Download presentation

Presentation is loading. Please wait.

1

Chapter 8 Mean-Reverting Processes and Term Structure Modeling

2

Short And Long Term Rates As discussed in Chapters 3 and 4, the yield curve depicts varying spot rates over associated bond terms to maturity. Spot rates are interest rates on loans originated at time zero (e.g., now). The yield curve is typically constructed from the yields of benchmark highly liquid (where possible) default-free fixed income and/or zero coupon instruments. Bond prices are affected by short-term (technically, instantaneous short rates) and long-term interest rates. Instantaneous rates, which are unobservable because they don't actually exist in reality, might be proxied by overnight rates.

. The yield curve is typically constructed from the yields of benchmark highly liquid (where possible) default-free fixed income and/or zero coupon instruments. Bond prices are affected by short-term (technically, instantaneous short rates) and long-term interest rates. Instantaneous rates, which are unobservable because they don t actually exist in reality, might be proxied by overnight rates..")

3

Short And Long Term Rates (Continued) We will focus on single factor models, where the entire yield curve and its related bond prices are driven by a single factor, being short-term interest rates. These short-term interest rates in turn will be modeled as particular stochastic processes. How one chooses a short-interest rate model is a matter of taste, and there is a variety of models to choose from. We will discuss a number of these models in this chapter. More generally, understanding the stochastic processes that drive security prices, interest rates and other rates is essential to valuing and hedging the securities, their derivative securities and portfolios related to them. In this chapter, we analyze alternatives to Brownian motion processes for security and rate process, with a particular focus on interest rates and debt instruments.

