Download presentation

Presentation is loading. Please wait.

1

Statement of Cash Flows

4

CENTRAL FACT Over long enough periods: NI = Cash from Ops. + Cash from Inv. = Free Cash Flows The difference is timing The goal of SCF is to explain the difference

5

Why do we care about cash? Information on: –Liquidity –“Quality” of earnings –“Free cash flows” for valuation Problem: –interpretation is difficult and context specific –depends on the life-cycle of the company –it is hard to know what is a good cash flow

6

Fundamental Relations Assets = Liabilities + Owners’ Equity Cash = Liabilities + OE - Noncash Assets Cash = Liab. + OE - Noncash Assets Cash = NI + Liab. + CC - Div. - NCA

10

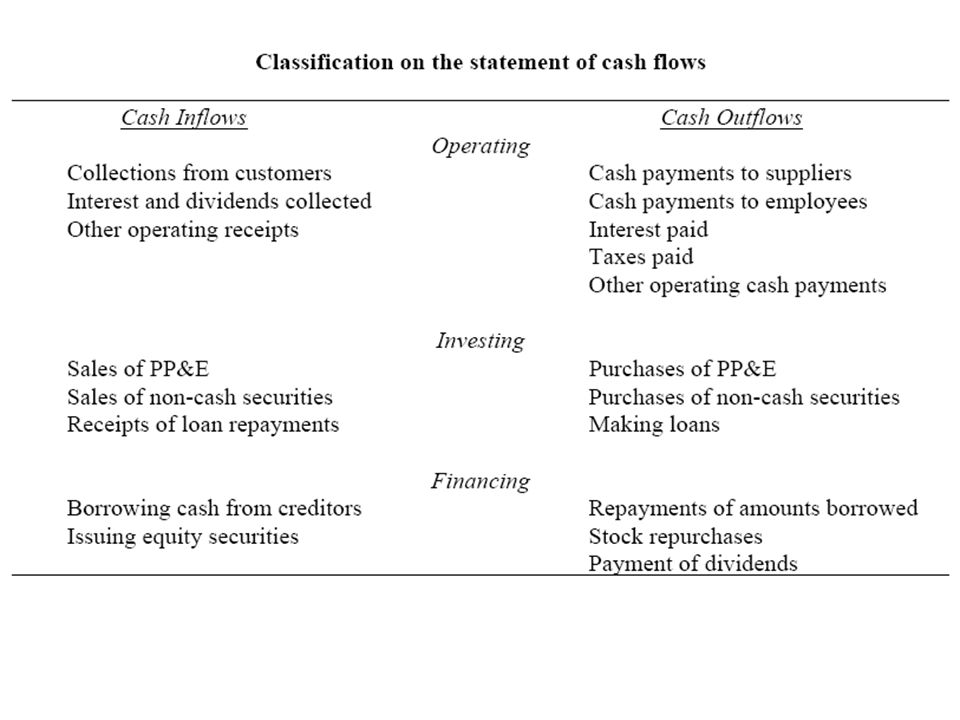

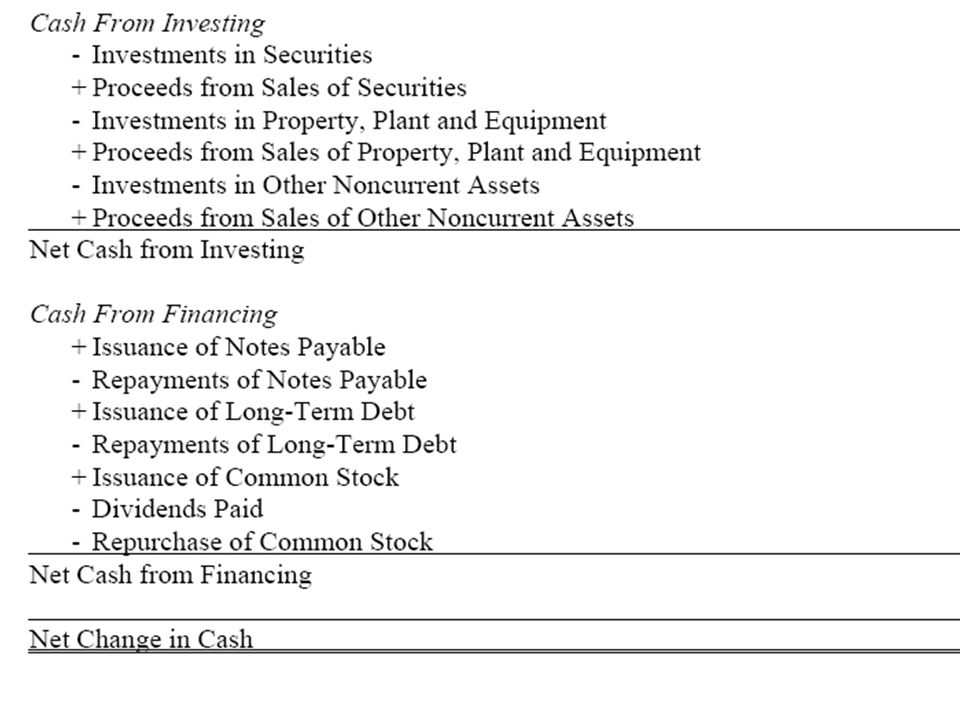

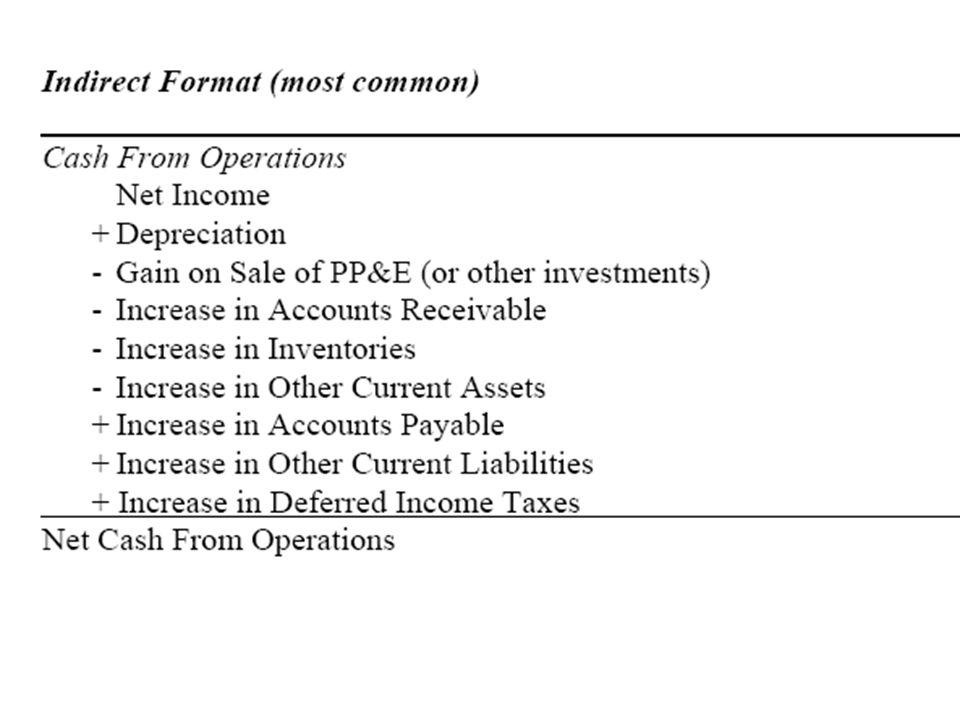

Formats Two formats for the operation section Financing and investing are always the same

14

Miscellaneous Cash Flow Stuff Why don’t lines on SCF tie to changes on B/S? Foreign currency translation –subsidiaries are generally accounted for in local currency –in consolidation local currency is converted to dollars –changes in accounting balances that result from changes in currency are handled as a separate line item on SCF –changes in shareholders’ equity go to “other equity” on the balance sheet

15

Example Foreign sub with the following ‘96 and ‘97 ¥ B/S and the ¥ weakening from ¥100/$ to ¥111/$. ‘96 & ‘97‘96‘97 Cash¥100$1.0$0.9 Inventory¥200$2.0$1.8 Equity (100% owned) ¥300$3.0$2.7 B/S--change in equity ($0.3) is “foreign currency translation adjustment” in shareholders’ equity SCF--the change in cash ($0.1) is separate line item (not spread across change in inventory, etc)

¥300$3.0$2.7 B/S--change in equity ($0.3) is foreign currency translation adjustment in shareholders’ equity SCF--the change in cash ($0.1) is separate line item (not spread across change in inventory, etc).")

