Download presentation

Presentation is loading. Please wait.

1

ManEc 300Day 1 Bryson 1. This daily outline is subject to revision and upgrading. It might be wise to rely on the syllabus as an agenda 2. Review syllabus 3. On the s ignificance of economics. Review Power Point presentation on the methodology and power of microeconomics

2

3. Personal introduction and testimony 4. Feedback on concerns. What concerns do you have about ManEc 300? ManEc 300Day 1 Bryson(Cont’d)

.")

3

Course Objective I: Help you understand the firm in its competitive environment and its internal organization by mastering these concepts. My objectives will be achieved by understanding. 4 Bounded rationality and private information 4 Central economic planning vs. markets. 4 Competitive markets 4 Competitive advantage 4 How markets work 4 Elasticities 4 Isoquants and Isocost curves 4 Industrial regulation 4 Isoquants and isocosts 4 Coordination and motivation in organizations

4

4 Mathematics and Micro-economics 4 Market models: competition and imperfect comp. 4 Contracting and opportunistic behavior 4 Performance Incentives 4 Porter’s five competitive forces. Strategy and Economics 4 Production and Costs 4 Property Rights and Ownership Course Objective II: Help you gain the conviction through class activities that all these concepts are useful in application.

5

For Tomorrow’s (Second) Session 4 Look over syllabus 4 Read Chap. 1, pp. 14-19, 34-39, Chapter 3 and Chapter 4. 4 Get accustomed to web site 4 See online: Markets, 300.ppt

6

ManEc 300Day 2 Bryson 1. Make seating chart 2. Discuss student presentations (Review syllabus) 3. Introduce TA for the course, Plarent Sinamati sinamati@hotmail.com 4. Sign up for The Wall Street Journal

7

ManEc 300Day 2 Bryson Discuss markets and the market economy by reviewing concepts in “Markets, 300” Non-price variablesDemand curve Substitute productsCeteris paribus Change in supplyChange in q supplied EquilibriumSurplus/shortage Consumer surplusProducer Surplus Market automaticityGovernment intervention

8

ManEc 300Day 2 Bryson 4 Review of first text reading assignment and Markets, 300.ppt. 4 Look at the end of Chapter 4, “Demand Estimation.” 4 Review Econometrics.ppt

9

For Tomorrow’s (Third) Session Finish reading (or review) chapter 4 and brush up on elasticities No quizzes yet. Just do the homework assignment due on Thursday.

10

Group 1: CEO Compensation Scott Brinkerhoff, Jason Greenwood, Rob Murtagh, Jonathan Nielsen Group 2: Intellectual Property Rights Hayden Arnold, Shaun Bailey, Sunne Drinkwater, David Stevens Group 3: K-Mart Bryan Barney, Brian Cooley, Andrea Everts, David Jensen TEAMS, Summer, 2004

11

Group 4: Microsoft as a Monopoly Nathan Palki, Travy Ka Ying Wong, Sabrina Wu, Sandra Woodruff Group 5: Apple Computers and Technology Corey Davis, Aubrey Duncan, Rich Hamilton, Will Kearl TEAMS, Summer, 2004

12

Team Organization 4 Introductions. Choose team spokesman. Exchange phone numbers, etc. 4 Team meeting time. 4 Team name?

13

Team Organization Choose three issues your team would like to present. If there are no conflicts, you will be assigned your first preference. oChoose a major firm and explain its strategies and describe its performance, oDescribe the problems of an entire industry, oTalk about an important problem in the environment of the economy or for a particular industry

14

Team Organization 4 Spokesman. 4 Meeting time. 4 Team name? 4 Select presentation topic priorities: Choose three issues to present. If there are no conflicts, you will be assigned your first choice. oA major firm oAn industry, oAn important micro problem

15

4 Elasticity, Alfred Marshall Consumer response to price change ($1 off on gum/washing machine) 4 ∆p 0, ceteris paribus 4 The Definition %∆Quantity %∆Price ManEc 300Day 3 Bryson

4 ∆p 0, ceteris paribus 4 The Definition %∆Quantity %∆Price ManEc 300Day 3 Bryson")

16

4 Another way to write that 4 ∆Q x 100 Q (mean) ∆P x 100 P (mean) 4 or, point elasticity is: η = (P/Q)(dq/dp) ManEc 300Day 3 Bryson

∆P x 100 P (mean) 4 or, point elasticity is: η = (P/Q)(dq/dp) ManEc 300Day 3 Bryson")

17

%∆Quantity ∆Q x 100 %∆Price Q (mean) ∆P x 100 P (mean) P1=30 P2=40 Q1=133Q2=200 = -[∆Q/(Q1+Q2)/2] / [∆P/P1+P2)/2] =-[-67/(200+133)/2] / [10/(30+40)/2] = 1.4

![%∆Quantity ∆Q x 100 %∆Price Q (mean) ∆P x 100 P (mean) P1=30 P2=40 Q1=133Q2=200 = -[∆Q/(Q1+Q2)/2] / [∆P/P1+P2)/2] =-[-67/( )/2] / [10/(30+40)/2] = 1.4](http://images.slideplayer.com/16/5045911/slides/slide_17.jpg "%∆Quantity ∆Q x 100 %∆Price Q (mean) ∆P x 100 P (mean) P1=30 P2=40 Q1=133Q2=200 = -[∆Q/(Q1+Q2)/2] / [∆P/P1+P2)/2] =-[-67/( )/2] / [10/(30+40)/2] = 1.4")

18

or, point = (P/Q)(dq/dp)

(dq/dp)")

19

4.Elasticity and revenues 5.Elastic >1P TR Inelastic <1 P TR Unitary =1TR max *Diagrams showing each as well as summary diagram ManEc 300Day 3 Bryson

20

“Elastic”: >1P TR

21

“Inelastic”: <1P TR

22

Unitary: =1TR max Summary diagram

23

s, Elasticity of Supply %∆ in Q supplied %∆ in price (∆Q/Q)/(∆P/P) Note positive sign

/(∆P/P) Note positive sign")

24

Cross of Demand % change in Q of X % change in P of Y (∆Qx/Qx) (∆Py/Py) + sign: substitutes - sign: complements Closer relationships indicated by higher coefficient

(∆Py/Py) + sign: substitutes - sign: complements Closer relationships indicated by higher coefficient")

25

Income of Demand % change in Q of X % change in income (∆Qx/Qx) (∆I/I) Q I neg zero low unit High ( i>1)

(∆I/I) Q I neg zero low unit High ( i>1)")

26

For tomorrow’s (fourth) session 1. Review Power Point Presentation: Markets vs. Hierarchies (“Hierarchies”) 2. Complete first homework assignment, which is due tomorrow. 3. For subscribers, t he Journal is available on line. When it starts to come, get on line and go to http://services.wsj.com/ Enter your account number, which is on the address sticker.

