Download presentation

Presentation is loading. Please wait.

1

Supported by Workshop on Stochastic Analysis and Computational Finance, November 2005 Imperial College (London) G.N. Milstein and M.V. Tretyakov Numerical analysis of Monte Carlo evaluation of Greeks by finite differences J. Comp. Fin. 8, No 3 (2005), 1-33

,")

2

MC evaluation of Greeks by finite differences Plan Model Model Other approaches Other approaches Finite difference approach Finite difference approach Numerical integration error Numerical integration error Monte Carlo error Monte Carlo error Other Greeks Other Greeks Numerical examples Numerical examples Conclusions Conclusions

3

Model

4

Model

5

Model

6

Other approaches Broadie, Glasserman (1996); Milstein, Schoenmakers (2002)

; Milstein, Schoenmakers (2002)")

7

Other approaches Fournie, Lasry, Lebuchoux, Lions, Touzi (1999, 2001); Benhamou (2000)

; Benhamou (2000)")

8

Finite difference approach Standard finite difference formulas Weak-sense numerical integration of SDEs Monte Carlo technique

9

Finite difference approach Newton (1997); Wagner (1998); Milstein, Schoenmakers (2002); M&T (2004)

; Wagner (1998); Milstein, Schoenmakers (2002); M&T (2004)")

10

Weak Euler scheme

11

Estimator for the option price

12

Estimator for deltas

13

Estimators for deltas

14

Assumptions

15

Numerical integration error Proof. It is based on the Talay-Tubaro error expansion (Talay, Tubaro (1990); M&T (2004))

; M&T (2004)).")

16

Numerical integration error: proof

17

Monte Carlo error: price

18

Monte Carlo error: deltas If all the realizations are independent

19

Monte Carlo error: deltas Boyle (1997); Glasserman (2003), Glasserman, Yao (1992), Glynn (1989); L’Ecuyer, Perron (1994)

; Glasserman (2003), Glasserman, Yao (1992), Glynn (1989); L’Ecuyer, Perron (1994)")

20

Monte Carlo error: deltas

21

Main theorem

22

Higher-order integrators

23

Non-smooth payoff functions Bally, Talay (1996)

")

