Download presentation

Presentation is loading. Please wait.

1

1 Jan Pasmooij RE RA RO Chair Assurance Working Group XBRL Int. Chair XBRL Netherlands Member International Steering Committee XBRL Int. Manager ICT Knowledge Center Koninklijk NIVRA Program Director Postgraduate Curriculum IT-Auditing, Erasmus University, Rotterdam Chair International Innovation Network The impact of electronic business reporting on audit and assurance A new challenge for the audit profession WCOA 2006, Workshop 2.1.1, November 15, 2006

2

Program The current reporting model Issues of technology – XBRL Risk involved Audit and assurance issues Scenarios for the use of interactive data The impact of the future reporting model on the assurance standards Proposals for assurance framework for electronic business reporting Call to action

3

Current reporting model Information- systems Banks Chambers of Commerce Governments Regulators Analysts Shareholders Manual input Preparing process Financial Statement Loc al US IFRS GAAP

4

NL Information- systems Manual input US IFRS XBRL preparing process XBRL GAAP Taxonomies Extension Taxonomy Banks Chambers of Commerce Governments Regulators Analysts Shareholders Financial Statements XBRL Instance-documen t Reporting based on XBRL

9

The current reporting model based on XBRL Information- systems Banks Chambers Of Commerce Governments Regulators Analysts GAAP Taxonomies Shareholders Manual input Local US IFRS t Preparing process Financial Statements XBRL Instance-documen t

11

Risks involved With data in electronic format we need specific controls for: Identification Integrity Authenticity

12

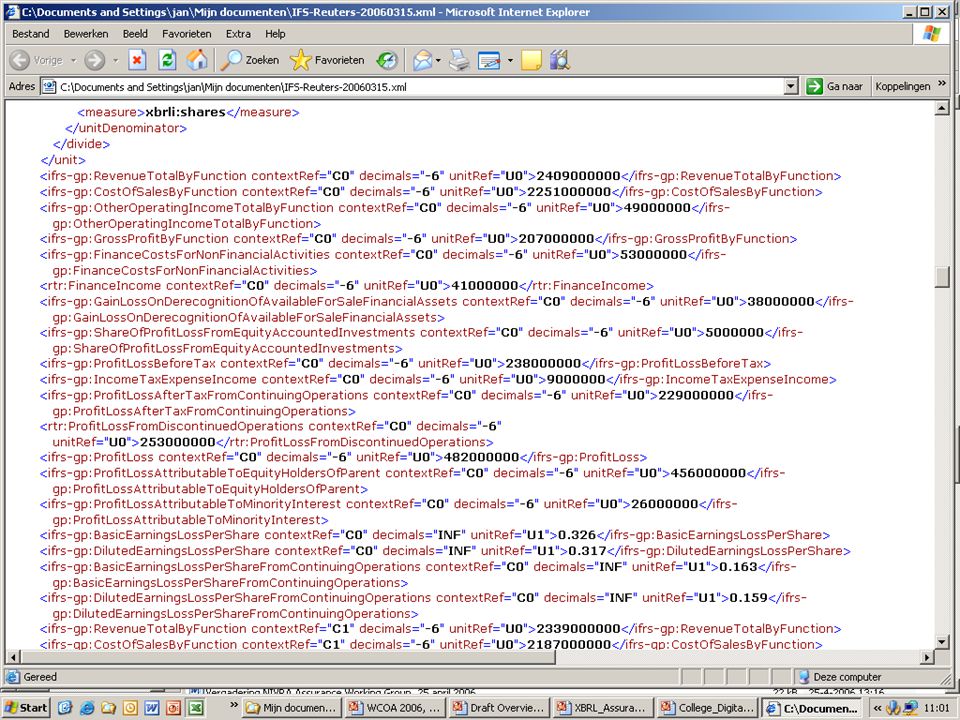

Audit and assurance issues The current auditing standards are providing no guidance how to provide assurance on information in electronic format Current audit opinion is focusing on document level (fair view) Instance document is a dataset, presentation via a style sheet, so no fair view?? So we need assurance on data-level?? We have no taxonomy for the audit opinion or guidance how to connect the opinion to an instance document, could be the FS No requirements yet for integrity and authenticity of instances documents No guidance yet about signing audit opinions and validations of the signature

