Download presentation

Presentation is loading. Please wait.

1

The redistributive effects of Personal Income Tax reforms during the Great Recession in Spain M. Adiego (IEF), O. Cantó (UAH), M. Paniagua (IEF) and T. Pérez (IEF) European Meeting of the International Microsimulation Association, Dublin, May 17-19 2012

, O. Cantó (UAH), M. Paniagua (IEF) and T. Pérez (IEF) European Meeting of the International Microsimulation Association, Dublin, May")

2

1.Introduction 2.Personal Income Tax in Spain and main reforms 3.Methodology 1.Model and data 2.Simulations and measurements 4.Conclusions

3

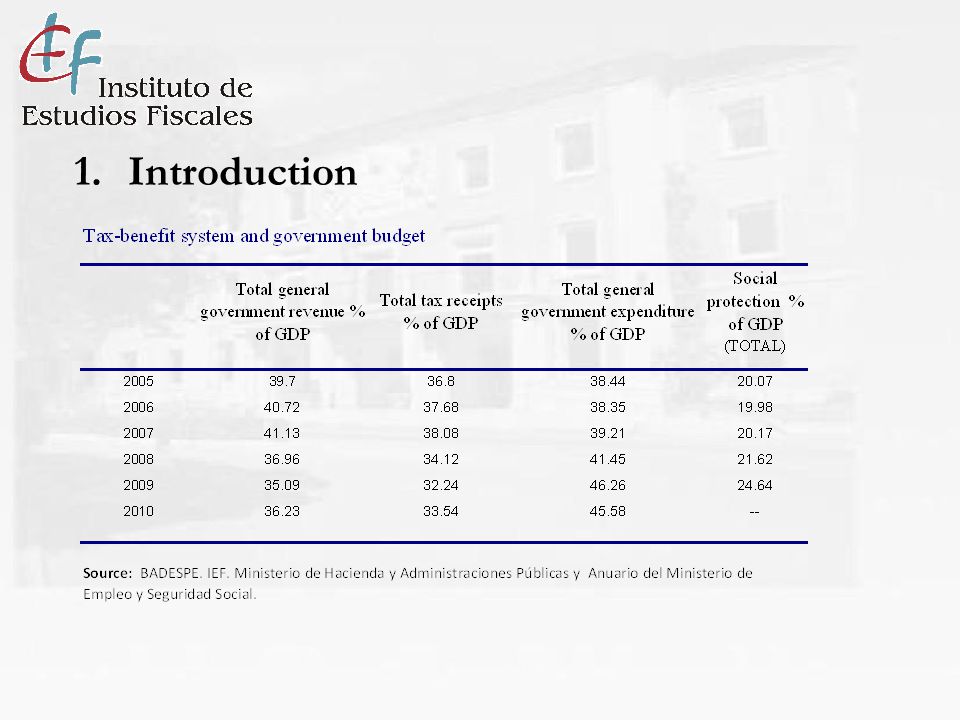

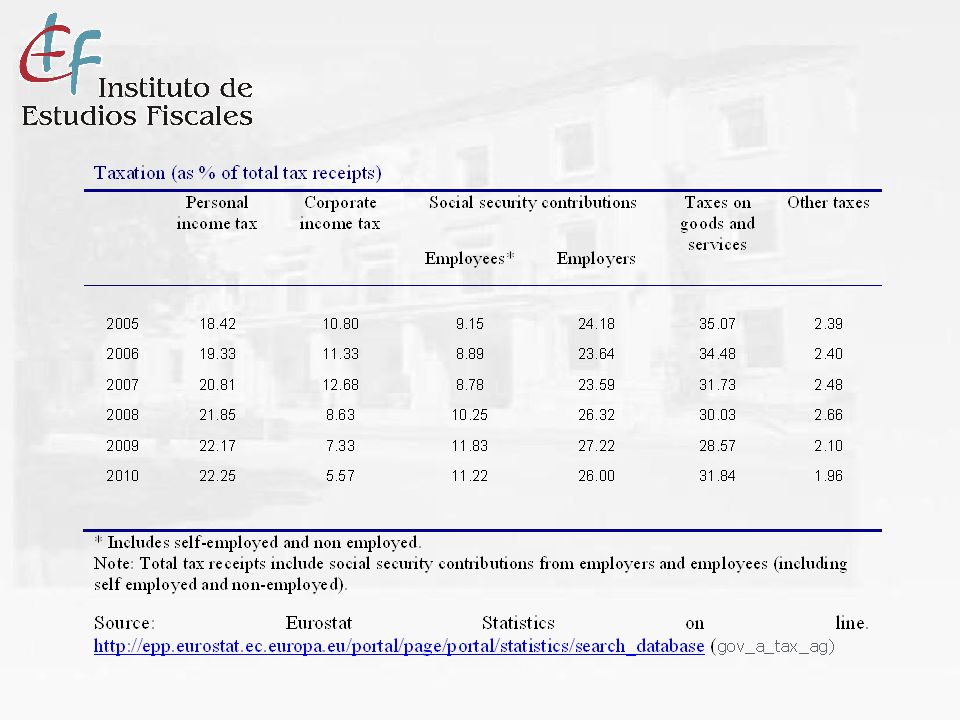

Personal Income Tax very important within the Spanish tax-benefit system aiming at disposable income redistribution. Trends since 1990s (similar to OECD countries) meant reduction in number of tax brackets and fall in high marginal tax rates. Thus, benefits (mainly old age pensions and unemployment benefits) have the largest impact in equalizing disposable income (see graph). Further, since 2007 incresing decentralization of PIT revenue towards regions and increase in regional governments use of design capacity. In 2008, 3-4 regions used their legal capacity to reduce their PIT marginal tax rates (Madrid, La Rioja, C. Valenciana) and introduce regional tax credits. HOWEVER: since Great Recession (2008) the need for fiscal consolidation has led regional (2011) and state (2012) governments to reform PIT. 1.Introduction