24

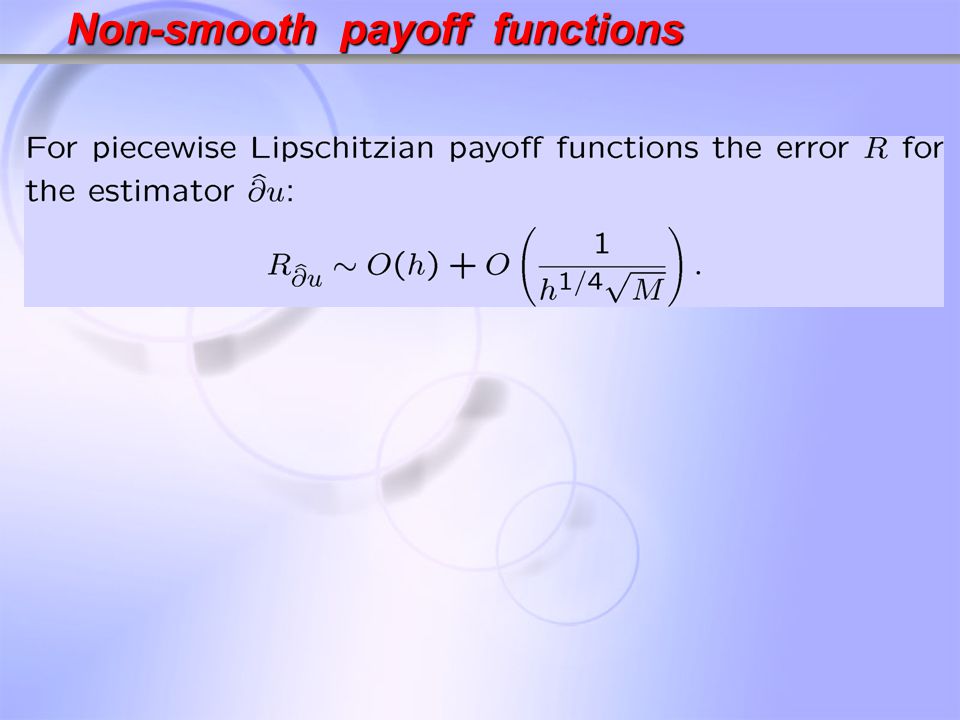

Non-smooth payoff functions

26

Other Greeks

27

Other Greeks: theta

28

Numerical tests: European call

29

Numerical tests: variance reduction Newton (1997); Milstein, Schoenmakers (2002); M&T (2004)

; Milstein, Schoenmakers (2002); M&T (2004)")

