Download presentation

Presentation is loading. Please wait.

1

http://www.ahe.es THE SPANISH HOUSING & MORTGAGE EXPERIENCE José Ramón Ormazabal Spanish Mortgage Association Moscow, 27 Oct 2007

2

http://www.ahe.es The origins & evolution of the market Fundamentals of the growth of the market Current situation & prospects Mortgage Market Legal Modernization TABLE OF CONTENTS

3

http://www.ahe.es THE ORIGINS OF THE MODERN MORTGAGE MARKET The Mortgage Law (1946) Provides legal security to registered charge holders. Establishes the role of Public Land Registry, Public Notaries in the Registration Procedure and the Judiciary in Foreclosing Procedures. Establishes the principle of Right of Credit. Accessoriness. IT PROVIDES LEGAL & OPERATIONAL SECURITY

4

http://www.ahe.es THE ORIGINS OF THE MODERN MORTGAGE MARKET TIME TO REGISTER MORTGAGE, MONTHS TIME TO REPOSSESS, MONTHS SOURCE:EUROPEAN MORTGAGE FEDERATION

5

http://www.ahe.es THE ORIGINS OF THE MODERN MORTGAGE MARKET LAW 2/1981 & ROYAL DECREE 685/1982 THE MONCLOA AGREEMENTS October 1977 ITEM V.9 Removal of Legal and Administrative obstacles preventing the creation of AN EFFICIENT MORTGAGE MARKET

6

http://www.ahe.es The 1982 Mortgage Market Law Opens up the Mortgage Market to all types of Banks. Fosters the creation of single purpose Mortgage Entities. Establishes the conditions for Loans to be under the umbrella of this Law: - Purpose of the Loan - Maximum LTV’s. 70%. (80% for housing) - First rank charge over full property dominion - Damage Insurance Policy Valuation methodology, rules and supervision of Valuers are established. THE ORIGINS OF THE MODERN MORTGAGE MARKET Establishes new rules for Mortgage Funding Instruments.

- First rank charge over full property dominion - Damage Insurance Policy Valuation methodology, rules and supervision of Valuers are established. THE ORIGINS OF THE MODERN MORTGAGE MARKET Establishes new rules for Mortgage Funding Instruments..")

7

http://www.ahe.es EVOLUTION OF MORTGAGE LENDING OUTSTANDING DEC -81 12,921 Source: Bank of Spain and Spanish Mortgage Association (AHE) JUL - 07 1,.005,594 Million Euro

JUL ,.005,594 Million Euro")

8

http://www.ahe.es SPAIN IN 1996 Unemployment Rate: 24% 5 years of negative housing cycle. Accumulation of unsatisfied housing demand. Solid Banking system with strict Banking Supervision. Need to commercially grow in a context of poor consumption level. High liquidity with low credit demand. Newly elected Government. Need to streamline the economy to comply in January 1998 with Euro convergence rules.

9

http://www.ahe.es Source: Bank of Spain and AHE TOTAL DOMESTIC PRIVATE LENDING 1996-2006 MORTGAGE CREDIT AS A % OF: GROSS DOMESTIC PRODUCT

10

http://www.ahe.es Secondary Market Evolution (AIAF) Mortgage Covered Bonds (Cédulas) Dec-06: € 214.8 billion (05-06 growth: 43%) MBS Dec-06: € 93.7 billion (05-06 growth: >40%) Total MCB & MBS: € 308,5 billion ( 05-06 growth: 40%) Mortgage MCB & MBS as a % of Mortgage Credit

Mortgage Covered Bonds (Cédulas) Dec-06: € billion (05-06 growth: 43%) MBS Dec-06: € 93.7 billion (05-06 growth: >40%) Total MCB & MBS: € 308,5 billion ( growth: 40%) Mortgage MCB & MBS as a % of Mortgage Credit")

11

http://www.ahe.es HOUSING ACTIVITY Source: Ministerio de Fomento

12

http://www.ahe.es EMPLOYMENT EVOLUTION IN THE CONSTRUCTION INDUSTRY (People ‘000) Source: INE

Source: INE")

