Download presentation

Presentation is loading. Please wait.

1

Taxes October 22, 2014

2

“ In this world nothing can be said to be certain, except death and taxes. ” Benjamin Franklin, 1789

3

Pre-Tax Analysis

4

After-Tax Analysis

5

Pre-Tax and After Tax MARR The company wants an after-tax profit that gives a 20% rate of return on investment. So, must the pre-tax rate of return on investment be greater or less than 20%? Some portion of the pre-tax profit will be taken away in taxes: Profit pre = Profit after + taxes $ pre = $ pre (1-t) + $ pre t

+ $ pre t.")

6

Pre-Tax and After Tax MARR Therefore, our pre-tax MARR should be greater than our after-tax MARR. A good estimate for the pre-tax MARR would be MARR pre = MARR after /(1-t) where t is the tax rate.

where t is the tax rate..")

7

After-Tax Analysis Same as pre-tax analysis, except we use the after-tax MARR and adjust the cash flows to take account of the effects of taxation. Taxation has two main effects: Operating costs and incomes are affected by the tax rate (simple) Capital costs are affected by the tax rate and depreciation allowances (a bit complicated ) Details depend on the country we’re in.

Capital costs are affected by the tax rate and depreciation allowances (a bit complicated ) Details depend on the country we’re in..")

8

16.5

9

Capital Cost Allowance When a company buys a capital asset, it can’t deduct the cost of the purchase from its income. But it can deduct the subsequent annual depreciation of the asset from its income. The rules for how and how fast things depreciate vary from one country to another.

10

Clarification: What is a capital asset? YesNo

11

Clarification: What is a capital asset? YesNo

12

Example: A Placidian company buys a robot, which Placidian law allows them to depreciate by straight-line depreciation over five years. If the robot costs 45,000, and the company’s after-tax MARR is 12%, and if the tax rate is 42%, what is the present worth of the robot’s first cost?

13

The robot costs 45,000, it straight-line depreciates over five years, and the tax rate is 42%. Where does the annual 3,780 come from? So each year it depreciates by 9,000. We take this out of the pre-tax cash flow. If we hadn’t taken it out, we would have paid 9,000 × 0.42 = 3,780 taxes on this part of the cash flow.

14

So the after-tax present worth of the robot’s first cost is actually: PW first-cost = - 45,000 + 3,780(P/A,0.12,5) = - 31 400

=")

15

This is one part of an after-tax analysis. Let’s consider a more detailed example: The Placidian company will use the robot to reduce its operating costs by 23,000 a year. But the robot will require 7,300 to be spent on maintenance every year. After five years, it will be sold for salvage at a price of 5,000. What is the present worth of purchasing the robot and all the resultant cash flows? The excess of cost savings over maintenance costs is 15 700 a year. We assume this cash flow to occur at the end of each year of the 5-year life. It is taxed at 42%, so the after-tax cash flows are an annuity of: A = 15,700 × (1 – 0.42) = 9,106 So PW income = 9,106(P/A,0.12,5) = 32,800

= 9,106 So PW income = 9,106(P/A,0.12,5) = 32,800.")

16

The Placidian company will use the robot to reduce its operating costs by 23,000 a year. But the robot will require 7,300 to be spent on maintenance every year. After five years, it will be sold for salvage at a price of 5,000. What is the present worth of purchasing the robot and all the resultant cash flows? S = 5,000 × (1 – 0.42) = 2,900 So PW salvage = 2,900(P/F,0.12,5) = 1,646 Lastly, we have to deal with the salvage costs. In this case, the salvage value is income, so it gets taxed at 42%

= 2,900 So PW salvage = 2,900(P/F,0.12,5) = 1,646 Lastly, we have to deal with the salvage costs. In this case, the salvage value is income, so it gets taxed at 42%.")

