Download presentation

Presentation is loading. Please wait.

1

FRONTIERS OF REAL-TIME DATA ANALYSIS Dean Croushore Associate Professor, University of Richmond Interim Director, Real-Time Data Research Center, Federal Reserve Bank of Philadelphia October 2008

2

Introduction First paper to do real-time data analysis: –Gartaganis-Goldberger, Econometrica (1955) Statistical properties of the statistical discrepancy between GNP and gross national income changed after data were revised in 1954

Statistical properties of the statistical discrepancy between GNP and gross national income changed after data were revised in 1954")

3

Research Categories Data Revisions Forecasting Monetary Policy Macroeconomic Research Current Analysis

4

Introduction Data sets –Real-Time Data Set for Macroeconomists Philadelphia Fed + University of Richmond –Need for good institutional support –Club good: non-rival but excludable

5

Introduction Data sets –Unrestricted access: U.S.: Philadelphia Fed, St. Louis Fed, BEA OECD Bank of England (recently updated) –Restricted access: EABCN –Fate unclear: Canada –One-time research projects: Many, most not continuously updated

–Restricted access: EABCN –Fate unclear: Canada –One-time research projects: Many, most not continuously updated.")

6

Introduction Analysis of data revisions is not criticism of government statistical agencies! –May help agencies improve data production process –Revisions reflect limited resources devoted to data collection –Revised data usually superior to unrevised data (U.S. CPI vs. PCE price index)

.")

7

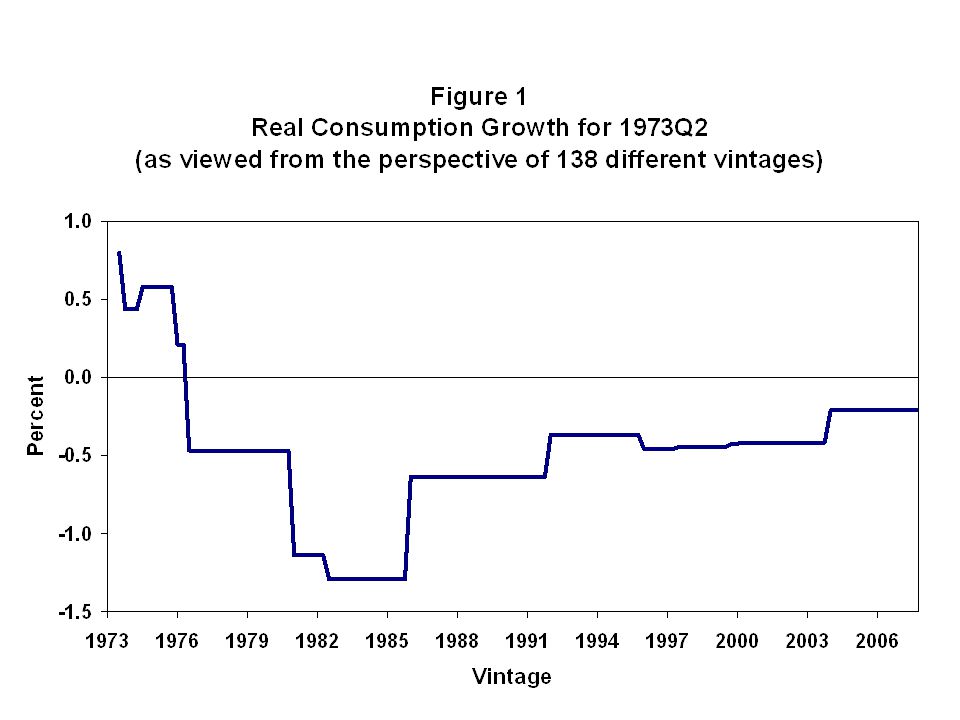

Introduction Structure of data sets –The data matrix Columns report vintages (dates on which data series are observed) Rows report dates for which economic activity is measured Moving across rows shows revisions Main diagonal shows initial releases Huge jumps in numbers indicate benchmark revisions with base year changes

Rows report dates for which economic activity is measured Moving across rows shows revisions Main diagonal shows initial releases Huge jumps in numbers indicate benchmark revisions with base year changes")

8

REAL OUTPUT Vintage: 11/65 2/66 5/66... 11/07 2/08 Date 47Q1306.4306.4306.4...1570.5 1570.5 47Q2309.0309.0309.0...1568.7 1568.7 47Q3309.6309.6309.6...1568.0 1568.0....... 65Q3609.1613.0613.0...3214.1 3214.1 65Q4 NA621.7624.4...3291.8 3291.8 66Q1 NA NA633.8...3372.3 3372.3....... 07Q1 NA NA NA... 11412.6 11412.6 07Q2 NA NA NA... 11520.1 11520.1 07Q3 NA NA NA... 11630.711658.9 07Q4 NA NA NA... NA11677.4

9

Data Revisions

10

What Do Data Revisions Look Like? Are They News or Noise? Is the Government Using Information Efficiently? Are Revisions Forecastable? How Should We Model Data Revisions? Key issue: are data revisions large enough economically to worry about?