13

http://www.ahe.es (*) Source: The Housing Unit (UEPC) Simple Average: 440,2 528 HOUSING STOCK PER 1,000 INHABITANTS IN EUROPE

Source: The Housing Unit (UEPC) Simple Average: 440,2 528 HOUSING STOCK PER 1,000 INHABITANTS IN EUROPE")

14

http://www.ahe.es HOUSING PRICES EFFECTS ON THE MARKET Positive Effects: Rise on Real Estate Wealth Setbacks: Increasing need of Mortgage finance 1. Deterioration of the debt to income ratios… 2. Lower-Income groups out of market: young people… But still, Net Real Estate Wealth,…a very positive effect.... Source: Ministerio de Vivienda

15

http://www.ahe.es 2005 Owner Occupation Rates in European Countries Source: European Mortgage Federation

16

http://www.ahe.es HOUSEHOLD REAL ESTATE WEALTH NET OF MORTGAGE DEBT (*) Since mar-05 the data estimated due to the change of housing prices statistics Source: Bank of Spain

Since mar-05 the data estimated due to the change of housing prices statistics Source: Bank of Spain")

17

http://www.ahe.es STRUCTURE OF RESIDENTIAL GROSS LENDING 2004-2006 200420052006 First Home:34,33536,8 Second House2022,524,7 TOTAL HOUSE2931,534,4 Others (*)152121,5 SOURCE: AHE (*) Including Renovation, Improvement works, garages, etc. 200420052006 First Home:71,571,968,95 Second House6064,565 TOTAL HOUSE6566,568,2 Others (*)404645 DEBT-SERVICE TO INCOME RATIO (%) LOAN TO VALUE (%)

DEBT-SERVICE TO INCOME RATIO (%) LOAN TO VALUE (%).")

18

http://www.ahe.es THE SPANISH HOUSING & MORTGAGE EXPERIENCE 1. FUNDAMENTALS OF DEMAND HOW HAS THIS EVOLUTION BEEN POSSIBLE?

19

http://www.ahe.es EVOLUTION OF LEGAL FOREIGNERS IN SPAIN NUMBER OF HOUSEHOLDS (000s) Source: INE

Source: INE")

20

http://www.ahe.es Source: INE RISE 94-06 Men: 3,7 Women: 4,0 Total: 7,7

21

http://www.ahe.es THE SPANISH HOUSING & MORTGAGE EXPERIENCE 2. FUNDAMENTALS OF (MORTGAGE CREDIT) SUPPLY

SUPPLY.")

