Download presentation

Presentation is loading. Please wait.

1

Impact of the introduction of the risk management products Dr. San-Lin Chung Department of Finance National Taiwan University

2

In this chapter Smithson (1999) discuss the impact of the introduction of the risk management products from three aspects: 1.The impact on the markets for the underlying assets 2.The impact on the economy 3.The impact of the derivative markets on each other Three dimensions of analysis

discuss the impact of the introduction of the risk management products from three aspects: 1.The impact on the markets for the underlying assets 2.The impact on the economy 3.The impact of the derivative markets on each other Three dimensions of analysis")

3

The financial derivatives may have the following impacts on the markets for underlying assets: The volatility of the underlying asset price The speed adjustment in the underlying asset market The bid-ask spreads in the underlying markets Trading volume for the underlying asset The impact on the markets for the underlying assets

4

The impact on price volatility Derivatives were blamed for the cause of the October 1987 crash. However the empirical evidence does not support the increased-volatility story Table 3-1

5

The effects of triple-witching hours On the third Friday of March, June, September, and December three types of derivative contracts expire – stock index option, stock index futures, and options on stock index futures. The maturities used to occur at the close of the market. The last trading hour on those Fridays is called the triple-witching hour.

6

The effects of triple-witching hours Expiration effects: the volatility of stock returns was higher on average for futures ’ expiration days than for non-expiration days. The expiration effects became insignificant probably due to the change in the settlement of index-linked contracts from the close of trading to the open of trading on expiration days.

7

To conclude: look at Figure 3-1Figure 3-1 Derivatives volatility Volatility derivatives

8

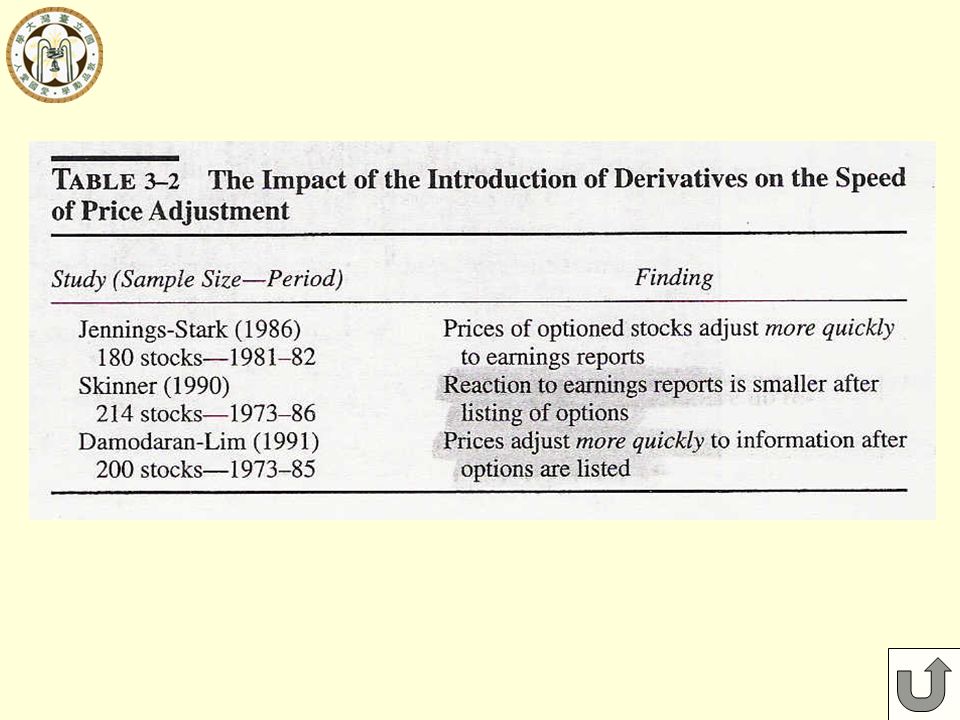

The empirical evidence suggests that the market adjust to information more quickly, i.e. market is more efficient. Table 3-2 The impact on adjustment speed

