Download presentation

Presentation is loading. Please wait.

1

Law and Economic Development in China: The Case of Stock Market Growth Dr. Zhong Zhang School of East Asian Studies University of Sheffield

2

Outline Introduction The growth history of China’s stock market Legal developments The role of law in the growth The causality between law and market growth Causes for market growth Conclusion

3

Introduction Law and economic development – Optimists: Personal security; law and order; incentive for wealth creation (property law); facilitating commerce (contract law); limiting government power and bureaucracy; controlling corruption – Sceptics: What is the rule of law? which components are important than the others? Inconsistent empirical evidence The direction of causality Informal institutions Failure to promote the rule of law

4

Introduction The experience of China – Sceptics “Little explanatory power” “An important counterexample” “Because of weak law” – Optimists Progress in the rule of law Stages of economic development “Middle income trap” Strengthening the rule of law to sustain economic growth

5

Introduction The stock market of China

6

Introduction

8

Questions – Is China a counterexample? Are investors not concerned that their investment might be lost? – Is growth sustainable if law remains weak? – What cause/impede the improvement of law? – What can the experience tell about law and economic development in China in general?

9

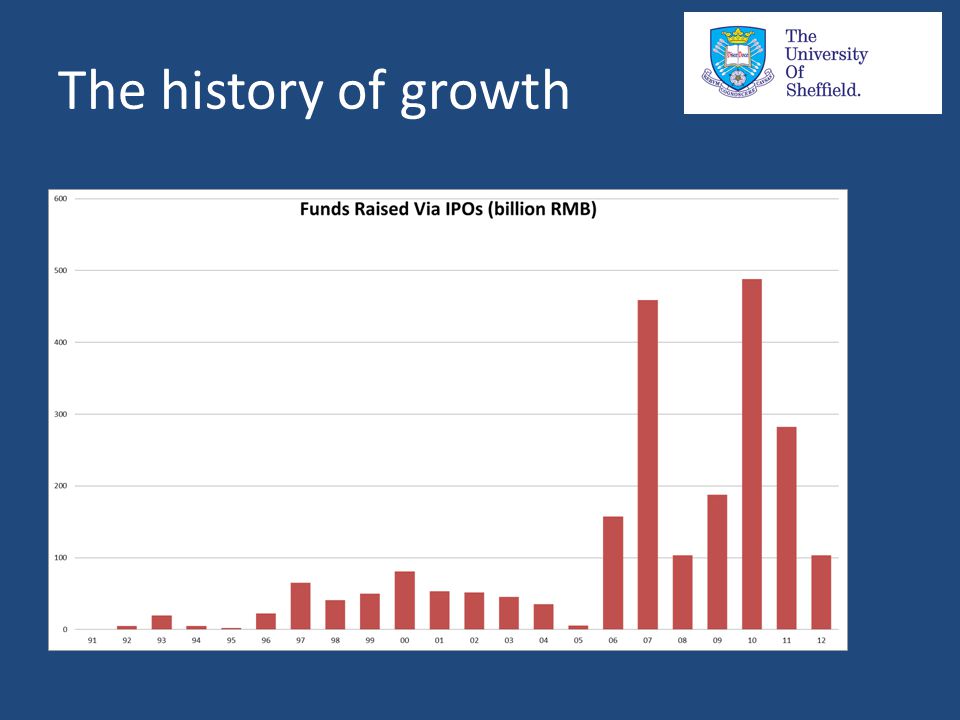

The history of growth Before 90: emergence of shareholding system and establishing the stock exchanges 1st stage (90/01): rapid growth 2nd stage (01/05): stock market in crisis 3rd stage (06/09): boom, bust, stimulation 4th stage (10/14): prolonged bear market

: rapid growth 2nd stage (01/05): stock market in crisis 3rd stage (06/09): boom, bust, stimulation 4th stage (10/14): prolonged bear market")

10

The history of growth Stages of growth

11

The history of growth

13

Legal development Before 1993: no national legislation; rudimentary local operational rules; no specialized regulator; 1993/2000: establishing the legal and regulatory framework – Regulatory framework 1992: CSRC 1997: CSRC taking over control of the stock exchanges 1999: centralisation and specialisation – Major legislations: Company Law 1993; Provisional Regulations on Issuing and Trading Shares 1993; Securities Law 1998; Regulations on Stock exchanges 1996; criminal legislation (1995, 1997, 1999) 2001-: improvements – Legislation: CG Code 2001; Independent director 2001; company law 2005; securities law 2005; criminal legislation 2005; Special regulations for minority shareholder protection 2004 – Enforcement: Inputs and outputs

