Download presentation

Presentation is loading. Please wait.

1

Introduction to Economics

2

What is Economics? Scarcity: Economics is about the allocation of scarce resources among society’s various needs and wants. Tradeoffs: individuals and society as whole are constantly making choices involving tradeoff between alternatives. Whether it’s what goods to consume, what goods to produce, how to produce them, and so on. Opportunity Cost: “the opportunity cost is the opportunity lost”. In other words, every economic decision involves giving up something. NOTHING IS FREE!! Humans' wants are unlimited, while the resources needed to meet those wants are limited and scarce

3

What is Economics? People can’t have everything they want or need, must consider options to decide how to fulfill their needs when they face a limited supply of resources Economics is how people seek to satisfy their needs and wants by making choices Why must people make these choices? The reason is scarcity Americans find it hard to understand scarcity We have an abundance of goods and services

4

Scarcity Limited quantities of resources to meet unlimited wants, never an unlimited supply of anything Shortage- can’t offer goods or services at current prices (can be short term or long term) Scarcity- always exists because there is never an unlimited quantity Goods and services are scarce because they are made from resources that are scarce

Scarcity- always exists because there is never an unlimited quantity. Goods and services are scarce because they are made from resources that are scarce.")

5

Land, Labor and Capital Four resources used to make goods and services are called factors of production Factors of production are land, labor and capital Land- natural resources used to produce goods (farmland and products, coal, oil, etc.) Labor- effort used by person for which person is paid Capital- human made resource that is used to produce goods and services, two categories physical and human capital

Labor- effort used by person for which person is paid. Capital- human made resource that is used to produce goods and services, two categories physical and human capital.")

6

Two Types of Capital Physical Capital- human made objects used to create goods and services Important factor of production because it can save a great deal of time and money, increases efficiency Human Capital- knowledge and skills a worker gains through education and experience Entrepreneurs- (4th factor) Pull resources together Decide how to pull together land, labor and capital to produce goods and services

Pull resources together. Decide how to pull together land, labor and capital to produce goods and services.")

7

Scarce Resources All goods and services are scarce because land, labor and capital are limited What goes into making French fries?

8

Opportunity Cost Trade offs- alternatives we sacrifice when we make a decision, individuals and businesses make trade offs Business’ make trade offs on how to use land, labor and capital resources Societies and governments make trade offs Economists call these decisions guns or butter, a country that chooses to make military equipment has fewer resources to devote to food production

9

Defining Opportunity Cost

One alternative is always more desirable than another, desirable alternative given up is opportunity cost Example- Every day decision to sleep late or study , what you are willing to give up (better grades, more rest) is the opportunity cost We select one alternative from the decisions we have to make and forgo the benefits of the others

is the opportunity cost. We select one alternative from the decisions we have to make and forgo the benefits of the others.")

10

Opportunity Cost You must give up something to have what you want

Examples: The opportunity cost of watching TV on a weeknight is the benefit you could have gotten from studying. The opportunity cost of going to college is the income you could have earned by getting a job out of high school The opportunity cost of starting your own business is the wages you give up by working for another company The opportunity cost of using forest resources to build houses is the enjoyment people get from having pristine forests

11

Thinking at the Margin Deciding whether to add or use one additional unit of a resource Need to make decisions, when is the cost no longer worth the benefit? Thinking at the margin lets us evaluate options based on available resources Decision making process is called cost/benefit analysis Means making a decision about how much more or less to do Allows us to evaluate options based on available resources Once opportunity cost outweighs benefits no more units should be added

12

Production Possibilities Curves

Economists use graphs to decide what trade offs to make Production possibilities curves (PPC) are used to decide ways to use productive resources, what goods and services to produce Illustrates the possible combinations of goods or services that can be produced by a single nation, firm, or individual using resources efficiently Using resources to produce one product means fewer resources are available to make something else

are used to decide ways to use productive resources, what goods and services to produce. Illustrates the possible combinations of goods or services that can be produced by a single nation, firm, or individual using resources efficiently. Using resources to produce one product means fewer resources are available to make something else.")

13

Efficiency, Growth and Cost

PPC can show how productive an economy is, its growth or possibility for growth Efficiency- maximizing resources for production output of goods and services Underutilization is using fewer resources than the economy is capable of using Growth- availability of resources are constantly changing Examples- increase in labor force or better technology causes growth; aging population or health crisis can stop growth

14

Efficiency, Growth and Cost

Cost- alternative we give up when we choose one product over another Not always money Always means opportunity cost Increasingly expensive trade offs known as law of increasing costs Law states that as production switches from one item to another more resources are needed to produce second item, opportunity cost increases Technology has an effect on the PPC, production possibilities depend on the technological level and resources available

15

Economic Systems Chapter 2

16

Economic Systems Scarcity forces societies to make decisions

Different economic systems have evolved in response to the problem of scarcity Economic system- method used by society to distribute goods and services

17

Economic Systems What goods and services should be produced?