2. Complete first homework assignment, which is due tomorrow. 3. For subscribers, t he Journal is available on line. When it starts to come, get on line and go to Enter your account number, which is on the address sticker..")

27

ManEc 300Day 4 Bryson See Power Point Presentation: Markets vs. Hierarchies (“Hierarchies”)

")

28

Day 4 For the next (5 th ) Session 4 See Power Point presentation: The Firm’s Coordination of Plans and Activities (“Firm Coordination”) Be prepared in class to discuss or take a quiz on the following: Should there be market coordination within the corporation? What are design attributes? Firms don’t always have dispatchers or coxswains, so what organizational problem do they have?

29

Day 4 ( Cont’d) Preparation for next session What problems of information flow does the firm have in its planning? What is brittleness? When can the firm not rely on organizational routine for proper functioning of productive processes? How do economies of scale and scope affect the firm’s coordination?

30

ManEc 300, Day 5 Review Questions from Session 4 What problems of information flow does the firm have in its planning? What is brittleness? When can the firm not rely on organizational routine for proper functioning of productive processes? How do economies of scale and scope affect the firm’s coordination? What problems of information flow does the firm have in its planning? What is brittleness? When can the firm not rely on organizational routine for proper functioning of productive processes? How do economies of scale and scope affect the firm’s coordination?

31

ManEc 300Day 5, cont. 4 Review “The Principle-Agent Problem” 4 For tomorrow, you should be well into the reading of Chapter 5 of the text. When you get a chance, review Coase and transactions costs. (See the last part of Chapter 4 and the ppt, “Markets vs. Hierarchies”).

..")

32

The Neo-classical Theory of the Firm, Part II, Production and costs. Start with an unspecified production function: Q = f(a,b,...n) = f(X1, X2,…Xn) ManEc 300Day 6 Bryson

= f(X1, X2,…Xn) ManEc 300Day 6 Bryson.")

33

A specific production function may appear as suggested in the text. Q = S 1/2 A 1/2, where S = steel and A = Aluminum. Reminder: S 1/2 = S and S 1/n = n S ManEc 300Day 6 Bryson

34

Law of Diminishing Returns: holding all inputs constant but one, increasing variable inputs will give rise first to increasing returns, but ultimately, additional units of the input will bring less than proportional returns. Production Functions and costs.

35

Diminishing returns can be shown by exponents that add to less than one. S 1/2 (S 1/2 ) = S S 1/3 (S 1/3 ) = S 2/3 Production Functions and costs.

= S S 1/3 (S 1/3 ) = S 2/3 Production Functions and costs..")

36

Stages of Production 4 Begin with a Total Product (TP) curve. With two geometric “tricks,” find Average Product (AP) and Marginal Product (MP) curves. Discuss these concepts. 4 Relationship between average and marginal values.

and Marginal Product (MP) curves. Discuss these concepts. 4 Relationship between average and marginal values..")

37

Stages of Production 4 At boundary of stages I/II, AP = MP, at boundary of stage II/III, MP = 0. Discuss other characteristics. 4 Why we produce in stage II of production.

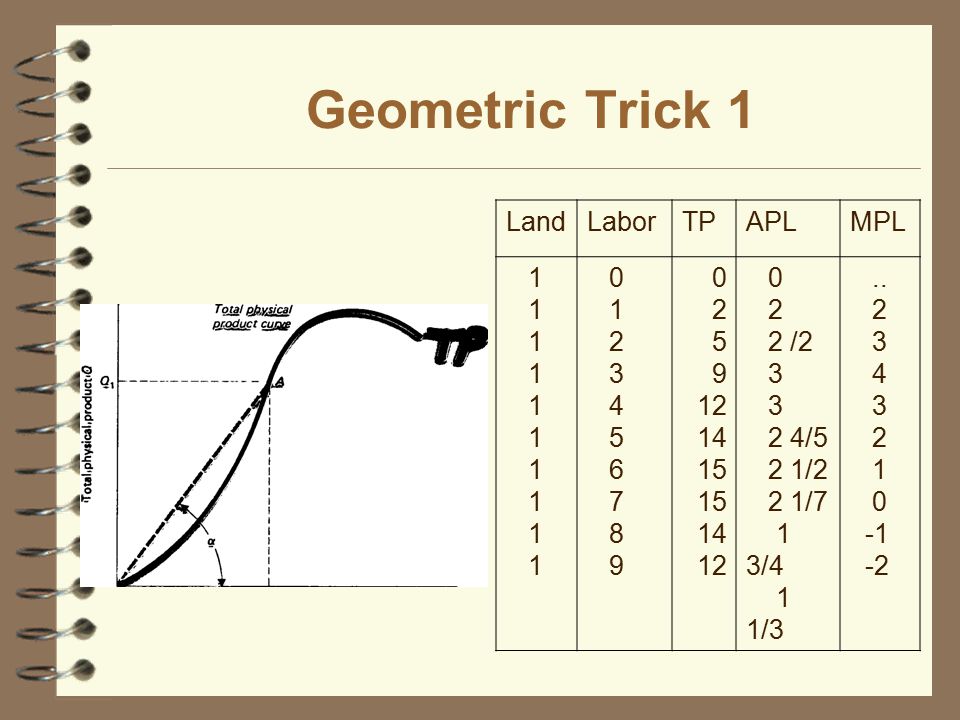

38

Geometric Trick 1 Holding land constant and adding labor leads to a growth of TP until diminishing returns set in. APL = TP/labor. MPL = the change in TP when labor (a) increases by 1 unit. Geometrically, APL = TP/a or the slope of a ray from the origin, intersecting the TP curve at some level of output.

increases by 1 unit. Geometrically, APL = TP/a or the slope of a ray from the origin, intersecting the TP curve at some level of output..")

39

Geometric Trick 1 LandLaborTPAPLMPL 1 1 1 1 1 1 1 1 1 1 0 1 2 3 4 5 6 7 8 9 0 2 5 9 12 14 15 15 14 12 0 2 2 /2 3 3 2 4/5 2 1/2 2 1/7 1 3/4 1 1/3.. 2 3 4 3 2 1 0 -1 -2

40

Geometric Trick 1, the old ray from the origin trick. 4 Slope = rise/run = T/a 4 APL = TP/a 4 Draw a ray from O through the relevant point on the TP curve. 4 Notice that this slope rises to point E, then falls again at larger outputs.

