Download presentation

Presentation is loading. Please wait.

2

Mark H. Crocker, CPA, CGMA Executive Director, Tennessee State Board of Accountancy Don Mills, CPA, CFE, CFF TNSBA Investigator Ray Butler, Jr., CPA TNSBA Investigator

3

THIS PRESENTATION IS BEING BROUGHT TO YOU BY THE MEMBERS OF THE TENNESSEE STATE BOARD OF ACCOUNTANCY…

4

William Blaufuss, CPA, Chairman. – Nashville William Blaufuss, CPA, Chairman. – Nashville Don Royston, CPA, Vice- Chair – Kingsport Don Royston, CPA, Vice- Chair – Kingsport Henry Hoss, CPA, Sec. – Chattanooga Henry Hoss, CPA, Sec. – Chattanooga Vic Alexander, CPA – Nashville Vic Alexander, CPA – Nashville Gay Moon, CPA – Nashville Gay Moon, CPA – Nashville Jennifer Brundige, JD – Nashville, Public Member Jennifer Brundige, JD – Nashville, Public Member Stephen Eldridge, CPA – Jackson Stephen Eldridge, CPA – Jackson John Roberts, Attorney-at- Law – Nashville, Attorney Member John Roberts, Attorney-at- Law – Nashville, Attorney Member Charlene Spiceland, CPA – Memphis Charlene Spiceland, CPA – Memphis Casey Stuart, CPA– Chattanooga Casey Stuart, CPA– Chattanooga Trey Watkins, CPA– Memphis Trey Watkins, CPA– Memphis

5

Quiz Question New Members of the Accountancy Board are selected by: a.The Governor b.The TNSBA c.Current members of the Board d.A secret committee that meets in Nashville e.A random drawing that includes all active Licensees

6

IN THE TNSBA COMPLAINT SYSTEM, THERE ARE TWO SEPARATE YET DISTINCT ENTITIES: THOSE INDIVIDUALS WHO ARE LICENSED BY THE STATE, AND THOSE WHO ARE NOT. THESE ARE THEIR STORIES…

8

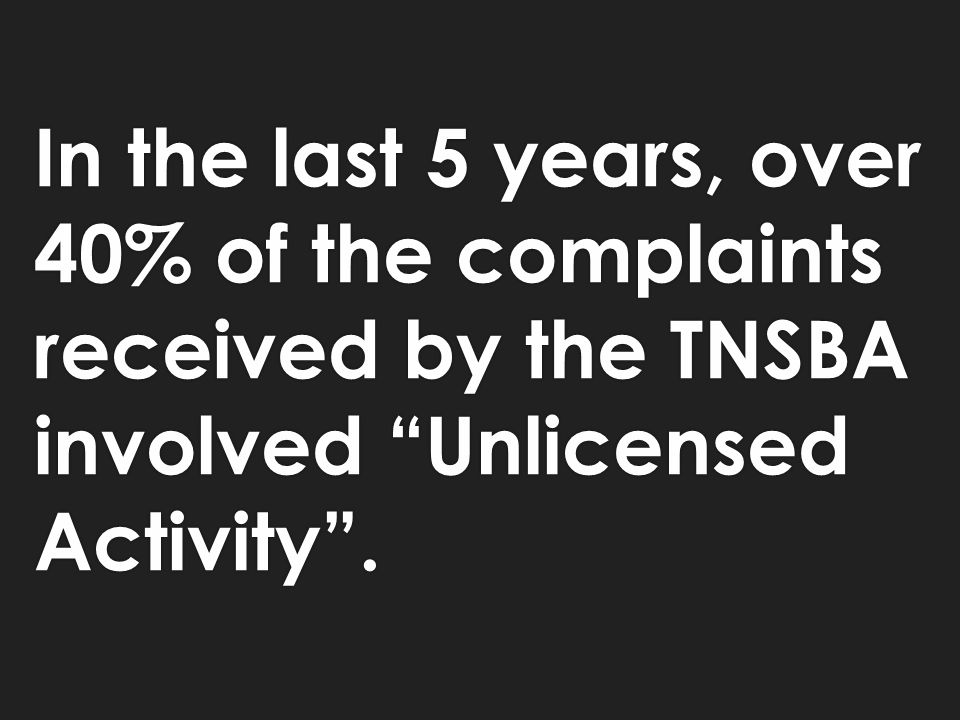

In the last 5 years, over 40% of the complaints received by the TNSBA involved “Unlicensed Activity”.