16

Acquisition Accounting You buy a company with identifiable assets with a book value of $100 (fair value of $200) for $250. Identifiable Assets$200 Goodwill$50 Cash $250 Goodwill will appear as an intangible asset On the SCF, the only effect will be $250 as an investing use of cash, even though lots of other accounts change

17

Major Noncash Transactions Transactions not involving cash are not reported on the face of the statement –e.g., purchase PP&E for debt, acquire other companies for stock, swap assets Disclosure is required –typically at the bottom of the SCF

18

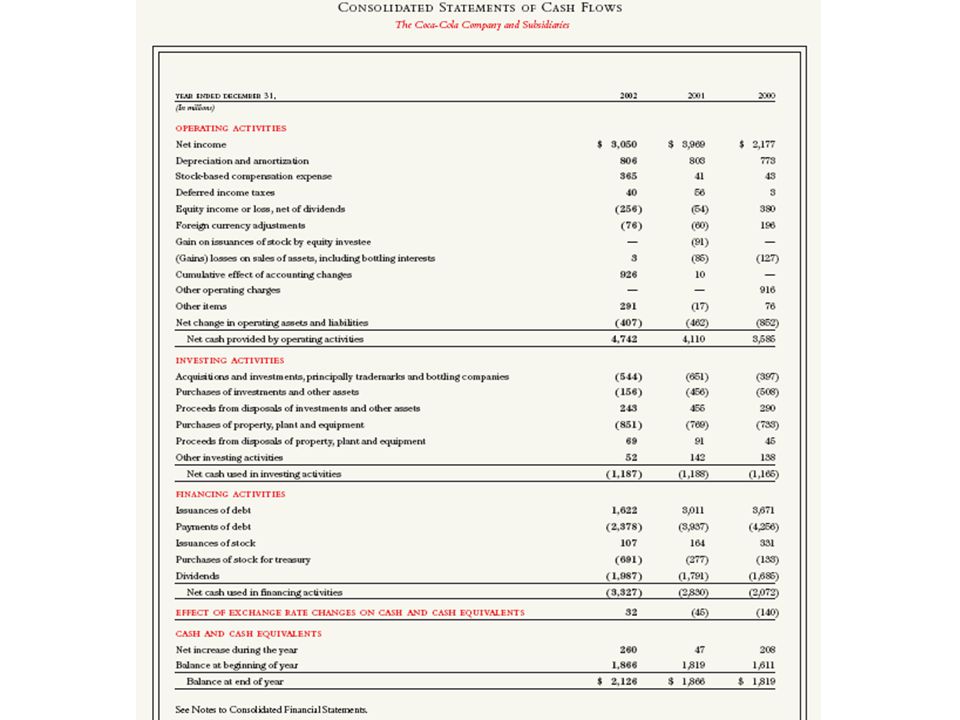

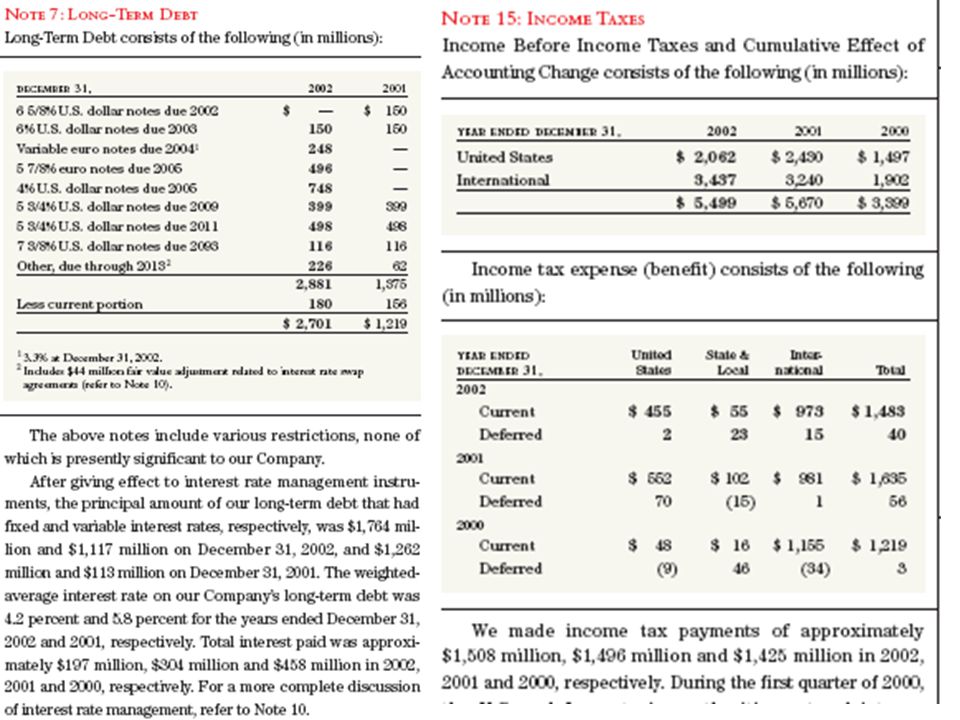

Other Items Firms must disclose interest and taxes paid –income statement gives “accrual” amounts –cash interest & taxes are used in some analysis –generally disclosed at the bottom of SCF –sometimes disclosed in notes (e.g., Coke)

")

Similar presentations

Statement of Cash Flows (1987) Research.>")