Three Key Economic Questions What goods and services should be produced? How should these goods and services be produced? Who consumes these goods and services?

18

What to Produce? Basic Needs: Food, Clothing, and Shelter

Examples include: Basic Needs: Food, Clothing, and Shelter Wants: Luxury Items Services: Education, Health Care, Defense, etc. Each production decision has an opportunity cost

19

How should goods and services be produced?

How to use our resources Decide how to use factors of production Examples Include: Size and Organization of Facilities Time and Effort Committed

20

Who consumes these goods and services?

How are goods and services divided up? How do societies distribute income? How do we decide the worth of a factor of production? Factors of payment- income people receive for supplying factors of production (rents, wages, profits) Society places different values on different resources and products Examples Include: Choices in Products The Value/Price of Products Access to Services

Society places different values on different resources and products. Examples Include: Choices in Products. The Value/Price of Products. Access to Services.")

21

Economic Goals and Social Values

Different societies answer these economic questions based on the importance they attach to economic goals They pursue each of these goals at the expense of others (opportunity cost) There are 5 major goals 1. Economic efficiency- maximize what they can get for the resources they have to work with 2. Economic freedom- different nations have different degrees of economic freedom Americans have freedom from government intervention in the production of goods and services

There are 5 major goals. 1. Economic efficiency- maximize what they can get for the resources they have to work with. 2. Economic freedom- different nations have different degrees of economic freedom. Americans have freedom from government intervention in the production of goods and services.")

22

Economic Goals and Social Values

3. Economic security and predictability- economic systems reassure people that goods and services will be available and that government will provide a safety need for needy and those with economic disadvantages 4. Economic equity- how society divides the economic pie, society does not value all jobs equally

23

Economic Goals and Social Values

5. Economic growth and innovation- economy must grow to improve its standard of living, provide jobs and income Innovation plays a role in growth it increases production and brings new goods and services Additional Goals- Other important concerns (health care for everybody, environmental concerns), nations must prioritize Achieving goals comes with a trade off

, nations must prioritize. Achieving goals comes with a trade off.")

24

The aftermath of Hurricane Katrina

The aftermath of Hurricane Katrina. What economic goals could help them recover from this storm?

25

Different Economic Systems

Four distinct economic systems have developed to address these key economic questions Each reflects the values of the societies they represent Traditional economy- relies on habit, custom and ritual Little room for innovation and change Family oriented and it works along gender lines Often from small societies that have a low standard of living and a lack of modern conveniences

26

Different Economic Systems

Market Economy- decisions are made by individuals and based on exchange and profit Individuals determine the answers to the three basic economic questions Also known as capitalism or free market economy Command Economy- government decides how to answer three key questions Also known as a centrally planned economy Mixed Economy- market based system where government plays a limited role and free markets play a role

27

The Free Market Market – an arrangement that allows buyers and sellers to exchange things Why do they exist? Nobody is self- sufficient, allow us to exchange what we have for what we want We can’t produce everything so we just produce a few or one product This is called specialization (concentration of efforts on a limited number of activities) Specialization allows us to sell what we make and buy what we want

Specialization allows us to sell what we make and buy what we want.")

28

Free Market Economy Economic systems based on voluntary exchanges in markets called free market economy Individuals own factors of production and answer three key economic questions Key players in free market economy are households and firms Households consume goods and services, own factors of production Firms are organization that produce goods and services; take inputs (factors of production) and turn them into outputs( products)

and turn them into outputs( products)")