9

Such as this case study….

10

Unlicensed Activities Case Study: An anonymous individual submitted the following “opinion” and asked if we could tell if it was a real audit; noting that the company used the word “audit” 5 times in their letter. What do you think?

11

ABC Accounting & Tax Services, Inc. We have audited XYZ’s statement of financial position for the calendar year 2006, 2008, and 2010. These financial statements are the responsibility of XYZ management. Our responsibility is to express an opinion on these financial statements based on our audit.

12

An audit includes examining on a test basis, evidence supporting the amounts reported on the financial statements. We have audited the following items in your financial statements: Revenues for all three years Expenses for all three years Collections for all three years 1099 Filings Tax return filing

13

In our opinion, the financial statements are referred to above to be fairly presented with except of the items listed below: 2010- A $1.00 variance between Revenue calculated and what was deposited. Tax return was prepared properly. 2008- Tax filing and income statement includes $2000 Transfer from operating account to Certified Deposit as being an expense when this is just a balance sheet transfer. Transfer from one bank account to another (or CD for this transaction) is not an expense; entity still holds control over this money. 2006- Revenue for this year could not be tested due to a lack of supporting documents; did not have bank statements to verify that all revenue was deposited. We understand this is due to change in property manager. Tax return was prepared properly.

is not an expense; entity still holds control over this money Revenue for this year could not be tested due to a lack of supporting documents; did not have bank statements to verify that all revenue was deposited. We understand this is due to change in property manager. Tax return was prepared properly..")

14

Signed: ABC Accounting & Tax Services, Inc. Disclosure: ABC Accounting & Tax Services and its associates are not certified public accountant. Owner does have a master’s degree with concentration in accounting. This information was disclosed to the company’s president and approved us for performing this audit.

15

Believe it or not… There is a provision in the Law & Rules that provides disclaimer language for non-licensees in connection with financial statements that will not be a violation.

16

Rule 0020-4-.06 Safe Harbor Language “ We have prepared the accompanying (financial statements) of (name of entity) as of (time period) for the (period) then ended. This presentation is limited to preparing, in the form of financial statements, information that is the representation of management.” “We have not audited, reviewed or compiled, under professional standards prescribed for such services, the accompanying financial statements and accordingly do not express an opinion or any other form of assurance on them. We are not licensed by this state, as a certified public accountant or accounting firm, to provide those types of services.”

17

Quiz Question Which of the following activities are prohibited unless the individual is a licensed CPA in the state of Tennessee? a.Using the designation “CPA” b.Using the word “accountant” or “accounting” c.Issuance of a report on financial statements of any person, organization or governmental unit. d.Use of any language in any statement relating to the financial affairs of a person or entity that is conventionally used by licensees. e.All of the above.

18

The Repeat Offender 1997- paid a $500 civil penalty for issuing a review report on financial statements. 2004- Two complaints for advertising his firm under “Accountants- Certified Public”. 2008- paid a $5,000 civil penalty with regard to two complaints for holding out as a CPA and use of the word “Accounting” in his firm name 2010-Fined $7,500 for signing a Federal tax return as a CPA.

19

2012- During the investigation of two new complaints against the individual, special agents from the Tennessee Department of Revenue asked that the complaints be suspended while they conducted an investigation. It appears that our repeat offender had discovered a new way to prepare his clients’ sales tax returns.