9

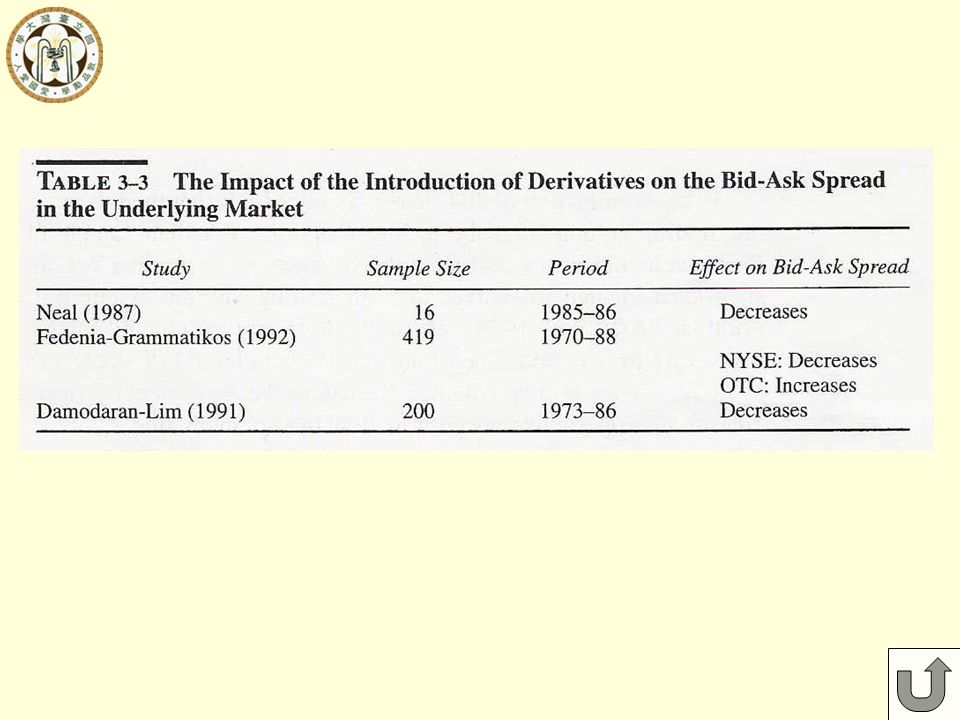

Two possible explanations (or determinants) for bid-ask spread Inventory cost Information asymmetry among traders The introduction of derivatives generally cause the bid- ask spread for the underlying asset to decline. Table 3-3 The impact on bid-ask spread

