Download presentation

Presentation is loading. Please wait.

1

Han Yang, Tianbai Wang, Honglu Liu, and Rui (Cindy) Deng April 12, 2012 Molycorp (MCP)

Deng April 12, 2012 Molycorp (MCP)")

2

Rare earth elements consisted 17 chemical elements – fifteen lanthanides, plus scandium and yttrium Source: http://ilookchina.net/tag/rare-earth-minerals/

3

Rare earths are moderately abundant in the earth’s crust, some even more abundant than copper, lead, and gold REEs are not concentrated enough to make them easily exploitable economically

4

Rare earths are critical inputs in many existing and emerging applications including: Clean energy technologies hybrid and electric vehicles and wind power turbines High-tech uses fiber optics, lasers and hard disk drives Defense applications guidance and control systems and global positioning systems Advanced water treatment technology industrial, military and outdoor recreation applications

5

China owns more than 50% of the rare earth reserves in the world and produce about 97% of rare earth in 2010. The total production in china is approximately 130,000 tons in 2010 The US does not produce rare earth and 93% of rare earth is imported from China

7

China has tightened its exported by reducing the export quota for both economic and environmental reasons The export quota has reduced from 60,000 tons/ year in 2007 to 30,000 tons/year in 2011 The export quota is expected to remain at current level Regulation increased to reduce the illegal exporting

8

Source: Economists

9

World demand for rare earth elements is estimated at 136,000 tons per year World demand is projected to rise to 185,000 tons annually by 2015 China’s output by 2015 is estimated between 130,000-140,000 tons and China’s demand would rise to 111,000 tons. Non-China annual output would need to be between 45,000 to 70,000 tons to meet global demand. There is potential shortfall.

10

Molycorp, Inc. is the only rare earth oxide (REO) producer in the Western hemisphere. It owns and operates the world’s largest, most fully developed rare earth mine and oxide manufacturing facility outside of China, located in Mountain Pass, California. It has been producing rare earth products for more than 59 years.

11

Global demand for rare earth elements (REEs) is projected to steadily increase due to Continuing growth in existing applications Increased innovation and development of new end uses

is projected to steadily increase due to Continuing growth in existing applications Increased innovation and development of new end uses")

12

Holder NameAmount held% Outstanding RESOURCE CAPITAL FUNDS13,843,86316.5 MOLIBDENOS Y METALES S A12,500,00014.9 MORGAN STANLEY INVEST MGMT8,647,56610.3 PEGASUS PARTNERS IV LP7,970,0739.5 Total42,961,50251.2 Ownership Source: Bloomberg

13

Molycorp Mountain Pass in Mountain Pass, California Molycorp Tolleson in Tolleson, Arizona Molycorp Sillamae in Sillamae, Estonia Three operating facilities

14

Data Source: MCP Website

15

Phase 1 To produce at an annual rate of 19,050 metric tons of rare earth oxides by the end of the third quarter of 2012. Phase 2 To give an annual production capacity of 40,000 metric tons of rare earth oxides per year by the end of 2012. Project Phoenix (two expansion phases) Modernizing and expanding the rare earth mine, mill, and rare earth oxide manufacturing facility at Mountain Pass

Modernizing and expanding the rare earth mine, mill, and rare earth oxide manufacturing facility at Mountain Pass.")

16

Data Source: MCP Website

17

“Mine-to-Magnets” Strategy Vertical integration strategy Ensure MCP can produce high quality rare earth materials in all five stages of the rare earth value chain Data Source: MCP Website

18

Mining Stage 1 Molycorp Mountain Pass Material Processing Stage 2 Molycorp Mountain Pass Molycorp Sillamae Metal Making Stage 3 Molycorp Sillamae Molycorp Tolleson Alloy Manufacture Stage 4 Molycorp Tolleson Magnet Manufacture Stage 5 Molycorp in joint venture with Daido Steel and Mitsubishi Corp. to manufacture NdFeB magnets “Mine-to-Magnets” Strategy

19

200920102011 Profitability ROA% -29.27%-10.59%9.43% ROE% -38.31%-11.37%14.00% Margin Analysis Gross Margin% -207.13%-6.92%55.17% SG&A Margin% 178.84%135.15%16.23% EBIT Margin% -402.85%-145.57%38.52% NI Margin% -403.03%-144.42%29.82%

20

200920102011 Asset Turnover Total Asset Turnover 0.07 0.32 Inventory Turnover 0.831.873.54 A/R Turnover 5.812.145.61 Liquidity Total Debt/Total Equity 0.00%0.64%0.07% Cash Ratio 0.7315.282.34 Quick Ratio 0.8616.072.74 Current Ratio 1.9417.063.58

22

Current P/E Ratio: 25.00 Graham : g = 8.25 GreenBlatt : EBIT/Tangible Assets = 25.94% EBIT/EV = 6.02% PEG Ratio : 0.79

23

Valuation: Methods Valuation P/E MultipleDCF Model

24

P/E Multiple: Comparable Companies US Domestic International Same BusinessSimilar Business Molycorp LYC AVL ARU RIO BHP MLM

25

P/E Multiple: Comparable Companies Lynas Corporation Ltd. (Yahoo: LYC.AX) Avalon Rare Metal Inc. (Yahoo: AVL.TO) Arafura Resources Ltd. (Yahoo: ARU.AX) International + Same Business

Avalon Rare Metal Inc. (Yahoo: AVL.TO) Arafura Resources Ltd. (Yahoo: ARU.AX) International + Same Business.")