20

In October of 2012, The Board dismissed both complaints against the individual in favor of criminal charges brought by the State, consisting of over 3 dozen felony counts. Most of the felony counts were for “obstructing lawful tax collection”; however, one felony count of impersonation of a professional was added at the Board’s request.

21

Quiz Question A Licensee must, upon request by a client or former client, furnish which of the following records? a.Any reports or other documents belonging to or obtained from the client. b.Any accounting or other documents belonging to or obtained from the client. c.Any working papers that would ordinarily constitute part of the client’s books and records, such as general ledgers, fixed asset and depreciation schedules. d.a. and b., but not c. e.All of the above.

22

HOW MANY CPAS IN TENNESSEE TODAY? Active 10,459 Inactive 4,188 Closed 2,811 Probation/Suspended 2 Revoked 54 Retired 1,008 Expired (Grace) 142 Expired 2,281 Deceased 2,262 Other 251 Total Licenses 24,056

142 Expired 2,281 Deceased 2,262 Other 251 Total Licenses 24,056.")

23

Top 5 Problems with Licensees: 1.License renewal 2.Firm permit renewal 3.Continuing Professional Education 4.Peer Review 5.Professional Privilege Tax

24

1. License renewal - Good Standing StatusPay License Renewal Fee Complete CPEPay Professional Privilege Tax ActiveYes InactiveYesNo Retired (55 yrs+) YesNo Retired Over 65 No ClosedNo – But Must Return Wall Certificate No

YesNo Retired Over 65 No ClosedNo – But Must Return Wall Certificate No.")

25

1. License Renewal – Not so Good Expired-Grace Expired Probation Suspended Revoked Expired-Grace Expired Probation Suspended Revoked

26

Quiz Question The only difference between a retired license and an expired license is that no fees are required to maintain an expired license. a.True b.False.

27

2. Firm Permit Renewal – Annually Update and Confirm: Physical Information – Where is your office? Ownership- Must be 51% owned by CPAs Experience of Resident Manager Peer Review Selection or Exempt Request – Sign up with TSCPA upon application for firm permit CPA owners and CPA employees

28

Quiz Question A Licensee is not required to obtain a firm permit in which of the following circumstances? a.Licensee is a sole proprietor and does not perform attest services. b.Practice is limited to preparation of tax returns. c.Practice is limited to personal financial planning. d.Licensee advertises practice as limited to “consulting”. e.All of the above are exceptions to the firm permit requirement.

29

3. Continuing Professional Education All Licensees Holding Active License 80 Approved Hours every two years – add 8 penalty hours if you don’t 40 Technical Hours (A&A, Taxes, Ethics & Management Advisory) 2 Hours State Specific Ethics – Such as this course! Minimum of 20 Hours Each Year – add 8 penalty hours if you don’t Special Areas: Attest Services – 20 Hours A&A Expert Witness Services – 20 Hours in Area

2 Hours State Specific Ethics – Such as this course. Minimum of 20 Hours Each Year – add 8 penalty hours if you don’t Special Areas: Attest Services – 20 Hours A&A Expert Witness Services – 20 Hours in Area.")

30

3. Continuing Professional Education Helpful Hints: If you are short on technical hours but still have completed 80, you can make them up without penalty. 40 Technical Hours (A&A, Taxes, Ethics & Management Advisory) You may carry over up to 24 hours from the previous reporting period, but they become reclassified as “other”. And – They cannot be used to meet the annual 20 hour requirement. If you miss your 20 hour requirement in one year but have a total of 88 hours for the reporting period – the extra 8 hours can be reported as your “penalty” hours

You may carry over up to 24 hours from the previous reporting period, but they become reclassified as other . And – They cannot be used to meet the annual 20 hour requirement. If you miss your 20 hour requirement in one year but have a total of 88 hours for the reporting period – the extra 8 hours can be reported as your penalty hours.")

31

4. Peer Review Requirements Tennessee requires peer review for any firm that performs the attest function. Tennessee defines the attest function to include compilations. Only engagements conducted under SSARS #8 may be excluded from the requirement. (Be careful, this is a high risk area)

.")