11

Data Revisions What Do Data Revisions Look Like? –Short Term (example) –Long Term (example) What Do Different Types of Data Revisions Look Like? –Short run revisions based on additional source data –Benchmark revisions based on structural changes or updating base year

–Long Term (example) What Do Different Types of Data Revisions Look Like. –Short run revisions based on additional source data –Benchmark revisions based on structural changes or updating base year.")

14

Data Revisions Are Data Revisions News or Noise? –Data Revisions Add News: Data are optimal forecasts, so revisions are orthogonal to early data; revisions are not forecastable –Data Revisions Reduce Noise: Data are measured with error, so revisions are orthogonal to final data; revisions are forecastable

15

Data Revisions Are Data Revisions News or Noise? –Mankiw-Runkle-Shapiro (1984): Money data revisions reduce noise –Mankiw-Shapiro (1986): GDP data revisions contain news –Mork (1987): GMM results show “final” NIPA data contain news; other vintages are inefficient and neither noise nor noise –UK: Patterson-Heravi (1991): revisions to most components of GDP reduce noise

: Money data revisions reduce noise –Mankiw-Shapiro (1986): GDP data revisions contain news –Mork (1987): GMM results show final NIPA data contain news; other vintages are inefficient and neither noise nor noise –UK: Patterson-Heravi (1991): revisions to most components of GDP reduce noise.")

16

Data Revisions Is the Government Using Information Efficiently? Theoretical Issue: Should the government report its sample information or project an unbiased estimate using extraneous information?

17

Data Revisions Is the Government Using Information Efficiently? Key Issue: What is the trade-off the government faces between timeliness and accuracy? –Zarnowitz (1982): evaluates quality of different series –McNees (1989): found within-quarter estimate of GDP to be as accurate as estimate released 15 days after quarter end

: evaluates quality of different series –McNees (1989): found within-quarter estimate of GDP to be as accurate as estimate released 15 days after quarter end.")

18

Data Revisions Findings of bias and inefficiency based on ex-post tests –UK: Garratt-Vahey (2003) –US: Aruoba (2008)

–US: Aruoba (2008)")

19

Data Revisions Findings of bias and inefficiency of seasonally revised data –Kavajecz-Collins (1995) –Swanson-Ghysels-Callan (1999) Revisions to seasonals may be larger than revisions to NSA data: Fixler-Grimm-Lee (2003) Key question: Are seasonal revisions predictable? Who cares if that is an artifact of construction?

20

Data Revisions Key Issue: If early government data are projections, then state of business cycle may be related to later data revisions. –Dynan-Elmendorf (2001): GDP is misleading at turning points –Swanson-van Dijk (2004): volatility of revisions to industrial production and producer prices increases in recessions

: GDP is misleading at turning points –Swanson-van Dijk (2004): volatility of revisions to industrial production and producer prices increases in recessions.")

21

Data Revisions Are Revisions Forecastable? –Conrad-Corrado (1979): use Kalman filter to improve government’s monthly data on retail sales –Aruoba (2008): revisions to many U.S. variables are forecastable

: use Kalman filter to improve government’s monthly data on retail sales –Aruoba (2008): revisions to many U.S. variables are forecastable.")

22

Data Revisions Are Revisions Forecastable? –Key Issue: can revisions be forecast in real- time (or just ex-post)? Guerrero (1993): combines historical data with preliminary data on Mexican industrial production to get improved estimates of final data Faust-Rogers-Wright (2005): Examines G-7 countries’ output forecasts; find Japan & U.K. output revisions forecastable in real time

. Guerrero (1993): combines historical data with preliminary data on Mexican industrial production to get improved estimates of final data Faust-Rogers-Wright (2005): Examines G-7 countries’ output forecasts; find Japan & U.K. output revisions forecastable in real time.")

23

Data Revisions How Should We Model Data Revisions? –Howrey (1978) –Conrad-Corrado (1979) –UK: Holden-Peel (1982) –Harvey-McKenzie-Blake-Desai (1983) –UK: Patterson (1995) –UK: Kapetanios-Yates (2004)

–Conrad-Corrado (1979) –UK: Holden-Peel (1982) –Harvey-McKenzie-Blake-Desai (1983) –UK: Patterson (1995) –UK: Kapetanios-Yates (2004).")