17

The Placidian company will use the robot to reduce its operating costs by 23,000 a year. But the robot will require 7,300 to be spent on maintenance every year. After five years, it will be sold for salvage at a price of 5,000. What is the present worth of purchasing the robot and all the resultant cash flows? PW first-cost = -31,400 PW income = 32,800 PW salvage = 1,646 So, summarising, the after-tax present worth of the investment is: So the total after-tax present worth is 3,046 So they should buy the robot.

18

Corporate Tax Laws in Canada Property taxes Paid to local government, usually small compared with income taxes Excise Taxes Sales tax, GST, import taxes. Not that important Income taxes Most important. Levied by federal and provincial governments

19

Capital Gains Everything a company owns, except what is held primarily for sale to customers, is a capital asset. YESNO

20

Capital Gains A capital gain occurs when a capital asset is sold for more than its purchase price. Capital gains are usually taxed at a lower rate than ordinary income.

21

The general rate was reduced to 16.5% in 2011 It will go down to 15% in January 2012 The small business rate was reduced to 11% in January 2008. On top of this, add the provincial tax:

22

In BC, ``small’’ means less than $400 000 taxable annual income Province or territory Small bus. Higher rate Newfoundland and Labrador5% 14% Nova Scotia5%16% Prince Edward Island4.3%*16% New Brunswick5%13% Ontario5.5%14% Manitoba2%14% Saskatchewan4.5%13% British Columbia4.5%12% Yukon4%15% Northwest Territories4%11.5% Nunavut4%12%

23

Unlike Placidia, Canada does not allow companies to depreciate capital assets by straight-line depreciation.

24

What is this `pooled by class’ thing?

25

The `pooled by class’ thing:

26

Example: Yellow Cabs buys two taxis for $40,000 each. They are in Class 16, so they depreciate at 40% per year. So in the first year, there is $80,000 in the class, and so the first year depreciation is $80,000 × 0.4 = $32,000. * So the capital cost allowance for the first year is $32,000, and the undepreciated capital cost [`UCC’] at the beginning of the second year is $48,000. So Yellow Cabs saves $32,000t from their taxes in Year 1. * ignores first-year rule

27

Example: Yellow Cabs’s undepreciated capital cost [`UCC’] at the beginning of the second year is $48,000. Now they sell one of their cabs for $40,000. They now have an undepreciated capital cost of just $8,000 in the pool. During the year this depreciates by 40%, so they can claim a depreciation allowance of $3,200. This saves them $3,200t in taxes. They begin the third year with $4,800 in the class.

![Example: Yellow Cabs’s undepreciated capital cost [`UCC’] at the beginning of the second year is $48,000.](http://images.slideplayer.com/18/5678810/slides/slide_27.jpg "Now they sell one of their cabs for $40,000. They now have an undepreciated capital cost of just $8,000 in the pool. During the year this depreciates by 40%, so they can claim a depreciation allowance of $3,200. This saves them $3,200t in taxes. They begin the third year with $4,800 in the class..")

28

Example: Yellow Cabs’s undepreciated capital cost [`UCC’] at the beginning of the third year is $4,800. Now they sell the remaining cab for $40,000. What happens now? Yellow Cabs’s CCA class 16 is now empty. The company has a net income from the sale of $40,000 – $4,800 = $35,200 and pays taxes ($35,200t) on this income.

![Example: Yellow Cabs’s undepreciated capital cost [`UCC’] at the beginning of the third year is $4,800.](http://images.slideplayer.com/18/5678810/slides/slide_28.jpg "Now they sell the remaining cab for $40,000. What happens now. Yellow Cabs’s CCA class 16 is now empty. The company has a net income from the sale of $40,000 – $4,800 = $35,200 and pays taxes ($35,200t) on this income..")

29

The First-Year Rule Whenever in the year you buy an asset, at the end of the year you can claim the CCA on that asset’s depreciation over the entire year. So, when do you buy your assets?

30

The First-Year Rule To prevent this, the Government introduced the first-year rule in 1981. This says that you can only depreciate half the cost of an asset in its first year.