32

5. Professional Privilege Tax Assessed every June by the Tennessee Department of Revenue. Every Licensee with an active license is subject to the tax – regardless of where you are practicing.

33

Quiz Question After a Formal Hearing, the Board may revoke, suspend, reprimand, censure or limit the scope of practice of a licensee for which of the following reasons: a.Fraud in obtaining a license b.Disciplinary action taken by another state c.Revocation of the right to practice before any state or federal agency d.Dishonesty, fraud or gross negligence in the performance of services e.Violation of the rules of professional conduct f.All of the above

34

How about a case study to illustrate the idea that- No good deed goes unpunished.

35

THE COMPLAINT The Complainant stated that the Licensee had been hired to serve as a Power of Attorney; to pay bills; and to serve as the Executor of her elderly mother’s will. Specific allegations were as follows: The Licensee told the 93 year old client she had dementia. The Licensee tried to force the client into a living situation against her will. The Licensee filed a lawsuit against the client that cost her $10,000 Approximately $1,000 of the client’s money was spent in “unexplainable” ways.

36

THE RESPONSE The Licensee stated that the client’s physician told family members that she had mild dementia and needed help with her finances. The Licensee admitted meeting with the client and her financial advisor because the client was being forced to sell her home (by the Complainant). The “lawsuit” was actually a filing by the Licensee of a petition for conservatorship in order to protect the client’s assets. All issues were resolved by settlement of the family members and the petition was dropped.

. The lawsuit was actually a filing by the Licensee of a petition for conservatorship in order to protect the client’s assets. All issues were resolved by settlement of the family members and the petition was dropped..")

37

THE STORY CONTINUES A review of the Licensee’s workpaper files showed that the “unexplainable” expenses consisted of blank checks that had been given to the client and signed for by the client. The Licensee did not have check signing privileges. Two of the Complainant’s siblings provided affidavits stating that they had full confidence in the Licensee; however, they did assert that the Complainant was responsible for over $500,000 in unaccounted for funds missing from their mother’s investment accounts.

38

THE RESOLUTION Throughout the investigation, the Complainant was unable to provide any documentation regarding her allegations against the Licensee. Although the Board dismissed the complaint, the client passed away during the investigation and the Licensee is now working as the Executor of the client’s estate; having been told by the Complainant that no fees will ever be paid for the work

39

Quiz Question Which of the following actions are available to the Board concerning complaints? a.Dismissal. b.Letters of Caution, Warning or Instruction. c.Consent Order. d.Informal Hearing. e.Formal Hearing. f.All of the above.

40

Whoever said, “There is nothing new under the sun,” was definitely not an accountant

41

New Rules for the Tennessee CPA Rule 0020-01-.04(1) Fees Amended to reduce the CPA license renewal fee to one hundred ten dollars ($110.00) biennially Rule 0020-01-.04(1) Fees Amended to reduce the CPA license renewal fee to one hundred ten dollars ($110.00) biennially

Fees Amended to reduce the CPA license renewal fee to one hundred ten dollars ($110.00) biennially Rule (1) Fees Amended to reduce the CPA license renewal fee to one hundred ten dollars ($110.00) biennially")

42

Rule 0020-01-.05 Applications Amended paragraph (3) to read as follows: A candidate who fails to appear for the examination shall forfeit all fees charged for both the application and the examination. All applications for initial licensure shall expire one (1) year from the date of the application for initial licensure. Amended paragraph (3) to read as follows: A candidate who fails to appear for the examination shall forfeit all fees charged for both the application and the examination. All applications for initial licensure shall expire one (1) year from the date of the application for initial licensure.

year from the date of the application for initial licensure. Amended paragraph (3) to read as follows: A candidate who fails to appear for the examination shall forfeit all fees charged for both the application and the examination. All applications for initial licensure shall expire one (1) year from the date of the application for initial licensure..")

