Download presentation

Presentation is loading. Please wait.

1

MGMT 7730 – Economics and Institutions

Course Convenor: Houman Younessi Tel:

2

Course objectives: This course will introduce the basic principles of economics and establish this discipline as a managerial decision-making framework. The course will draw on economic analysis of concepts such as demand, cost, profit, competition, price and pricing strategy, and market protection and tie them to operational business decisions.

3

Key textbook: Kent, P.G.; Young, P.K.Y.

Managerial Economics: Economic Tools for Today’s Decision Maker; 6th (or Fifth) Edition; Pearson-Prentice-Hall (2006)

Edition; Pearson-Prentice-Hall 2010 (2006)")

4

Computing Requirements:

Student must be proficient with the basic use of spreadsheet software. Access to the internet and the World-Wide Web is also necessary Use of other software packages and facilities is permitted to assist with learning and assignments but is not mandatory.

5

Teaching Method: Assessment:

The principal teaching is through lectures and discussions. There will be 10 lectures during the semester. Whilst formal attendance is not taken, attending all lectures is expected of students and is deemed an important critical success factor. Assessment: Assessment is through two take-home assignments and a final paper Assignments: 30% each (60% total) Final paper 40%

Final paper 40%")

6

Syllabus: Introduction and the theory of the firm

Demand and various elasticities of demand Rational choice, estimating demand and forecasting Production and the production function Cost, cost factors and break-even analysis Strategic behavior and game-theory Markets and competition: strict monopoly - perfect competition, a spectrum Monopolistic competition and sophisticated monopolistic behavior Oligopoly Risk, moral hazard and the principal-agent problem Public goods and the role of government

7

Silk, Sword and SUV – Global Business

The interaction of enterprise, markets and the environment.

8

Providing Value: need for high quality products and services

Why do business at all? What products should we make and where should we sell them? How do I get the most reward for my enterprising effort? How long can I/ should I continue in that enterprise?

9

Profit Why do business at all? What is Profit?

Accounting profit versus economic profit Opportunity cost

10

Demand What products should we make and where should we sell them?

If you are certain that there will not be – ever - anyone out there who wishes to buy the product under question, then it should not be offered

11

How do I get the most reward for my enterprising effort?

Determining which item should be sold where and when Demand manipulation: Price setting, Advertising, Market generation, Income, Wealth, etc Elasticity of Demand

12

Supply How do I get the most reward for my enterprising effort?

Supply management: Amount of supply, Competing Products, Complementary products, etc.

13

How long can I/ should I continue in that enterprise?

Risk Opportunity

14

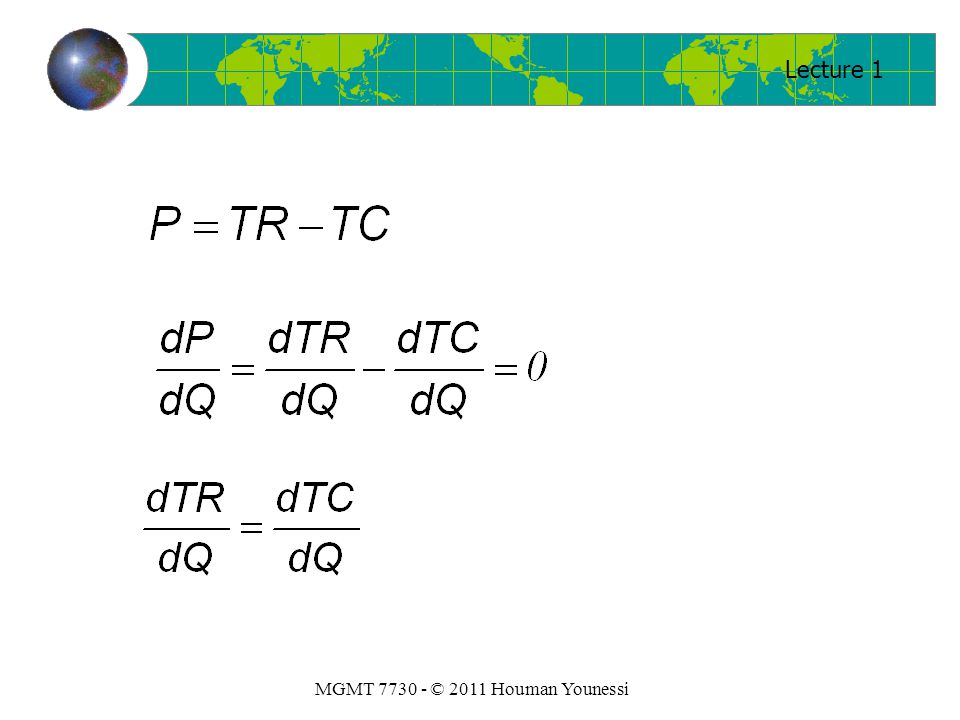

Profit is the difference between revenue and cost

p = r - c Profit is the difference between revenue and cost

15

P0 Current profit figure P0 Value of current profit now

P1 Profit next year Value of next year’s profit now Value now of profit earned in two years time, P2 Profit year after next Value now of profits earned in two consecutive years So, Represents the present value of all profits earned over n years

16

The Value of Firm Model:

17

r Firms would have revenue if there was demand for their products.

