Download presentation

Presentation is loading. Please wait.

1

Applying Stochastic Programs to Improve Investor Performance Professor John M. Mulvey Bendheim Center for Finance Department of Operations Research & Financial Engineering Princeton University Senior Consultant: Towers Perrin–Tillinghast, Mt. Lucas Management Hedge Fund, Rydex Investments June 27, 2007

2

Outline 1. Advanced Portfolio Theory Alternative optimization frameworks Success stories Advantages of multi-period portfolio models Optimize overlay strategies in a global hedge fund Novel sources for diversification (momentum?) 2.Optimize Pension Trust and Sponsoring Company Status of pension trusts in U.S. ALM model equations Hybrid approach Link stochastic program policy simulator 3.Future Research 1.Active managers and momentum strategies 2.Other issues

2.Optimize Pension Trust and Sponsoring Company Status of pension trusts in U.S. ALM model equations Hybrid approach Link stochastic program policy simulator 3.Future Research 1.Active managers and momentum strategies 2.Other issues.")

3

Alternative Frameworks for Optimization A. Dynamic stochastic control Discretize state space Solve via dynamic program B. Multi-stage stochastic program Discretize uncertainties (scenario tree) C. Policy simulation (with optimization) Given a policy rule (s) Apply across scenarios via Monte Carlo simulation D. Hybrid strategies Stylized stochastic program (discover sound rules) Evaluate in a comprehensive policy simulator

C. Policy simulation (with optimization) Given a policy rule (s) Apply across scenarios via Monte Carlo simulation D. Hybrid strategies Stylized stochastic program (discover sound rules) Evaluate in a comprehensive policy simulator.")

4

Success Stories: Leading U.S. University Endowments Harvard ($29b), Yale ($18b), Princeton ($13b) 16-22 % annual return over past decade How? –Stress private markets (e.g. private equity, venture capital, hedge funds) –Wide diversification Novel asset classes (timber, tips, structured products) Uncorrelated return patterns (when possible) Employ leverage with careful risk management Reference: David Swensen Pioneering Portfolio Management, Free Press, 2000, CIO-Yale U.

, Yale ($18b), Princeton ($13b) % annual return over past decade How. –Stress private markets (e.g. private equity, venture capital, hedge funds) –Wide diversification Novel asset classes (timber, tips, structured products) Uncorrelated return patterns (when possible) Employ leverage with careful risk management Reference: David Swensen Pioneering Portfolio Management, Free Press, 2000, CIO-Yale U..")

5

Princeton Policy Portfolio (2005)

")

6

Success Stories: Global (Re) Insurance Companies Enterprise risk management (ERM/DFA) –AXA (Paris) –Renaissance Reinsurance (Bermuda) –Geo Vera (California and Florida) How? –Add new insurance activities to gain diversification benefits and increased profit (higher returns and reduced risks) –Search for businesses across the global wide diversification Lower capital requirement due to reduced loss tail Greater profits

–Search for businesses across the global wide diversification Lower capital requirement due to reduced loss tail Greater profits.")

7

Success Stories: Defined Benefit Pension Trusts (few and far between) Goal: Maintain fund surplus and grow assets with superior performance Example: Kodak Pension Plan (School of Hard Knocks, R. Olson) How? Discover assets with relatively high volatility and good performance during economic downturns -strips (zero coupon government bonds) Rebalance portfolio to achieve rebalancing gains Advanced concept – apply overlay strategies

How. Discover assets with relatively high volatility and good performance during economic downturns -strips (zero coupon government bonds) Rebalance portfolio to achieve rebalancing gains Advanced concept – apply overlay strategies.")

8

Why Dynamic (Multi-Period) Portfolio Models? (J. of Portfolio Management, Winter 2003, Summer 2004) Advantages Greater realism (transaction costs, contribution, borrowing) Addresses temporal issues (short vs. long horizons) Greater performance (rebalancing gains)

Advantages Greater realism (transaction costs, contribution, borrowing) Addresses temporal issues (short vs. long horizons) Greater performance (rebalancing gains).")

9

9 Dynamic Diversification Given assets with identical growth =15%/year and volatility = 20%, independent Combine ten assets (equal weights, rebalanced monthly) 1.Total portfolio return = 15% + 1.8% (excess rebalancing gains) 2.If Vol = 40% portfolio return = 15 + 7.2% 3.If Vol = 60% portfolio return = 15 + 16.2% Luenberger (1998) “Volatility is not the same as risk. Volatility is an opportunity.”