meant reduction in number of tax brackets and fall in high marginal tax rates. Thus, benefits (mainly old age pensions and unemployment benefits) have the largest impact in equalizing disposable income (see graph). Further, since 2007 incresing decentralization of PIT revenue towards regions and increase in regional governments use of design capacity. In 2008, 3-4 regions used their legal capacity to reduce their PIT marginal tax rates (Madrid, La Rioja, C. Valenciana) and introduce regional tax credits. HOWEVER: since Great Recession (2008) the need for fiscal consolidation has led regional (2011) and state (2012) governments to reform PIT. 1.Introduction.")

6

Redistributive impact of Tax-Benefit policies in Spain 2005-2009 % reduction in the Gini coefficient attributed to each disposable income component Source: EUROMOD 4.26. For years 2005 to 2007 incomes correspond to policy year. In 2008 and 2009 incomes are those in 2007 (ECV 2008) grossed up using upgrading factors.

grossed up using upgrading factors..")

7

2.Personal Income Tax in Spain and main reforms 1998 Reform: introduction of tax allowances, individual and children. reduction of tax brackets from 8 to 6, fall in highest marginal tax rate (from 56% to 45%) and increase in lowest (from 18 to 20%) and intermediate ones capital income 20% flat tax Reform cost: approx. 19% revenue (Levy and Mercader-Prats. 1999) Reduction in redistributive impact of PIT on disposable income: small increase disposable income inequality, decreases income in first two deciles (Levy and Mercader-Prats.,1998)

and increase in lowest (from 18 to 20%) and intermediate ones capital income 20% flat tax Reform cost: approx. 19% revenue (Levy and Mercader-Prats. 1999) Reduction in redistributive impact of PIT on disposable income: small increase disposable income inequality, decreases income in first two deciles (Levy and Mercader-Prats.,1998).")