29

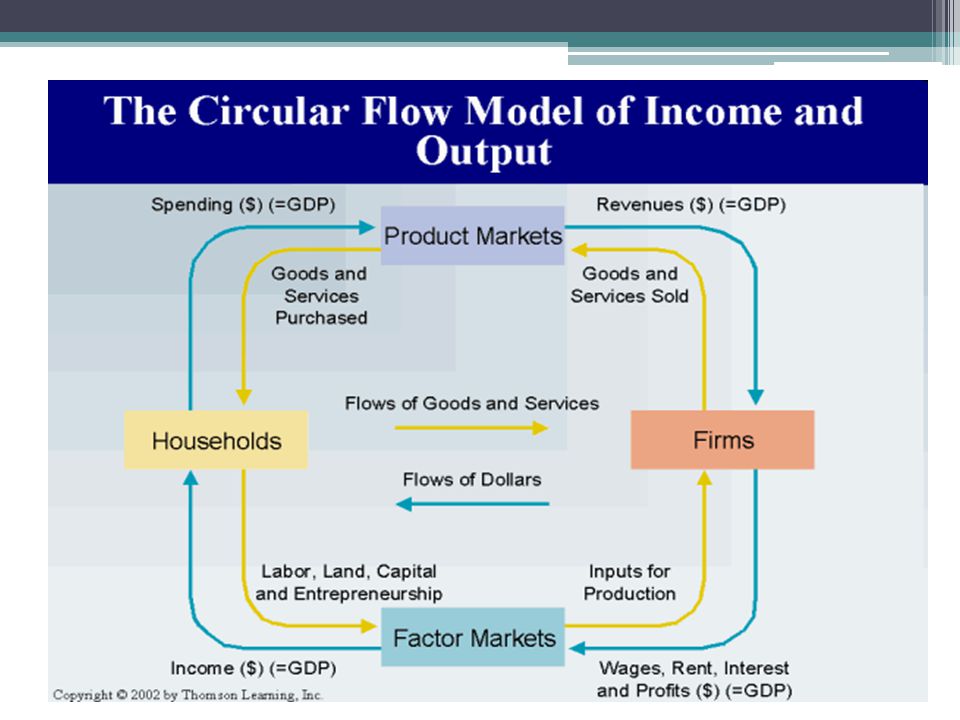

Free Market Economy Firms purchase factors of production from households Hire workers, pay wages, borrow money to purchase capital and paying them in interest or profit in return Area of exchange called a factor market Goods and services firms produced are purchased by households in the product market These exchanges are represented in a circular flow diagram that shows how individuals and businesses exchange money

31

The Self- Regulating Nature of the Marketplace

Why do these groups cooperate ? According to Scottish social philosopher Adam Smith it is competition and our own self interest that keeps marketplace moving Smith wrote Wealth of Nations (1776) that described how the market functions Self Interest He said an economy is made up of countless transactions In each the buyer and seller consider only their own self interest and this motivates the free market

that described how the market functions. Self Interest. He said an economy is made up of countless transactions. In each the buyer and seller consider only their own self interest and this motivates the free market.")

32

The Self- Regulating Nature of the Marketplace

Competition Because of self interest consumers have an incentive to look for the best prices Firms seek to make greater profit by increasing sales The struggle between producers and consumers is called competition Self interest is a motivating force and competition is a regulating force These forces working together to regulate the market was called by Smith “the invisible hand”

33

Advantages of the Free Market

Economic efficiency- responds rapidly to changing conditions Economic Freedom- workers work where they want, producers produce what they want Economic Growth- competition and the profit motivate encourage growth and innovation Additional Goals- offers a wide variety of goods and services, consumers decide what is produced (consumer sovereignty) Weaknesses of a free market- no pure free market exists, economic equity and economic security are difficult to achieve

Weaknesses of a free market- no pure free market exists, economic equity and economic security are difficult to achieve.")

34

Centrally Planned Economies

35

How is a Centrally planned Economy Organized?

Direct contrast to free market economy Central government answers key economic questions Government owns factors of production, set quotas on what to produce Self interest and competition absent from system There is no consumer sovereignty

36

Socialism and Communism

Socialism political and social philosophy based on belief that democratic means should be used to distribute the wealth Public controls centers of economic power Government owns major industries Communism economic and political power lies in the hands of the central government Society can only change after a violent revolution and all government is authoritarian

37

The Former Soviet Union

Russian Revolution in early 20th century led to rise of communism and central planning USSR concerned with status as world power Allocated all factors of production and put resources in hands of armed forces, factories and agriculture Agriculture and industry established quotas to and distribution systems planned by central government Took away incentive for production, quality and innovation Left consumers with low quality goods because state had to buy them Makers of consumer goods and consumers experienced the burden of this opportunity cost

38

Problems with Centrally Planned Economies

Can be used to jumpstart industries and guarantee jobs and income Disadvantages Lack of incentive can lead to poor quality goods and diminishing production Stalin had some success in USSR with heavy industry Performance always falls short of ideals Systems lack flexibility to meet consumer demands and wants Sacrifice individual freedom for societal goals Few countries have centrally planned economies because experiment has failed Many countries are moving toward a mixed economy

