Download presentation

Presentation is loading. Please wait.

2

DA 201 Course Tim Quigg, Associate Chairman Department of Computer Science UNC at Chapel Hill Salt Lake City October 25, 2004 Financial Planning and Shadow Accounting Copyright © 2004, SRA International and Sharon Kiser, Steve Lawrence, Tim Quigg, Lawrie Robertson, Cary Thomas, Sheila Vrana, and Mark Wdowik. All rights reserved.

3

DA 201 Course http://www.cs.unc.edu/~quigg

4

DA 201 Course Arguing with an Auditor is Like Wrestling with a Pig in Mud... After a while, you realize the pig ENJOYS it!

5

DA 201 Course The Importance of Financial Planning at the Departmental Level Cannot be Overstated! Question 1: Where are we now? Question 2: Where are we going?

6

DA 201 Course Financial Planning Question 1: Where are we now? Critical need for accurate, detailed and current view of financial status (by project and department-wide) If institutional accounting records provide this – fine! If not, you need a departmental system (“shadow accounting”).

If institutional accounting records provide this – fine. If not, you need a departmental system ( shadow accounting )..")

7

DA 201 Course Financial Planning Question 2: Where are we going? Projecting expenditure/revenue forecasts into the future (for fiscal year) Special attention to personnel –Plan to cover soft money people for year –Note institutional policy for “layoffs”

Special attention to personnel –Plan to cover soft money people for year –Note institutional policy for layoffs .")

8

Personnel Funding Chart

10

DA 201 Course Question 2: Where are we going? Projecting expenditure/revenue forecasts into the future (for fiscal year) Special attention to personnel –Plan to cover soft money people for year –Note institutional policy for “layoffs” Special attention to fixed expenses –Equipment (or software) maintenance contracts, rent Financial Planning

Special attention to personnel –Plan to cover soft money people for year –Note institutional policy for layoffs Special attention to fixed expenses –Equipment (or software) maintenance contracts, rent Financial Planning.")

11

DA 201 Course Do You Need A Departmental System? Remember, central systems are first designed to meet institutional needs Department needs are secondary Central systems often don’t provide everything that is needed to “run a department”, for example: Store backup for purchase quotes (your auditors will want to see these) Store vacation and sick leave data Give you the flexibility to produce the reports that you need ENCUMBER SALARIES THROUGH BUDGET PERIOD

Store vacation and sick leave data Give you the flexibility to produce the reports that you need ENCUMBER SALARIES THROUGH BUDGET PERIOD.")

12

DA 201 Course Are Central Records Systems Adequate? “Relying upon poor data from a central system to manage the financial affairs of your department is like relying upon the tide to steer your ship.” It Just Doesn’t Make Sense!

13

DA 201 Course Shadow Accounting Systems “A shadow accounting system is a set of records maintained at a local level independent of the official records” Have existed in some form probably forever PIs keeping account balances in lab books Personal computers fostered an explosion of shadow systems

14

DA 201 Course When To Implement A Shadow Accounting System? When central records Do not provide enough detailed information, The information is not readily available in a usable form, When there is too much lag time between incurring an obligation and it being posted to the central records, and If the benefits (dollars and time) out weigh the costs!

out weigh the costs!.")

15

DA 201 Course Additional Advantages Tracking Extra Data on Transactions Purpose of expense, e.g., graduate student education fund, faculty recruiting Category of expense, e.g., supplies for particular class Maintaining sub accounts internally for a single central account Departmental “earmarks” for gift or institutional accounts May be easier to keep in one account (less institutional hassle and paperwork)

")

16

DA 201 Course “Dos” Do be sure to enter transactions into your system before they “leave your office” (paper or electronic) Do be sure that your records are secure and stored in a safe form and location Do perform a regular, thorough reconciliation to official records using a reconciliation worksheet Do print and store reports in a form that are useful in audit situations Do train more than one person on the proper use of the system.

Do be sure that your records are secure and stored in a safe form and location Do perform a regular, thorough reconciliation to official records using a reconciliation worksheet Do print and store reports in a form that are useful in audit situations Do train more than one person on the proper use of the system.")

17

DA 201 Course “Don’ts” Don’t assume that magnetic files will always be available for printing the report the auditor is going to request! Don’t assume that just because you recorded the transaction correctly in YOUR system, that it got posted correctly in THEIR system! Don’t assume that the person who uses the system today will ALWAYS be around tomorrow!