41

Geometric Trick 2, the old tangency trick. MPa = ∆TP when we use one more unit of a. MPa = ∆TP/∆Q

42

Geometric Trick 2, the old tangency trick. Find the slope of TP at a given output to determine the MPa at at that output.. Find the slope geometrically by drawing a tangent line to the TP curve at the interesting output.

43

The Stages of Production Let us 4 draw these and 4 conclude by showing why we operate in Stage II of production. In stage I, we keep going for more inputs because it results in growing average and marginal productivity. In stage III we are experiencing diminishing returns (negative MPa)

.")

44

Review of Costs 1. Show: TVC, TFC, TC What are these? What are their slopes? ManEc 300Day 7 Bryson

45

2. Review two geometric tricks: 1. Find SR: AVC, AFC, AC, 2. Find MC. 3. Relationship between average and marginal values. ManEc 300Day 7 Bryson

46

Total Costs At first, TVC and TC rise gradually, Q rises faster than cost because of increasing returns. Then, TVC and TC rise rapidly. Costs rise faster than output because of diminishing returns.

47

Average variable, average total costs We can find the average costs from the totals, using geometric trick #1, the old ray trick. Draw a ray from the origin through a point on the TC or TVC curve. The slope of the ray is the average cost

48

Average variable, average total costs (Rise/Run = TC/Q = AC. First it declines (increasing returns, then rises (diminishing returns.

49

Marginal Costs Marginal cost is the change in TC or TVC when output is increased by one unit. Or, it is the slope of TC or TVC. Therefore, we can find it by taking the derivative of a TC function.

50

Marginal Costs Or, we can use geometric trick #2, the old tangency trick. Draw a tangency to the TC (or TVC) curve. The slope of the tangent is MC. First, MC declines (increasing returns), but ultimately rises (decreasing returns).

curve. The slope of the tangent is MC. First, MC declines (increasing returns), but ultimately rises (decreasing returns)..")

51

Relate AVC to APP 4 Note that the APP rises and falls in correspondence with the decline, then increase of AVC. AP increases (AVC) falls as increasing returns to the variable factor occurs. 4 But as diminishing returns set in, APP falls, which means that AVC rises.

falls as increasing returns to the variable factor occurs. 4 But as diminishing returns set in, APP falls, which means that AVC rises..")

52

Discuss LR Costs 1. No fixed factors 2. Unlimited number of conceptual SRAC curves ManEc 300Day 7 Prof. Bryson(Cont’d)

.")

53

Discuss LR Costs 3. Envelope curve 4. “For any output, min cost by using the scale of plant whose SRAC curve is tangent to the LRAC curve.” ManEc 300Day 7 Prof. Bryson(Cont’d)

.")

54

5. Why is it U-shaped? Economies of scale vs. Law of diminishing returns Economies of scale: division and specialization of labor, advanced technology, large machines, digitalization and electronics. Diseconomies of scale: control and coordination problems ManEc 300Day 7 Bryson(Cont’d)

.")

55

6.Learning curve 7. 7.Four LRAC curves Textbook U (Range of) constant returns Constant returns through replication Continually increasing returns ManEc 300Day 7 Bryson(Cont’d)

constant returns Constant returns through replication Continually increasing returns ManEc 300Day 7 Bryson(Cont’d).")

56

For the next session, review pp. 111-117 on Isoquants and Isocost lines. ManEc 300Day 7 Bryson(Cont’d)

.")

57

Isoquant/Isocost approach to production, trade, equilibrium and efficiency. ManEc 300Episode 8 Bryson

58

Isoquants--purpose for use Get up to speed on diagrams. Tight logic (and math) vs. Scientists prize -- skepticism, -- rigorous reasoning, and -- empirical experimentation.) ManEc 300Episode 8 Bryson

vs. Scientists prize -- skepticism, -- rigorous reasoning, and -- empirical experimentation.) ManEc 300Episode 8 Bryson.")

59

Appreciate and understand Tradeoffs Budget constraints Logic of maximization Representation of efficiency Get ready for a quiz next session on the production box. Learning Objectives

60

The analysis 1. Intuition on isoquants: Movement NE = improvement. Discovering substitutability of inputs. MRTS lk = ∆ K/ ∆ L one unit of L will compensate. ManEc 300Day 8 (Cont’d)

.")

61

The analysis 2. Characteristics of isoquants a. No intersection b. Downward slope MRTS lk = amount of K lost for which one unit of L will compensate. ManEc 300Day 8 (Cont’d)

.")

62

Total Cost = C = wL + rK Rewrite: rK = C - wL K = C/r - (w/r)L Intercept ratio of factor prices = slope of budget line Budget line

L Intercept ratio of factor prices = slope of budget line Budget line")

63

Slope of isoquant = MRTS lk = MP l /MP k = ∆ K/ ∆L Discuss diminishing MRTS lk Notion of tradeoff ∆Q = MP l (∆L)∆Q = MP k (∆K) Budget line

∆Q = MP k (∆K) Budget line")

64

On the isoquant MP l (∆ L) + MP k (∆K) = 0 At equilibrium Slope of Isoquant = Slope of isocost ManEc 300Day 8 Bryson

+ MP k (∆K) = 0 At equilibrium Slope of Isoquant = Slope of isocost ManEc 300Day 8 Bryson")

65

Mp l /MP k = w/r Mp l /w = MP k /r (Mp l /P l = Mp k /P k ) 4. Show changing slope of isocost line 5. Show changing isocost line (shift when budget changes) ManEc 300Day 8 Bryson

ManEc 300Day 8 Bryson.")

66

Preparation for quiz on isoquants and the Edgeworth Box: 1. Review the effect of price changes 2. Explain the Edgeworth-Bowley Box Trading from any point off the contract curve to a point on the contract curve. 3 ManEc 300Day 9 Bryson

67

Preparation for quiz on isoquants and the Edgeworth Box: 3. Gains of trade. Efficiency is being on the contract curve. ManEc 300Day 9 Bryson

68

4. How does one move on the contract curve? Theft, violence, opportunism-- Elaborate according to time on “economic man” as rational optimizer vs. more modern problem of opportunism. ManEc 300Day 9 Bryson(Cont’d)

.")

69

Contrast utility maximization to opportunism 5. Show connection of points on the contract curve to points on PPF. ManEc 300Day 9 Bryson(Cont’d)

.")

70

Begin with a Total Product (TP) curve. With two geometric “tricks,” find Average Product (AP) and Marginal Product (MP) curves. Discuss these concepts.

and Marginal Product (MP) curves. Discuss these concepts..")

