Download presentation

Presentation is loading. Please wait.

1

Coding and Taxing of Foreign National Payments in PeopleSoft

2

Introduction University of Florida hosts a variety of foreign national visitors, employees and students each year. Payments to these visitors can be complicated due to IRS tax laws and immigration regulations. Today we will be discussing how to process payments for employment, scholarships & fellowships, honorariums and vendor payments. Before any payment can be made, we first must determine a foreign national’s tax status. Is this individual a “nonresident alien” (NRA) or “resident alien” (RA) for tax purposes? Per IRS Publication 519 “U.S. Tax Guide for Aliens”, there are two tests to determine the residency status of a foreign visitor. The “green card” test and the “substantial presence” test. - Nonresident Aliens are aliens who have not passed the substantial presence test. Resident Aliens are aliens who have either passed the substantial presence test or the green card test. (Individuals who were lawful permanent residents of the United States at any time during the calendar year.)

or resident alien (RA) for tax purposes. Per IRS Publication 519 U.S. Tax Guide for Aliens , there are two tests to determine the residency status of a foreign visitor. The green card test and the substantial presence test. - Nonresident Aliens are aliens who have not passed the substantial presence test. Resident Aliens are aliens who have either passed the substantial presence test or the green card test. (Individuals who were lawful permanent residents of the United States at any time during the calendar year.).")

3

- The test is met if the foreign national is physically present in the U.S. for at least: 31 days during the current year, and 183 days during the 3- year period the includes the current year and the 2 years immediately before that, counting: -(a) all the days the foreign national was present in the current year, and - (b) 1/3 of the days the foreign national was present during the first preceding year, and - (c) 1/6 of the days that the foreign national was present in the second preceding year Substantial Presence Test NRA or RA

all the days the foreign national was present in the current year, and - (b) 1/3 of the days the foreign national was present during the first preceding year, and - (c) 1/6 of the days that the foreign national was present in the second preceding year Substantial Presence Test NRA or RA.")

4

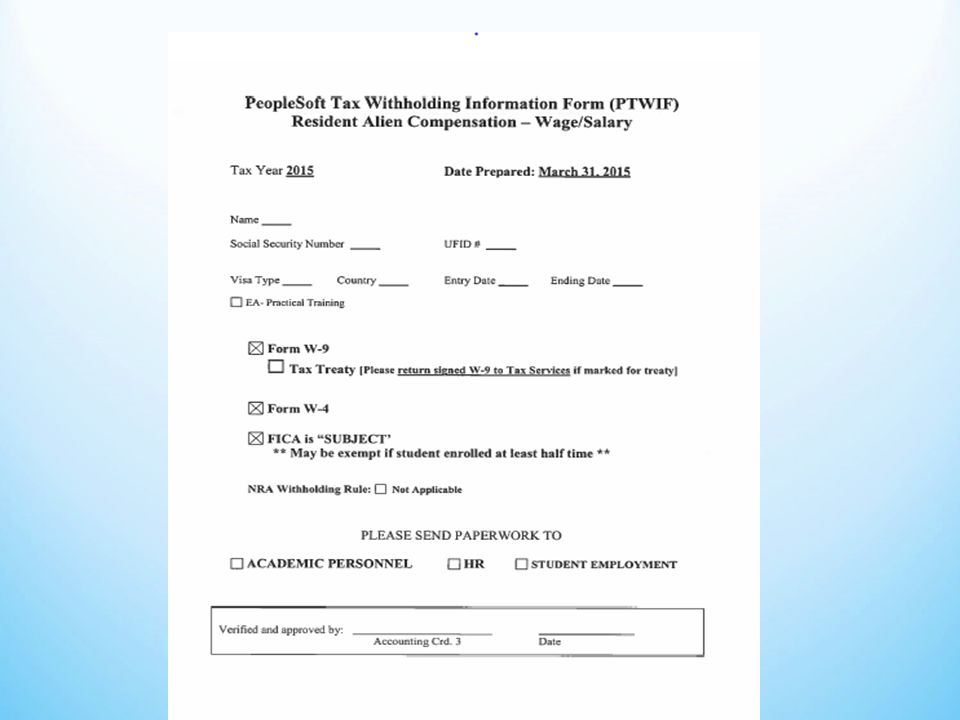

Department representatives should have each foreign visitor compete a Foreign National Information Form. The FNIF and supplemental tax documentation should be sent to Tax Services to be processed. The information provided will be used to evaluate the individual’s tax status, eligibility for an exemption from withholding, FICA status and workgroup. Once processed, the following forms will be returned to the department for signature. The signed forms should be imaged into the ePAF. PeopleSoft Tax Withholding Information Form (PTWIF) – contains the necessary codes needed to enter the hire. W-4 Form - W-9 Form - For individuals who are “residents for tax purposes”. Tax Treaty Forms – 8233 or treaty W-9 (If a treaty applies). Treaty Analysis Log- Employment

– contains the necessary codes needed to enter the hire. W-4 Form - W-9 Form - For individuals who are residents for tax purposes . Tax Treaty Forms – 8233 or treaty W-9 (If a treaty applies). Treaty Analysis Log- Employment.")