4

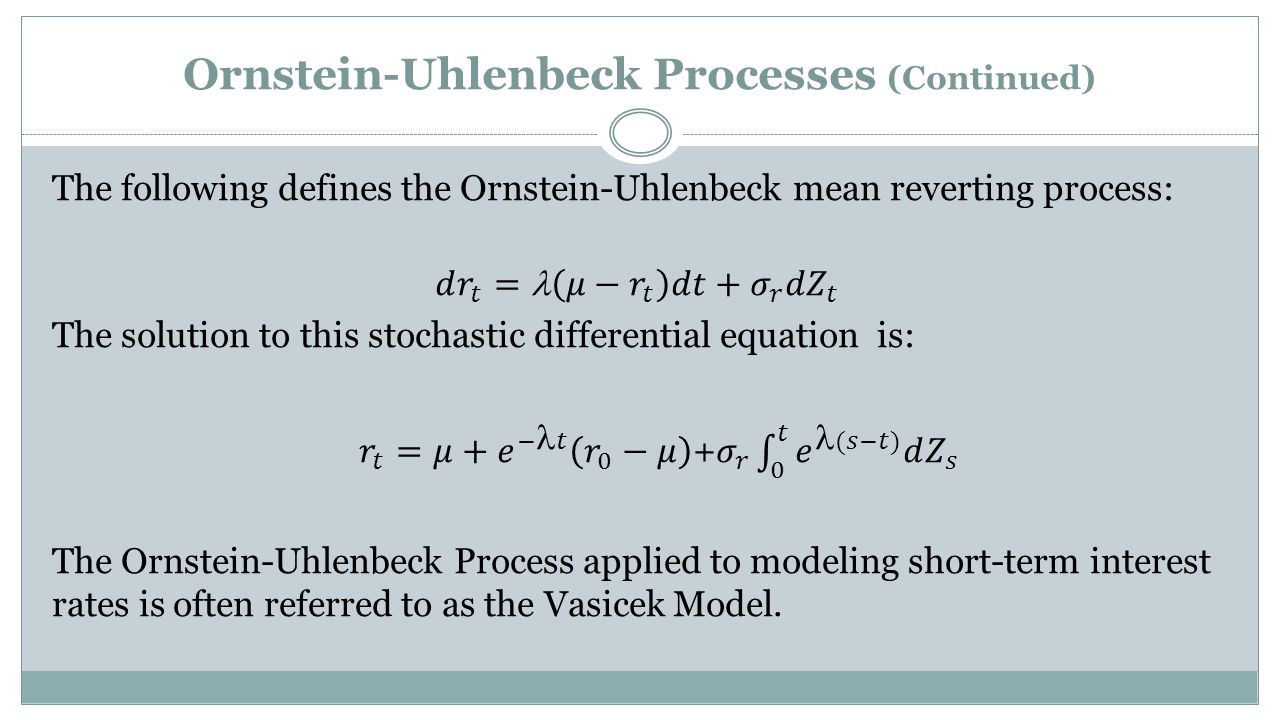

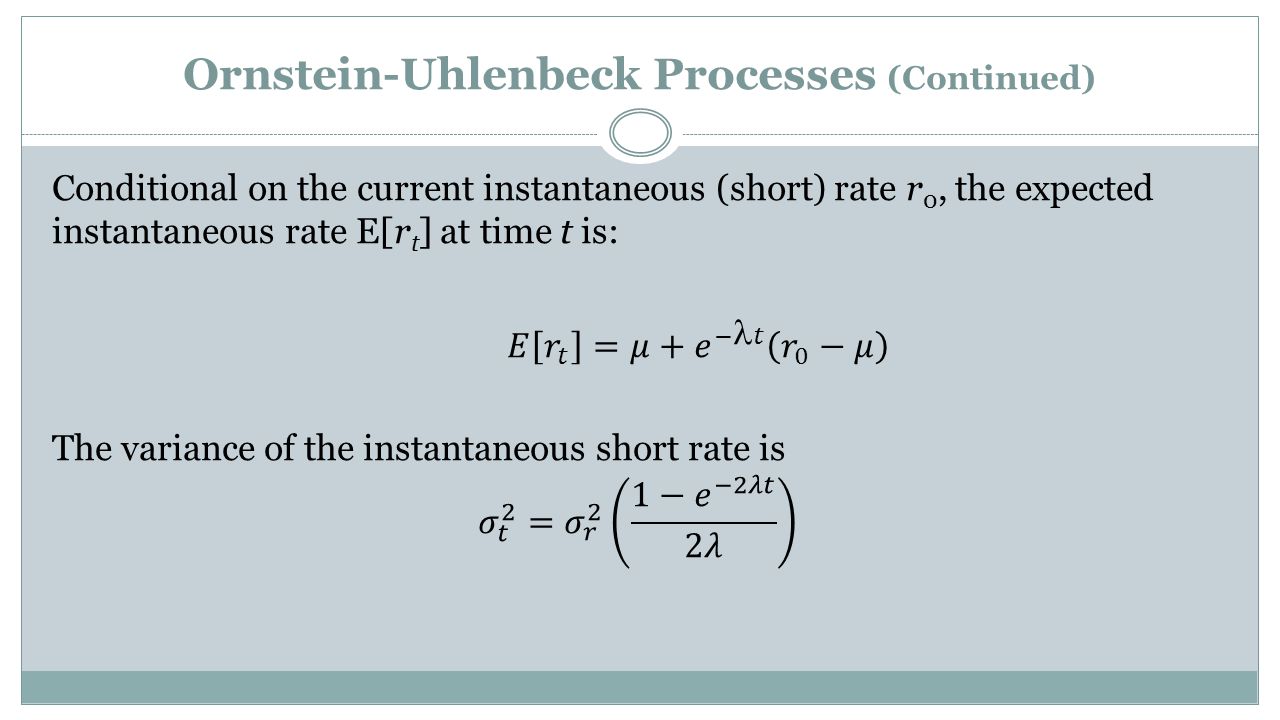

Ornstein-Uhlenbeck Processes

5

Ornstein-Uhlenbeck Processes (Continued)

")

8

Illustration Of The Vasicek Model

9

Illustration Of The Vasicek Model (Continued)

")