10

10 The Rebalancing Decision Initial investment mix 50% Nikkei, 50% Bonds Equity up Equity down 65% Nikkei, 35% Bonds 45% Nikkei, 55% Bonds 6 Months Option: to sell and purchase assets back to original mix? What should be done? Active Rebalancing

11

Durable Policy Rule: Fixed Mix Target mix each period = i = % of wealth in asset i, each period Example: 70% stock, and 30% government bonds (70/30) Active rebalancing each period (e.g. monthly) Address Transaction and market impact costs No-trade-zone: Fixed-Mix Optimization requires Non- convex Solver (or approximation NLP)

Address Transaction and market impact costs No-trade-zone: Fixed-Mix Optimization requires Non- convex Solver (or approximation NLP).")

12

12 Simple Example A: Enhance Performance Typical target portfolio: –70% Equity –30% bonds –How to Improve? Traditional approach – adjust equity/bond mix depending upon forecast (say due to interest rate, volatility, or other triggers) Add diversifying assets –Additional equity markets, bond categories, real estate, etc. Overlay strategy via futures contracts »Trend following »Go long or short based on position relative to moving average Rebalance regularly to get volatility pumping

Add diversifying assets –Additional equity markets, bond categories, real estate, etc. Overlay strategy via futures contracts »Trend following »Go long or short based on position relative to moving average Rebalance regularly to get volatility pumping.")

13

Historical Returns of Asset Classes

14

Advantages of Wide Diversification

15

Example B: Enhance Performance by Non Traditional Strategies Core portfolio: –70% U. S. Equity –30% U. S. Government bonds –Geometric returns = 9.73% (1991 to 2005) –How to Improve? Traditional approach – adjust equity/bond mix depending upon forecast on scenario tree (stochastic program) Non-traditional approach – add overlay strategy via futures contracts –Trend following –Go long or short based on position relative to moving average »(rebalance each month)

–How to Improve. Traditional approach – adjust equity/bond mix depending upon forecast on scenario tree (stochastic program) Non-traditional approach – add overlay strategy via futures contracts –Trend following –Go long or short based on position relative to moving average »(rebalance each month).")

16

Commodities and Inflation Do Commodity Prices Always Rise?

17

Why trend follow? Wheat Price Chart 09/1990 – 08/2004

18

MLM Index provides Diversification and Equity like Returns

19

19 Results of Wide Diversification and Overlay Strategy

20

The Fixed-Mix Rule and an Equity Momentum Strategy (a) The dynamic diversification strategy is –a fixed mix portfolio of –long-only industry-level momentum strategies with various parameters (evaluation period, holding period) –across five markets that cover the most of the world stock market (US, EU, Europe ex. EU, Japan, Asia ex. Japan). Over the last 27 years (1980~2006), the performance of the dynamic diversification strategy has been outstanding.

. Over the last 27 years (1980~2006), the performance of the dynamic diversification strategy has been outstanding..")

21

Portfolio of Equity Momentum Strategies (b)

")

22

The Fixed-Mix Rule and Equity Momentum Strategies (c)

")

23

Actively Managed Funds and the Momentum Strategies (a) Many actively managed funds have become highly correlated with the momentum strategy after 1992. A considerable amount of the active funds seem to be adopting the momentum strategy as their stock selection rules, although a deep style analysis is required to conclude so. Interestingly, the similarity to the momentum strategy is proportionate to fund performance. Even for the value-oriented funds, which are not supposed to employ aggressive strategies as the momentum strategy, the best performance group has shown similar return patterns as the momentum strategy during the last decade. Trivia: The key paper on the momentum strategy by Jegadeesh and Titman, “Returns to buying winners and selling losers: implications for stock market efficiency”, was published on 1993!