There will be demand only if the product: Satisfies a need or want Represents an adequate level of quality The required quality is offered at an acceptable price

18

INFORMATION on Retain Obtain Process Disseminate use

What products and, products that we contemplate offering in the future are (or will be) needed? What level(s) of quality of products will be demanded by the market and where? What is the quality level of the products we currently make and how much does it take to improve that quality? What level of demand will there be for our products and when will that demand manifest itself? What prices should the firm set for their products, and should the prices be uniform or vary in their different markets? Process Disseminate use

needed What level(s) of quality of products will be demanded by the market and where What is the quality level of the products we currently make and how much does it take to improve that quality What level of demand will there be for our products and when will that demand manifest itself What prices should the firm set for their products, and should the prices be uniform or vary in their different markets Process. Disseminate. use.")

19

c Capability Production Quality Technology Resources

20

i

21

n

22

Element Concept Information Category Information System Revenue Demand Market trends and marketing Product quality Pricing Data Acquisition Data Analysis Control Forecasting Optimization Cost Production Process capability Technology Estimating Risk Uncertainty Macroeconomic Environment Internal control Longevity Sustainability Environment Integration and systemicity

23

Aggregate Demand and Aggregate Supply

Product Process Enterprise Environ. Quality Efficiency Effective- ness Sustain. Aggregate Demand and Aggregate Supply Demand and Supply Supply Side Demand Side

24

Demand and the Concept of the Market

Market: A group of organizations and individuals that are in touch with each other in order to buy or sell some good. Every market has a demand side and a supply side

25

Demand Side of the Market

At Price ($) 8 6 4 2 Buyers would buy Quantity (ton) 10 20 30 40

Buyers would buy Quantity. (ton)")

26

Supply Side of the Market

At Price ($) 8 6 4 2 Sellers would sell Quantity (ton) 10 20 30 40

Sellers would sell Quantity. (ton)")

27

Equilibrium Price 8 Excess Supply 6 4 2 Excess Demand 10 20 30 40

($) 8 Excess Supply 6 4 2 Excess Demand Quantity (ton) 10 20 30 40

8. Excess Supply Excess Demand. Quantity. (ton)")

28

Decline in Demand Price ($) 8 6 4 2 Quantity (ton) 10 20 30 40

Quantity (ton)")

29

Rise in Demand Price ($) 8 6 4 2 Quantity (ton) 10 20 30 40

Quantity (ton)")

30

Decline in Supply Price ($) 8 6 4 2 Quantity (ton) 10 20 30 40

Quantity (ton)")

31

Rise in Supply Price ($) 8 6 4 2 Quantity (ton) 10 20 30 40

Quantity (ton)")

32

Functional Relationship

Q=f(P) Q=f(P,I,T,PA,A,…)

Q=f(P,I,T,PA,A,…)")

33

Marginal Value The change in a dependent variable associated with a ONE UNIT change in a particular independent variable As such: Marginal profit is the change in total profit associated with a one unit change in output

34

Number of units of output

Total Profit Average Profit Marginal Profit --- 100 1 100 100 150 2 250 125 350 3 600 200 400 1000 250 4 350 1350 270 5 150 6 1500 250 50 7 1550 221.4 (-50) 8 1500 187.5 (-100) 9 1400 155.5 (-200) 120 10 1200

(-100) (-200)")

35

Marginal Change Profit Marginal profit is the change in profit with respect to change in quantity Total Profit Q0 Q1 Q2 Q3 Number of units of output Profit per unit of output Marginal Profit Q0 Q1 Q2 Q3 Number of units of output

36

Marginal value is the slope of the tangent of the curve

(P2-P1) / (Q2-Q1) Profit C B P2 (P3-P1) / (Q3-Q1) P3 A P1 Marginal value is the slope of the tangent of the curve Q1 Q3 Q2 Number of units of output

/ (Q2-Q1) Profit. C. B. P2. (P3-P1) / (Q3-Q1) P3. A. P1. Marginal value is the slope of the tangent of the curve. Q1. Q3. Q2. Number of units of output.")

37

Profit A Q1 Number of units of output

38

Profit A Q1 Number of units of output

39

Total Cost $ Total Revenue Number of units of output

Similar presentations

9904 7135. Fax: (03)9907 4100.>")