Download presentation

Presentation is loading. Please wait.

1

Competence Center Corporate Finance & Risk Management by Harald Weiß Stuttgart, Jan 27th 2006 Pricing Liquidity Risk

2

Agenda 1.Motivation 2. Liquidity Measures 3. Pricing Liquidity Risk with APT 4.Using OPT for Valuing the Time Dimension of Liquidity 5.Extending the Longstaff model

3

Practitioner´s view majority of market participants consider the liquidity of assets in portfolio decisions Until recently liquidity research was focussed on individual assets asset value is reduced by lower liquidity investor demands for a liquidity premium Current research about liquidity liquidity is a market-wide phenomena Is liquidity risk a non-diversifiable risk? 1. Motivation

4

2. Liquidity Measures Asset Liquidity Time DimensionPrice Dimension Keynes (1930): „realisable at short notice without loss“ market liquidity is characterized by the trade-off between the selling-price and the time-till-sale for a given set of market conditions

: „realisable at short notice without loss market liquidity is characterized by the trade-off between the selling-price and the time-till-sale for a given set of market conditions.")

5

2. Liquidity Measures A closer to look to the Xetra-Orderbook

6

2. Liquidity Measures Aitken and Comerton-Forde (Pacific-Basin Finance Journal, 2003 (1)) found 68 different measures used in the literature Selected liquidity measures with summary statistics for NYSE (Roll, 2005)

) found 68 different measures used in the literature Selected liquidity measures with summary statistics for NYSE (Roll, 2005).")

7

3. Pricing Liquidity Risk with APT Pastor and Stambaugh (2003) model

model")

8

3. Pricing Liquidity Risk with APT

9

4. Using OPT for Valuing the Time Dimension of Liquidity Perfectly liquid asset: t=0t=1 S t=0t=1 S Il liquid asset: Restricted from trading more flexibility for investors holding the liquid asset standard no-arbitrage argument: value of marketability is equal to the price difference between the two assets (positive) value of marketability can be viewed as a trading option tt

value of marketability can be viewed as a trading option tt.")

10

Idea:a put option provides a protection against illiquidity a position hedged by a put self-liquidates as money is lost and markets become illiquid put price can be viewed as the value of liquidity concept of portfolio insurance In general:put option gives the holder the right to sell the underlying asset by a certain date T for a certain price X Short Put X Payoff S T (Terminal stock price) 0 4. Using OPT for Valuing the Time Dimension of Liquidity

11

Longstaff, Journal of Finance (1995) investor has perfect market timing ability, knows the optimal selling point in t=0 additional profit: = payoff of a European lookback put option upper bound for the value of marketability Lookback option underlying stochastic process is normally a geometric Brownian motion modification: Brownian bridge process 5. Extending the Longstaff model

12

Definition of the underlying stochastic procees

13

Simulation of the underlying stochastic process 5. Extending the Longstaff model

14

Pricing Lookback options using Monte Carlo Simulation (STATA) Program: (1)Select the starting parameters here: S 0, S T, σ, T, dt (2) Simulate the underlying stochastic process from t=0 to t=T (3)Keep in mind the maximum stock price during t=0 and t=T (4)Calculate the option price as (5)Repeat steps (1) to (4) (here: 1000 times) (6)Option price is calculated as the mean of (5) (7)Vary the starting parameters σ and T and repeat the simulation steps (1) to (6) 5. Extending the Longstaff model

