Download presentation

Presentation is loading. Please wait.

1

Accounting Information Systems C H A P T E R 8 Electronic Presentations in Microsoft® PowerPoint®

2

1. Explain the relationship of the accounting information system to the management information system and identify the components of an AIS 2. Explain the goals and uses of special journals. 3. Describe the use of controlling accounts and subledgers. Learning Objectives

3

4. Journalize and post transactions using special journals. 5. Prepare and test the accuracy of subledgers. 6. Apply journalizing and posting of transactions using special journals in a periodic inventory system. (Appendix 8A) 7. Journalize and post transactions with sales taxes to special journals. (Appendix 8B) Learning Objectives

7. Journalize and post transactions with sales taxes to special journals. (Appendix 8B) Learning Objectives.")

4

A system designed to collect and process data within an organization for the purpose of providing users with information. Management Information Systems

5

Management Information System Sales and Marketing System Finance System Accounting Information System Human Resources System Production System InternalExternal Community Competitors Customers Government Industry Suppliers

6

The people, records, methods, and equipment that collect and process data from transactions and organize them in useful forms, and communicate results to decision makers. Accounting Information Systems (AIS)

.")

7

Components of an AIS Accounting Information System Accounts Payable Payroll Capital Assets Accounts Receivable Inputs Source Documents Outputs Reports/ Information to Internal/ External Users Feedback Loop

8

Impact of technology-based systems on accounting. Electronic funds transfer (EFT) E-commerce Computer hardware Computer software Accounting and Technology

E-commerce Computer hardware Computer software Accounting and Technology.")

9

Most organizations use Special Journals to enhance efficiency of transaction processing. Types Sales Journal Cash Receipts Journal Purchases Journal Cash Disbursements Journal Special Journals

10

A listing of individual accounts with a common characteristic. Common Subledgers Accounts Receivable Accounts Payable Inventory Subledgers

11

Accounts Receivable Subledger A separate subledger account is used to show how much each individual customer owes.

12

After all items are posted, the balance in the Accounts Receivable controlling account must equal the sum of the balances in the subledger. Accounts Receivable Subledger

13

A subsidiary ledger: A) Includes transactions not covered by special journals. B) Is a listing of all of the accounts of a business. C) Is a listing of individual accounts with a common characteristic. D) Is a listing of all accounts with balances. E) Is a listing of all special journals. Mini-Quiz

Is a listing of all of the accounts of a business. C) Is a listing of individual accounts with a common characteristic. D) Is a listing of all accounts with balances. E) Is a listing of all special journals. Mini-Quiz.")

14

A subsidiary ledger: A) Includes transactions not covered by special journals. B) Is a listing of all of the accounts of a business. C) Is a listing of individual accounts with a common characteristic. D) Is a listing of all accounts with balances. E) Is a listing of all special journals. Mini-Quiz

Is a listing of all of the accounts of a business. C) Is a listing of individual accounts with a common characteristic. D) Is a listing of all accounts with balances. E) Is a listing of all special journals. Mini-Quiz.")

15

The sales journal is used to record sales of merchandise on credit. Sales Journal

16

On February 2, Jason Henry purchased $450 of merchandise on account from Outdoors Unlimited. The goods originally cost Outdoors $315. Record the entry in the Sales Journal. (Assume the use of a perpetual inventory system.) Sales Journal — Example

Sales Journal — Example.")

17

Sales Journal Since each transaction yields a debit to Accounts Receivable and a credit to Sales, we need only one column for these two accounts. This column total is posted monthly.

18

Sales Journal Similarly, each transaction yields a debit to Cost of Goods Sold and a credit to Inventory. Therefore, these accounts can also be included together in one column. This column total would also be posted monthly.

19

Sales Journal Daily, each transaction is posted to the appropriate Accounts Receivable subledger account.

20

Sales Journal A in the PR column indicates the transaction has been posted to the subledger account.