39

Modern Economies

40

The Rise of Mixed Economies

Most contemporary economies are mixed economies that blend the market and government intervention Limits of Laissez Faire Smith thought free market brought greatest benefit and raised standard of living Laissez faire doctrine that government should not interfere in marketplace Over time market economies have evolved, needs an wants of society are difficult to meet in a totally free marketplace

41

The Rise of Mixed Economies

Governments create laws protecting property, enforcing contracts and insisting on competition Provides incentive for innovation, and keeps one firm from dominating marketplace Society has to assess values and prioritize economic goals Some goals met better by market and some by government Each nation decides opportunity cost to pursue goals (what they have to give up)

")

42

Circular Flow of Mixed Economy

Government purchases land, labor and capital from households in the factor market (federal employees) Government purchases goods and services in the product market (office supplies) Government provides goods and services through combination of factor resources (roads) Government collects taxes from individuals, businesses and transfers it across the economy

Government purchases goods and services in the product market (office supplies) Government provides goods and services through combination of factor resources (roads) Government collects taxes from individuals, businesses and transfers it across the economy.")

43

Comparing Mixed Economies

Foundation of US economy is free market (private ownership of capital goods) where individuals make decisions rather than the state At one end lies North Korea at the other is Hong Kong

where individuals make decisions rather than the state. At one end lies North Korea at the other is Hong Kong.")

44

Comparing Mixed Economies

North Korea- almost totally controlled by the government, business owned by government and imports banned China- economy is dominated by government, many enterprises are becoming owned by individuals (privatization), China is a transition economy Hong Kong- one of the worlds freest markets, private sector rule and there is rarely government interference except to control some rents and wages

, China is a transition economy. Hong Kong- one of the worlds freest markets, private sector rule and there is rarely government interference except to control some rents and wages.")

45

American Free Enterprise

46

Tradition of Free Enterprise

America considered “land of opportunity”, can achieve success through hard work Why has America had economic success? Open land, natural resources, open (?) immigration, tradition of free enterprise (commitment to giving people freedom and flexibility to compete in the marketplace)

immigration, tradition of free enterprise (commitment to giving people freedom and flexibility to compete in the marketplace)")

47

Constitutional Protection

Constitution guarantees rights that allow people to engage in business activities Property rights- 5th, 14th Amendments 5th Amendment protects property rights from government interference, 14th amendment limits state governments from taking property Government must provide a fair price for property that is taken (imminent domain)

")

48

Constitutional Protection

Taxation Constitution has basic rules to tax individuals and businesses 16th Amendment (1913) gave Congress power to tax based on income Article I, Sec. 10 gives businesses the right to make contracts, term can’t be changed by legislative action, political process can’t be used to get out of contracts

gave Congress power to tax based on income. Article I, Sec. 10 gives businesses the right to make contracts, term can’t be changed by legislative action, political process can’t be used to get out of contracts.")

49

Basic Principles of Free Enterprise

Key characteristics: profit motive, open opportunity, legal equality, private property rights, free contracts, voluntary exchange, competition Profit Motive- force that encourages improvement of material well being, makes people responsible for their own success and failure, rewards innovation Open Opportunity- everyone can compete in the marketplace, allows economic mobility up and down

50

Basic Principles of Free Enterprise

Economic Rights- legal equality everyone has the same rights property rights right to control property and possessions free contract decide what agreements we want to enter into voluntary exchange decide what we want to buy and sell competition rivalry among sellers and customers

51

Role of the Consumer Fundamental purpose is to give consumer freedom to make economic choices Consumers can make wishes known by forming interest groups to persuade public officials on economic issues like taxation, land use, etc.

52

The Role of Government Expect government to carry out duties and protect Constitutional rights, and business activities Information and free enterprise- consumers expect basic information on what we purchase, educated consumers make market work more efficiently Protecting health, safety and well- being- government regulates industry, imposes various restrictions (consumer protection laws, environmental regulation) Negative effects of regulation- protections costly to implement and can lead to higher prices, stifles competition

Negative effects of regulation- protections costly to implement and can lead to higher prices, stifles competition.")

53

Promoting Growth and Stability

American economy very big, armies of economists predict whether business will grow or shrink One way to measure economic trends is calculate Gross Domestic Product (GDP), total value of all goods and services produced by economy GDP can predict business cycles (periods of expansion followed by contraction) Free enterprise subject to ups and downs because economic decisions are made by business and individuals acting in their own self interest

, total value of all goods and services produced by economy. GDP can predict business cycles (periods of expansion followed by contraction) Free enterprise subject to ups and downs because economic decisions are made by business and individuals acting in their own self interest.")