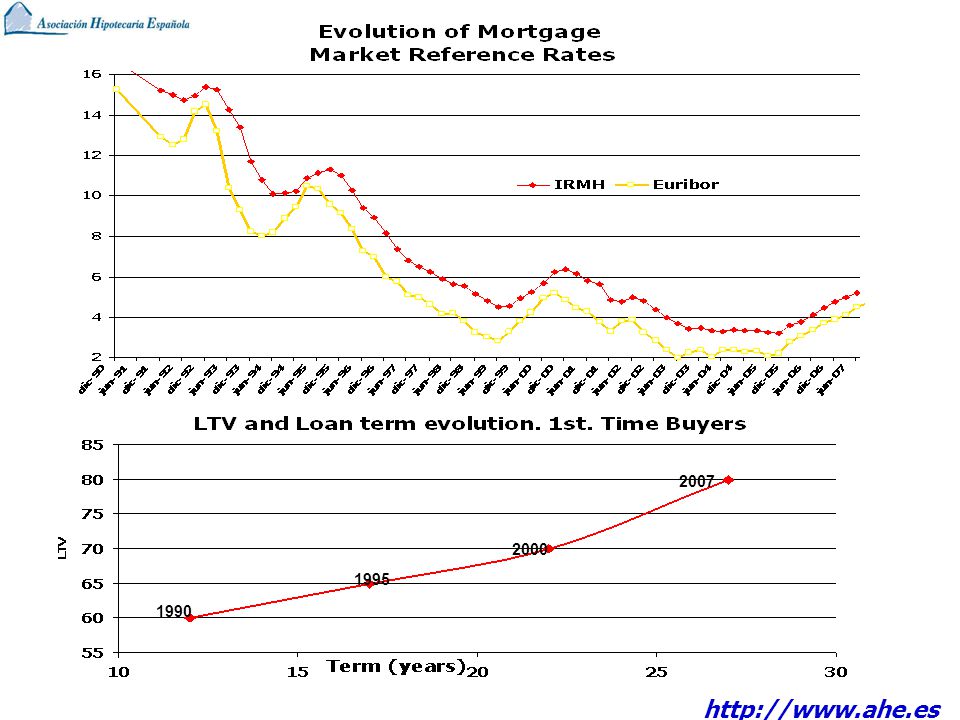

22

http://www.ahe.es 1990 1995 2000 2007

23

http://www.ahe.es A Indebtedness capacity evolution Access to housing A: x 5,15 B: x 3,3 A/B: approx x 1,5 Source: Bank of Spain and INE. Data up to July 2007

24

http://www.ahe.es THE SPANISH HOUSING & MORTGAGE EXPERIENCE CURRENT SITUATION

25

http://www.ahe.es MORTGAGE LENDING OUTSTANDING YEAR TO YEAR VARIATION RATES Source: Bank of Spain and Spanish Mortgage Association (*) Data of 2007 corresponds to July INCREASE IN TOTAL OUTSTANDING JULY 2007: 18,8%

Data of 2007 corresponds to July INCREASE IN TOTAL OUTSTANDING JULY 2007: 18,8%")

26

http://www.ahe.es NUMBER OF MORTGAGE LOANS PROVIDED SINCE 1995 Source: Bank of Spain and AHE 1.7 1.6 million mortg.

27

http://www.ahe.es EVOLUTION OF HOUSING PRICES IN SPAIN Source: Ministerio de Vivienda

28

http://www.ahe.es PROSPECTS 2007 Positive evolution on households’ income and employment and Demographics and Foreign Investment MODERATION OF DEMAND and gradual PRICE ADJUSMENT GROWTH MORTGAGE LENDING OUTSTANDING IN 2007: 14% GROWTH IN HOUSE PRICES (approx 3%) DESPITE Increasing path of real mortgage interest rates

DESPITE Increasing path of real mortgage interest rates")

29

http://www.ahe.es Source: AHE, Bank of Spain and INE. (Data for 2007 estimated for the 3th quarter) HOUSEHOLDS’ AVERAGE MORTGAGE DEBT-SERVICE ANNUAL COST

HOUSEHOLDS’ AVERAGE MORTGAGE DEBT-SERVICE ANNUAL COST.")

30

http://www.ahe.es Mortgage delinquency rates Percentage of outstanding amount of loans Source: OCDE Note: Loans refer to mortgages for all countries except Finland and Italy where they include all loans to the households sector. For Italy, they refer to new bad debts during the year as a percentage of outstanding loans.

31

http://www.ahe.es WEAK POSITION IN EUROPE WITH REGARDS: INNOVATION– NEW PRODUCTS – TYPE OF BORROWERS TYPE OF BORROWER AND PURPOSE RANGE OF PRODUCTS Source: “Study on the Financial Integration of Mortgage Markets” EMF and Mercer Oliver Wyman WEAK POINTS OF THE CURRENT MODEL

32

http://www.ahe.es WEAK POINTS OF THE CURRENT MODEL Since 1994 INTEREST RATE: VARIABLE RATE (30% -> -> 98,25%) REFERENCED: EURIBOR 12 MONTHS VARIABILITY: 6-12 MONTHS ATYPICAL PROFILE IN EUROPE

REFERENCED: EURIBOR 12 MONTHS VARIABILITY: 6-12 MONTHS ATYPICAL PROFILE IN EUROPE")

33

http://www.ahe.es Share of adjustable-rate in housing loans Per cent Source: European Mortgage Federation and OECD

34

http://www.ahe.es FUTURE LAW OF MODERNISATION OF MORTGAGE MARKET To expand mortgage product completeness To promote portfolio transfers To fine-tune regulation on mortgage funding instruments. To promote the development of equity release products. Regulation on Reverse Mortgage To enhance Valuation Companies independence

Similar presentations