31

Example: Yellow Cabs buys two taxis for $40,000 each. They are in Class 16, so they depreciate at 40% per year. So in the first year, there is $80,000 in the class, and so the first year depreciation is $80,000 × 0.5× 0.4 = $16,000. * So the capital cost allowance for the first year is $16,000, and the undepreciated capital cost [`UCC’] at the beginning of the second year is $64,000. So Yellow Cabs saves $16,000t from their taxes in Year 1. * now includes first-year rule

32

Example: Yellow Cabs’s undepreciated capital cost [`UCC’] at the beginning of the second year is $64,000. Now they sell one of their cabs for $40,000. They now have an undepreciated capital cost of $24,000 in the pool. During the year this depreciates by 40%, so they can claim a depreciation allowance of $9,600. This saves them $9,600t in taxes. They begin the third year with $14,400 in the class.

![Example: Yellow Cabs’s undepreciated capital cost [`UCC’] at the beginning of the second year is $64,000.](http://images.slideplayer.com/18/5678810/slides/slide_32.jpg "Now they sell one of their cabs for $40,000. They now have an undepreciated capital cost of $24,000 in the pool. During the year this depreciates by 40%, so they can claim a depreciation allowance of $9,600. This saves them $9,600t in taxes. They begin the third year with $14,400 in the class..")

34

Australian Tax Rules

36

UK Tax Rules

38

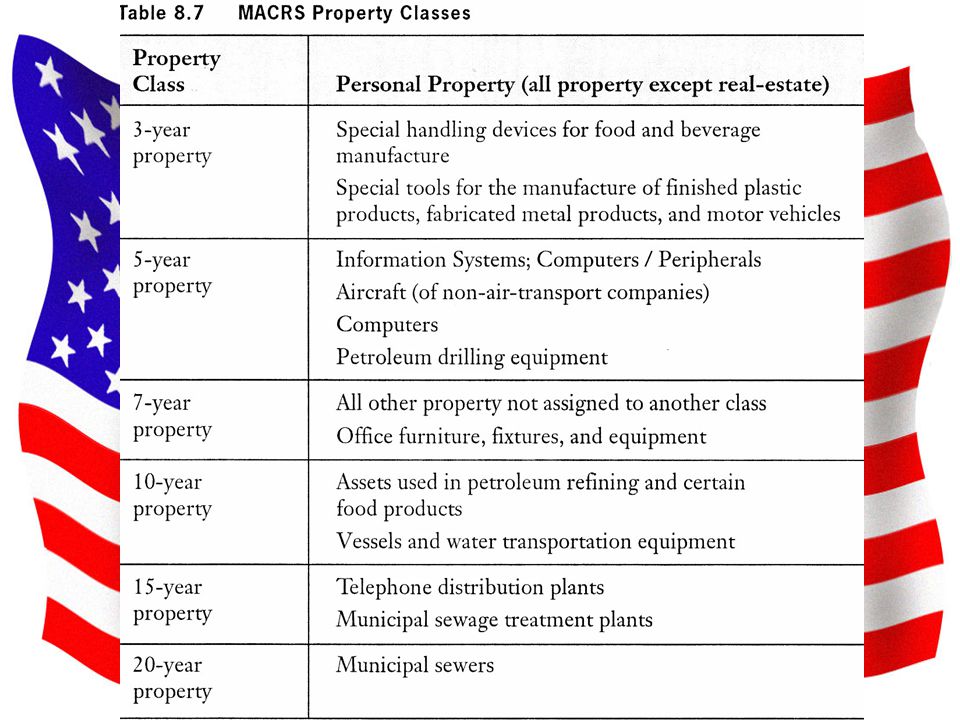

US Tax Rules

Similar presentations

, obsolescence and lower resale value.>")

– total income realized from all revenue-producing sources, including items such as the sales.>")

>")