Download presentation

Presentation is loading. Please wait.

1

LESSON 10-1 Journalizing Sales on Account Using a Sales Journal

4/17/2017 LESSON 10-1 Journalizing Sales on Account Using a Sales Journal

2

Sales Tax: A tax on the sale of merchandise or services.

New Vocabulary Customer: A person or business to whom merchandise or services are sold. Sales Tax: A tax on the sale of merchandise or services. 10-1

3

SALES TAX page 270 10-1

4

SALES OF MERCHANDISE ON ACCOUNT

page 271 10-1

5

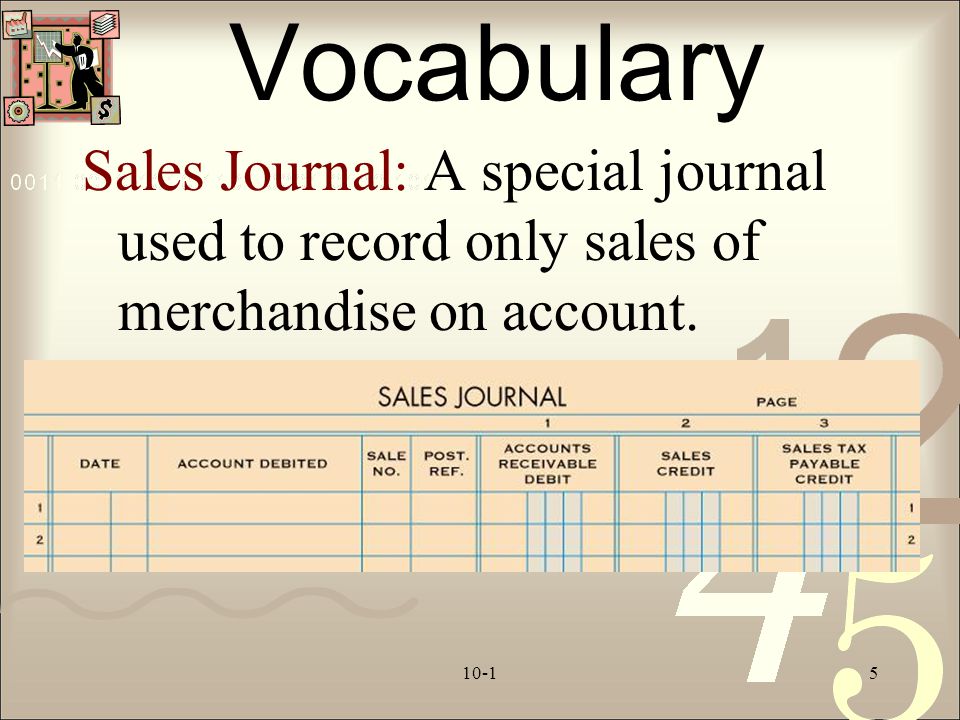

Vocabulary Sales Journal: A special journal used to record only sales of merchandise on account. 10-1

6

SALES INVOICE page 272 10-1

7

SALE ON ACCOUNT page 273 November 3. Sold merchandise on account to Village Crafts, $540.00, plus sales tax, $32.40; total, $ Sales Invoice No. 76. 10-1

8

TOTALING, PROVING, AND RULING A SALES JOURNAL

page 274 10-1

9

Audit Your Understanding

How are sales tax rates usually stated? As a percentage of sales 10-1

10

Audit Your Understanding

Why is sales tax collected considered a liability? The amount of sales tax collected is a business liability until paid to the government. What is the title of the general ledger account used to summarize the total amount due from all charge customers? Accounts Receivable 10-1

11

Work Together & OYO P. 275 10-1

12

Journalizing Cash Receipts Using a Cash Receipts Journal

LESSON 10-2 Journalizing Cash Receipts Using a Cash Receipts Journal

13

New Vocabulary Cash sale: A sale of which cash is received for the total amount the sale at the time of the transaction (Includes credit card sales) Credit card sale: A sale in which a credit card is used for the total amount of the sale at the time at the transaction Point-of-sale terminal: A computer used to collect, store, and report all the information of sales transaction 10-1