5

NRA W-4 Form – preprinted with single and one exemption (per IRS Pub 15) Workgroup- ends with the following: 9- for students 8- for teacher/researchers FICA status - exempt Tax treaty benefits- Claimed on an 8233 RA W-4 Form- Editable by employee Workgroup - Will NOT end in a number (unless claiming a tax treaty). W-9 Form- verify individual is a resident for tax purposes FICA status – subject (unless enrolled as a student ) Tax treaty benefits- Claimed on a W-9 Form

Tax treaty benefits- Claimed on a W-9 Form.")

8

Scholarships are issued to assist a person in pursuing a course of study. The IRS allows qualified scholarships to be tax free as long as the student is in a degree program and the funds are used for tuition, books and fees. Any portion of scholarship funds used for any other purpose is non-qualified and taxable. The only exception is if the student is eligible to claim a treaty. The Bursar’s Office sends a NRA Scholarship Report to Tax Services for review. Each student is checked to determine if they are a “resident” or “nonresident” for tax purposes. Nonresidents (NRA) are required to sign a W-8 Ben or W-8 Ben (treaty) form. Residents (RA) sign a W-9 Form. Scholarship Payments to Foreign Nationals

are required to sign a W-8 Ben or W-8 Ben (treaty) form. Residents (RA) sign a W-9 Form. Scholarship Payments to Foreign Nationals.")

9

W-8 and W-9 Forms

10

Scholarships cont. Nonresident aliens Signs a W-8Ben or W-8 Ben Treaty Form Qualified : Equal to or less than the current fees for that semester. Nonqualified: More than the current fees for that semester. Is paid through Payroll and taxed at 14% unless a treaty applies. FICA Exempt Reported on a 1042S Form at year end. Resident aliens Signs a W-9 Form Qualified or Nonqualified the scholarship is not taxed before it is released to the student. FICA Exempt Reported on a 1098T Form at year end

11

Fellowships are issued at the graduate level to assist with research. Fellowships paid to foreign nationals are paid through the Payroll system. Just like scholarship payments, the student is required to complete a Foreign National Information Form. Tax Services will send the department a coversheet with either a W-8Ben Form or W-9 Form for signature. The difference is fellowships are not reviewed to determine if they are qualified or nonqualified. The payments are coded based on the student’s residency status of NRA or RA. NRA RA * Taxed at 14% before the payment * Not taxed before the payment is is issued (unless a treaty applies). issued. * FICA Exempt * FICA Exempt * Reported on a 1042S Form at year end * Reported on a 1098T Form at year end Non-employment fellowship payments to Foreign Nationals

. issued. * FICA Exempt * FICA Exempt * Reported on a 1042S Form at year end * Reported on a 1098T Form at year end Non-employment fellowship payments to Foreign Nationals.")

12

Use the following codes when entering the fellowship payment in PeopleSoft. Earnings Code Reason NRA Post-Doc Fellow N15 FLT Pre-Doc Fellow N15 FUS RA Post-Doc Fellow FEL FLT Pre-Doc Fellow FEL FUS Fellowships cont.

13

An honorarium may be paid to a foreign national for “usual academic activity or activities”. These include lecturing, teaching and sharing of knowledge. However, only certain visa classifications are authorized to accept an honorarium. These payments are also taxable at 30% unless a treaty applies. The visitor will receive a 1042S Form at year end for tax reporting. B-1 Visa- Issued for business. B-2 Visa- Issued for pleasure. ESTA Program- Electronic System for Travel Authorization - Visa waiver for business - Visa waiver for pleasure Visitors receiving honorarium payments under a B visa or ESTA program are bound by the American Competitiveness Workforce Act of 1998. Under the Act, an activity may not exceed nine days at a single institution. In addition, such visa holders cannot accept honoraria and/ or incidental expenses from more than five such institutions in the previous six-month period. Honorarium Payments to Foreign Nationals

14

J-1 non-student short term scholars These visitors are not bound by the 9/5/6 rule. J-1 (non-student) from another institution- These visitors are also not bound by the 9/5/6 rule. They do however need permission from their sponsoring institution to lecture off campus. Note: Foreign nationals under an H-1, Diplomatic Visa, F-1 or Religious Visa are not permitted to receive honorarium payments or be reimbursed for travel expenses. Honorarium payments cont.

from another institution- These visitors are also not bound by the 9/5/6 rule. They do however need permission from their sponsoring institution to lecture off campus. Note: Foreign nationals under an H-1, Diplomatic Visa, F-1 or Religious Visa are not permitted to receive honorarium payments or be reimbursed for travel expenses. Honorarium payments cont..")