8

2.Personal Income Tax in Spain and main reforms 2002 Reform: reduction in tax brackets: from 6 to 5 and fall in lowest marginal tax rate (15%) increase in tax exemptions and more detail in terms of family characteristics (disability and old-age parents care) capital income tax rate falls for some particular cases to 18% Reform cost: approx. 15% revenue (Castañer et al. 2004) Reduction in redistributive impact of PIT on disposable income: 9% (Castañer et al. 2004)

Reduction in redistributive impact of PIT on disposable income: 9% (Castañer et al. 2004).")

9

2.Personal Income Tax in Spain and main reforms 2007 Reform: reduction of tax brackets from 5 to 4 and reduction of highest marginal tax rate to 43% and increase in lowest to 24% change of child allowances to child tax credits capital income 18% flat tax Reform cost: approx. 6% revenue (Díaz de Sarralde et al., 2006) Reduction in redistributive impact of PIT on disposable income: small, somewhat increase in progressivity and reduction in revenue, Sanz et al. (2008)

Reduction in redistributive impact of PIT on disposable income: small, somewhat increase in progressivity and reduction in revenue, Sanz et al. (2008).")

10

2.Personal Income Tax in Spain (2010 – baseline) PIT 2010:

PIT 2010:")

11

2.Personal Income Tax in Spain (2011 reform) 2011 REFORM State adds two new high income brackets with higher marginal tax rates (over 120,000 euro (44%), over 175,000 euro (45%)) Some regions create new brackets at top with higher marginal rates (Asturias, Andalucía, Cantabria, Cataluña, Extremadura)

2011 REFORM State adds two new high income brackets with higher marginal tax rates (over 120,000 euro (44%), over 175,000 euro (45%)) Some regions create new brackets at top with higher marginal rates (Asturias, Andalucía, Cantabria, Cataluña, Extremadura)")

12

2.Personal Income Tax in Spain (2011 reform) PIT 2010 (regional examples):

PIT 2010 (regional examples):")

13

2.Personal Income Tax in Spain (2012 reform) PIT 2012: State introduces a temporary and progressive increase in all PIT tax brackets. Adds a new bracket for incomes over 300,000 euro

14

3.Methodology: model and data Use of EUROMOD v5.30 as a microsimulation tool to calculate household disposable income in 2010 and after 2011 and 2012 PIT reforms. Income data come from Encuesta de Condiciones de Vida 2008 (2007 incomes), the Spanish version of EU-SILC provided by the Spanish Statistical Office (splitting of some variables)

, the Spanish version of EU-SILC provided by the Spanish Statistical Office (splitting of some variables).")

15

3.Methodology: simulation and measurements 3.1. Simulation We simulate the Personal Income Tax reforms implemented in 2011 and 2012 regarding changes in marginal tax rates. Data come from ECV 2008 (annual incomes reported for 2007). Data updated to 2010 with upgrading factors. We use 2010 policy as a baseline for analysis. We compare the results obtained implementing the changes in the Personal Income Tax (2011 and 2012 simulated policies) keeping other policies in 2010 fixed (benefits, social contributions, etc..).

. Data updated to 2010 with upgrading factors. We use 2010 policy as a baseline for analysis. We compare the results obtained implementing the changes in the Personal Income Tax (2011 and 2012 simulated policies) keeping other policies in 2010 fixed (benefits, social contributions, etc..)..")