14

PROCESSING CASH SALES TRANSACTIONS

page 277 Cash Register Receipt Point-of-Sale (POS) Terminal Receipt UPC (Universal Product Code) (continued on next slide) 10-1

Terminal Receipt. UPC (Universal Product Code) (continued on next slide)")

15

New Vocabulary Terminal Summary Terminal Summary: A report that summarizes the cash and credit card sales of a point-of-sale terminal 10-1

16

New Vocabulary Batch report: a report of credit card sales produced by a point-of-sale terminal Batching out: The process of preparing a batch report of credit card sales from a point-of-sale terminal Batch Report 10-1

17

New Vocabulary Cash Receipts Journal: A special journal used to record only cash receipt transactions Sales discount: the cash discount on sales taken by a customer when paying early

18

CASH AND CREDIT CARD SALES

page 279 November 4. Recorded cash and credit card sales, $5,460.00, plus sales tax, $327.60; total, $5, Terminal Summary 34. 10-1

19

CASH RECEIPTS ON ACCOUNT

page 280 November 6. Received cash on account from Country Crafters, $2,162.40, covering S69. Receipt No. 90. 10-1

20

CASH RECEIPT ON ACCOUNT --with a 2% sales discount

page 282 November 7. Received cash on account from Cumberland Center, $1,176.00, covering Sales Invoice No. 74 for $1,200.00, less 2% discount, $ Receipt No. 91. 10-1

21

TOTALING, PROVING, AND RULING A CASH RECEIPTS JOURNAL

page 283 10-1

22

Audit Your Understanding

Who transfers files between the banks involved in the credit card sales? The funds are transferred among the banks issuing the credit cards. 10-1

23

Worked Together & OYO P. 284 10-1

24

LESSON 10-1 Recording Transactions Using a General Journal

4/17/2017 LESSON 10-3 Recording Transactions Using a General Journal

25

New Vocabulary Sales return: Credit allowed a customer for the sales price of returned merchandise, resulting in a decrease in the vendor’s accounts receivable Sales allowance: Credit allowed a customer for part of the sales price of merchandise that is not returned, resulting in a decrease in the vendor’s accounts receivable Credit memorandum: A form prepared by the vendor showing the amount deducted for returns and allowances 10-1

26

CREDIT MEMORANDUM FOR SALES RETURNS AND ALLOWANCES

page 285 10-1

27

JOURNALIZING SALES RETURNS AND ALLOWANCES

page 286 March 11. Granted credit to Village Crafts for merchandise returned, $58.50, plus sales tax, $3.51, from S160; total, $ Credit Memorandum No. 41. 10-1

28

Audit Your Understanding

What is the difference between a sales return and a sales allowance? A sales return is credit allowed a customer for the sales price of returned merchandise; A sales allowance is credit allowed a customer for part of the sales price of merchandise that is not returned. What is a source document for journalizing sales returns and allowances? Credit memorandum 10-1

29

Work Together & OYO P. 287 10-1

30

Enjoy the Show… 10-1

58

Preschooler Test I already knew I was dumber than the fifth graders...but now it's the preschoolers.

59

Which way is the bus below traveling? To the left or to the right?

10-1

60

Look carefully at the picture again.

Can't make up your mind? Look carefully at the picture again. Still don't know? 10-1

61

90% of the pre-schoolers gave this answer:

Pre-schoolers all over the United States were shown this picture and asked the same question. 90% of the pre-schoolers gave this answer: "The bus is traveling to the left.." 10-1

62

"Because you can't see the door to get on the bus.“

When asked, "Why do you think the bus is traveling to the left?“ They answered: "Because you can't see the door to get on the bus.“ 10-1

63

The End 10-1

Similar presentations