Download presentation

Presentation is loading. Please wait.

1

Bank Performance 20

2

Performance Evaluation of Banks

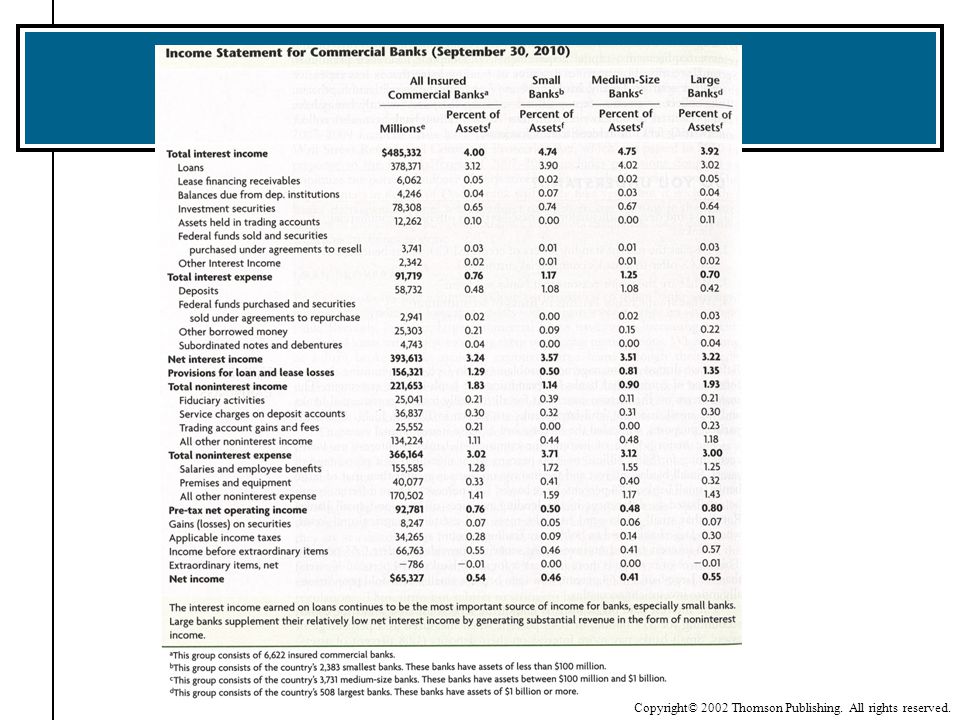

OUTLINE OF INCOME STATEMENT Interest Income (from loans & investments) Interest Expense = Net Interest Income (spread or margin) + Non-interest Income Non-interest Expense Loan Losses (Bad Debt Expense) +/- Security Gains/Losses Income Tax = Net Income

Interest Expense. = Net Interest Income (spread or margin) + Non-interest Income. Non-interest Expense. Loan Losses (Bad Debt Expense) +/- Security Gains/Losses. Income Tax. = Net Income.")

3

Exhibit 20.2

4

Ch 20, Problem (10e, p. 529; 11e, p.563) Managing in Financial Markets

INCOME STATEMENT FOR HAWAII BANK % of Avg Assets Interest Income (from loans & invest.) ?% Interest Expense ?% = Net Interest Income (spread or margin) ?% + Non-interest Income ?% Non-interest Expense ?% Loan Losses (Bad Debt Expense) ?% = Net Income before Tax ?% Income Tax ?% = Net Income ?% ROA = (Net Inc / Avg Assets) = ?% ROE = (Net Inc / Equity) ?% / ?% = ?% or ROE = ROA * (Avg Assets/Equity) = ?%

% Interest Expense % = Net Interest Income (spread or margin) % + Non-interest Income % Non-interest Expense % Loan Losses (Bad Debt Expense) % = Net Income before Tax % Income Tax % = Net Income % ROA = (Net Inc / Avg Assets) = % ROE = (Net Inc / Equity) % / % = % or ROE = ROA * (Avg Assets/Equity) = %")

5

Performance Evaluation of Banks

Interest income and expenses Gross interest income = interest income generated from all interest-bearing assets Affected by market rates Impacted by composition of bank assets (loans provide higher rate than liquid investments) Gross interest expenses = interest paid on deposits and borrowed funds Impacted by the composition of bank liabilities (demand accounts are less costly than time deposits) Net interest income = gross interest income – interest expenses

Gross interest expenses = interest paid on deposits and borrowed funds. Impacted by the composition of bank liabilities (demand accounts are less costly than time deposits) Net interest income = gross interest income – interest expenses.")