16

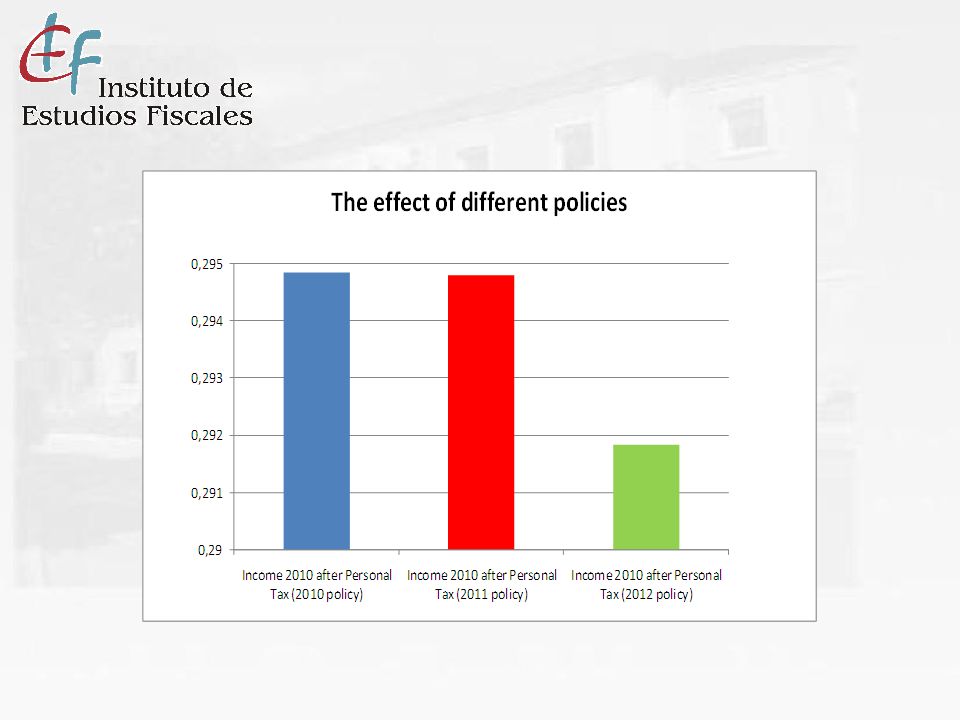

3.2. Distributional effect of the PIT The PIT in 2010 reduces mean income less in higher income groups than the new tax marginal rates implemented in 2012. The relative reduction is around 2% in lower income groups and 22% in the highest income group. The 2012 reform pushes the last three deciles reduction upwards.

18

We find losers in all groups. However, within the higher income groups almost all individuals lose with the reform which is not the case in the first and second deciles. The annual mean loss is 661.2 euros. This loss is rather small for individuals in low income groups, while it is considerably large for those in high income groups. Gainers and Losers 2012 reform

19

Losers 2012 reform (versus 2010 policy)

")

20

In 2010, the effect of the Personal Income Tax on the Gini index was approximately 11% (reduction from 0.333 to 0.295), similar to its impact along the 2005-2009 period. Under 2011 and 2012 PIT policies this reduction is larger. However, 2011 policies do not have a big effect whereas 2012 PIT reform does push the Gini index downwards to an extra reduction of 0.003. Effects on inequality. The Gini Index

23

Effects on poverty. Foster-Greer-Thorbecke indices

24

In 2010, the effect of the Personal Income Tax on the poverty headcount was approximately a 2% (reduction from 21% to 19%). The PIT reduced also poverty intensity and inequality (FGT(1) and FGT(2)) Under 2011 and 2012 PIT policies, poverty incidence, intensity and inequality in Spain is pretty similar to that under the 2010 system Effects on poverty. The FGT Index

and FGT(2)) Under 2011 and 2012 PIT policies, poverty incidence, intensity and inequality in Spain is pretty similar to that under the 2010 system Effects on poverty. The FGT Index.")

25

4.Conclusions The 2011 reform related to changes in regional PIT including new tax brackets at the top and higher marginal rates for the rich had a very limited impact on inequality in Spain The 2012 reform instead had larger effects on the income distribution which can make us think that it will probably have this real redistributive impact in 2012. Both reforms have been quite neutral in reducing poverty incidence, intensity and inequality.

26

Thank you for attending this session. Comments are welcome ! milagros.paniagua@ief.minhap.es

Similar presentations

(May 30th, 2006)>")