24

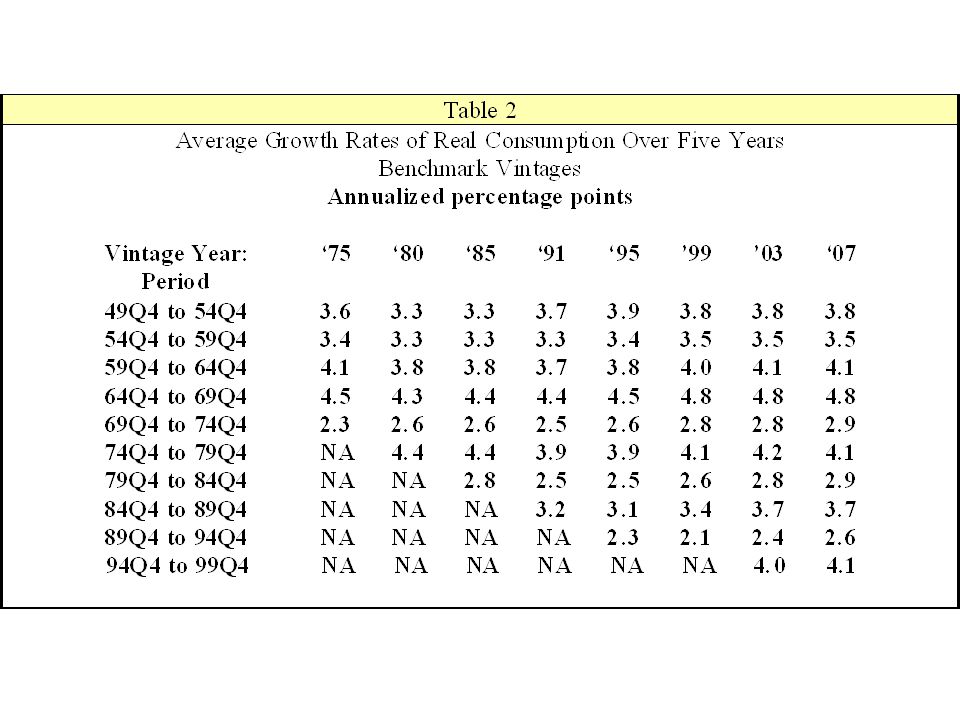

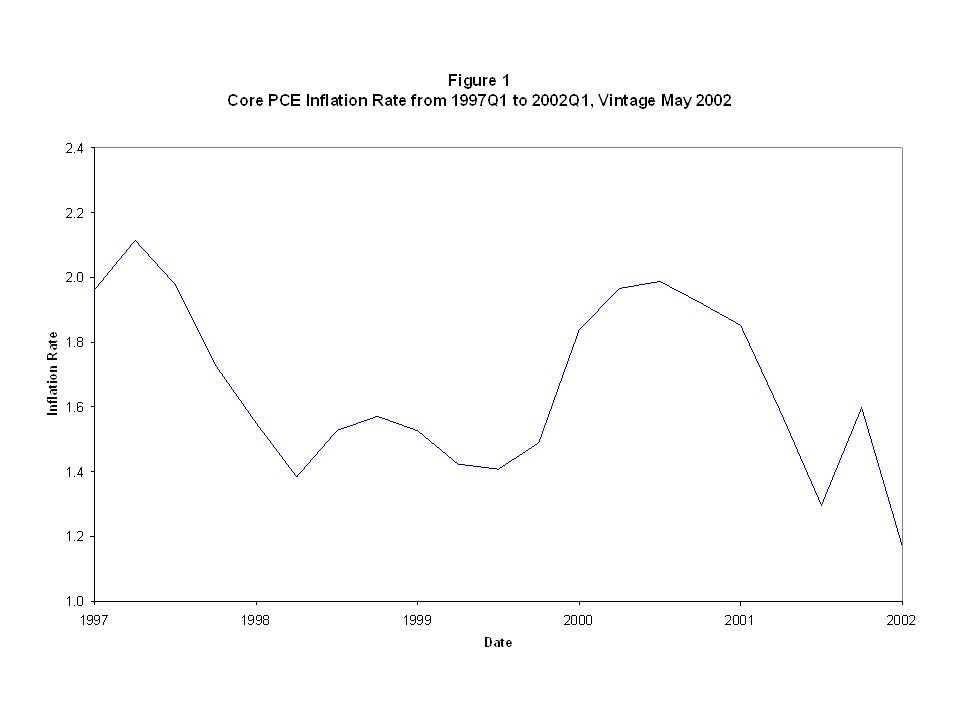

Data Revisions How Should We Model Data Revisions? –Is there any scope for new research here? Show predictability between different vintages to help data agencies improve methods Ex: US data on PCE inflation

25

Forecasting

26

Forecasts are only as good as the data behind them Literature focuses on model development: trying to build a better forecasting model, especially comparing forecasts from a new model to other models or to forecasts made in real time Details: Croushore (2006) Handbook of Economic Forecasting

