Download presentation

Presentation is loading. Please wait.

1

2009 Volunteer Tax Preparation NJ Division of Taxation www.njtaxation.org

2

Important Contact Information Regional Taxpayer Service Offices Customer Service Center 609/292-6400 Division of Revenue E-File Unit 609/633-1132 www.njtaxation.org

5

New for 2009 Earned Income Tax Credit Increases to 25% New Tax Rates Incomes $400,000 and over Property Tax Deduction NJ Lottery Winnings

6

Important Processing Information Do not use mailing label if it is incorrect Do not staple, clip or otherwise attach pages together Place only 1 return for each envelope

7

Important Processing Information You may not report a loss on Form NJ-1040 Use only blue or black ink Do not use dollar signs or dashes Leave unused lines ‘Blank’

8

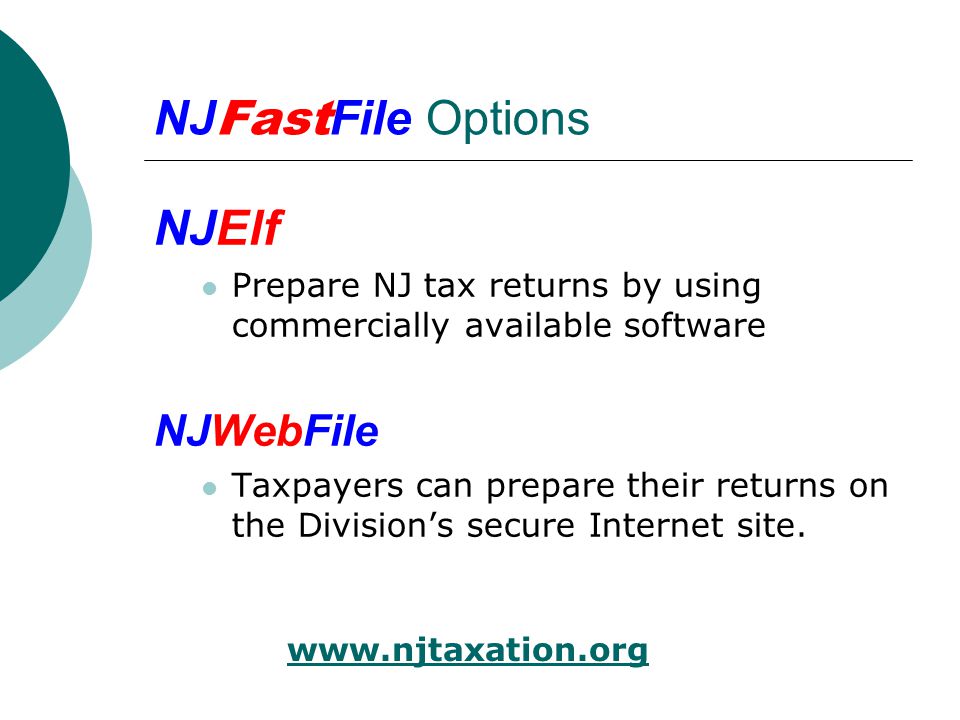

NJ Fast File Options NJElf Prepare NJ tax returns by using commercially available software NJWebFile Taxpayers can prepare their returns on the Division’s secure Internet site. www.njtaxation.org

9

Benefits of E-Filing Minimizes processing errors Faster Refunds Can be directly deposited Allows file now... pay later Payments can be made electronically or via mail

10

Form NJ-1040 Identifying Information Page 1

11

Filing Status (Lines 1 – 5) Same filing status used as for Federal purposes Exception: Civil Union Couples File NJ income tax as Married IRS does not recognize CU’s

Same filing status used as for Federal purposes Exception: Civil Union Couples File NJ income tax as Married IRS does not recognize CU’s")

12

Personal Exemptions (Lines 6 - 8) Line 6 applies to taxpayer, spouse/CU, domestic partner Line 7 for those Age 65 or Older Line 8 for those Blind or Disabled Domestic Partner, Age or disability exemptions must be documented

Line 6 applies to taxpayer, spouse/CU, domestic partner Line 7 for those Age 65 or Older Line 8 for those Blind or Disabled Domestic Partner, Age or disability exemptions must be documented")

13

Dependents (Lines 9 – 11) Line 9 – Dependent children; must be the same as Federal return Line 10 – Other dependents; must be the same as Federal return Line 11 – Enter dependents attending college

Line 9 – Dependent children; must be the same as Federal return Line 10 – Other dependents; must be the same as Federal return Line 11 – Enter dependents attending college")

14

Line 13 – Dependents Info Social Security Numbers must be listed

15

Form NJ-1040 Reportable Income Page 2

16

Tax-Exempt Income Social Security Unemployment Compensation NJ Lottery Winnings Military Pensions

17

Wages (Line 14) Use W-2 Box 16, ‘State Wages’ State wages often differ from Federal wages (Box 1) All W-2s received must be included with the NJ-1040

Use W-2 Box 16, ‘State Wages’ State wages often differ from Federal wages (Box 1) All W-2s received must be included with the NJ-1040")