71

Relationship between average and marginal values. Show TP, AP, and MP Diagram

72

At boundary of stages I/II, AP = MP, at boundary of stage II/III, MP = 0. Discuss other characteristics. Why we produce in stage II of production.

73

Geometric Trick 1 Holding land constant and adding labor leads to a growth of TP until diminishing returns set in. APL = TP/labor. MPL = the change in TP when labor (a) increases by 1 unit. Geometrically, APL = TP/a or the slope of a ray from the origin, intersecting the TP curve at some level of output.

increases by 1 unit. Geometrically, APL = TP/a or the slope of a ray from the origin, intersecting the TP curve at some level of output..")

74

Geometric Trick 1LandLaborTPAPLMPL 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 0 1 2 3 4 5 6 7 8 9 0 1 2 3 4 5 6 7 8 9 0 2 5 9 12 14 15 15 14 12 0 2 5 9 12 14 15 15 14 12 0 2 0 2 2 1/2 2 1/2 3 3 2 4/5 2 ½ 3 3 2 4/5 2 ½ 2 1/7 1 3/4 1 1/3 2 1/7 1 3/4 1 1/3.... 2 3 4 3 2 1 0 -1 -2 2 3 4 3 2 1 0 -1 -2

75

Geometric Trick 1, the old ray from the origin trick. Slope = rise/run = T/a Slope = rise/run = T/a APL = TP/a APL = TP/a Draw a ray from O through the relevant point on the TP curve. Draw a ray from O through the relevant point on the TP curve. Notice that this slope rises to point E, then falls again at larger outputs. Notice that this slope rises to point E, then falls again at larger outputs.

76

Geometric Trick 2, the old tangency trick. MPa = ∆TP when we use one more unit of a. MPa = ∆TP/∆Q

77

Geometric Trick 2, the old tangency trick. Find the slope of TP at a given output to determine the MPa at that output. Find the slope geometrically by drawing a tangent line to the TP curve at the interesting output.

78

Draw the stages of production

79

Show why we operate in Stage II In stage I, we keep going for more inputs because it results in growing average and marginal productivity. In stage III we are experiencing diminishing returns (negative MPa). In stage I, we keep going for more inputs because it results in growing average and marginal productivity. In stage III we are experiencing diminishing returns (negative MPa).

. In stage I, we keep going for more inputs because it results in growing average and marginal productivity. In stage III we are experiencing diminishing returns (negative MPa)..")

80

Show: TVC, TFC, TC and their slopes

81

Total Costs At first, TVC and TC rise gradually, Q rises faster than cost because of increasing returns. Then, TVC and TC rise rapidly. Costs rise faster than output because of diminishing returns.

82

Average variable, average total costs We can find the average costs from the totals, using geometric trick #1, the old ray trick.

83

Average variable, average total costs Draw a ray from the origin through a point on the TC or TVC curve. The slope of the ray is the average cost (Rise/Run = TC/Q = AC. First it declines (increasing returns, then rises (diminishing returns).

..")

84

Marginal Costs Marginal cost is the change in TC or TVC when output is increased by one unit. Or, it is the slope of TC or TVC. Therefore, we can find it by taking the derivative of a TC function.

85

Marginal Costs Or, we can use geometric trick #2, the old tangency trick. Draw a tangency to the TC (or TVC) curve. The slope of the tangent is MC. First, MC declines (increasing returns), but ultimately rises (decreasing returns).

curve. The slope of the tangent is MC. First, MC declines (increasing returns), but ultimately rises (decreasing returns)..")

86

Find SR: AVC, AFC, AC, and MC, using two geometric tricks.

87

Note that the APP rises and falls in correspondence with the decline, then increase of AVC.

88

AP increases (AVC) falls as increasing returns to the variable factor occurs. But as diminishing returns set in, APP falls, which means that AVC rises

89

Discuss LR Costs 1. No fixed factors 2. Unlimited number of conceptual SRAC curves. Choose your output, then the SRAC that produces it at the lowest cost.

90

Discuss LR Costs 3. Envelope curve 4. “For any output, min cost by using the scale of plant whose SRAC curve is tangent to the LRAC curve.”

91

Why is it U-shaped? Economies of scale vs. Law of diminishing returns Economies of scale: division and specialization of labor, advanced technology, large machines, digitalization and electronics. Diseconomies of scale: control and coordination problems

92

Learning curve. Four LRAC curves Textbook U (Range of) constant returns Constant returns through replication Continually increasing returns

constant returns Constant returns through replication Continually increasing returns.")

93

Isoquant/Isocost approach to production, trade, equilibrium and efficiency. Isoquants--purpose for use Get up to speed on diagrams. Tight logic (and math) vs.

vs..")

94

Isoquant/Isocost approach to production, trade, equilibrium and efficiency. Scientists prize -- skepticism, -- rigorous reasoning, and -- empirical experimentation.)

.")

95

Appreciate and understand Tradeoffs Budget constraints Logic of maximization Representation of efficiency Get ready for a quiz next session on the production box.

96

1. Intuition on isoquants: Movement NE = improvement. Discovering substitutability of inputs. MRTS lk = ∆ K/ ∆ L

97

2. Characteristics of isoquants a. No intersection b. Downward slope MRTS lk = amount of K lost for which one unit of L will compensate.

98

Total Cost = C = wL + rK Rewrite: rK = C - wL K = C/r - (w/r)L Intercept ratio of factor prices (or slope of budget line)

L Intercept ratio of factor prices (or slope of budget line)")

99

Slope of isoquant: MRTS lk = MP l /MP k = ∆ K/ ∆L Discuss diminishing MRTS lk (and tradeoffs) ∆Q = MP l (∆L) ∆Q = MP k ( ∆ K) On the isoquant MP l (∆ L) + MP k (∆K) = 0

∆Q = MP l (∆L) ∆Q = MP k ( ∆ K) On the isoquant MP l (∆ L) + MP k (∆K) = 0")

100

At equilibrium Slope of Isoquant = Slope of isocost Mp l /MP k = w/r Mp l /w = MP k /r (Mp l /P l = Mp k /P k )

")

101

4. Show isocost line

102

Preparation for quiz on isoquants and the Edgeworth Box: 1. Start with the two-producer barter case of production: the Edgeworth- Bowley Box

103

Gains of trade. Efficiency is being on the contract curve. Trading from any point off the contract curve to a point on the contract curve.

104

O Labor Capital (Food Producer Origin) 0 (Clothing Producer Origin) Labor Capital C

0 (Clothing Producer Origin) Labor Capital C")

105

O Labor Capital (Food Producer Origin) 0 (Clothing Producer Origin) Labor Capital C A Observe a movement from point A to a point on the Contract Curve. B Who has gained here? Is this a net social gain?