Handbook of Economic Forecasting")

27

Forecasting Does the fact that data are revised matter significantly (in an economic sense) for forecasts?

for forecasts")

28

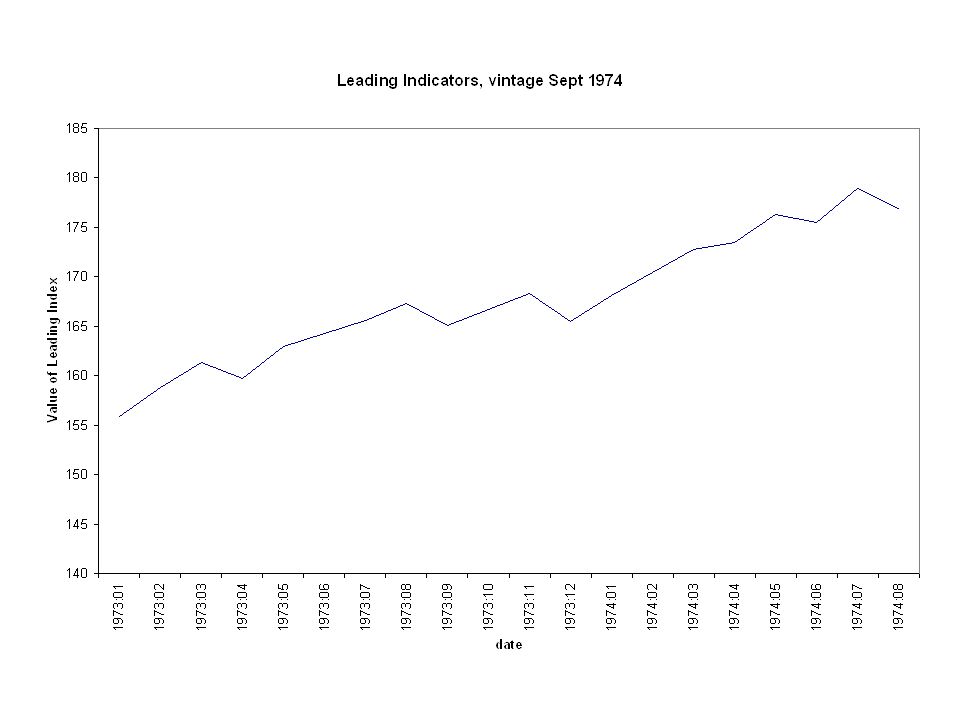

Forecasting EXAMPLE: THE INDEX OF LEADING INDICATORS Leading indicators: seem to predict recessions quite well. But did they do so in real time? The evidence suggests skepticism. Diebold and Rudebusch (1991) investigated the issue, using real-time data Their conclusion: The leading indicators do not lead and they do not indicate! The use of revised data gives a misleading picture of the forecasting ability of the leading indicators.

investigated the issue, using real-time data Their conclusion: The leading indicators do not lead and they do not indicate. The use of revised data gives a misleading picture of the forecasting ability of the leading indicators..")