2001-: improvements – Legislation: CG Code 2001; Independent director 2001; company law 2005; securities law 2005; criminal legislation 2005; Special regulations for minority shareholder protection 2004 – Enforcement: Inputs and outputs")

14

The role of law The first stage: irrelevant – Rudimentary, in the process of establishment – Enforcement: few activities – Lawlessness: misappropriating corporate funds (737/1287); false disclosure (72%), stock manipulation (80%) – “worse than a casino”; “a notoriously corrupt place” Why growth when law extraordinarily weak? – Behavioral explanation: bounded rationality – Time lag – Government bailouts – Lack of alternative investment opportunities

15

The role of law The second stage (01/05): stock market in crisis – Macro economy in best shape – Market performance: indices lost more than half; market cap/GDP: 48%-18%; investor withdrawal (30%); IPO suspensions; the securities industry: in red for 4 years – Bitter debates: “worse than a casino”; “scrap the old and build a new one from scratch” Why the crisis? – Bubble: P/E > 55 – Corporate profitability: loss-making companies (19%); ROE: 14.68%-5.35% – Frauds (market manipulation, misappropriation, false disclosure) and scandals: widespread (212); outrageous Weak law and the crisis – Weak law and corporate profitability – Weak law and frauds

; ROE: 14.68%-5.35% – Frauds (market manipulation, misappropriation, false disclosure) and scandals: widespread (212); outrageous Weak law and the crisis – Weak law and corporate profitability – Weak law and frauds.")

16

The role of law The third stage (06/09): market revival – The improvement of law: Crisis-forced Legislations Investor protection indices: ADI: 3-5; ASDI: 0.76; SPI: 6th/20 Enforcement – Inputs: new enforcement units and branches; personnel: 32-600 – Outputs: enforcement actions from single figure to over 100 A degree of law and order: traditional market manipulation; misappropriation; false disclosure; insider trading “The most transparent and efficient market with the highest degree of rule of law in China” – Market revival and the improvement of law

: market revival – The improvement of law: Crisis-forced Legislations Investor protection indices: ADI: 3-5; ASDI: 0.76; SPI: 6th/20 Enforcement – Inputs: new enforcement units and branches; personnel: – Outputs: enforcement actions from single figure to over 100 A degree of law and order: traditional market manipulation; misappropriation; false disclosure; insider trading The most transparent and efficient market with the highest degree of rule of law in China – Market revival and the improvement of law")

17

The role of law The 4th stage (10/14): Prolonged bear market – Reasons Macro economy Poor investment return: dividend yield: 0.75%, lowest; (1- year deposit interest rate: 3.25%; risk-free rate of return: 5%) Why?: low corporate profitability: ROA 5.58%, lower than 1- year bank loan interest rate Weak law and low corporate profitability – The dominance of SOEs: 47%; 90%; 86%; 74% – Poor corporate governance of SOEs: corruption, waste, over- investment and mismanagement – Law is weak

: Prolonged bear market – Reasons Macro economy Poor investment return: dividend yield: 0.75%, lowest; (1- year deposit interest rate: 3.25%; risk-free rate of return: 5%) Why : low corporate profitability: ROA 5.58%, lower than 1- year bank loan interest rate Weak law and low corporate profitability – The dominance of SOEs: 47%; 90%; 86%; 74% – Poor corporate governance of SOEs: corruption, waste, over- investment and mismanagement – Law is weak")

18

The role of law Summary – Law was indeed insignificant in the first stage – But weak law eventually led to crisis – Market revived, after investor protection strengthened and a degree law and order established – Weak law: one reason for the post-2010 bear market The role of law: critical to sustaining market growth

19

Law and growth: The causality

20

Market growth/lack of it: The causes Liberalization: ideological, political and economic Economic growth: demand for and supply of capital Other factors – Alternative investment opportunities – SOE dominance – SOE monopoly/oligopoly: finance, mining, energy, telecommunication – Business environment: bureaucracy and cost (96th/189, 158th, 185th, 120th) – Lack of technology, brand names, innovation: Apple vs. Foxconn

21

Conclusion China is not a counter-example Bidirectional causal relation between law and market growth and law first followed by law But the virtuous circle of “growth-law-further growth” is not a guarantee The first-order causes: liberalisation and economic development Policy implications: political and economic liberalisation

22

Conclusion What can the experience of stock market development tell about law and economic development in general? – Law is necessary for sustaining economic growth – Law is a result of economic growth – But economic growth does not always lead to the improvement law – Ideological, political and economic liberalisation is fundamental

Similar presentations

Enrico Perotti Presentation by Gerard Hertig.>")

The SGM doesn’t fit facts too well Saving and Investment Don’t.>")

to a free.>")