43

Rule 0020-01-.06 Applications Amended by adding a new paragraph (11) to read as follows: All CPA Exam scores shall expire ten (10) years after the first passing score is earned. However, upon written request by the applicant, the Board may, in its sole discretion, grant an extension of the score expiration date for good cause shown. Amended by adding a new paragraph (11) to read as follows: All CPA Exam scores shall expire ten (10) years after the first passing score is earned. However, upon written request by the applicant, the Board may, in its sole discretion, grant an extension of the score expiration date for good cause shown.

to read as follows: All CPA Exam scores shall expire ten (10) years after the first passing score is earned. However, upon written request by the applicant, the Board may, in its sole discretion, grant an extension of the score expiration date for good cause shown..")

44

Rule 0020-04-.03 Grounds for Disciplinary Action Amended by adding a new paragraph (3) to read as follows: The Board has no jurisdiction over fee disputes between a licensee and a client. The Board shall not seek to impose discipline against a licensee solely on the basis of a dispute between the licensee and the client regarding payment of fees by the client for professional services rendered by the licensee. Amended by adding a new paragraph (3) to read as follows: The Board has no jurisdiction over fee disputes between a licensee and a client. The Board shall not seek to impose discipline against a licensee solely on the basis of a dispute between the licensee and the client regarding payment of fees by the client for professional services rendered by the licensee.

to read as follows: The Board has no jurisdiction over fee disputes between a licensee and a client. The Board shall not seek to impose discipline against a licensee solely on the basis of a dispute between the licensee and the client regarding payment of fees by the client for professional services rendered by the licensee..")

45

Rule 0020-05-.03(3) Basic Requirements Amended by adding new subparagraphs to read as follows: (a)For purposes of disciplinary action, the Board shall retain jurisdiction over all certificate holders whose license is in inactive status. (b)Certificate holders who are granted inactive status by the Board shall be required to place the word “inactive” adjacent to their CPA or PA designation when using such designation for any lawful purpose, including, but not limited to use of such designation on any business card, letterhead, resume or biography. Amended by adding new subparagraphs to read as follows: (a)For purposes of disciplinary action, the Board shall retain jurisdiction over all certificate holders whose license is in inactive status. (b)Certificate holders who are granted inactive status by the Board shall be required to place the word “inactive” adjacent to their CPA or PA designation when using such designation for any lawful purpose, including, but not limited to use of such designation on any business card, letterhead, resume or biography.

Certificate holders who are granted inactive status by the Board shall be required to place the word inactive adjacent to their CPA or PA designation when using such designation for any lawful purpose, including, but not limited to use of such designation on any business card, letterhead, resume or biography. Amended by adding new subparagraphs to read as follows: (a)For purposes of disciplinary action, the Board shall retain jurisdiction over all certificate holders whose license is in inactive status. (b)Certificate holders who are granted inactive status by the Board shall be required to place the word inactive adjacent to their CPA or PA designation when using such designation for any lawful purpose, including, but not limited to use of such designation on any business card, letterhead, resume or biography..")

46

Rule 0020-05-.03(3) Basic Requirements (continued) c)A certificate holder who has been granted inactive status may not for compensation perform or offer to perform for the public, including the providing of accounting services from a licensed accounting firm, any of the following services: any accounting or auditing services which involves the issuance of reports on financial statements (including opinions, reviews, compilations, or attest engagements), any consulting engagement which would constitute the attest function, or furnishing advice on tax matters.

Basic Requirements (continued) c)A certificate holder who has been granted inactive status may not for compensation perform or offer to perform for the public, including the providing of accounting services from a licensed accounting firm, any of the following services: any accounting or auditing services which involves the issuance of reports on financial statements (including opinions, reviews, compilations, or attest engagements), any consulting engagement which would constitute the attest function, or furnishing advice on tax matters.")