30

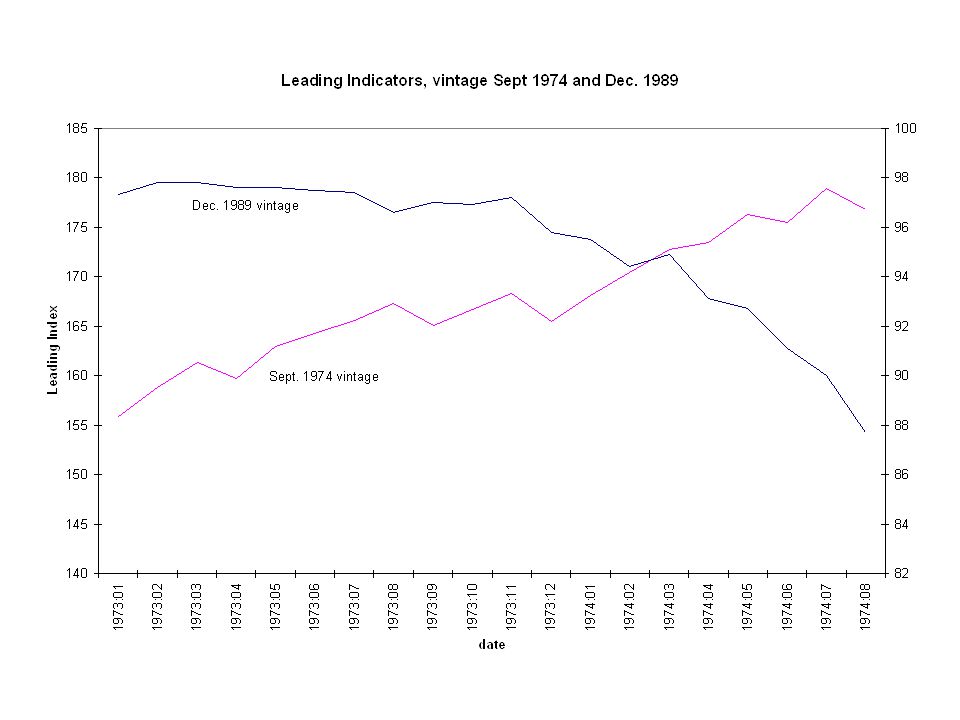

Forecasting EXAMPLE: THE INDEX OF LEADING INDICATORS Chart shows not much problem But recession started in November 1973 Subsequently, leading indicators were revised & ex-post they do much better

32

Forecasting Why Are Forecasts Affected by Data Revisions? –Change in data input into model –Change in estimated coefficients –Change in model itself (number of lags) –See experiments in Stark-Croushore (2002)

–See experiments in Stark-Croushore (2002).")

33

Forecasting What Do We Use as Actuals? –Answer: Depends on purpose –Best measures are probably latest-available data for “truth” (though perhaps not in fixed- weighting era) –But forecasters would not anticipate redefinitions and generally forecast to be consistent with government data methods (example: pre-chain-weighting period; 2013 capitalization of R&D)

–But forecasters would not anticipate redefinitions and generally forecast to be consistent with government data methods (example: pre-chain-weighting period; 2013 capitalization of R&D).")

34

Forecasting What Do We Use as Actuals? –Real-Time Data Set: many choices first release (or second, or third) four quarters later (or eight or twelve) Date of annual revision (July for U.S. data) last benchmark (the last vintage before a benchmark revision) latest available

four quarters later (or eight or twelve) Date of annual revision (July for U.S. data) last benchmark (the last vintage before a benchmark revision) latest available.")

35

Forecasting How Should Forecasts Be Made When Data Are Revised? –Key issue: temptation to cheat! Try method; it doesn’t work; but that’s because of one outlier; dummy out that observation; the method works! If data are not available, use a real-time proxy, don’t peak at future data Cheating is inherent because you know the history already

36

Forecasting Forecasting with Real-Time versus Latest- Available Data –Denton-Kuiper (1965): first to compare forecasts with real-time vs revised data –Cole (1969): data errors reduce forecast efficiency & may lead to biased forecasts –Trivellato-Rettore (1986): data errors in a simultaneous equations model affect everything: estimated coefficients and forecasts; but for small model of Italian economy, addition to forecast errors were not large

: first to compare forecasts with real-time vs revised data –Cole (1969): data errors reduce forecast efficiency & may lead to biased forecasts –Trivellato-Rettore (1986): data errors in a simultaneous equations model affect everything: estimated coefficients and forecasts; but for small model of Italian economy, addition to forecast errors were not large")

37

Forecasting Forecasting with Real-Time versus Latest- Available Data –Faust-Rogers-Wright (2003): research showing forecastability of exchange rates depended on a particular vintage of data; other vintages show no forecastability –Molodtsova (2007): combining real-time data with Taylor rule allows predictability of exchange rate –Moldtsova-Nikolsko-Rzhevskyy-Papell (2007): dollar/mark exchange rate predictable only with real- time data

: research showing forecastability of exchange rates depended on a particular vintage of data; other vintages show no forecastability –Molodtsova (2007): combining real-time data with Taylor rule allows predictability of exchange rate –Moldtsova-Nikolsko-Rzhevskyy-Papell (2007): dollar/mark exchange rate predictable only with real- time data")

38

Forecasting Summary: for forecasting, sometimes data vintage matters, other times it doesn’t

39

Forecasting Levels versus Growth Rates –Howrey (1996): level forecasts of GNP more sensitive than growth forecasts; so policy should feed back on growth rates, not levels –Kozicki (2002): choice of forecasting with real- time or latest-available data is important for variables with large level revisions

: level forecasts of GNP more sensitive than growth forecasts; so policy should feed back on growth rates, not levels –Kozicki (2002): choice of forecasting with real- time or latest-available data is important for variables with large level revisions")

40

Forecasting Model Selection and Specification –Swanson-White (1997): explores model selection –Robertson-Tallman (1998): real-time data affect model specification for industrial production but not for GDP –Harrison-Kapetanios-Yates (2005): it may be optimal to estimate a model without using most recent preliminary data –Summary: model choice is sometimes affected by data revisions

: explores model selection –Robertson-Tallman (1998): real-time data affect model specification for industrial production but not for GDP –Harrison-Kapetanios-Yates (2005): it may be optimal to estimate a model without using most recent preliminary data –Summary: model choice is sometimes affected by data revisions")

41

Forecasting Evidence on Predictive Content of Variables –Croushore (2005): consumer confidence indicators have no predictive power in real time, even when they appear to when using latest-available data