24

Actively Managed Funds and the Momentum Strategies (b) Table 1. Correlations of the Excess Returns of the Large-Cap Active Funds and the Momentum Strategies Fund Style Large Core Large Growth Large Value All Large-Cap Entire Sample Period (1987~2006) 0.3170.4680.1520.468 1987~1991-0.0730.0410.1180.061 1992~19960.3020.534-0.1170.320 1997~20010.4550.6280.3020.702 2002~20060.5220.5620.1060.563

~ ~ ~ ~")

25

Actively Managed Funds and the Momentum Strategies (c) Table 2. Correlations of the Excess Returns of the Momentum Strategy and the All Large-Cap Funds in Different Performance Levels Performance Ranking (Based on Excess Returns) 1st2nd3rd4th Entire Sample Period (1987~2006) 0.3930.4540.3500.203 1987~19910.134-0.033-0.0430.061 1992~19960.2820.3130.2530.384 1997~20010.7670.6550.4430.621 2002~20060.5800.4470.4830.442

1st2nd3rd4th Entire Sample Period (1987~2006) ~ ~ ~ ~")

26

Actively Managed Funds and the Momentum Strategies (d) Table 3. Correlations of the Excess Returns of the Momentum Strategy and the Large-Growth Funds in Different Performance Levels Performance Ranking (Based on Excess Returns) 1st2nd3rd4th Entire Sample Period (1987~2006) 0.4950.4540.3670.193 1987~19910.0460.0420.133-0.172 1992~19960.5150.4940.4330.502 1997~20010.7500.5550.4780.476 2002~20060.6340.5270.4920.377

1st2nd3rd4th Entire Sample Period (1987~2006) ~ ~ ~ ~")

27

Actively Managed Funds and the Momentum Strategies (e) Table 4. Correlations of the Excess Returns of the Momentum Strategy and the Large-Core Funds in Different Performance Levels Performance Ranking (Based on Excess Returns) 1st2nd3rd4th Entire Sample Period (1987~2006) 0.2300.3630.2320.063 1987~19910.1260.113-0.185-0.205 1992~19960.4220.3150.2560.198 1997~20010.5090.3410.3380.286 2002~20060.6670.5030.1610.014

1st2nd3rd4th Entire Sample Period (1987~2006) ~ ~ ~ ~")

28

Actively Managed Funds and the Momentum Strategies (f) Table 5. Correlations of the Excess Returns of the Momentum Strategy and the Large-Value Funds in Different Performance Levels Performance Ranking (Based on Excess Returns) 1st2nd3rd4th Entire Sample Period (1987~2006) 0.1630.1120.003-0.057 1987~1991-0.0240.1640.0060.167 1992~19960.036-0.082-0.205-0.259 1997~20010.3790.2980.3120.133 2002~20060.5100.186-0.077-0.332

1st2nd3rd4th Entire Sample Period (1987~2006) ~ ~ ~ ~")

29

2. Pension Trusts: ALM Issues Pension planning in the US –Defined benefit vs. Defined contribution S&P 500 DB Pension Plans (Dec 1999 May 2003) –Net surplus of $239 bn Net deficit of $252 bn Three primary causes –decline in equity markets decrease in pension plan assets –decrease in interest rates increase in pension liabilities –poor planning ASSETSASSETS LIABLIAB Surplus

–Net surplus of $239 bn Net deficit of $252 bn Three primary causes –decline in equity markets decrease in pension plan assets –decrease in interest rates increase in pension liabilities –poor planning ASSETSASSETS LIABLIAB Surplus.")

30

Pension Trust Stakeholders ( Defined Benefit – DB) Sponsoring company Pension System (A-L or A/L) contributions Pay retirees PBGC The public

Sponsoring company Pension System (A-L or A/L) contributions Pay retirees PBGC The public")

31

Status of Industries in S&P500

32

Optimize Assets and Liabilities/Goals Investors seek to maximize the growth of their wealth (capital) -- optimal asset allocation Financial organizations manage their products (banks, insurance companies) Assets (i) Products (liabilities, j)

-- optimal asset allocation Financial organizations manage their products (banks, insurance companies) Assets (i) Products (liabilities, j)")

33

Modeling Preliminaries Decisions: asset mix (proportions of equity, bonds, etc.) Contributions (from investors or outsiders) Payment policy (how much to pay and to whom) Uncertainties: Returns on assets Amount and timing of future cashflows Length of the horizon (insurance or pensions) Key Decision Variables: x(i, t, s) amount invested in asset i, time t, scenario s y(j,t,s) amount of liability or business activity

Contributions (from investors or outsiders) Payment policy (how much to pay and to whom) Uncertainties: Returns on assets Amount and timing of future cashflows Length of the horizon (insurance or pensions) Key Decision Variables: x(i, t, s) amount invested in asset i, time t, scenario s y(j,t,s) amount of liability or business activity")