11

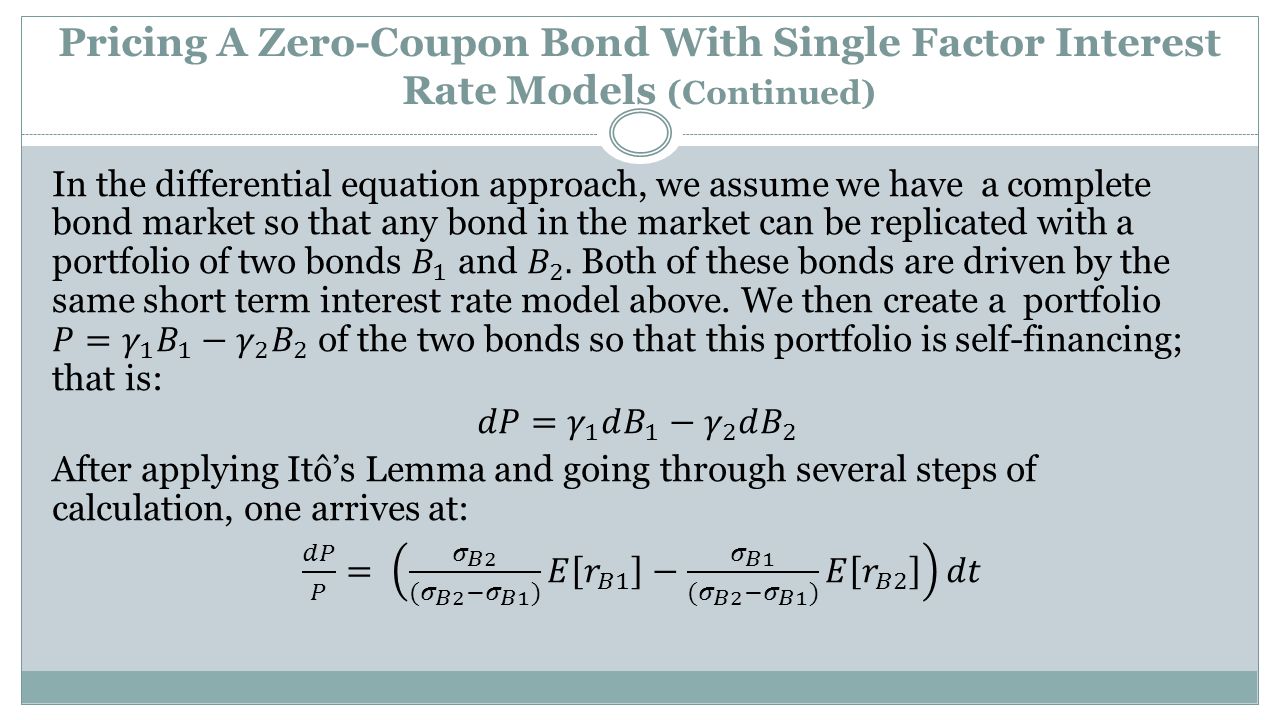

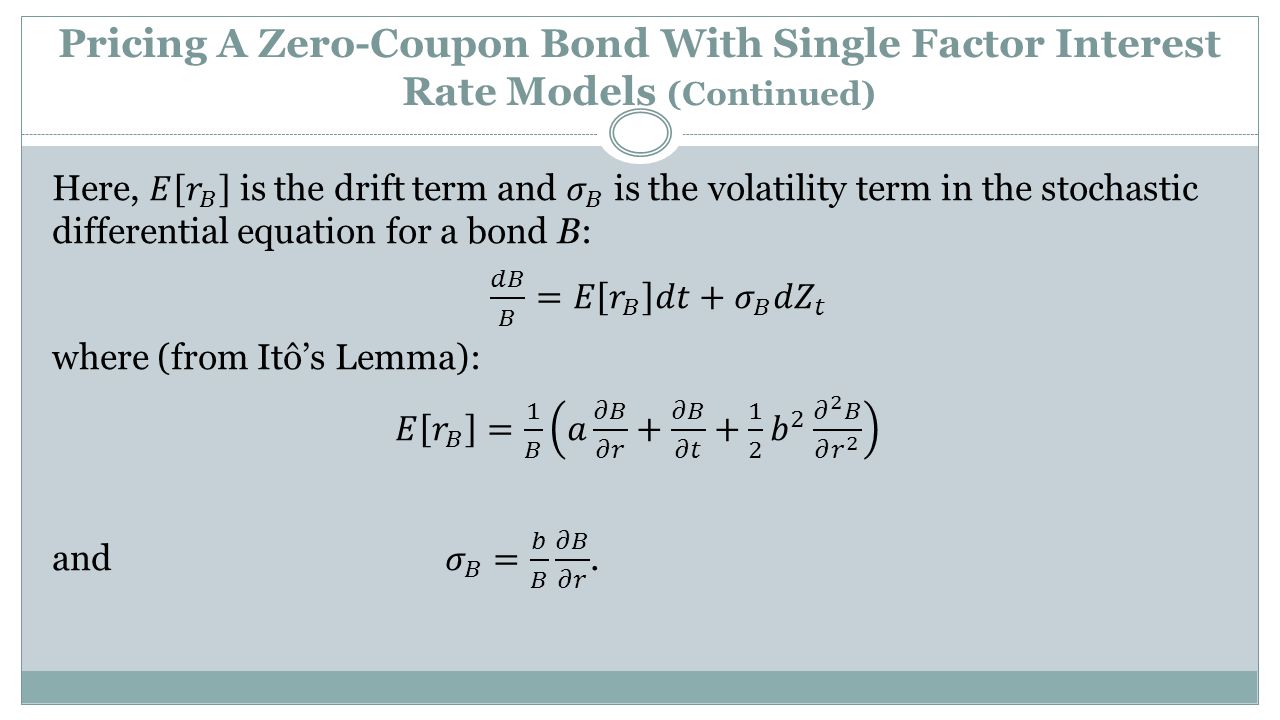

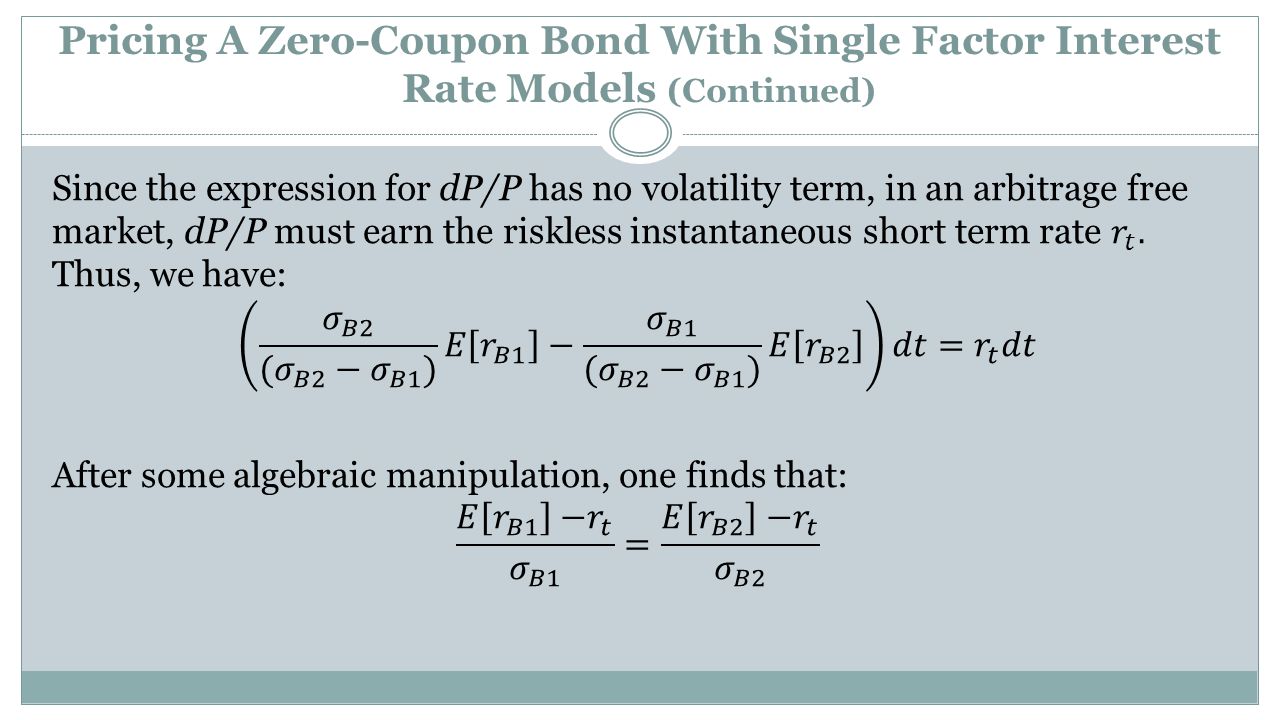

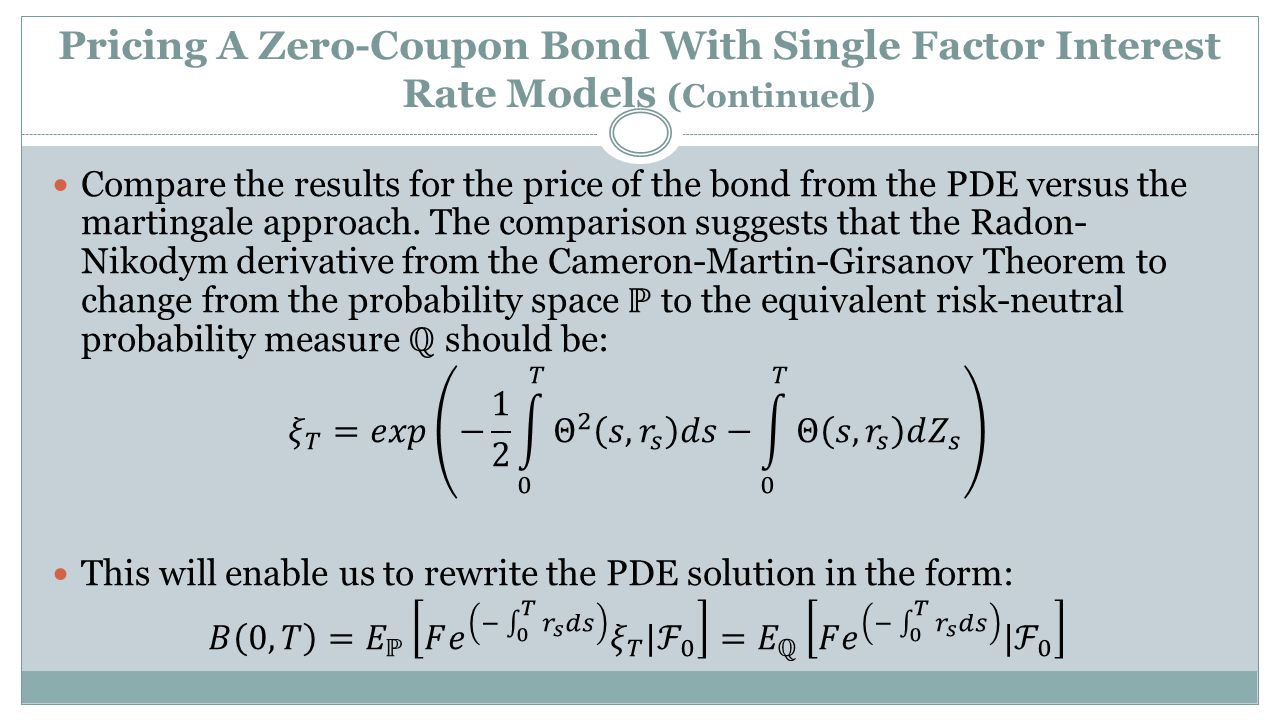

Pricing A Zero-Coupon Bond With Single Factor Interest Rate Models

12

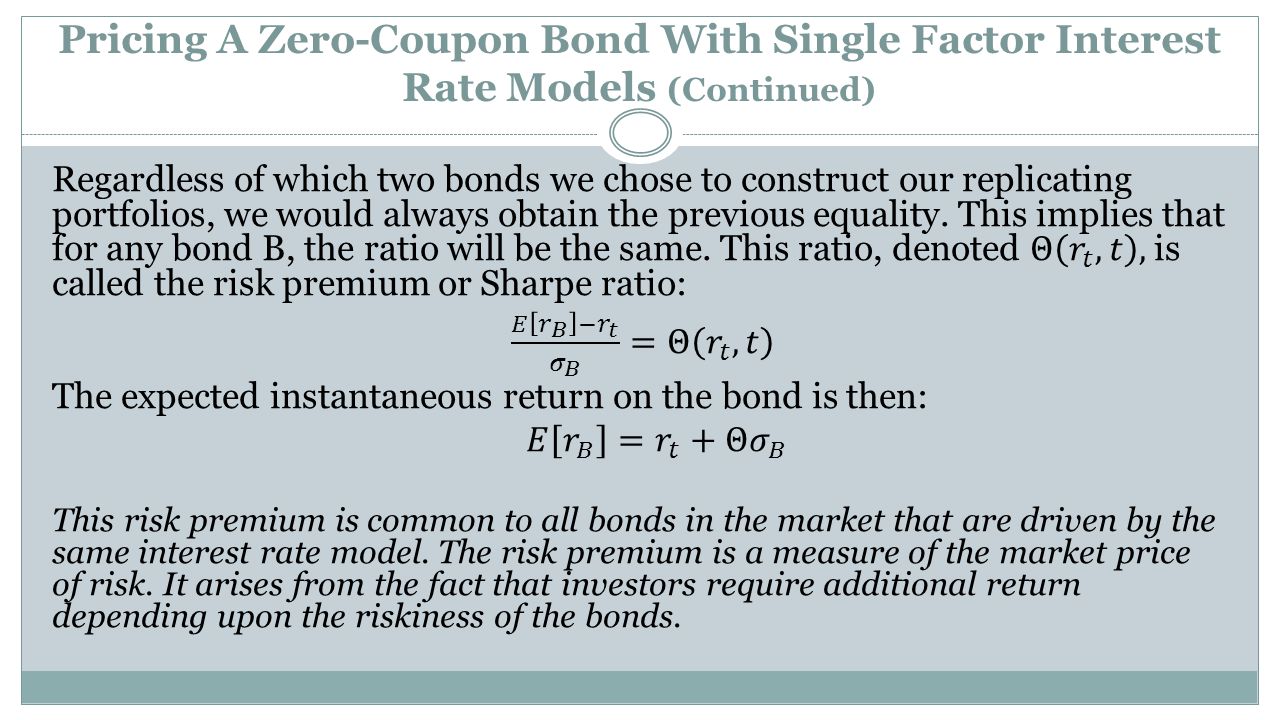

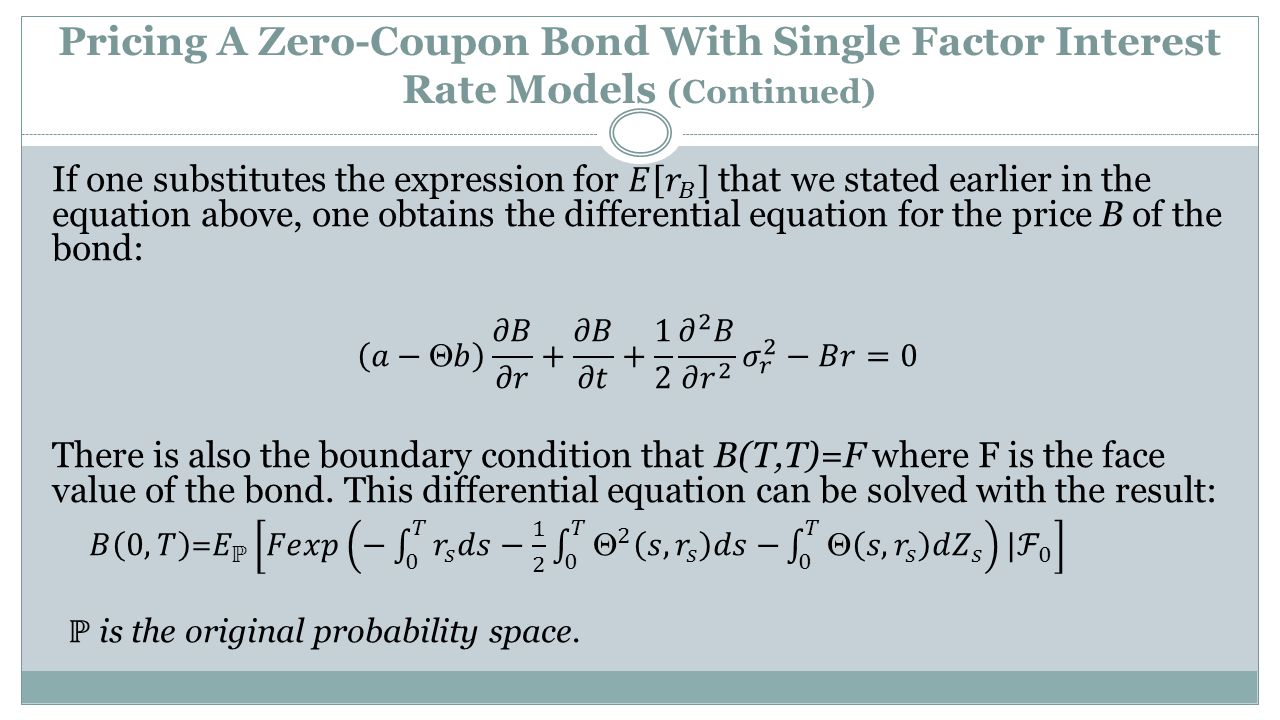

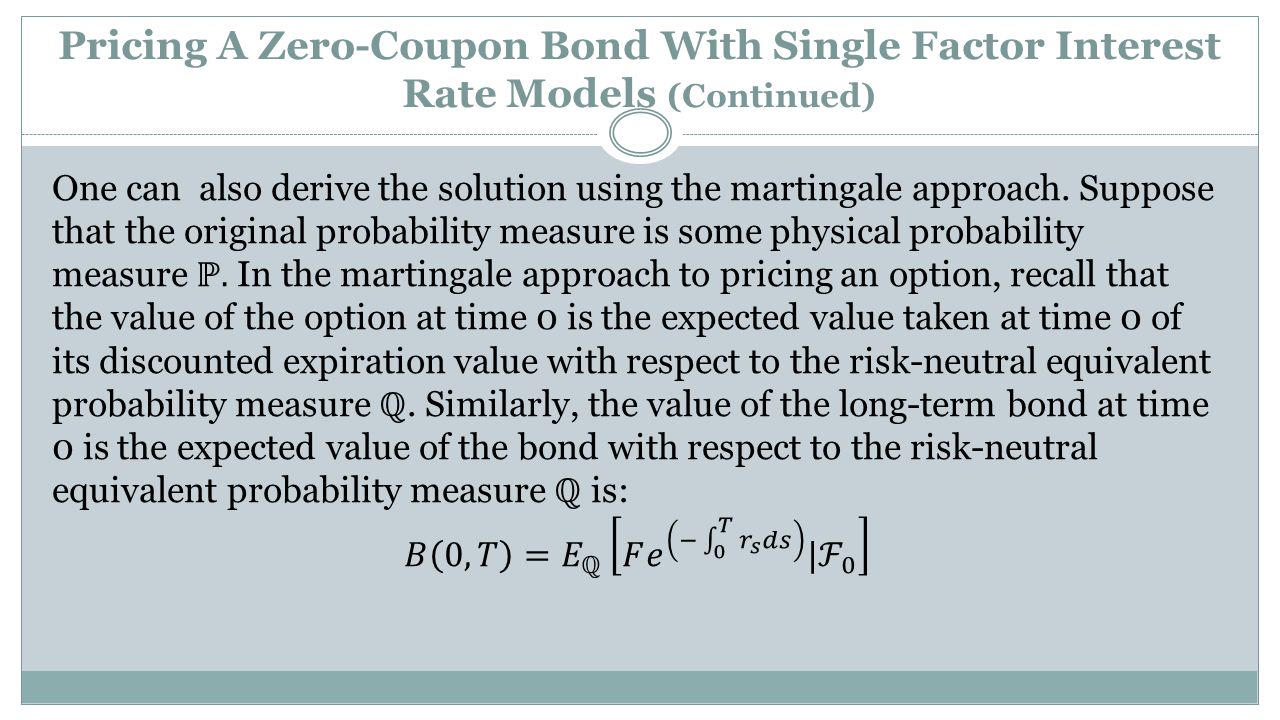

Pricing A Zero-Coupon Bond With Single Factor Interest Rate Models (Continued)

")

21

The Bond Pricing Formula For The Vasicek Model

22

The Bond Pricing Formula For The Vasicek Model (Continued)