: consumer confidence indicators have no predictive power in real time, even when they appear to when using latest-available data")

42

Forecasting Optimal Forecasting When Data Are Subject to Revision –Howrey (1978): adjusts for differing degrees of revision using Kalman filter; in forecasting, use recent data but filter it –Harvey-McKenzie-Blake-Desai (1983): use state-space methods with missing observations to account for irregular data revisions: large gain in forecast efficiency compared with ignoring data revisions

: adjusts for differing degrees of revision using Kalman filter; in forecasting, use recent data but filter it –Harvey-McKenzie-Blake-Desai (1983): use state-space methods with missing observations to account for irregular data revisions: large gain in forecast efficiency compared with ignoring data revisions")

43

Forecasting Optimal Forecasting When Data Are Subject to Revision –Howrey (1984): use of state-space models to improve forecasts of inventory investment yields little improvement –Patterson (2003): illustrates how to combine measurement process with data generation process to improve forecasts for income & consumption

: use of state-space models to improve forecasts of inventory investment yields little improvement –Patterson (2003): illustrates how to combine measurement process with data generation process to improve forecasts for income & consumption")

44

Forecasting Optimal Forecasting When Data Are Subject to Revision –What information set to use? Koenig-Dolmas-Piger (2003), Kishor-Koenig (2005): focus on diagonals to improve forecasting; treat data the same that have been revised to the same degree

, Kishor-Koenig (2005): focus on diagonals to improve forecasting; treat data the same that have been revised to the same degree.")

45

Forecasting Optimal Forecasting When Data Are Subject to Revision –Summary: There are sometimes gains to accounting for data revisions; but predictability of revisions (today for US data) is small relative to forecast error (mainly seasonal adjustment)

is small relative to forecast error (mainly seasonal adjustment)")

46

Forecasting A Troublesome Issue –Specifying a process for data revisions –Some papers specify an AR process But research on revisions suggests that benchmark revisions are not so easily characterized

47

Forecasting Key Issue: What are the costs and benefits of dealing with real-time data issues versus other forecasting issues?

48

Monetary Policy

49

Monetary Policy: Data Revisions How Much Does It Matter for Monetary Policy that Data Are Revised? How Misleading Is Monetary Policy Analysis Based on Final Data Instead of Real-Time Data? How Should Monetary Policymakers Handle Data Uncertainty?

50

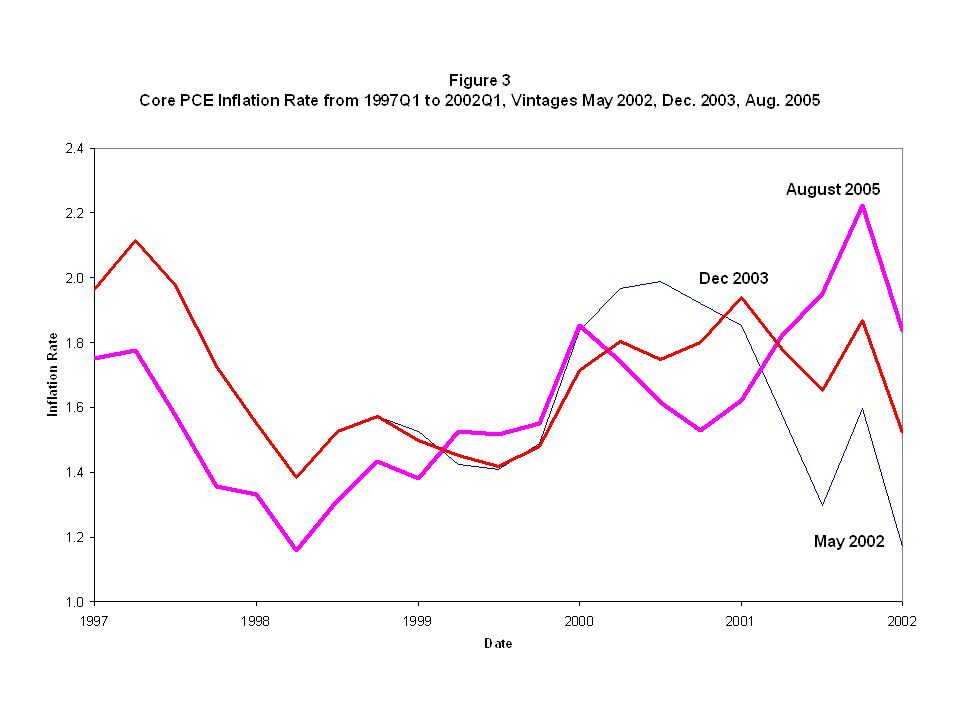

Monetary Policy: Data Revisions How Much Does It Matter for Monetary Policy that Data Are Revised? –Example: Fed’s favorite inflation measure is the Personal Consumption Expenditures Price Index Excluding Food & Energy Prices (PCEPIXFE) –But it has been revised substantially

–But it has been revised substantially.")