106

O Labor Capital (Food Producer Origin) 0 (Clothing Producer Origin) Labor Capital C A Observe a different movement from point A to a point on the Contract Curve. D Who has gained here? Is this a net social gain?

107

O Labor Capital (Food Producer Origin) 0 (Clothing Producer Origin) Labor Capital C A Observe a more reasonable movement from point A to point D on the Contract Curve. D Who has gained here? Is this a net social gain?

108

Movement along the contract curve To move to the contract curve is to achieve efficiency. What does movement along the curve represent? Theft, violence, opportunism– “economic man” as rational optimizer vs. opportunism.

109

The market production case. Isoquants and Isocost lines. TC = Pl(L) + Pk(K). The easy way to draw it.

+ Pk(K). The easy way to draw it..")

110

Say we have a budget of $100, P l = $.50 and P k = $1 $100 =.50L + K K = 100 – 0.5L 100 is the Y intercept, the slope is -1 times the ratio of the two prices (Pl/Pk).

.")

111

Show input prices varying and resultant isocost lines.

112

Ownership and Property Rights.ppt, 1. Review slide (power point) presentation for chapter 5. 2. The ppt presentation reviews Millgrom & Roberts notes. ManEc 300Day 10 Bryson

113

Ownership and Property Rights, II 1. Complete property rights discussion (& “tragedy of commons”) Coase Theorem 2. Read about government actions and other solutions to externalities problem. A. Cooperation and Group Ownership B. Reputation C. Taxes and Subsidies ManEc 300Day 11 Bryson

Coase Theorem 2. Read about government actions and other solutions to externalities problem. A. Cooperation and Group Ownership B. Reputation C. Taxes and Subsidies ManEc 300Day 11 Bryson.")

114

2. a. Discuss overhead “The Nature of Profits”. b. Millgrom & Roberts on “Ownership of Complex Assets”. ManEc 300Day 11 Bryson(Cont’d)

.")

115

ManEc 300Day 12 Prof. BrysonThe Profit Motive 4 Definition 4 I. Normal Profit (as opposed to accounting profits) assumes a return high enough to include: 4 A. Normal (opportunity cost) return to stockholders

assumes a return high enough to include: 4 A. Normal (opportunity cost) return to stockholders.")

116

ManEc 300Day 12 Prof. BrysonThe Profit Motive 4 B. Normal (opportunity cost) return to management (and all other factors). 4 II. Economic Profit or “Pure” Profit is any profit in excess of normal profit.

return to management (and all other factors). 4 II. Economic Profit or Pure Profit is any profit in excess of normal profit..")

117

The Function of Profit 4 Pure or Economic Profit permits: 1. Higher than normal returns (dividends) to owners 2. Increase in value of owners’ holdings (Or, profits “plowed back” into investments)

to owners 2. Increase in value of owners’ holdings (Or, profits plowed back into investments).")

118

The Function of Profit 3. Higher than normal (opportunity cost) returns for other factors of production. Profit can be a vitally important market signal of great social benefit.

returns for other factors of production. Profit can be a vitally important market signal of great social benefit..")

119

The Origins of Profit 4 Profits may result from 4 -- the exploitation of a monopoly position, 4 -- from innovative entrepreneurship and the effective introduction of new technologies (cost-cutting or revenue generating) in the face of risk, or

in the face of risk, or")

120

The Origins of Profit 4 Profits may result from 4 --from a new and superior means of satisfying consumer demands

121

Profit Maximization and Other Theories 4 1. Profit maximization, say most economists, is the best general theory. It has to work in pure competition. 4 2. Where a firm has little competition, or competitive “slack”, it may be at liberty to pursue other objectives, while “satisficing” profits. 4

122

Profit Maximization and Other Theories Other objectives might include: 4 A. Maximizing Sales Revenues 4 B. Maximizing Market Share 4 C. Ensuring Long-term Survival 4 D. Pursuing growth and Diversification for the firm 4 E. Pursuing Social Objectives

123

The Simple Mathematics of Micro 4 Production theory. Begin with a production function: showing output, Q, a function of the variable input, labor, a. 4 Marginal product of labor (MPa) is a) the addition to total product resulting from the use of one more unit of a.

is a) the addition to total product resulting from the use of one more unit of a..")

124

The Simple Mathematics of Micro 4 Marginal product of labor (MPa) is b) the slope of the total product curve, and c) the first derivative of a total product, TP, function, thus, dQ/da = MPa = 21 + 18a - 3a 2 * _______________________

is b) the slope of the total product curve, and c) the first derivative of a total product, TP, function, thus, dQ/da = MPa = a - 3a 2 * _______________________")

125

Taking Derivatives 4 *You will remember about first derivatives that: to get the derivative of a constant, dQ/da = 0. For example, in the expression Q = 21 + 7a - a 2 + 3a 3, the number 21 is a constant, for which dQ/da = 0.

126

Taking Derivatives 4 To get the derivative of a variable “a” preceded by a coefficient m, or ma, dQ/da = m. 4 For example, in the expression Q = 21 + 7a - a 2 + 3a 3, the term 7a consists of the coefficient 7 and the variable a, for which dQ/da = 7.

127

Taking Derivatives 4 To get the derivative of a variable with an exponent, a n, dQ/da = na n-1. 4 For example, in the expression Q = 21 + 7a - a 2 + 3a 3, the term a 2 consists of the variable a and the exponent 2, for which dQ/da = 2a. 4

128

Taking Derivatives 4 (By the formula, this would read 2a 1, but any number or variable taken to the first power, i.e., having an exponent of 1, is not changed. So we need not write the 1.)

.")

129

Taking Derivatives 4 To get the derivative of a variable with both coefficient m and exponent n, such as ma n, we have dQ/da = n(m)a n-1 4 For example, in the expression Q = 21 + 7a - a 2 + 3a 3, the term 3a 3 consists of the variable a with the coefficient 3 and exponent 3, for which dQ/da = 9a 2.

a n-1 4 For example, in the expression Q = a - a 2 + 3a 3, the term 3a 3 consists of the variable a with the coefficient 3 and exponent 3, for which dQ/da = 9a 2.")

130

Taking Derivatives For the entire expression, Q = 21 + 7a - a 2 + 3a 3, we get the derivative dQ/da = 7 - 2a + 9a 2. For average product, AP, we have APa = (TP/a) = (21a + 9a 2 - a 3 )/a = 21 + 9a - a 2

= (21a + 9a 2 - a 3 )/a = a - a 2.")