15

Forms- * Foreign National Information Form * Certification of Academic Activity (for B1-B2 and WB-WT visitors) * W-8 Ben Form Documents- * Passport page showing the passport number and date it expires * Visa (if the visitor traveled under one) * I-94 retrieval information from https://i94.cbp.dhs.gov/. Print out the I-94 and Travel History. * Entry stamp in the passport (if the passport was stamped) * Social security card or ITIN (If the visitor was previously issued one) This number is not required to receive an honorarium. * Travel itinerary from the airlines. * Letter of email inviting the visitor to lecture. This should include the dates of the lecture as well as the amount of the honorarium. https://i94.cbp.dhs.gov/ Required paperwork to pay an honorarium

* Social security card or ITIN (If the visitor was previously issued one) This number is not required to receive an honorarium. * Travel itinerary from the airlines. * Letter of inviting the visitor to lecture. This should include the dates of the lecture as well as the amount of the honorarium. Required paperwork to pay an honorarium.")

16

Departments should complete the top part of the FNIF before sending the packet to Tax Services. Our office will process the packet and return the following information to the department: * PeopleSoft Tax Withholding Information Form (PTWIF). This coversheet will contain all the codes needed to enter the payment in PeopleSoft. * 8233 Tax treaty form (if the visitor is eligible to claim a tax treaty). This form needs to be signed and returned before the ePAF is entered. Exceptions: If we find that the visitor is a resident for tax purposes (RA), the honorarium will need to be paid through AP. In this case they would need to sign a W-9 Form and complete a Vendor Payment Form. The visitor will be set up to receive a 1099 Form at year end. Required paperwork cont.

. This coversheet will contain all the codes needed to enter the payment in PeopleSoft. * 8233 Tax treaty form (if the visitor is eligible to claim a tax treaty). This form needs to be signed and returned before the ePAF is entered. Exceptions: If we find that the visitor is a resident for tax purposes (RA), the honorarium will need to be paid through AP. In this case they would need to sign a W-9 Form and complete a Vendor Payment Form. The visitor will be set up to receive a 1099 Form at year end. Required paperwork cont..")

17

Foreign vendors should complete a Vendor Application Form and one of the following W-8 Forms. W-8BEN Form- if the vendor is an individual W-8BEN-E Form- if the vendor is an entity W-8ECI Form- Individual or entity claiming that the income is effectively connected with a trade or business in the U.S. W-8EXP Form- To be completed by a foreign government, international organization, foreign tax-exempt organization. Paying a foreign vendor through AP

18

Departments should forward the Vendor Application and W-8 Form to Tax Services. The following questions will also need to be answered by the department. 1. What is the name of the vendor? [This name should be the same as the payee] 2. Is the foreign vendor a US Citizen living abroad? If not, Skip to #3. If so they will need to complete a W-9 Form in place of the W-8. A copy of their US passport page, showing citizenship, passport number will be required. 3. What service is the vendor providing to the University, or what is being purchased? [Please provide or attach description/ details] 4. What are the dates of service or time of the purchase? 5. What is the disbursement amount for this product/service? Will there be more than one payment? 6. If for service, where will the service be performed? 7. If for merchandise, will it be shipped directly from outside the States to the University? Vendor payments cont.

19

8. Will anyone from this company need to travel here to the States at any time as part of this service? a. If yes, list the dates of travel b. If this is an honorarium payment, additional paperwork will be required. 9. If for software: a. Will the software be used in your area? B. will the software be altered in any way or sold to the public? Taxing and coding of foreign vendor payments: * Payments for services provided in the States is taxable and reportable at year end. * Payments for services provided outside of the States is not taxable or reportable at year end. Vendor payments cont.

20

IRS Publications that can be found at www.irs.gov. 513- Tax information for Visitors to the U.S. 515- Withholding of Tax on Nonresident Aliens 519- U.S. Tax Guide for Aliens 901-U.S. Tax Treaties 970- Tax Benefits for Education Finance and Accounting http://www.fa.ufl.edu/directives-and-procedures/tax-services/ Any questions?www.irs.gov http://www.fa.ufl.edu/directives-and-procedures/tax-services/ Conclusion:

Similar presentations

University of Washington Student Fiscal Services.>")

>")

University of Washington Student Fiscal Services.>")