21

Here is the Sales Journal after recording some additional sales. Sales Journal

22

On Feb. 28 th, post the column total to Accounts Receivable and Sales. Feb. 2 S1 2,150 2,150 2011

23

Sales Journal Now post to the COGS and Inventory accounts … Feb. 2 S1 1,500 1,500 2011

24

Sales Journal … and include the posting references. Feb. 2 S1 1,500 1,500 2011

25

The Accounts Receivable controlling account and the subledger are in balance. Testing the Ledger

26

If a company has few sales returns, they may record them in the General Journal. But, if a company has lots of sales returns, they may use a Sales Returns and Allowances Journal. Sales Returns and Allowances

27

The cash receipts journal is used to record all receipts of cash. Cash Receipts Journal

28

Categories of Cash Receipts Cash from cash sales Cash from credit customers Cash from other sources Cash Receipts Journal — Example

29

Cash Receipts Journal

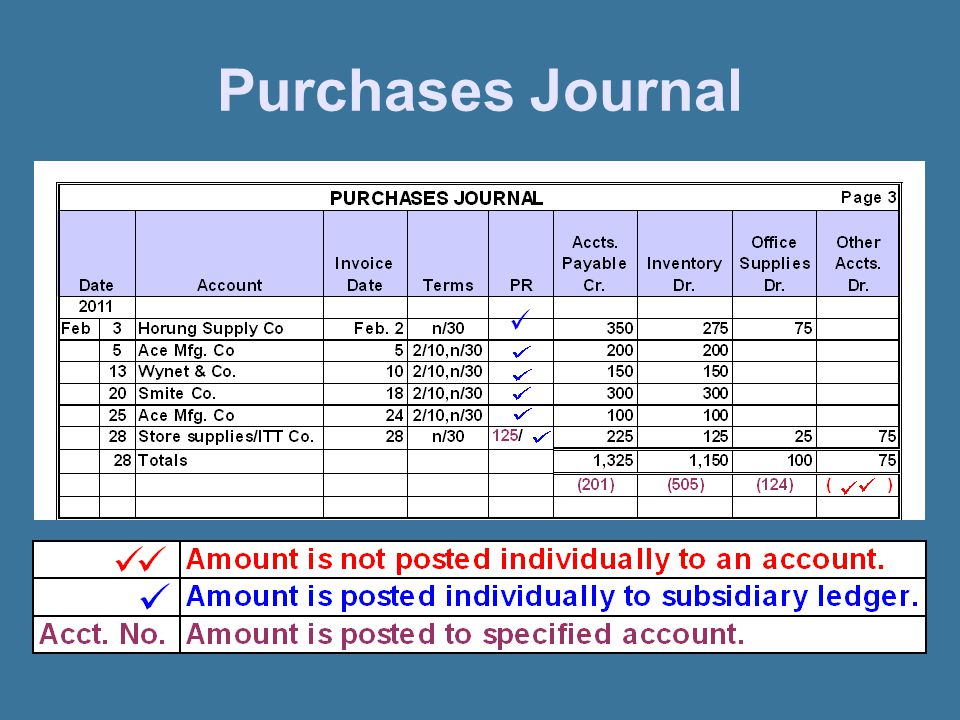

30

The Purchases Journal is used to record all purchases on credit. Purchases Journal

32

The Cash Disbursements Journal is used to record all payments of cash. Outdoors Unlimited Cash Disbursements Journal

34

Used for all transactions not recorded in a special journal. Closing entries Adjusting entries Correcting entries Other entries General Journal

35

Mini-Quiz Purchased equipment on credit. Sold merchandise for cash. Paid for supplies that were purchased on account. Sold merchandise on account. Give the name of the journal in which the following transactions should be recorded. PJ CRJ CDJ SJ

36

Recording and posting is similar to a perpetual system. Some of the columns change in a periodic system. Special Journals Under a Periodic System-Appendix 8A

37

The column for Cost of Goods Sold and Inventory is not needed with the periodic system. Sales Journal — Periodic System

38

Cash Receipts Journal Periodic System The column for Cost of Goods Sold and Inventory is not needed with the periodic system.

39

Purchases Journal — Periodic System The Inventory column in the perpetual system is replaced with Purchases column in the periodic system.

40

Cash Disbursements Journal Periodic System The Inventory column in the perpetual system is replaced with Purchases Discounts column in the periodic system.

41

Additional columns must be added to special journals to record PST and GST. Column Needed Journal PST Payable GST Payable GST Receivable Salesyes Cash Rec.yes Purchasesyes Cash Disb.yes Special Journals and Sales Taxes- Appendix 8B

42

Identify the different types of special journals? Sales journal Cash receipts journal Purchases journal Disbursements journal Review

43

What is the purpose of special journals? Special journals help reduce the costs related to the time and effort of posting accounts. Review

44

Why should sales to and receipts of cash from credit customers be recorded and posted daily? Daily recording and posting of credit sales and cash receipts from customers provides up-to-date information used in decisions about granting credit to customers. Also, up-to-date account balances are needed if customers inquire about the amount of their balances. Review

45

End of Chapter

Similar presentations