26

P/E Multiple: Equivalent P/E Market Data Center, Wall Street Journal Equivalent P/E = Original P/E x US Market P/E AUS Market P/E Example: Lynas is an Australian Company. Based on S&P/AUX 200: 13.4 1 2 1 Based on S&P 500: 16.3 Share Market Report, Reserve Bank of Australia 2 Data Source:

27

P/E Multiple: Comparable Companies Lynas Coporation Ltd. (Yahoo: LYC.AX) Avalon Rare Metal Inc. (Yahoo: AVL.TO) Arafura Resources Ltd. (Yahoo: ARU.AX) International + Same Business Negative EPS

Avalon Rare Metal Inc. (Yahoo: AVL.TO) Arafura Resources Ltd. (Yahoo: ARU.AX) International + Same Business Negative EPS.")

28

P/E Multiple: Comparable Companies Rio Tinto plc (NYSE: RIO) BHP Billiton Ltd. (NYSE: BHP) Martin Marietta Materials Inc. (NYSE: MLM) US Domestic + Similar Business 12.54 17.62 48.99 P/E (ttm) Average $ 33.5 Molycorp EPS$ 1.27 26.4 Valuation: Price Per Share Current Market Price (Apr 11, 2012) Data Source: Yahoo! Finance $ 31.68

Martin Marietta Materials Inc. (NYSE: MLM) US Domestic + Similar Business P/E (ttm) Average $ 33.5 Molycorp EPS$ Valuation: Price Per Share Current Market Price (Apr 11, 2012) Data Source: Yahoo. Finance $")

29

DCF Model: Framework DCF Model Discount Rate = 15.6%Financial Projection WACC + 400bp = 15.6%ROE $ 79.16 $ 23.15 $ 31.68 52 week range X $ 30 Price Per Share Data Source: Yahoo! Finance $ 31.68Mkt. 11.6%

30

Historical and Projected CAPEX, 2008-2022 (Dollar Amount in Millions) DCF Model: CAPEX Projection Data Source: Annual Reports and Students Analysis Internal Financing By the end of FY 2011: Cash & Cash Equiv. = $ 419 mil. Additional $ 213 mil. Needed.

31

Historical and Projected Revenue, 2008-2022 (Dollar Amount in Millions) DCF Model: Revenue Projection Data Source: Annual Reports and Students Analysis

DCF Model: Revenue Projection Data Source: Annual Reports and Students Analysis")

32

Han personally owns 110 shares of MCP. And he will not change the position in next 12 months.

33

DCF Model: Sensitivity Analysis Revenue = P X Q By 2012 Q3: 20,000 mt (Capacity) By 2012 Year-End: 40,000 mt (Capacity) 2011 : 5,000 mt (Real) Production

By 2012 Year-End: 40,000 mt (Capacity) 2011 : 5,000 mt (Real) Production")

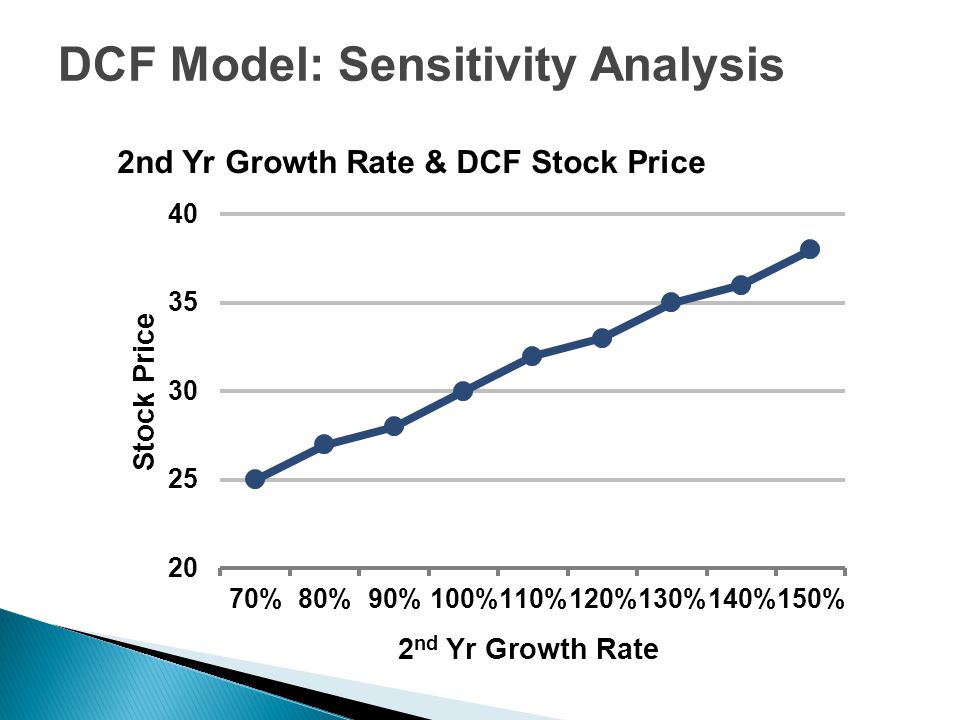

34

DCF Model: Sensitivity Analysis

38

Recommendation Buy 200 Shares At Market Price Cost = 200 x 30 = $ 6,000 2% of Our Portfolio

Similar presentations

NYSE Recommendation: BUY Price (10/3/14): $21.55.>")

Stock Price 55.62 Market Capitalization 8.7B Beta1.64 EPS 7.02 DPS 0.6 P/E 6.3% Dividend Yield 1.1% Dividend Payout Ratio.>")

. Industry Overview 2 Gold mining is capital intensive Capital is very expensive for small exploration and production.>")

>")

are 17 elements within the periodic table which, contrary to their.>")