10

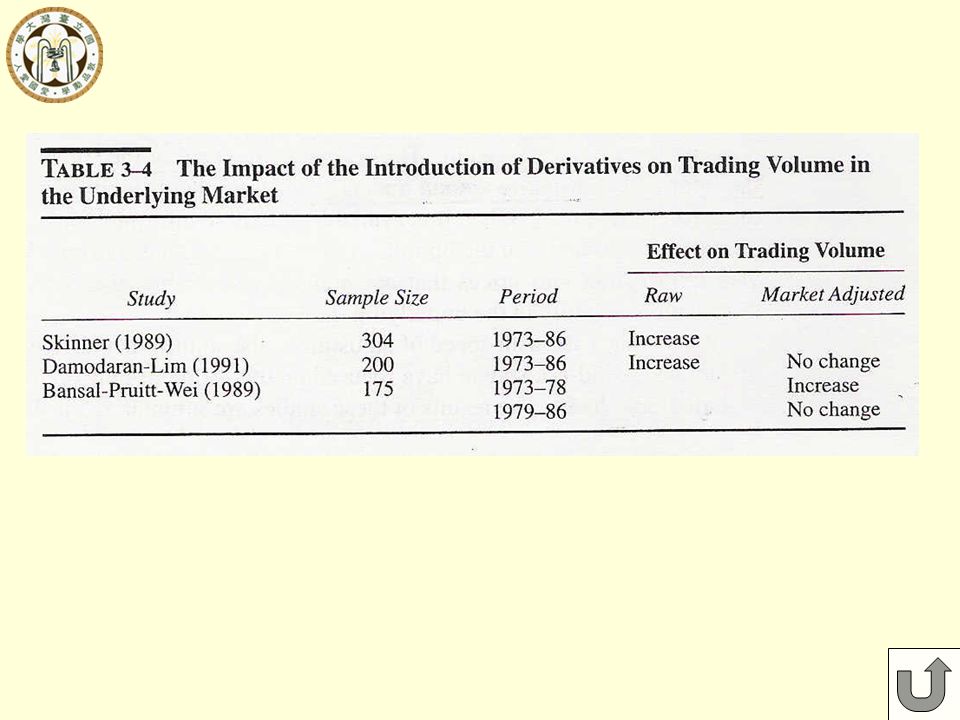

Theory suggests that trading volume on the underlying asset should increase when derivatives are introduced. The empirical evidence show that the introduction of derivatives has had little effect on market-adjusted trading volume in the underlying market. Table 3-4 The impact on trading volume

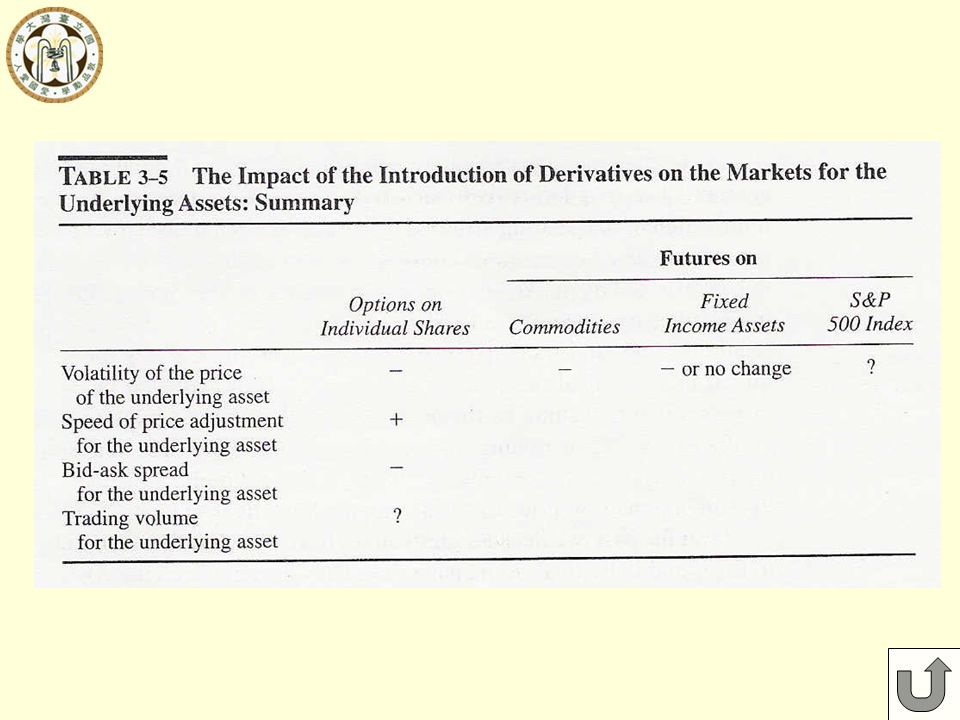

11

Table 3-5 Summary

12

The social benefits of financial innovation far outweigh the cost. Improvement in the allocation of risk within the financial system Help firm to hedge their risk without diversification of their investment Increase liquidity and efficiency of financial markets The impact of risk management on the economy

13

The impact of the OTC derivative market on the exchange-traded derivatives The trading volume in the OTC derivatives seems increasing at the expense of the exchanges However, Merton argue that the OTC markets still needs the exchange market to hedge their positions. The impact of derivative markets on each other

Similar presentations

>")

>")