")

23

The Yield Curve

24

Illustration of Pricing a Bond Using the Vasicek Model

25

Illustration of Pricing a Bond Using the Vasicek Model (Continued)

")

26

The Problem with Vasicek Models The Vasicek yield curve model has a number of desirable characteristics. The model captures the empirical tendency for interest rates to revert towards some sort of mean rate. The model is driven off short term interest rates, much as actual interest rates might be impacted by the Federal Funds rate, the "overnight" bank-to-bank controlled by the central bank (Fed). However, there are a number of problems with the Vasicek model in characterizing the behavior of the yield curve: 1.Empirical tests reveal that the Vasicek model does not characterize observed interest rate structures well.

. However, there are a number of problems with the Vasicek model in characterizing the behavior of the yield curve: 1.Empirical tests reveal that the Vasicek model does not characterize observed interest rate structures well..")

27

The Problem with Vasicek Models (Continued) 2.The Vasicek model assumes only a single underlying risk factor when, in fact, there is significant evidence that there may well be multiple factors. For example, sometimes the yield curve can "twist;" that is, long- and short-term rates can move in opposite directions. Multiple risk factors can often explain such "twisting." 3.The Vasicek model allows for the possibility of negative interest rates, even for negative real interest rates, a phenomenon that we should expect to observe rarely, if at all.

28

The Problem with Vasicek Models (Continued) Why work with an interest rate model that presents all of these difficulties? As with most other financial models, we simply balance realism and ease of model building. The Vasicek model does capture some of the characteristics of a reasonable interest rate process and it is rather easy to work with, particularly in terms of parameter calibration. In addition, it is useful and sometimes very straightforward to adapt this framework into more realistic alternative depictions of interest rate processes.