7

Gross Interest Income/Expense

9

Performance Evaluation of Banks

Noninterest income and expenses Noninterest income results from fees charged on services Lockboxes, overdraft fees, ATM fees, banker’s acceptances fees, cashier check fees, foreign exchange transactions, investment banking and other advisory fees Loan loss provision is a reserve account established in anticipation of future losses Noninterest expenses include salaries, office equipment Securities gains and losses

12

Performance Evaluation of Banks

Return on assets (ROA) Net income as a percent of total assets Net Income / Total Assets = ROA Usually lower for large banks (money center banks) because they obtain funds from large deposits (CDs) that pay higher interest rates. Small banks usually get funds from demand deposits (zero interest) and small savings accounts (low interest).

Net income as a percent of total assets Net Income / Total Assets = ROA. Usually lower for large banks (money center banks) because they obtain funds from large deposits (CDs) that pay higher interest rates. Small banks usually get funds from demand deposits (zero interest) and small savings accounts (low interest).")

13

How to Evaluate a Bank’s Performance

Examination of Return on Assets (ROA) Will usually reveal poor performance, but will not indicate the source of the problem Possible reasons for a low ROA: Excessive interest expenses (e.g too many CDs) Low interest received on loans and securities Too conservative with loans—excessive short-term securities Insufficient noninterest income Service fees too low (should raise NSF fees, etc.) High provision for loans losses

Will usually reveal poor performance, but will not indicate the source of the problem. Possible reasons for a low ROA: Excessive interest expenses (e.g too many CDs) Low interest received on loans and securities. Too conservative with loans—excessive short-term securities. Insufficient noninterest income. Service fees too low (should raise NSF fees, etc.) High provision for loans losses.")

14

Performance Evaluation of Banks

Return on equity (ROE) The return on capital invested Net Income / Capital = ROE ROE = ROA x leverage multiplier (inverse of capital ratio) ROE for large banks has been lower than for small banks for the same reasons that their ROA has been lower

The return on capital invested Net Income / Capital = ROE. ROE = ROA x leverage multiplier (inverse of capital ratio) ROE for large banks has been lower than for small banks for the same reasons that their ROA has been lower.")

16

Exhibit 20.11 Breakdown of Performance Measures

17

Influence of Bank Policies and Other Factors on a Bank’s Income Statement

18

Zager Bank Example Example of Zager Bank Application:

Zager bank is a medium size bank Aggressive management style can be viewed as risky due to limited collateral and cash flow situation. The bank charges high interest rates on loans because the borrowers do not have alternative lenders. Strategy was successful during strong economic conditions. When economy weakened in 2008, borrowers had trouble repaying their loans.

19

Zager Bank Example

20

Risk Evaluation of Banks

No consensus measurement exists that would allow for comparison of various types of risk among all banks Some analysts measure a firm’s risk by its beta, which measures the sensitivity of stock returns to the market as a whole, but Beta ignores firm-specific characteristics Examples: look up BofA (BAC) or Banner Bank (BANR).

or Banner Bank (BANR).")

21

Beta measures non-diversifiable risk

22

Betas During Financial Crisis

Feb-08 / Today 0.19 / ? (BAC - Bank of America) 1.14 / ? (C - Citibank) 0.5 / ? (JPM - JP Morgan Chase) 0.04 / ? (WFC - Wells Fargo) 1.17 / ? (BANR - Banner Bank)

1.14 / (C - Citibank) 0.5 / (JPM - JP Morgan Chase) 0.04 / (WFC - Wells Fargo) 1.17 / (BANR - Banner Bank)")

23

History of U.S. Bank Failures

# of banks failed 3 in 2007 30 in 2008 148 in 2009 157 in 2010 92 in in in so far in 2014 See FDIC website for details

24

Bank Failures Historical reasons for bank failure

Fraud from poor internal controls Embezzlement of funds No separation of personnel duties—esp. at small banks High loan default percentage Excessive reliance on a specific industry (such as oil, defense, or agriculture) or a specific geographic location. Recession periods Liquidity crisis Bank runs, panics Loss of confidence of financial markets Increased competition (very tight margins) Under-capitalization / over-leverage (too much debt)

or a specific geographic location. Recession periods. Liquidity crisis. Bank runs, panics. Loss of confidence of financial markets. Increased competition (very tight margins) Under-capitalization / over-leverage (too much debt)")

25

Bank Failures Study by the Office of the Comptroller of the Currency reviewed 162 national banks that have failed since 1979 and found that: 81% did not have a loan policy or did not closely follow their policy 59 % did not use an adequate system to identify problem loans 63% did not adequately monitor key bank officers or departments 57% allowed one individual to make major corporate decisions Since these are all controllable, must conclude major reason is poor management.

Similar presentations