53

Monetary Policy: Data Revisions How Much Does It Matter for Monetary Policy that Data Are Revised? –Croushore (2008): PCE revisions could mislead the Fed –Maravall-Pierce (1986): The Fed optimally signal extracts from the noise in money data, so data revisions would not significantly affect monetary policy –Kugler et al. (2005): Monetary policy shojuld be less aggressive because of data revisions

: PCE revisions could mislead the Fed –Maravall-Pierce (1986): The Fed optimally signal extracts from the noise in money data, so data revisions would not significantly affect monetary policy –Kugler et al. (2005): Monetary policy shojuld be less aggressive because of data revisions.")

54

Monetary Policy: Data Revisions How Misleading Is Monetary Policy Analysis Based on Final Data Instead of Real-Time Data? –Croushore-Evans (2006): Data revisions do not significantly affect measures of monetary policy shocks in recursive systems, but they make identification of simultaneous systems problematic

: Data revisions do not significantly affect measures of monetary policy shocks in recursive systems, but they make identification of simultaneous systems problematic.")

55

Monetary Policy: Data Revisions How Should Monetary Policymakers Handle Data Uncertainty? –Coenen-Levin-Wieland (2001): use money as an indicator when GDP data are uncertain –Bernanke-Boivin (2003): use factor model to incorporate much data; results do not depend on using real-time data instead of revised data

: use money as an indicator when GDP data are uncertain –Bernanke-Boivin (2003): use factor model to incorporate much data; results do not depend on using real-time data instead of revised data.")

56

Monetary Policy: Data Revisions How Should Monetary Policymakers Handle Data Uncertainty? –Giannone-Reichlin-Sala (2005): extract real- time information to determine a real shock and a nominal shock, which represent fundamental dynamics of US economy

: extract real- time information to determine a real shock and a nominal shock, which represent fundamental dynamics of US economy.")

57

Monetary Policy: Data Revisions How Should Monetary Policymakers Handle Data Uncertainty? –Aoki (2003): without certainty equivalence, policymakers need to react less aggressively; theoretical view –Similar results hold with uncertainty about potential output or other analytical concepts

: without certainty equivalence, policymakers need to react less aggressively; theoretical view –Similar results hold with uncertainty about potential output or other analytical concepts.")

58

Monetary Policy: Analytical Revisions What Happens When Economists or Policymakers Revise Conceptual Variables? –Output gap –Natural rate of unemployment –Equilibrium real interest rate Concepts are never observed, but are centerpiece of macroeconomic theory

59

Monetary Policy: Analytical Revisions Orphanides (2001): Fed overreacted to perceived output gap in 1970s, causing Great Inflation; but output gap was mismeasured

: Fed overreacted to perceived output gap in 1970s, causing Great Inflation; but output gap was mismeasured")

60

Monetary Policy: Analytical Revisions One strand of literature: plug alternative data vintages into Taylor rule: –Kozicki (2004) on U.S. data –Kamada (2005) on Japanese data Other Taylor rule work: –Rudebusch (2001): reverse engineer Taylor rule; it would be more aggressive if data weren’t uncertain –Orphanides (2003): if policy rules are based on revised data, they are too aggressive

on Japanese data Other Taylor rule work: –Rudebusch (2001): reverse engineer Taylor rule; it would be more aggressive if data weren’t uncertain –Orphanides (2003): if policy rules are based on revised data, they are too aggressive.")

61

Monetary Policy: Analytical Revisions Other real-time models of policy rules: –Cukierman-Lippi (2005): Fed was too aggressive in 1970s, appropriately conservative in 1990s –Boivin (2006): Fed changed policy parameters in 1970s and temporarily reduced response to inflation: causing Great Inflation

: Fed was too aggressive in 1970s, appropriately conservative in 1990s –Boivin (2006): Fed changed policy parameters in 1970s and temporarily reduced response to inflation: causing Great Inflation")

62

Monetary Policy: Analytical Revisions Other natural rate issues –Orphanides-Williams (2002): large costs to ignoring mismeasurement of natural rate of unemployment and natural rate of interest –Staiger-Stock-Watson (1997): tremendous uncertainty about natural rate of unemployment –Clark-Kozicki (2005): ditto for natural rates of interest

: large costs to ignoring mismeasurement of natural rate of unemployment and natural rate of interest –Staiger-Stock-Watson (1997): tremendous uncertainty about natural rate of unemployment –Clark-Kozicki (2005): ditto for natural rates of interest")