29

Alternative Interest Rate Processes The Merton Model The Cox, Ingersoll and Ross (CIR) Process

Process")

30

The Merton Model

31

The Merton Model (Continued)

")

32

Note : Here that a shift in the short-term rate r 0 will result in a parallel shift in the yield curve; that is, the shift in r 0,T will be the same for all T. Such a parallel shift is inconsistent with the empirical observation that short- term rates are more volatile than are long-term rates. Note also that the yield curve can never be monotonically increasing; it is either humped (when > r ) or downward sloping. However, often when it is humped, the upward sloping portion of the hump can extend beyond the period being analyzed. Thus, the yield curve can be upward sloping over the "relevant" period.

or downward sloping. However, often when it is humped, the upward sloping portion of the hump can extend beyond the period being analyzed. Thus, the yield curve can be upward sloping over the relevant period..")

33

The Cox, Ingersoll and Ross (CIR) Process

Process")

34

The Cox, Ingersoll and Ross (CIR) Process (Continued)

Process (Continued)")

35

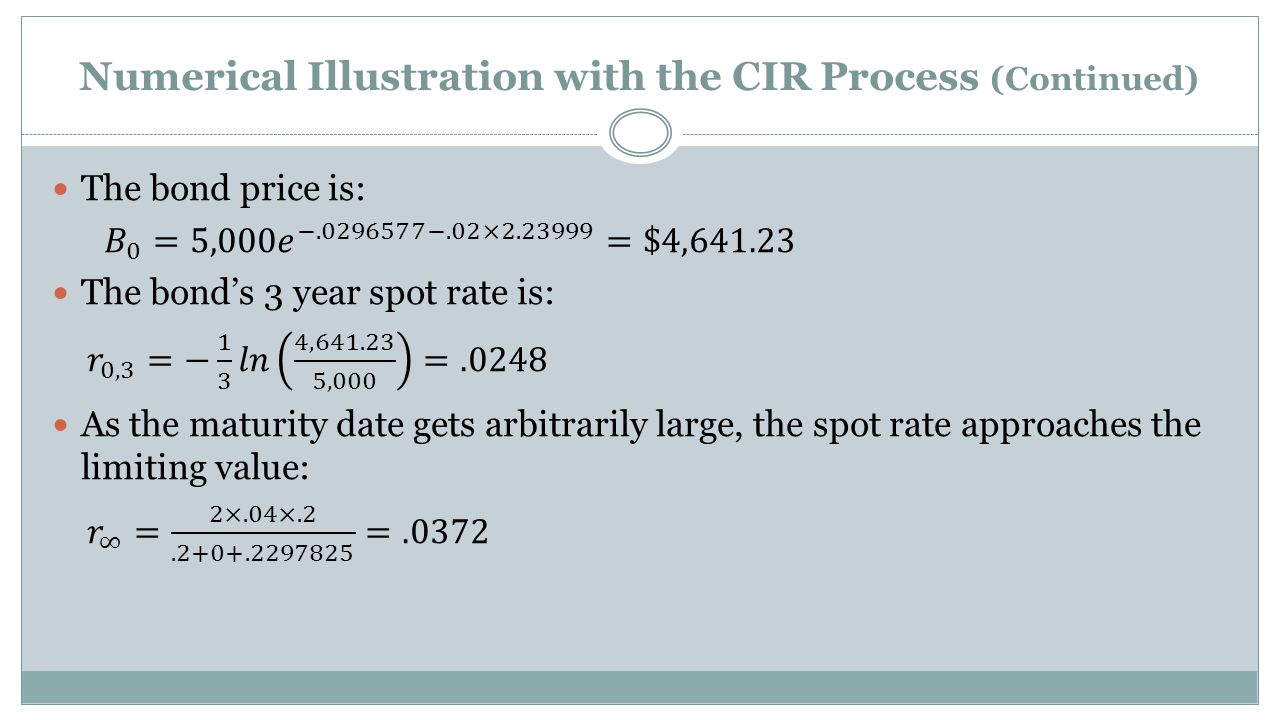

Numerical Illustration with the CIR Process Suppose short term interest rates follow a CIR Process with pullback factor of.2, a long term mean interest rate of.04, an instantaneous standard deviation of.08, a current short rate of.02, and a risk premium of 0. What stochastic differential equation governs the short term interest rate? Find the price of a 3 year zero coupon bond with a face value of $5,000. Find its 3 year spot rate. What rate does the spot rate approach as the maturity date gets arbitrarily large?

36

Numerical Illustration with the CIR Process (Continued)

")

Similar presentations

to Asset Market (MP):>")

>")