34

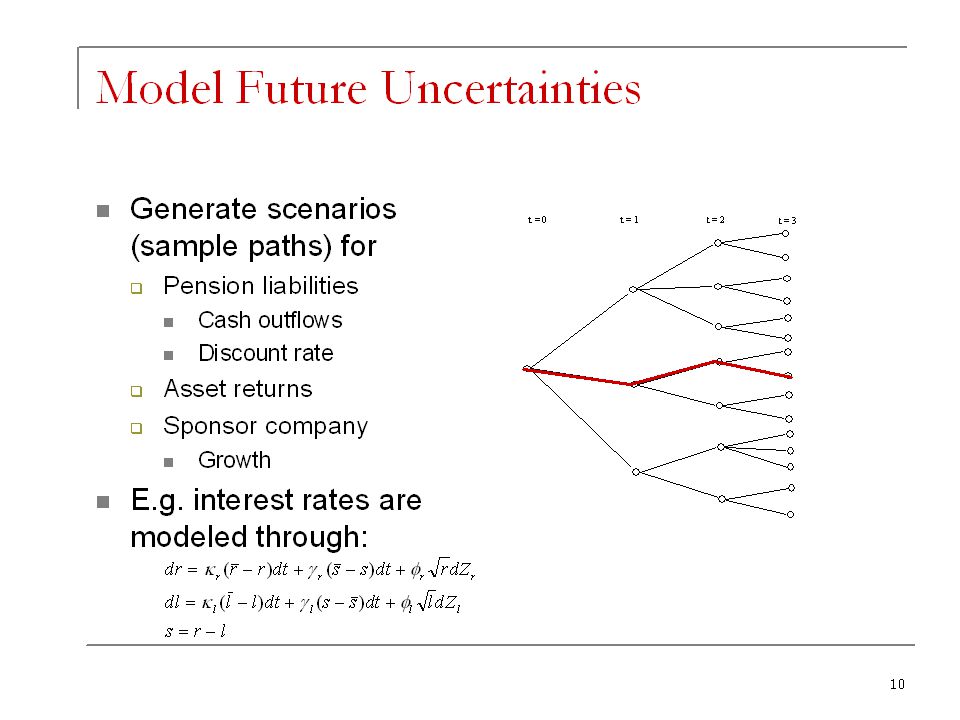

34 Structure of Multi Stage Portfolio Models: Developing an Investment Policy Project state of enterprise across multi-period horizon –Decisions at beginning each stage –Uncertainties occur between decision points –Policy rules or model recommendations guide system –Iterate over all scenarios {S} 1234...T time Horizon Decisions

36

36 Currencies Real Yields Stock Dividend Growth Rate Dividend Yields Fixed Income Returns Stock Returns Other Asset Classes General Price Inflation Treasury Yield Curve Expected Inflation Wage Inflation CAP:Link : Cascade of Stochastic Processes

37

Fundamental Asset Equations (for every scenario) cash asset j purchasessales

cash asset j purchasessales")

38

Integrated Framework

39

Anticipatory Integrated Corporate/Pension Planning Model i=1 i=2 i=M i=1 i=2 i=M i=1 i=2 i=M CP Company Pension Plan t=1t=2t=T cash

40

The Integrated Pension-Corporate Financial Planning Problem as a Multi-stage Stochastic Program

41

Model Structure The integrated pension and corporate financial planning problem as a multi-stage stochastic program.

42

42 Empirical Analysis to Assist Pensions Regain Financial Health

43

Optimization Model for U.S. Department of Labor (Multi-stage stochastic program ) 3343111380178217260Solve Time (seconds) MinCompromiseMaxMinCompromiseMax Point on the efficient frontier 385,00077, 000 Number of constraints 340,00068, 000Number of variables 5000-Scenario Tree1000-Scenario Tree * Solver: CPLEX Algorithms: Dual Simplex for LP and QP Barrier

Solve Time (seconds) MinCompromiseMaxMinCompromiseMax Point on the efficient frontier 385,00077, 000 Number of constraints 340,00068, 000Number of variables 5000-Scenario Tree1000-Scenario Tree * Solver: CPLEX Algorithms: Dual Simplex for LP and QP Barrier.")