54

Promoting Economic Strength

Government makes public policy to stabilize economy Goals are high employment, steady growth and stable prices Unemployment- rate 4-6% is desirable, economic policy is to create jobs Growth- Each generation wants higher standard of living than previous generation, means economy must grow Stability- People want stable economy; government promotes stability, keeps prices from sudden dramatic shifts Desire stable financial institutions, money protected from fraud and mismanagement Governments regulate business and banks to insure stability Elective choices guide government economic policy

55

Technology and Productivity

American have higher standard of living than most other countries Factors- work ethic, technology Work ethic- Americans value work and purposeful activity Technology- produces more output, allows economy to operate efficiently and productively Gives US competitive advantages

56

The Government’s Role Government is engine of free enterprise system

Provides incentives for innovation Funds research and development through universities, own research institutions (NASA) Offers inventors possibility of making huge profits through patent and copyright grants Patent- exclusive right to produce and sell product for 20 years Copyright- exclusive right to sell creative works Copyrights and patents protected by Constitution (Article1, Sec. 8)

Offers inventors possibility of making huge profits through patent and copyright grants. Patent- exclusive right to produce and sell product for 20 years. Copyright- exclusive right to sell creative works. Copyrights and patents protected by Constitution (Article1, Sec. 8)")

57

Providing Public Goods

Shared good or service for which it would be impractical to make consumers pay for individually or to exclude non payers Making customers fund projects in public interest is the reason behind taxation To not exclude non-payers we believe certain facilities and services should be available to all Everybody should be able to use public goods without reducing the benefits to any single consumer

58

Costs and Benefits of Public Goods

Cost critical in determining whether something is produced as public good Benefit to each individual is less than cost that each would have to pay if it were provided privately Benefits to society are greater than cost Public goods financed by public sector (part of economy that involves transactions of government)

")

59

Free Rider Problem Free rider- someone who would not choose to pay for something but would receive benefits anyway, consume what they do not pay for Fire protection, national defense are examples Taxes are collected to reduce this phenomenon All people are better off if government provides service

60

Market Failures and Externalities

Market failure situation in which market does not distribute resources efficiently Markets operate on individual choice, competition and self interest, distributes resources unevenly Public ownership can produce positive and negative side effects called externalities Externalities- economic side effect of a good or service that generates benefits or costs to someone other than the person deciding how much to produce or consume (side effects of economic decisions)

")

62

Positive and Negative Externalities

Positive externalities- Public goods that generate benefits to many people Many believe that private sector can generate positive externalities more efficiently Negative externalities- cause part of the cost to be paid by someone other than the producer Government’s goals- encourage creation of positive externalities (ex. education), limit negative externalities (ex. pollution)

, limit negative externalities (ex. pollution)")

63

Providing a Safety Net Free market great a generating wealth, but wealth is spread unevenly through society Some live below poverty threshold (income level below what is needed to support a household) Government tries to provide opportunity to lift poor out of poverty Society recognizes need to help elderly, very young, poor, disabled; to help government provides a safety net Many want a limited government role

Government tries to provide opportunity to lift poor out of poverty. Society recognizes need to help elderly, very young, poor, disabled; to help government provides a safety net. Many want a limited government role.")

64

The Welfare System 1930’s government took a more active role to ease poverty, funds redistributed in form of welfare Great Depression started social welfare programs, increased in 1960’s during Lyndon Johnson’s “War on Poverty” 1990’s concern with population becoming dependent on welfare led to reform, arguments were that it discouraged productivity

65

Redistribution Programs

Major redistribution programs run by federal government Cash transfers- direct payments Temporary Assistance for Needy Families- states are given welfare funds, establish rules and work benefits, placed limits on benefits Social Security- provides money to retired, disabled Americans Unemployment insurance- provides money to workers that lost their jobs Workers Compensation- provides money to workers injured on job, employers pay insurance to fund program

66

Redistribution Programs

In-Kind Benefits- goods and services provided free or greatly reduced benefits (food stamps, subsidized housing) Medical Benefits Medicare- health insurance for elderly, disabled Medicaid- covers unemployed and those not covered by insurance (COBRA) Education- education provided from preschool to college, adds to productivity of nation Faith-Based Initiatives Signed by Bush gives government support to religious organizations to deliver social services

Medical Benefits. Medicare- health insurance for elderly, disabled. Medicaid- covers unemployed and those not covered by insurance (COBRA) Education- education provided from preschool to college, adds to productivity of nation. Faith-Based Initiatives. Signed by Bush gives government support to religious organizations to deliver social services.")

Similar presentations