and specify how this is to be manufactured. © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

13

13 Target costing XY Ltd wishes to produce and sell a new product. Similar products are in the market for sale at just over £50 per unit and XY Ltd thinks that it could sell approximately 10,000 units at £50. Above £50, it believes there would be a sharp fall in demand. XY Ltd, has a target profit to sales of 20%. TARGET COSTING 1. Market price £50 * 10,000 units = £500,000 2. Less required profit £10 * 10,000 units = £100,000 Target cost £40 * 10,000 units = £400,000 © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

14

14 Traditional v target costing (2) Traditional costing Step 3 – Costs are estimated. If high designers will look for cost savings. Step 4 - Expected selling price is established –For example by adding the desired profit margin to the estimatedcosts Target costing Step 3 – Actual costs are estimated. A multidisciplinary approach is taken Step 4 – Where costs are higher than target costs, multi- disciplinary teams will investigate cost savings. © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

15

15 Looking for cost savings Tear-down analysis –Examining a competitor’s product in order to identify opportunities for improvement in the firm’s own product. Value engineering –An examination of each component to see if it is possible to reduce cost without losing functionality. © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

16

16 Pricing strategies Pricing strategies for existing products –Price leader –Price taker –Predatory Pricing strategies for new products –Price skimming –Penetration pricing © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

17

17 Product lifecycle - different policies at different stages of the PLC © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

18

18 Life cycle costing © 2008 John Wiley & Sons Ltd. www.wileyeurope.com/college/bowhill

Similar presentations

>")