Download presentation

Presentation is loading. Please wait.

1

I NVENTORY AND C OST OF GOOD SOLD Chapter 5 T.Haya Alajaji

2

Objectives : 1. Inventory. 2. Explain how to report inventory and cost of goods sold. 3. Compute costs using four inventory costing methods

3

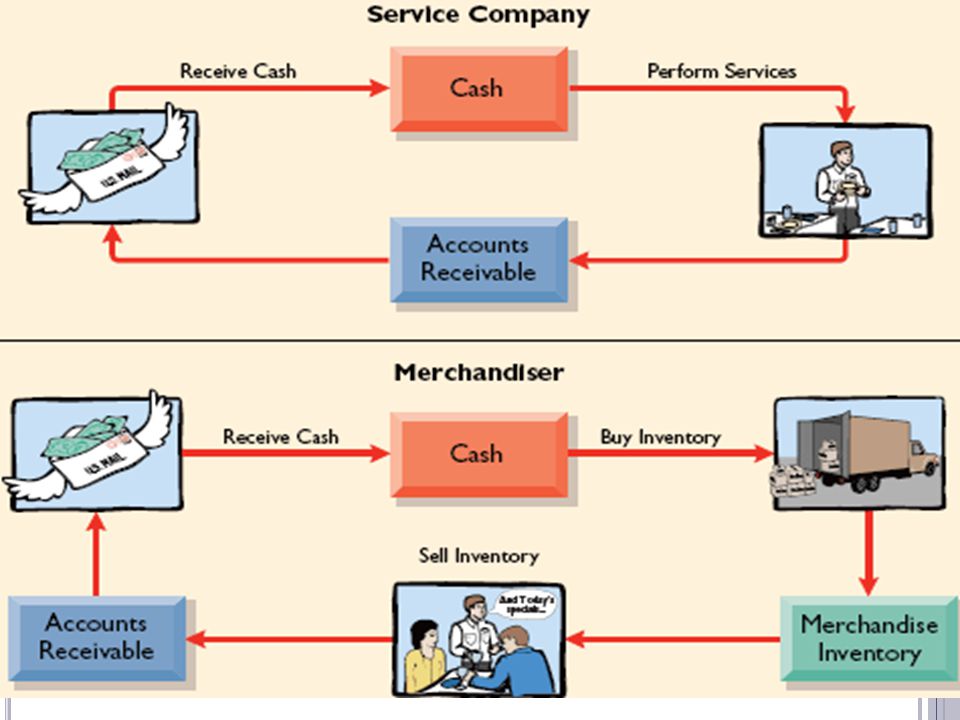

Ch5 InventoryGoods Raws Materils Merchandi s inventory Manufactu re inventory Raw Materials Work in Process Finished goods Merchandising Inventory = Balance Sheet Cost of Goods = Income Statement

5

I NVENTORY : inventory is a stock of goods or other items owned by a firm and hold for sale or for processing before being sold, as part of a firm’s ordinary operations. Goods or Raw material owned by the company.

6

T YPES OF I NVENTORY Merchandisers... Buy finished goods. Sell finished goods. Manufacturers... Buy raw materials. Produce and sell finished goods. Raw Materials Work in Process Finished goods Merchandise inventory Materials waiting to be processed Partially complete products Completed products awaiting sale 7-6

7

L EARNING O BJECTIVE 2 Explain how to report inventory and cost of goods sold in financial statement. 7-7

8

B ALANCE S HEET AND I NCOME S TATEMENT R EPORTING 7-8

9

C OST OF G OODS S OLD E QUATION BI + P – CGS = EI American Eagle Outfitters’ beginning inventory was $4,800. During the period, the company purchased inventory for $10,200. The cost of goods sold for the period is $9,000. Compute the ending inventory.

10

C OST OF G OODS S OLD E QUATION Beginning Inventory $4,800 + Goods Available for Sale $15,000 Purchases $10,000 Ending Inventory $6,000 (Balance Sheet) Cost of Goods Sold $9,000 (Income Statement)

Cost of Goods Sold $9,000 (Income Statement)")

11

L EARNING O BJECTIVE 3 Compute costs using four inventory costing methods.

12

I NVENTORY C OSTING M ETHODS First-in, first-out (FIFO) Last-in, first-out (LIFO) Weighted average

Last-in, first-out (LIFO) Weighted average")

13

I NVENTORY C OSTING M ETHODS Consider the following information This method individually identifies and records the cost of each item sold as part of cost of goods sold. If the items sold were identified as the ones that cost $70 and $95, the total cost of those items ($70 + 95 = $165) would be reported as Cost of Goods Sold. The cost of the remaining item ($75) would be reported as Inventory on the balance sheet at the end of the period. Specific Identification May 5 $75 cost May 3 $70 cost May 6 $95 cost 7-13

would be reported as Cost of Goods Sold. The cost of the remaining item ($75) would be reported as Inventory on the balance sheet at the end of the period. Specific Identification May 5 $75 cost May 3 $70 cost May 6 $95 cost")

14

I NVENTORY C OSTING M ETHODS FIFOLIFOWeighted average May 6 $95 cost May 5 $75 cost May 3 $70 cost May 6 $95 cost May 5 $75 cost May 3 $70 cost May 6 $95 cost May 5 $75 cost May 3 $70 cost Sold Still there Sold Still there Sold Still there $240 3 = $80 per unit 7-14

15

I NVENTORY C OSTING M ETHODS Summary

16

I NVENTORY C OST F LOW C OMPUTATIONS Weighted Average Weighted Average Cost = Cost of goods Available for Sale Number of Units Available for Sale Weighted Average Cost = $410 50 units = $8.20 per unit

17

I NVENTORY C OST F LOW C OMPUTATIONS 15 units @ $8.20 35 units @ $8.20

18

F INANCIAL S TATEMENT E FFECTS 7-18

19

F INANCIAL S TATEMENT E FFECTS 7-19

Similar presentations

8 Brown/Red ($2 each) 2) 7 Blue/Green ($3 each) 3) 5 Yellow/Orange ($4 each) 20 Total.>")