47

Rule 0020-05-.03(3) Basic Requirements (continued) d)A certificate holder who has been granted inactive status may perform the services set forth in c) above if: the services are provided without compensation to the certificate holder, if the services are performed solely for the certificate holder’s employer and such employer is not a licensed accounting firm, or if the certificate holder does not use the CPA or PA designation in association with his or her name while providing such lawful services.

Basic Requirements (continued) d)A certificate holder who has been granted inactive status may perform the services set forth in c) above if: the services are provided without compensation to the certificate holder, if the services are performed solely for the certificate holder’s employer and such employer is not a licensed accounting firm, or if the certificate holder does not use the CPA or PA designation in association with his or her name while providing such lawful services.")

48

Rule 0020-05-.03(3) Basic Requirements (continued) e)A certificate holder who is 65 years old or older and possesses a certificate in inactive status shall not be required to pay the biennial license renewal fee required for licensees as set forth in these rules.

Basic Requirements (continued) e)A certificate holder who is 65 years old or older and possesses a certificate in inactive status shall not be required to pay the biennial license renewal fee required for licensees as set forth in these rules.")

49

Rule 0020-05-.03(3) Basic Requirements (continued) f)Certificate holders who are granted inactive status must complete eighty (80) hours of CPE in the areas of accounting, accounting ethics, attest, taxation, or management advisory services during the twenty-four (24) month period preceding the date of their request for reactivation of their license. The CPE hours required to reactivate a license may also be used as credit toward the renewal requirement so long as those hours are completed within the two (2) year window prior to the licensee’s next December 31 renewal date.

year window prior to the licensee’s next December 31 renewal date..")

50

Rule 0020-05-.03 Basic Requirements Amend paragraph (6) to read as follows: An applicant for renewal whose license has expired as set forth in Rule 0020-1-.08(7) shall complete no less than eighty (80) hours of CPE in the areas of accounting, accounting ethics, attest, taxation, or management advisory services during the six (6) month period preceding the date of reapplication. The CPE hours required to reinstate an expired license are considered penalty hours and may not be used to offset the CPE hours required for the renewal of a license. Amend paragraph (6) to read as follows: An applicant for renewal whose license has expired as set forth in Rule 0020-1-.08(7) shall complete no less than eighty (80) hours of CPE in the areas of accounting, accounting ethics, attest, taxation, or management advisory services during the six (6) month period preceding the date of reapplication. The CPE hours required to reinstate an expired license are considered penalty hours and may not be used to offset the CPE hours required for the renewal of a license.

to read as follows: An applicant for renewal whose license has expired as set forth in Rule (7) shall complete no less than eighty (80) hours of CPE in the areas of accounting, accounting ethics, attest, taxation, or management advisory services during the six (6) month period preceding the date of reapplication. The CPE hours required to reinstate an expired license are considered penalty hours and may not be used to offset the CPE hours required for the renewal of a license..")

51

Quiz Question A Consent Order from the Board may contain which of the following: a.Civil penalty b.Additional CPE or peer review c.A probationary period for the Licensee d.Revocation of the Respondent’s license. e.All of the above. f.Every action except revocation.