131

Cost Analysis 4 Now consider costs, using the same kind of analysis. We recall the simple short-run relationships, specifically that total cost, TC, equals total fixed costs (TFC) plus total variable costs (TVC) or TC = TFC + TVC

plus total variable costs (TVC) or TC = TFC + TVC.")

132

Cost Analysis TC = TFC + TVC 4 Dividing both sides by Q, or quantity of output, we have TC/Q = TFC/Q + TVC/Q, or AC = AFC + AVC.

133

Cost Analysis 4 For total cost, consider the expression TC = 128 + 69Q - 14Q 2 + Q 3. Here, TFC = 128 and TVC = 69Q - 14Q 2 + Q 3.

134

Cost Analysis 4 MC = dTC/dQ = dTVC/dQ = 69 - 28Q + 3Q2 4 AVC = TVC/Q = (69Q - 14Q 2 + Q 3 )/Q = 69 - 14Q + Q 2

/Q = Q + Q 2")

135

The Demand Function 4 Consider now a demand function such as P = 3200 - 13Q. 4 It will be recalled that demand = average revenue, AR, so we also have AR = 3200 - 13Q

136

The Demand Function 4 Note that in this expression of a linear demand function, 3200 is the intercept, -13 the slope. 4 To get total revenue, TR, we observe that TR = P x Q, so TR = 3200Q - 13Q 2

137

Marginal Revenue 4 Marginal revenue, MR, is simply the slope of a total revenue curve, or the first derivative of a TR function, 4 so from P = 3200-13Q. TR = PQ = 3200Q – 13Q 2 MR = dTR/dQ = 3200 - 26Q.

138

Marginal Revenue 4 It will be noticed that the MR has the same intercept (3200) as the demand or average revenue curve, while the slope (-26 rather than -13) of MR is twice as great as the slope of AR, i.e., the MR curve falls twice as fast as the demand curve.

as the demand or average revenue curve, while the slope (-26 rather than -13) of MR is twice as great as the slope of AR, i.e., the MR curve falls twice as fast as the demand curve.")

139

Maximizing Profits Now, maximizing the firm’s profits. TR = PQ = 3200Q - 13Q 2 MR = 3200 - 26Q. Assume: TC= 24,000 + 500Q - 13Q 2 + Q 3, MC = 500 - 26Q + 3Q 2.

140

Maximizing Profits To get profit maximization, we simply equate MC and MR, so MC = MR 3200 - 26Q = 500 - 26Q + 3Q 2 2700 = 3Q 2 900 = Q 2 Q = 30

141

Optimal Price with Quantity = 30 4 Looking back at the demand function again, we have P = 3200 - 13(30) P = 3200 - 390 P = 2810. This is the right price to charge for sales of 30 units of output in the pursuit of maximal profit.

142

Don’t forget the group math homework due next session. 1. Math assignment Hints: Problem 3: plug value of Q into formula up front, not after you have differentiated. FOR THE NEXT SESSION

143

Note that dp/dq = 1/(dQ/dP), dQ/dP = 1/(dP/dQ) No quadratic equation used. Follow problem 4's hint. Factor Q 2 so (...Q)(...Q) FOR THE NEXT SESSION

(...Q) FOR THE NEXT SESSION.")

144

As soon as the next discussion (on competition) Is complete, we will have a quiz on that topic. Please look at the reading for the next session.. ManEc 300 Conclusion, Day 12 Prof Bryson

145

Pure Competition 4 The assumptions of pure competition. –A large number of buyers and sellers –Product homogeneity –Free entry and exit 4 The assumption that makes for perfect competition –Rapid dissemination of low-cost, accurate information

146

Pure Competition 4 Discuss the standard, market/firm, double diagram of competition. 4 Short-term profits lead to entry, which can impact costs: constant, increasing, decreasing.

147

3.Review of pure competition. a. TC, TR and NR diagrams for NR>0, NR=0, NR<0. b. When making losses? When shut down? (Go fishing) ManEc 300Day 13 Prof. Bryson Pure Competition

ManEc 300Day 13 Prof. Bryson Pure Competition.")

148

3.Review of pure competition. c. Why is perfect competition efficient? d. Show constant & increasing (then decreasing) costs. 4. Why all cost curves are equal in competition e. ManEc 300Day 13 Prof. Bryson Pure Competition

costs. 4. Why all cost curves are equal in competition e. ManEc 300Day 13 Prof. Bryson Pure Competition.")

149

As soon as the next discussion (on competition) Is complete, we will have a quiz on that topic. Please look at the reading for the next session..

150

The assumptions of pure competition. The assumptions of pure competition. A large number of buyers and sellers A large number of buyers and sellers Product homogeneity Product homogeneity Free entry and exit Free entry and exit

151

The assumption that makes for perfect competition Rapid dissemination of low-cost, accurate information Rapid dissemination of low-cost, accurate information

152

Discuss the standard, market/firm, double diagram of competition. Discuss the standard, market/firm, double diagram of competition. P Q qq q

153

Short-term profits lead to entry. Short-term profits lead to entry. P=MR=AR D S 0 Q P q P S’

154

Entry can impact costs: constant, increasing, decreasing.

155

First, consider an increasing cost industry in pure competition

156

1. Demand Increases 2. Price rises 3. Entry Occurs, pushing S out to the right 4. Costs change as a result of entry, here they rise P=MR=AR D S 0 P q

157

Consider now a decreasing-cost industry in pure competition

158

1. Demand Increases 2. Price rises 3. Entry Occurs, pushing S out to the right 4. Costs change as a result of entry, here they fall P=MR=AR D S 0 P q

159

Finally, consider a constant-cost industry

160

1. Demand Increases 2. Price rises 3. Entry Occurs, pushing S out to the right 4. Costs usually change as a result of entry, but here they remain the same P=MR=AR D S 0 P q

161

TC, TR and NR diagrams for NR>0, NR=0, NR<0.

162

TR TC NR TC NR TC NR

163

When making losses? When shut down? (Go fishing) NR TC TR If we shut down, we must pay? Total Fishing Costs! TFC If we produce, we suffer only our operating losses

164

Why is perfect competition efficient? The consumer pays only the minimal average costs of production. All factors of production get normal opportunity cost returns.

165

Why all cost curves are equal in competition Firm A Firm B Assume Firm A has a production factor that reduces production costs, lowering cost curves Firm B and many others will try to bid that factor away from A. If A doesn’t pay that factor more, It will leave. So A’s cost curves go back up.

166

Quiz on competition Begin monopoly See Power Point presentation Day 15 Review session before midterm. Day 16 Midterm at Testing Center. ManEc 300Day 14 Bryson(Cont’d)

.")