18

DA 201 Course Goal Financial Reconciliation Process

19

DA 201 Course Step 1 Obtain central data (financial reports and transaction data) in a form that you can match with the shadow system (typically by account for a particular accounting period) Financial Reconciliation Process

in a form that you can match with the shadow system (typically by account for a particular accounting period) Financial Reconciliation Process")

20

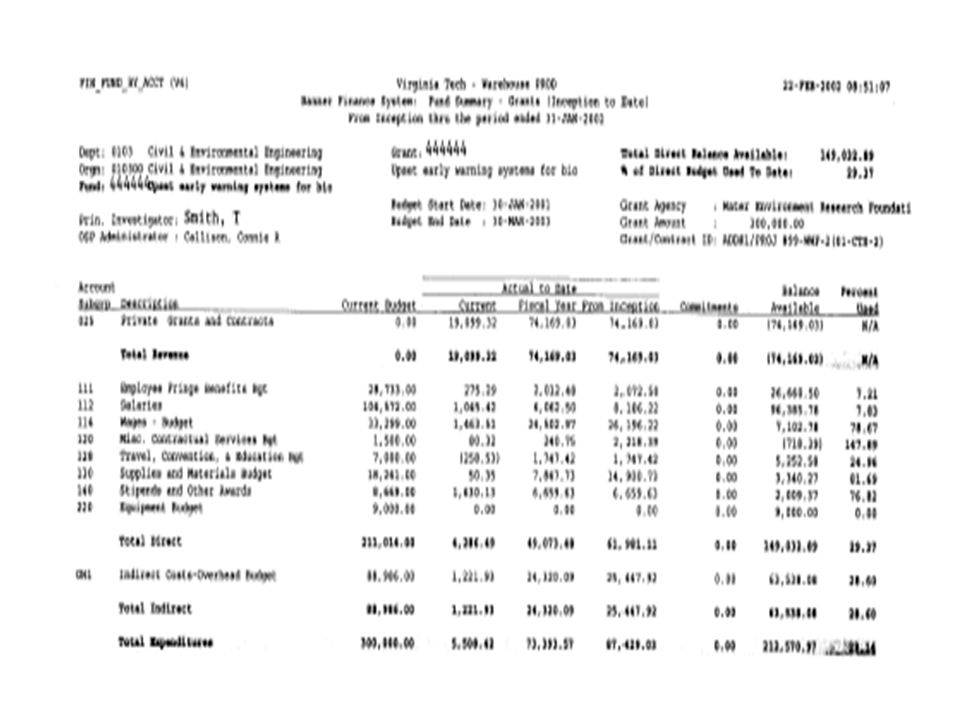

UNC Central Report

23

DA 201 Course Financial Reconciliation Process Step 2 Prepare shadow data (financial reports and transaction data) in the matching format as the central data.

in the matching format as the central data.")

24

Computer Science Department Report

26

DA 201 Course Step 3 Compare differences in expenditures/balances by object code between central and departmental financial reports This will alert you to particular areas of discrepancy Summary of Discrepancies Central RecordsDepartmental RecordsDifference Personnel255,069.96248,560.506,509.46 Supplies7,384.004,345.063,038.94 Travel2,137.67593.871,543.80 Financial Reconciliation Process

27

DA 201 Course Step 4 Best approach - compare all transactions for the period and “check off” those that match. Compromise approach (use in situations where volume is enormous and accounting staff resources are limited) - compare all transactions for the period in the object codes where discrepancies were noted in the comparison of financial reports. Financial Reconciliation Process

- compare all transactions for the period in the object codes where discrepancies were noted in the comparison of financial reports. Financial Reconciliation Process.")

28

DA 201 Course Every discrepancy must be researched and explained! IMPORTANT

29

The Reward is Worth the Effort

30

DA 201 Course What Are Likely Explanations For These Discrepancies? Timing errors Posting errors Processing errors (the form is still sitting on your desk!)

.")

31

DA 201 Course Reconciliation Confirm the timing items by inquiry to the central system. If you can’t find them, you will need to do more research. Confirm posting errors to the central system and get them fixed. Correct departmental processing errors. Keep a list of items that should be corrected in the next accounting cycle.

32

DA 201 Course Reconciliation Unmatched central items “got past you” and need to be recorded in the shadow system, or explained out in a reconciliation worksheet.

33

The Right Tool Does Matter!

34

Our Motto: Whistle While You Work

35

That’s All Folks!

Similar presentations

>")