52

Before we quit, let’s do one more case study for the auditors in the crowd

54

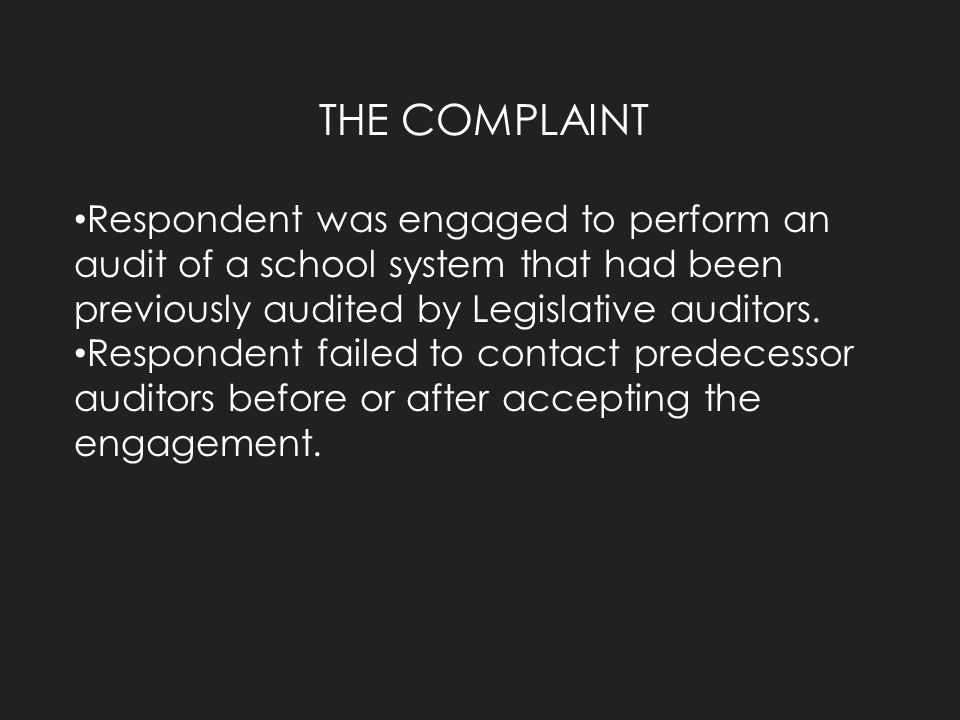

THE COMPLAINT Respondent was engaged to perform an audit of a school system that had been previously audited by Legislative auditors. Respondent failed to contact predecessor auditors before or after accepting the engagement.

55

THE STORY An initial review of the Licensee’s working papers raised questions as to whether or not they met auditing standards. An Investigator from another Board was engaged to perform a working paper review and report the results to the Board.

56

AUDIT DEFICIENCIES The Auditor: Failed to obtain management representations, but still gave an unqualified opinion. Incorrectly asserted that he was not a successor auditor. Identified supplemental information but did not provide an opinion as to whether or not that information was fairly stated. Did not include any language in the engagement letter stating the responsibilities of management or the auditor.

57

AUDIT DEFICIENCIES The Working Papers: Did not contain audit programs related to account balances, transaction classes, or audit objectives. The audit programs in the working papers were mostly incomplete and not referenced to the working papers. Did not contain a method of sampling used for tests of controls or any indication of the sampling method used for substantive tests. Did not support the conclusions reached by the auditor in 9 audit areas identified as significant during the planning phase of the audit.

58

BEST WORKING PAPER EVER The “Audit Process Checklist Document” stated that the auditor performed preliminary analytical review procedures. And here it is…..