30

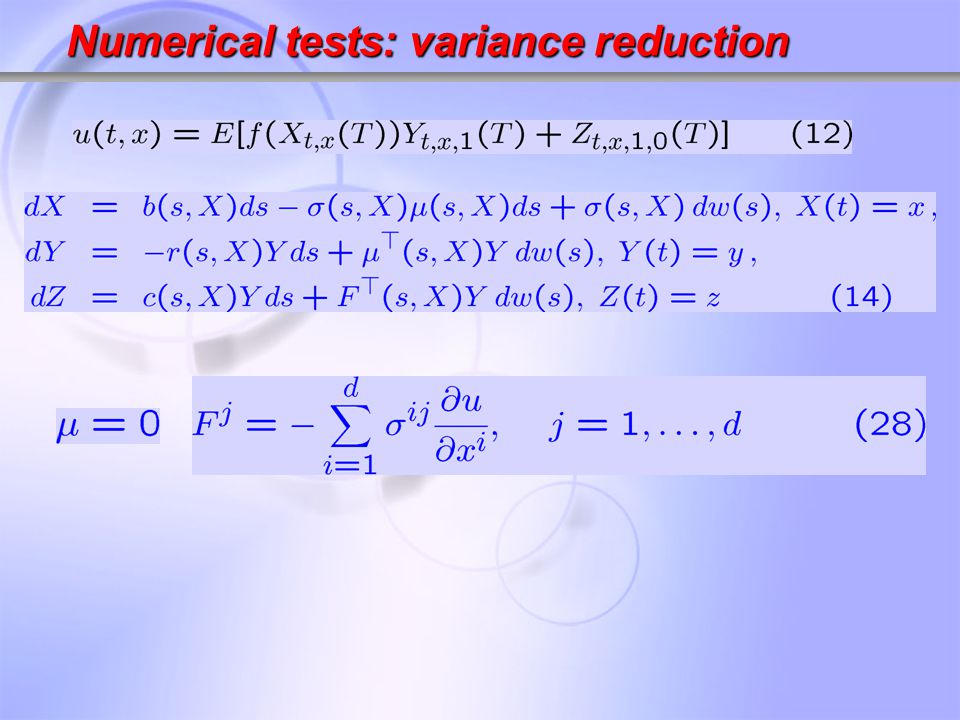

Numerical tests: variance reduction

32

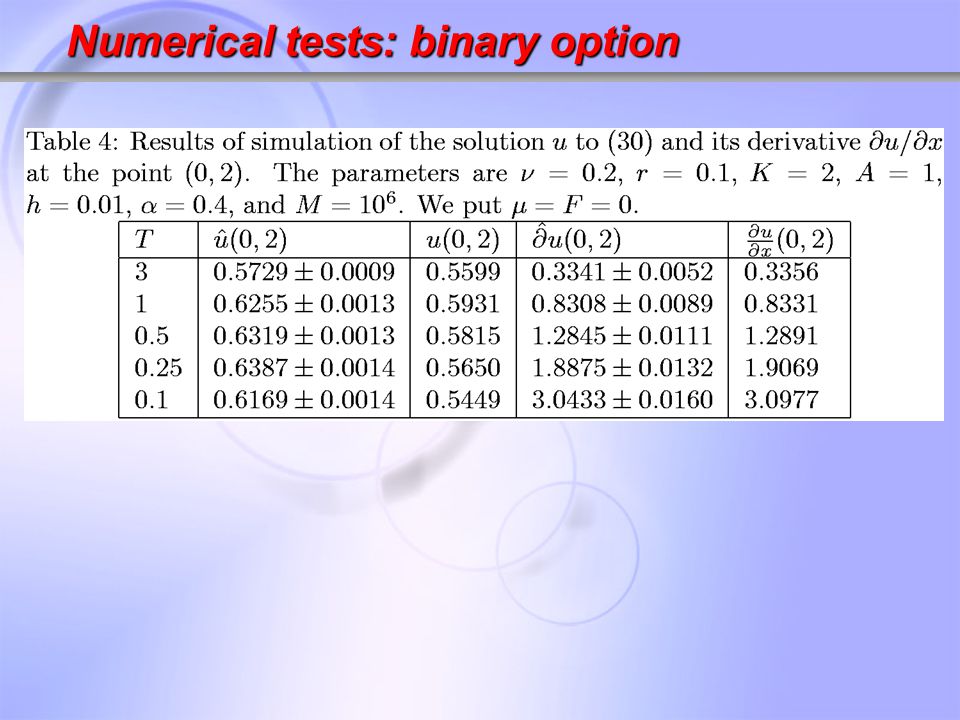

Numerical tests: binary option

34

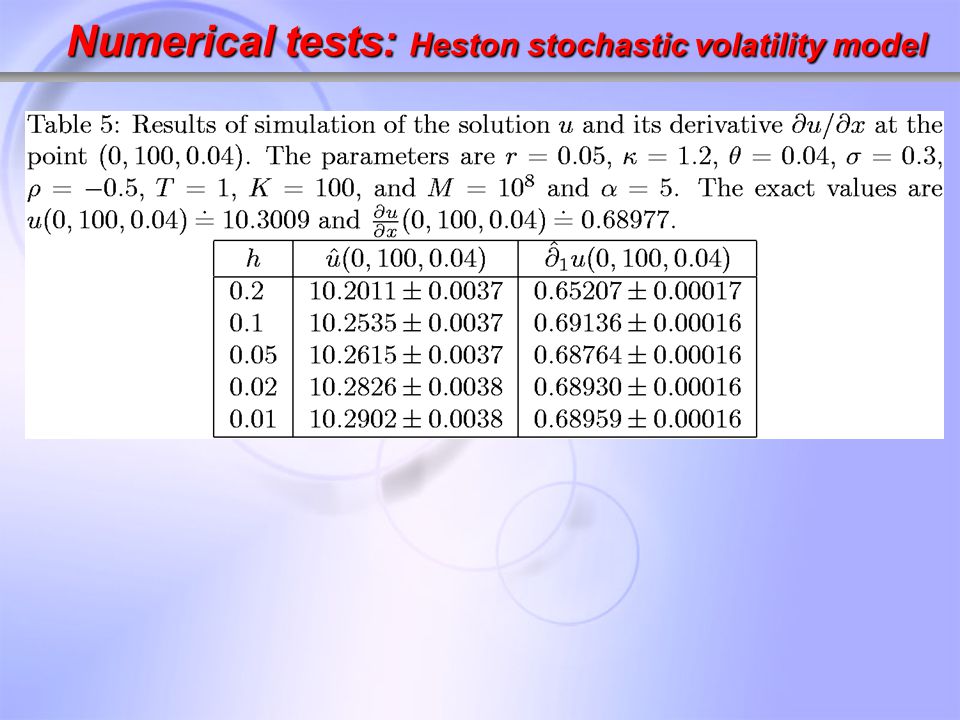

Numerical tests: Heston stochastic volatility model

36

Supported by Approximate deltas by finite differences taking into account that the price is evaluated by weak-sense numerical integration of SDEs together with the MC technique Exploit the method of dependent realizations in the MC simulations Rigorous error analysis Conclusions

Similar presentations