18

W-2 Sample

19

Line 15a – Taxable Interest Banks, S&Ls Credit Unions, Savings Accounts Checking Accounts Bonds, Notes, Certificates of Deposit Ginnie Maes, Fannie Maes, Freddie Macs Must enclose copy of Fed Schedule B if line 15a is over $1,500

20

Tax-Exempt Interest – Line 15b Obligations of the State of New Jersey and/or any of its political subdivisions Direct Federal Obligations Pub GIT-5, Exempt Obligations Must enclose an itemized schedule if line 15b is over $10,000

21

Line 16 – Dividends Stocks Mutual Funds Insurance Policies Other income reported on Form 1099-DIV (except capital gains)

")

22

Capital Gains (Line 18) All income received from the disposition of property Includes real estate, stocks, etc Reported on NJ Schedule B NJ Follows Federal Adjustments with Capital Gains

All income received from the disposition of property Includes real estate, stocks, etc Reported on NJ Schedule B NJ Follows Federal Adjustments with Capital Gains")

23

Reporting Pension, Annuity, and IRA Income Line 19

24

Retirement Plans ContributoryNon-Contributory fully taxable

25

Contributory Plans Three components: Employee contributions Employer contributions Earnings

26

Three-Year Rule If employee contributions recovered within three years of date of first pension payment Pension income is not reported until contributions are recovered IRS no longer allows three year rule

27

General Rule Percentage is used based on proportionate share of Contributions to Total Value of the Pension This is applied each year to the Pension amount received Use Worksheet A, pg 22, to determine which pension method to use

28

IRA Withdrawals Lump-sum Periodic payments Use Worksheet C, Page 24

29

IRAs Consist of: Contributions (non-taxable) Earnings (taxable) Rollovers

Earnings (taxable) Rollovers")

30

Taxable Pension (Line 19) Line 19 is for the total of: Taxable Pensions (after reduction by Three-year or General Rule) Taxable Annuities Taxable IRAs

Line 19 is for the total of: Taxable Pensions (after reduction by Three-year or General Rule) Taxable Annuities Taxable IRAs")

31

Gambling Winnings (Line 23) Substantiated Gambling losses may be deducted from winnings prior to reporting on Line 23 Certain NJ Lottery Winnings must also be included on Line 23

Substantiated Gambling losses may be deducted from winnings prior to reporting on Line 23 Certain NJ Lottery Winnings must also be included on Line 23")

32

New for ‘09 - NJ Lottery Winnings Prizes Exceeding $10,000 Taxable Subject to 3% Withholdings $10,000 or below Remain Non-Taxable

33

Record Keeping - Losses Substantiated through: Daily log Journal Canceled check Losing race track pari-mutuel tickets Letters from casino which rate gambling activity

34

Alimony Received (Line 24) Use to report Alimony and Separate maintenance payments received Child Support is not reported anywhere on Form NJ-1040

Use to report Alimony and Separate maintenance payments received Child Support is not reported anywhere on Form NJ-1040")

35

Other Income (Line 25) Prizes and Awards Income in Respect of a Decedent Income from Estates and Trusts Scholarships/Fellowships Jury duty pay Poll worker pay

Prizes and Awards Income in Respect of a Decedent Income from Estates and Trusts Scholarships/Fellowships Jury duty pay Poll worker pay")

36

Pension Exclusion (Line 27a) Eligibility: Age 62 or older; or Disabled as defined by Social Security; Gross income of $100,000 or less

Eligibility: Age 62 or older; or Disabled as defined by Social Security; Gross income of $100,000 or less")

37

Pension Exclusion Amounts

38

Retirement Exclusion (Line 27b) Taxpayer may deduct unused Pension Exclusion from Line 27a if: Line 14 ___ Line 17 ___ Line 20 ___ Line 21 ___ Total less than $3,000

Taxpayer may deduct unused Pension Exclusion from Line 27a if: Line 14 ___ Line 17 ___ Line 20 ___ Line 21 ___ Total less than $3,000")

39

Gross Income – Who Must File? $10,000 or less Single Married/CU - Filing Separate $20,000 or less Married/CU Filing Joint Head of Household Qualifying widower

40

Exemptions (Line 29) Use totals from Lines 12a & 12b Line 12a Total __ x $1000 = ____ Line 12b Total __ x $1500 = ____ Total Exemption Amount = ____ See instructions on page 29

Use totals from Lines 12a & 12b Line 12a Total __ x $1000 = ____ Line 12b Total __ x $1500 = ____ Total Exemption Amount = ____ See instructions on page 29")

41

Medical Expenses (Line 30) For medical expenses not reimbursed by insurance Expenses in excess of 2% of line 28 Gross Income reported

For medical expenses not reimbursed by insurance Expenses in excess of 2% of line 28 Gross Income reported")

42

Other Available Deductions Line 31 – Alimony/Separate maintenance paid (court ordered) Line 32 – Qualified Conservation Contribution Line 33 – Health Enterprise Zone Deduction