60

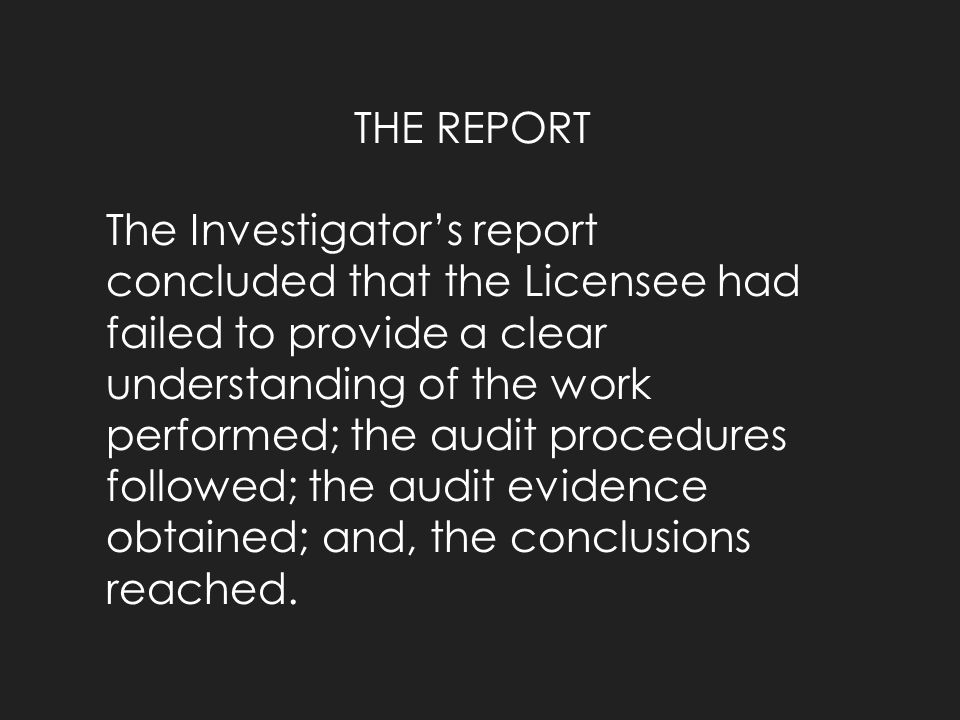

THE REPORT The Investigator’s report concluded that the Licensee had failed to provide a clear understanding of the work performed; the audit procedures followed; the audit evidence obtained; and, the conclusions reached.

61

THE RESOLUTION In a formal hearing, the Board ordered the following: A Civil Penalty of $13,500 plus court and investigative costs. An immediate peer review. A pre-release review of all audits performed by the Licensee.

62

Questions? Contact Information Contact Information Phone: 888-453-6150 or 615-741-2550 Phone: 888-453-6150 or 615-741-2550 Fax: 615-532-8800 Fax: 615-532-8800 Web: http://tn.gov/commerce/boards/tnsba Web: http://tn.gov/commerce/boards/tnsba http://tn.gov/commerce/boards/tnsba E-Mail: TNSBA web page has direct contact information for all Board Members and Staff Members E-Mail: TNSBA web page has direct contact information for all Board Members and Staff Members

63

WHO DO I ASK FOR? TNSBA Administrative Support Staff Executive Director – Mark H. Crocker, CPA, CGMA Executive Director – Mark H. Crocker, CPA, CGMA Investigator – Don Mills, CPA, CFE Investigator – Don Mills, CPA, CFE Investigator – Ray Butler, CPA Investigator – Ray Butler, CPA Advisory Attorney – Chris Whittaker, Esq. Advisory Attorney – Chris Whittaker, Esq. Education Coordinator – Denise Hickerson Education Coordinator – Denise Hickerson Complaint Coordinator – Josh Canan Complaint Coordinator – Josh Canan Licensing Coordinator – Brenda Demastus Licensing Coordinator – Brenda Demastus Firm Permit Coordinator – Karen Condon Firm Permit Coordinator – Karen Condon Administrative Assistant – Sandy Cooper Administrative Assistant – Sandy Cooper

64

FUNCTION OF ADMINISTRATIVE OFFICE Initial Licensing (testing and reciprocity) Initial Licensing (testing and reciprocity) Renewing Licenses Renewing Licenses Updating Files Updating Files Assisting Licensees & Public Assisting Licensees & Public Investigation of Complaints Investigation of Complaints Education Education

Initial Licensing (testing and reciprocity) Renewing Licenses Renewing Licenses Updating Files Updating Files Assisting Licensees & Public Assisting Licensees & Public Investigation of Complaints Investigation of Complaints Education Education")

65

Final Quiz Question On December 31 st, you realize that you do not have enough CPE. Which is your best option regarding your renewal? a.Continue to practice on a delinquent license and pray that no one notices. b.Go ahead and renew. Answer “no” to the CPE question, then finish your hours. c.Close your license and get a job with H & R Block. d.Request an extension of time because your in-laws came to visit at Thanksgiving and are still in your house. e.Move to another state.

Similar presentations

:>")

Summary of Key Changes Effective September 16, 2010.>")

Training.>")

The audit is to be performed by a person or persons have adequate technical training and proficiency as an auditor. 2)In all matters.>")