167

1. PowerPoint presentation of monopoly. 2. There will be a multiple choice quiz next class session on monopoly. ManEc 300Day 17 Bryson

168

Discussion on monopoly regulation and contestable markets. ManEc 300Days 18, 19 Prof. Bryson Announcements: In the File Directory, see “Practice Multiple Choice Questions.doc.” At the bottom of the file are references to on-line multiple choice questions for practice and tips on doing them.

169

ManEc 300Day 19 Bryson Competition from a spiritual perspective.. Discussion on Price discrimination Monopolistic competition

170

ManEc 300Day 20 Bryson Begin oligopoly, which will cover The Kinked Demand Curve (see ppt) Baumol’s model of Sales Maximization with a profit constraint, and Game theory

Baumol’s model of Sales Maximization with a profit constraint, and Game theory")

171

Profit constrained sales maximization 4 Goal: maximize total revenue (dollar sales, not physical volume), while making sufficient profit. 4 Sufficient profit –Pays satisfactory dividends –Provides net investment for growth –Ensures financial safety, and –Retains capital market confidence.

172

Baumol on Sales Maximization 4 Oligopoly and the real world X $ 0 TR TC Min ΠNR A We used this model for Monopoly, and it applies here. A = NR or Π max C = Sales max, but with big losses. B = greatest sales that still yield sufficient and minimally required profit. B C

173

Baumol: conclusions 4 This is not really like cost-plus pricing, which produces some output, figures the cost and adds a profit markup. Baumol’s model pre-determines output B as the greatest one that yields sufficient profit.

174

Baumol: conclusions 4 This model incorporates interdependence, which can shift around the TR curve greatly. 4 Lack of emphasis on profit here may help avoid anti-trust action and entry.

175

2. Kinked Demand Curve PowerPoint presentation ManEc 300Day 20 Bryson

176

ManEc 300Session 22 Bryson Conclusion of Oligopoly. Power Point Presentation on Game Theory

177

BOUNDED RATIONALITY AND CONTRACTING ManEc 300Session 22 Bryson 4 The motivation problem. 4 The question here is motivation. Management must assure that the various actors and contract participants actually do their parts, both acting and reporting appropriately.

178

BOUNDED RATIONALITY AND CONTRACTING ManEc 300Session 22 Bryson 4 Incentive Compatibility 4 People will do only what they perceive to be in their interests. Affairs need to be arranged so that while pursuing their own interests, peoples’ actions also promote the interests of the corporation and (from the standpoint of the economist) the interests of the society as well.

the interests of the society as well..")

179

BOUNDED RATIONALITY 4 Perfect, complete contracts. 4 Contracts (or at least voluntary agreements) are the means by which mutual interests are pursued. 4 The motivation problem: all relevant plans cannot be completely described in enforceable contracts. To write a perfect contract, parties would have to foresee all contingencies, then agree on an efficient course of action responding to each one.

are the means by which mutual interests are pursued. 4 The motivation problem: all relevant plans cannot be completely described in enforceable contracts. To write a perfect contract, parties would have to foresee all contingencies, then agree on an efficient course of action responding to each one..")

180

BOUNDED RATIONALITY 4 Perfect, complete contracts. 4 But we must contract with bounded rationality, i.e., – limited foresight, –imprecise language, 4 In the face of bounded rationality, people act in an intentionally rational manner, doing the best they can given these limitations.

181

Contingency Responses 4 Especially when unforeseen contingencies arise, parties often adapt opportunistically. 4 Incomplete and unenforceable contracts lead to problems of imperfect commitment.

182

Contingency Responses 4 Where contingencies are foreseen, impacts and probability of occurrence may be misperceived, so they may not be included in the contract. 4 Contracts usually relatively inflexible, covering many provisions very broadly.

183

Contingency Responses 4 Relational contracting avoids comprehensive contracts –agreement about goals and objectives –general provisions broadly applicable. –Procedures are outlined for making decisions and mechanisms for appeal.

184

Private Information and Adverse Selection 4 In contracting, private information may prohibit a value-maximizing agreement. 4 If private information held by one party we can incur an adverse selection problem.

185

Private Information and Adverse Selection The most famous example of asymmetric information and adverse selection: if the seller of a used car knows it is a lemon, the selection of products (cars) offered in a market is determined in a manner adverse to the buyers’ interests.

offered in a market is determined in a manner adverse to the buyers’ interests.")

186

Pre-contractual Opportunism Adverse Selection 4 Used Cars 4 Insurance (Maternity) 4 Gifthorse, or gifthamster 4 Auto air-conditioner –(Nissan/Calsonic- Harrison Co. A JV no. of Tokyo) Cases of Asymmetric Information 4 Courtship

Cases of Asymmetric Information 4 Courtship.")

187

Market vs. Government Solutions 4 Where AS is strong enough, the price of insurance can be driven so high that nobody can afford it, so that market collapses. No insurer, facing costs of insurance payments, plus overhead, can afford to serve the set of customers who wish to buy insurance.

188

Market vs. Government Solutions 4 George Akerloff (“lemon markets”) showed that the volume of trade in markets with AS is inefficiently low. As we have seen, the market can also fail. That failure often leads to clever alternative arrangements and practices in the private sector. Too often, some advocate that the government jump in with subsidies before seeing what the private market will come up with.

showed that the volume of trade in markets with AS is inefficiently low. As we have seen, the market can also fail. That failure often leads to clever alternative arrangements and practices in the private sector. Too often, some advocate that the government jump in with subsidies before seeing what the private market will come up with..")

189

Adverse Selection in Bank Loans 4 AS in Bank Loans. The interest rates that a bank charges can affect the selection of customers who apply for loans: when there is excess demand for loans, a bank may be inclined to raise its interest rates.

190

Adverse Selection in Bank Loans But at high rates, only those customers with very risky investments may be seeking loans. The bank should ration credit in cases of excess demand, rather than raising the interest rate.

191

Signaling and Screening 4 Signaling is an attempt to communicate private information credibly. 4 Example: –Talented workers may gain additional education as much for the value of credentials as to enhance their actual productivity.

192

Signaling and Screening 4 Screening is done to attract only desirable potential customers, workers, etc. Or, at least to sort groups into quality categories.

193

Signaling and Screening 4 Example: – offering some jobs with incentive pay schemes and others with fixed wages may tend to sort the workers. The most productive ones will tend to select the incentive pay jobs.

194

Alert! For tomorrow, go through the scheduled Power Point on Moral Hazard. We will have a quiz on it. ManEc 300Session 22 Bryson

195

Contract Incomplete, Bounded Rationality Imperfect Commitment Reneging Holdup Problem specific assets co-specialized assets ManEc 300Session 22 Bryson

196

Commitment and Reneging 4 One of the parties to an imperfect contract may try to renege -- payment won’t be made or the product won’t be delivered.