Line 32 – Qualified Conservation Contribution Line 33 – Health Enterprise Zone Deduction")

43

Property Tax Deduction/Credit Enter total property taxes paid (or 18% rent) on line 36a Residency Status – Line 36b

on line 36a Residency Status – Line 36b")

44

Property Tax Deduction/Credit Use Schedule 1 to determine which is the greater benefit Enter Property Taxes Paid on Line 36c or a flat $50 credit on Line 48 New: Deduction cannot be taken if Gross Income exceeds $250,000

45

Property Tax Deduction/Credit Suspended for $250,000/ovr Unless 65/ovr or Disabled $5,000 Cap Gross Incomes over $150,000 Unless 65/ovr or Disabled Renters are not subject to above restrictions

46

Tax (Line 38) Show NJ Tax amount based on taxable income Tax Tables (Pg 57) Tax Rates (Pg 66)

Show NJ Tax amount based on taxable income Tax Tables (Pg 57) Tax Rates (Pg 66)")

47

Credit for Taxes Paid (Line 40) Used for NJ Residents who have income subject to tax out of the state Schedule A must be completed Note: Income must be reported on the NJ-1040

Used for NJ Residents who have income subject to tax out of the state Schedule A must be completed Note: Income must be reported on the NJ-1040")

48

Form NJ-1040 Calculating Tax and Payments Page 3

49

Line 41 – Line 44 Line 41 - Balance of Tax Line 42 – Sheltered Workshop Tax Credit Line 44 – Use Tax Due See page 39

50

Use Tax Items purchased out of state, for use in New Jersey are subject to a Use Tax Enter 0.00 if no Use Tax is due

51

Total Tax (Line 46) Shows combined: Tax (line 43); Use Tax (line 44); and Estimated Tax Penalty (line 45)

Shows combined: Tax (line 43); Use Tax (line 44); and Estimated Tax Penalty (line 45)")

52

NJ Income Tax Withheld (Line 47) Form W-2, Box 17 (State Income Tax Withheld) Form 1099-R (Pensions, etc) Include amounts from all W-2s & 1099s received Note: Be sure W-2, Box 15 Shows ‘NJ’

Form W-2, Box 17 (State Income Tax Withheld) Form 1099-R (Pensions, etc) Include amounts from all W-2s & 1099s received Note: Be sure W-2, Box 15 Shows ‘NJ’")

53

W-2 Sample

54

Earned Income Tax Credit (Line 50) Expanded for Tax Year 2007 & after All NJ Residents who qualify for Federal EITC are now eligible 25% of Federal EIC amount

Expanded for Tax Year 2007 & after All NJ Residents who qualify for Federal EITC are now eligible 25% of Federal EIC amount")

55

Excess UI/DI (Lines 51-52) For people with: Multiple employers Multiple W-2s With excess UI/DI contributions Must complete and include Form NJ- 2450 with NJ-1040

For people with: Multiple employers Multiple W-2s With excess UI/DI contributions Must complete and include Form NJ with NJ-1040")

56

Total Payments/Credits (Line 53) Include: Total NJ Income Tax Withheld Property Tax Credit (if applicable) Estimated Tax Payments NJEIC Excess UI/HC/WD Excess DI

Include: Total NJ Income Tax Withheld Property Tax Credit (if applicable) Estimated Tax Payments NJEIC Excess UI/HC/WD Excess DI")

57

Underpaid or Overpaid Compare Total Payments (Line 53) to Total Tax (Line 46) If Line 53 is greater than line 46, the difference is an overpayment If Line 53 is less than line 46, the difference is due to the state

to Total Tax (Line 46) If Line 53 is greater than line 46, the difference is an overpayment If Line 53 is less than line 46, the difference is due to the state")

58

Refund Amount (Line 64) Overpayments can be: Left as a credit for next year; Donated (all or in part) to various charitable designations; or Refunded to the Taxpayer Be sure to include requested refund amount on Line 64

Overpayments can be: Left as a credit for next year; Donated (all or in part) to various charitable designations; or Refunded to the Taxpayer Be sure to include requested refund amount on Line 64")

59

Property Tax Relief Programs Homestead Rebate Available to Homeowners and Renters Property Tax Reimbursement Available only to Homeowners

60

Homestead Rebate Tenants use Form TR-1040 Page 4 of the NJ-1040 Homeowners Applications are mailed after April 15 th File by Phone or Online

61

PTR - Eligibility Must be Age 65/ovr or Disabled by 12/31/2008 NJ Resident for at least 10yrs Owned and lived in the home for at least 3 years Have fully paid property taxes due

62

Property Tax Reimbursement Income Eligibility Limits 2008 Single/Married $70,000 2009 Single/Married $80,000

63

PTR – Income Limits Virtually all gross income is included for PTR eligibility Social Security Unemployment Military Pension NJ Lottery Winnings This will often vary from the income tax form

64

PTR - Application Form PTR-1 Used for 1 st time applicants Form PTR-2 2 nd and later years Proof of Property Taxes must be included

Similar presentations

– Child Tax Credit (CTC) Refund.>")