63

Monetary Policy: Analytical Revisions Output gap uncertainty: –U.S.: Orphanides-van Norden (2002) –UK: Nelson-Nikolov (2003) –Germany: Gerberding-Seitz-Worms (2005) –Euro area: Gerdesmeieir-Roffia (2005) –Norway: Bernhardsen (2005) –Canada: Cayen-van Norden (2005) –Germany: Döpke (2005)

–UK: Nelson-Nikolov (2003) –Germany: Gerberding-Seitz-Worms (2005) –Euro area: Gerdesmeieir-Roffia (2005) –Norway: Bernhardsen (2005) –Canada: Cayen-van Norden (2005) –Germany: Döpke (2005)")

64

Monetary Policy: Analytical Revisions Policy models may change: –Tetlow-Ironside (2007): changes in FRB-US model changed the story the model was telling to policymakers

: changes in FRB-US model changed the story the model was telling to policymakers")

65

Monetary Policy: Analytical Revisions What Happens When Economists or Policymakers Revise Conceptual Variables? –Key issue: end-of-sample inference for forward-looking concepts (filters) –Key issue: optimal model of evolution of analytical concepts Most work is statistical; perhaps a theoretical breakthrough is needed

–Key issue: optimal model of evolution of analytical concepts Most work is statistical; perhaps a theoretical breakthrough is needed.")

66

Macroeconomic Research

67

How Is Macroeconomic Research Affected By Data Revisions? –Croushore-Stark (2003): how results from key macro studies are affected by alternative vintages –Boschen-Grossman (1982): testing neutrality of money under rational expectations: support for RE with revised data, but not with real-time data

: how results from key macro studies are affected by alternative vintages –Boschen-Grossman (1982): testing neutrality of money under rational expectations: support for RE with revised data, but not with real-time data.")

68

Macroeconomic Research How Is Macroeconomic Research Affected By Data Revisions? –Amato-Swanson (2001): the predictive content of money for output is not clear in real time; only in revised data

: the predictive content of money for output is not clear in real time; only in revised data.")

69

Macroeconomic Research Should Macroeconomic Models Incorporate Data Revisions? –Aruoba (2004): business-cycle dynamics are captured better by a DSGE model that accounts for data revisions than one that does not –Edge, Laubach, Williams (2004): learning explains long-run productivity growth forecasts; helps explain cycles in employment, investment, long-term interest rates

: business-cycle dynamics are captured better by a DSGE model that accounts for data revisions than one that does not –Edge, Laubach, Williams (2004): learning explains long-run productivity growth forecasts; helps explain cycles in employment, investment, long-term interest rates.")

70

Macroeconomic Research Do Data Revisions Affect Economic Activity? –Oh-Waldman (1990): false (positive) announcements increase economic activity with leading indicators and industrial production in real time –Bomfim (2001): improving the signal in data would exacerbate cyclical fluctuations if agents performed optimal signal extraction; but if agents ignore data revisions, then improving data quality would reduce cyclical fluctuations

: false (positive) announcements increase economic activity with leading indicators and industrial production in real time –Bomfim (2001): improving the signal in data would exacerbate cyclical fluctuations if agents performed optimal signal extraction; but if agents ignore data revisions, then improving data quality would reduce cyclical fluctuations.")

71

Macroeconomic Research Overall: literature in its infancy: more work needed in all three areas (robustness of research results, incorporating data revisions into macro models, examining how or whether data revisions affect economic activity)

")

72

Current Analysis How Do Financial Markets React to Data Revisions? –Christoffersen-Ghysels-Swanson (2002): need real-time data to properly determine announcement effects in financial markets

: need real-time data to properly determine announcement effects in financial markets.")

73

Current Analysis How Is Business Cycle Dating Affected By Data Revisions? –Economists like to argue about the state of the business cycle...

75

Current Analysis How Is Business Cycle Dating Affected By Data Revisions? –Chauvet-Piger (2003, 2005): test algorithms to identify turning points in real time –Chauvet-Hamilton (2006): develop alternative recession indicators and forecasts in real time –Nalewaik (2007): using real-time gross domestic income helps forecast recessions better than just using GDP

: test algorithms to identify turning points in real time –Chauvet-Hamilton (2006): develop alternative recession indicators and forecasts in real time –Nalewaik (2007): using real-time gross domestic income helps forecast recessions better than just using GDP.")

76

Current Analysis Overall: much additional research needed in current analysis in real time

77

Summary Field of real-time data analysis offers many opportunities for new research Most promising areas: –Macroeconomic research: incorporating data revisions into macro models –Current analysis of business and financial conditions –Other areas are more mature & need more sophisticated analysis

Similar presentations

= $11,814.9B (5.5%) Q2: GDP = $2,914.38.>")

? How is GDP calculated? What is the difference between nominal and.>")

, J.D. De La Salle University, Manila 51 st Philippine Economic.>")