197

Commitment and Reneging 4 Contract ambiguity may make it difficult even to know who is reneging. 4 Fear of reneging may cause a contract not to be completed in the first place.

198

Contract Renegotiation 4 A second commitment problem is that sometimes it becomes necessary to engage in ex post renegotiation of the contract.

199

Contract Renegotiation 4 Example: – Some firms provide incentives to executives by issuing stock options stating they can purchase stock at a specific price on future dates. The managers are supposed to work to get the stock price higher giving them a windfall gain.

200

Contract Renegotiation 4 Example: –But if after the options are issued a firm’s stock price falls drastically, the options are worthless and won’t provide incentives. So it will pay to renegotiate.

201

The Hold-up Problem 4 Where both parties to a contract need to worry about being forced to accept disadvantageous terms later, after it has sunk resources into an investment, there is a hold-up problem.

202

The Hold-up Problem 4 The problem: specific use of particular assets in imperfect contracting. 4 Fearing that a big investment may lead to later vulnerability can lead to a refusal to make the efficient investment.

203

The Hold-up Problem: Example 4 If a coal mine supplies a local power plant (as its only customer) and a big investment is required, will the relationship continue after the expensive investment? What will the price of coal be in the future?

204

The Hold-up Problem: Example 4 Post-contractual opportunism may result, so parties can exploit loopholes to gain unfair advantage. A common response to a cospecialized assets problem is for the same party or firm ultimately to own both assets.

205

Is this acceptable business behavior? Is this fair behavior? Is this OK behavior? Is this behavior we all engage in? Is this moral behavior? Read George Q. Cannon Statement We should critically evaluate opportunistic behavior

206

George Q. Cannon on Informational Asymmetry 4 Collected Discourses, Vol.5, George Q. Cannon, October 6, 1895 I might go on and speak about stealing, and dishonesty, and many other sins. I believe that the Latter-day Satins as a people are a more honest people, that they respect their obligations more than other people.

207

George Q. Cannon on Informational Asymmetry 4 Collected Discourses, Vol.5, George Q. Cannon, October 6, 1895 We show this in our business associations and dealing. We have the credit for it everywhere. Men who have found fault with our religion frequently acknowledge that we are an honest people, and our credit is "gilt edged." But there are some things that we are still guilty of.

208

George Q. Cannon on Informational Asymmetry I believe, however, that the young and rising generation will outgrow them. It is a strong temptation for a man, when he has got a piece of property and he has a chance to trade or sell it, to let the buyer think it is better than it is.

209

George Q. Cannon on Informational Asymmetry Now, if we were strictly honest, we would tell exactly the character of that which we have to sell. We would not allow a man to deceive himself; we would tell him the facts. But I know that we are all under the influence of the old traditions.

210

George Q. Cannon on Informational Asymmetry 4 The old traditions were that a man should have his own eyesight, and that the seller should not furnish him with anything to aid his perception or to enable him to perceive something that he would not otherwise see. It is a hard thing for men who have grown up under that system of things to refrain from it.

211

George Q. Cannon on Informational Asymmetry 4 You see everywhere where things are for sale the endeavor to make them appear better in the eyes of the purchaser than they are. We have got to change in this respect. Whenever a man yields to do a dishonest thing he yields to Satan, and Satan has influence and power over him to that extent. We have got to learn to overcome these things, and to have Satan bound.

212

Suggestion: Begin Reviewing for Final 4 In just a few days we will have an in- class review for the final. Please bring your questions to that session for discussion. 4 Tomorrow there will be a quiz on moral hazard.

213

Post-contractual Opportunism: Moral Hazard, Session 24 The definition: MH is the form of post-contractual opportunism that arises because actions that have efficiency consequences are not freely observable and so the person taking them may choose to pursue his or her private interests at others’ expense.

214

Post-contractual Opportunism: Moral Hazard, Session 24 The term originated in the insurance industry, where the tendency of people was observed to change their behavior in a way that led to larger claims against the insurance company (e.g., being lax about taking precautions to avoid or minimize losses).

.")

215

Commitment vs. Monitoring Shirking, Fraud/Deceit. In the case of the residual claimant, who monitors the monitor? South African Hosp AMA, Doctors vs. Litigation ManEc 300Day 24 B ryson

216

Principle-agent relationship Case of US Savings & Loan Crisis S&L’s borrow from savers, loan for mortgages-- low interest rates FSLIC Insurance 1980’s Fed Interest Rates Deregulation (cease monitoring) ManEc 300Day 24 Bryson

ManEc 300Day 24 Bryson")

217

S&LS CONTINUED: Fraud (25% of S&L bankruptcies) Depositors didn’t monitor (insured) Politicians wouldn’t monitor ManEc 300Day 24 Bryson

Depositors didn’t monitor (insured) Politicians wouldn’t monitor ManEc 300Day 24 Bryson")

218

Note public insurance examples: Gov. Nat’l Mortgage Association (GNMA)--insurance against default Student Loans ManEc 300Day 24 Bryson

--insurance against default Student Loans ManEc 300Day 24 Bryson.")

219

Economic Strategy and Michael Porter See and discuss Power Point, “Bryson on Porter” The firm’s competitive advantage 2.The Gershwin-playing hamster ManEc 300Day 25 Bryson

220

ManEc 300Days 26, 27 Bryson 4 Discussion of 4 Organizational Architecture.ppt 4 Review for final.

221

A little final math practice Suppose a firm’s TR is given as TR = 500Q - 4Q2 When output is 100, TR is When output is 100, TR is a. $2,000.b. $20,000.c. $10,000. d. $49,600.e. None of the above.

222

Suppose a firm’s TR is given as TR = 500Q - 4Q2 When output is 10 units, AR is When output is 10 units, AR is a. $460.b. $560c. More than $500 d. $360e. None of the above

223

When TR = 500Q - 4Q2 When TR = 500Q - 4Q2 At an output level equal to 20, MR is a. $440.b. $340c. More than 500. d. None of the above.

224

Marginal revenue Marginal revenue a. always exceeds marginal cost. b. always equals marginal cost. c. is the tangent of the average revenue curve. d. is the slope of the total revenue curve. e. is the distance between total revenue and total cost curves at optimal output.

225

When TR = 500Q - 4Q2 Marginal revenue and average revenue are equal when a. Q = 10.b. Q = 0.c. Q > 0. d. Q < 0.e. None of the above.

Similar presentations

Firm’s costs of production: Accounting costs: actual dollars spent on labor, rental price of bldg, etc. Economic costs: includes.>")