44

Analysis of DB Pension System in S&P 500 Consumer Discretionary Telecom. Services Industrials (ex GE) Funded Ratio 73%95%82% Industry Market Cap 2.93.5 Pension Assets Projected Expected Return 9.6%5.4%9.2% Correlation with S&P 500 88.5%84.4%90.5% 1.Identify industries with potential problems 2.Evaluate pension funding and investment decisions 3.Current conditions and simulation inputs:

Funded Ratio 73%95%82% Industry Market Cap Pension Assets Projected Expected Return 9.6%5.4%9.2% Correlation with S&P %84.4%90.5% 1.Identify industries with potential problems 2.Evaluate pension funding and investment decisions 3.Current conditions and simulation inputs:.")

45

Analysis of DB Pension System in S&P 500: Pockets of Severe Difficulty

46

Linking Stochastic Program and Policy Simulator Model Uncertainties Calibrate and Sample Stochastic Program Policy simulator Set out benchmarks Explore improved policy rules Scenario Tree Scenarios Complex details

47

Refine Policy Rules For Target Industries Stochastic Program Recommendations under Adverse Conditions New Policy Rules ExamineDesign Policy Simulator Test Improved Policy Rules

48

Refine Policy Rules For Telecom Services

49

Policy Rules For Telecom Services Switching investment strategies under adverse conditions: 1. Reduces excessive contributions considerably: - on average: dropping from $5 billion to $3.5 billion - worst case: from $10.6 billion to $7.5 billion 2. Maintains or improves all other objectives. 3.Much better results than alternatives (CPPI, etc.)

.")

50

Recommendations for DB Pension Trusts in U.S. Encourage healthy companies to remain in the DB system –Keep expected costs reasonable –Allow smoothing, if risk is deemed safe (for large companies) Regulatory oversight –Anticipating failures without placing too much burden of existing system (conditional regulations) Pay attention to companies with large ratios of pension assets to market capitalization Increase performance – wide diversification, leverage, and private investments

Regulatory oversight –Anticipating failures without placing too much burden of existing system (conditional regulations) Pay attention to companies with large ratios of pension assets to market capitalization Increase performance – wide diversification, leverage, and private investments.")

51

51 3. Future Research Create new assets/securities –Returns linked to novel factors (other than economy, interest rates, risk premium) –Futures markets for real estate, weather, etc. Formal method for discovering sound policy rules –From stochastic control and stochastic programs Faster computers/algorithms (naturally) Challenges –Many users are unfamiliar with dynamic models –Most regulators are similarly handicapped

–Futures markets for real estate, weather, etc. Formal method for discovering sound policy rules –From stochastic control and stochastic programs Faster computers/algorithms (naturally) Challenges –Many users are unfamiliar with dynamic models –Most regulators are similarly handicapped.")

52

52 Selected References Mulvey, J. M. (and PU doctoral students) “Modernizing the Defined-Benefit Pension System, J. of Portfolio Management, Winter 2005. “Improving Investment Performance for Pension Plans,” 2006. J. of Asset Management, 2006. “Improving Performance for Long-Term Investors: Wide Diversification, Leverage, and Overlay Strategies,” Quantitative Finance, April 2007. "Dynamic Financial Analysis for Multinational Insurance Companies” Chapter in Applications of Stochastic Programs,” (eds. Zenios and Ziemba), Volume 2, 2007. Luenberger, D. Investment Science, Oxford University Press, 1998. Swensen, D. Pioneering Portfolio Management, The Free Press, 2000. Ziemba, W.T. and Mulvey J.M., (eds.), Worldwide Asset and Liability Modeling, Cambridge University Press, November 1998.

Modernizing the Defined-Benefit Pension System, J. of Portfolio Management, Winter Improving Investment Performance for Pension Plans, J. of Asset Management, Improving Performance for Long-Term Investors: Wide Diversification, Leverage, and Overlay Strategies, Quantitative Finance, April Dynamic Financial Analysis for Multinational Insurance Companies Chapter in Applications of Stochastic Programs, (eds. Zenios and Ziemba), Volume 2, Luenberger, D. Investment Science, Oxford University Press, Swensen, D. Pioneering Portfolio Management, The Free Press, Ziemba, W.T. and Mulvey J.M., (eds.), Worldwide Asset and Liability Modeling, Cambridge University Press, November")

Similar presentations

2001 Contemporary Engineering Economics 1 Chapter 6 Principles of Investing Investing in Financial Assets Investment Strategies Investing in Stocks.>")