13

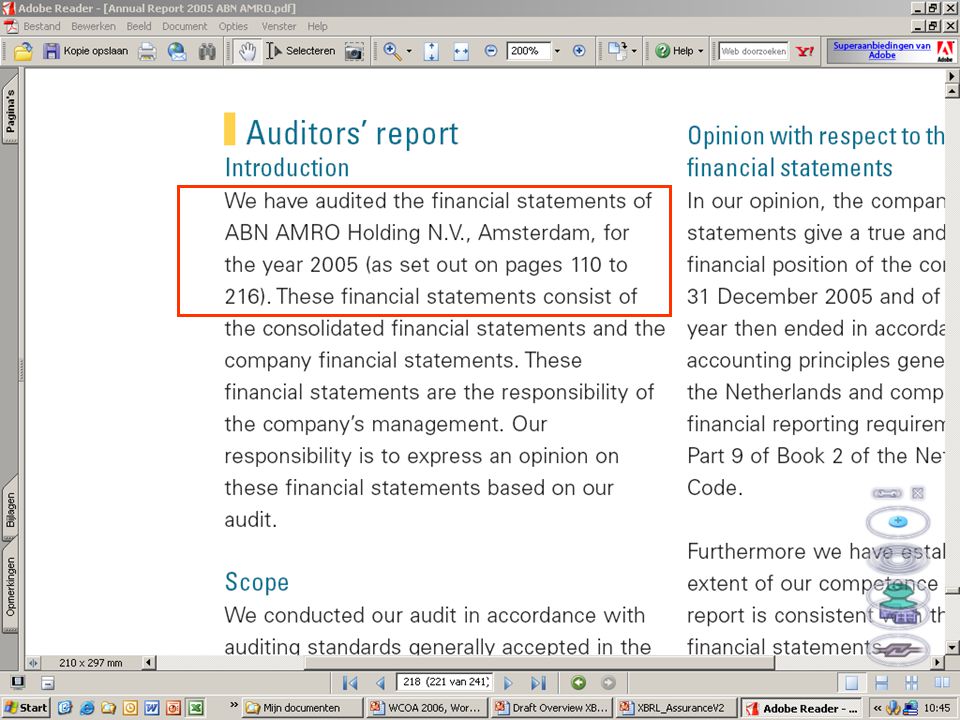

Subject matter: Financial Statements In paper format Identifying data (Entity) Data Classification / Grouping Disclosures Layout / Presentation Page numbers Graphics -- In XBRL format Identifying data (Entity) Data Tags Disclosures -- Taxonomy references ??

Data Classification / Grouping Disclosures Layout / Presentation Page numbers Graphics -- In XBRL format Identifying data (Entity) Data Tags Disclosures -- Taxonomy references ")

14

Loc al US Information- systems Users Manual input Preparing process Financial Statements The current audit opinion on Financial Statements is based on ISA 700, 701, 705 or 706. The audit opinion states that the financial statements give a “True and fair view or presented fairly, in all material respects, …………..” The current financial audit and opinion is based on the ISA’s 100 – 999 “Audits of Historical Financial Information”. IFRS GAAP Financial Statements on paper

15

Information- systems Users Manual input Financial Statements Users XBRL preparing process NL US IFRS XBRL Instance- documen t New ISA 80x or 30xx. The opinion should states that the data are derived from the Financial Statements of ….. are the same as GAAP Taxonomies Preparing process Loc al US IFRS GAAP Sc. : Traditional FS converted to XBRL format

16

Information- systems Users Manual input NL US IFRS XBRL Instance- documen t XBRL preparing process A specific ISA 70x for expressing an opinion on “Financial Statements” in XBRL format XBRL Taxonomies Sc. : FS in XBRL format only

17

Information- systems Users Manual input Users NL US IFRS XBRL Instance- documen t XBRL Preparing process Rendered Financial Statements A combined audit opinion about the quality of the data and the data presented being derived from a dataset in XBRL format using a specific style sheet, could be the traditional FS. Rendering process Sc. : FS in XBRL format only with rendered FS XBRL Taxonomies

18

Information- systems Users Manual input NL US IFRS XBRL Instance- documen t XBRL preparing process A specific ISA 30xx for an Assurance Engagements to provide a conclusion on data in XBRL format XBRL Taxonomies Sc. : Regulatory or Government filing

19

Information- systems Users Manual input NL US IFRS XBRL Instance- documen t XBRL preparing process A specific ISA 30xx for an Assurance Engagements to provide a conclusion on the XBRL preparing process XBRL Taxonomies Sc. : Assurance on XBRL preparing process

20

Call to action Recognition by auditors and users of the issues addressed Collect user views about assurance IFAC / IAASB take ownership of the assurance issues IFAC/IAASB should develop a long term strategy with regard to XBRL beyond the promulgation of immediate standards AWG and XBRL Int. are gladly willing to help

Similar presentations

Huub Lucassen Leader XBRL Assurance Services (Ernst & Young)>")

XBRL: eXtensible Business Reporting Language PowerPoint Presentations.>")

platform for the analysis, exchange, and reporting of financial information with the purpose.>")

![XBRL Adoption in Singapore [Mr Ivan Koo]](/20/6027590/big_thumb.jpg "XBRL Adoption in Singapore [Mr Ivan Koo]>")