15

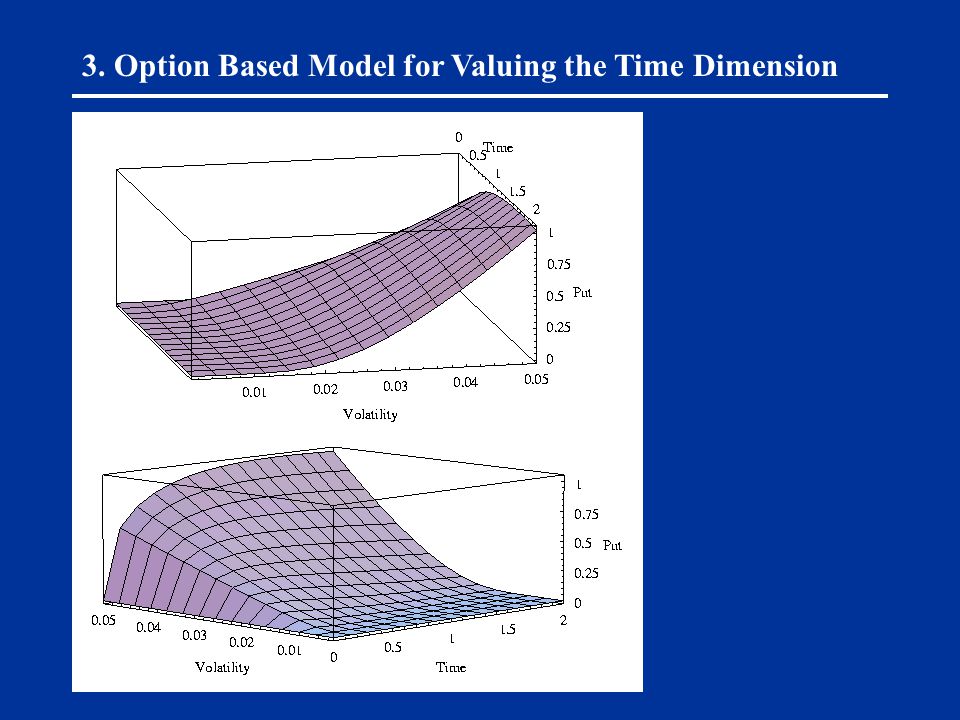

Simulation results

16

Back-up: Further Research Change the stochastic process of the underlying geometric Brownian motion Borwnian bridge process Ornstein-Uhlenbeck process Poisson process Vary the option type American vs. European Lookback, Russian Model the option parameters volatility model (GARCH) stochastic interest rate

stochastic interest rate.")

17

-> add additional risk factors (stochastic interest rates) integrate multiple non-trading periods -> investigate time-dependence of liquidity asset remains illiquid -> no continuous trading (trading is only possible at certrain points in time) -> distribution of trading dates (not uniform?) -> dividend payments Back-up: Further Research

integrate multiple non-trading periods -> investigate time-dependence of liquidity asset remains illiquid -> no continuous trading (trading is only possible at certrain points in time) -> distribution of trading dates (not uniform ) -> dividend payments Back-up: Further Research")

18

Kempf investor has no perfect foresight investor has an incentive to sell the asset when the reservations price Y t differs from the market price value of marketability depends from investor preferences X t follows a stochastic process with the restriction X T = 0 Koziol and Sauerbier, Working-Paper (2003) Lookback Option Stochastic interest rate, multiple non-trading periods, time varying liquidity of bonds Back-up: Option Based Models

Lookback Option Stochastic interest rate, multiple non-trading periods, time varying liquidity of bonds Back-up: Option Based Models")

19

Back-up: Limitations of the Model Discussing the Black-Scholes assumptions (here: selection) (1)underlying asset price follows a geometric Brownian Motion check empirical return distributions (2)assets are divisible (3)trading of the underlying asset is continuously same problem as for real options see assumption: complete capital market is needed Modelling Liquidity Risk exercies of the option which corresponds to the sale of the property is stochastic use Russian options which have no exipry date No general equilibrium model add further assumptions about investor preferences

(1)underlying asset price follows a geometric Brownian Motion check empirical return distributions (2)assets are divisible (3)trading of the underlying asset is continuously same problem as for real options see assumption: complete capital market is needed Modelling Liquidity Risk exercies of the option which corresponds to the sale of the property is stochastic use Russian options which have no exipry date No general equilibrium model add further assumptions about investor preferences")

20

Back-up: XETRA-Orderbook

21

Result both approaches should deliver the same risk-return profile -> Compare the results! =5% =6% we start here Back-up: Motivation

22

3. Option Based Model for Valuing the Time Dimension

24

Back-up

Similar presentations

–is an equilibrium factor mode of security returns –Principle.>")