Download presentation

Presentation is loading. Please wait.

1

Billing Schemes

2

O C C U P A T I O N A L F R A U D a n d A B U S E C L A S S I F I C A T I O N S Y S T E M

3

Asset Misappropriations Cash (90%) Inventory and Other Assets Skimming (28.9%) Larceny (4.1%) Fraudulent Disbursements (67.0%)

Inventory and Other Assets Skimming (28.9%) Larceny (4.1%) Fraudulent Disbursements (67.0%)")

4

Fraudulent Disbursements Billing Schemes Payroll Schemes Check Tampering Expense Reimb. Register Disbursmts.

6

Finally, most fraudulent disbursements fall into one of the above five categories.

8

What Are Billing Schemes? Schemes attacking purchasing function Cause organization to buy goods/services that are nonexistent, overpriced, or not needed Perp submits bogus invoice or other support Victim organization issues a check Perp collects payment

9

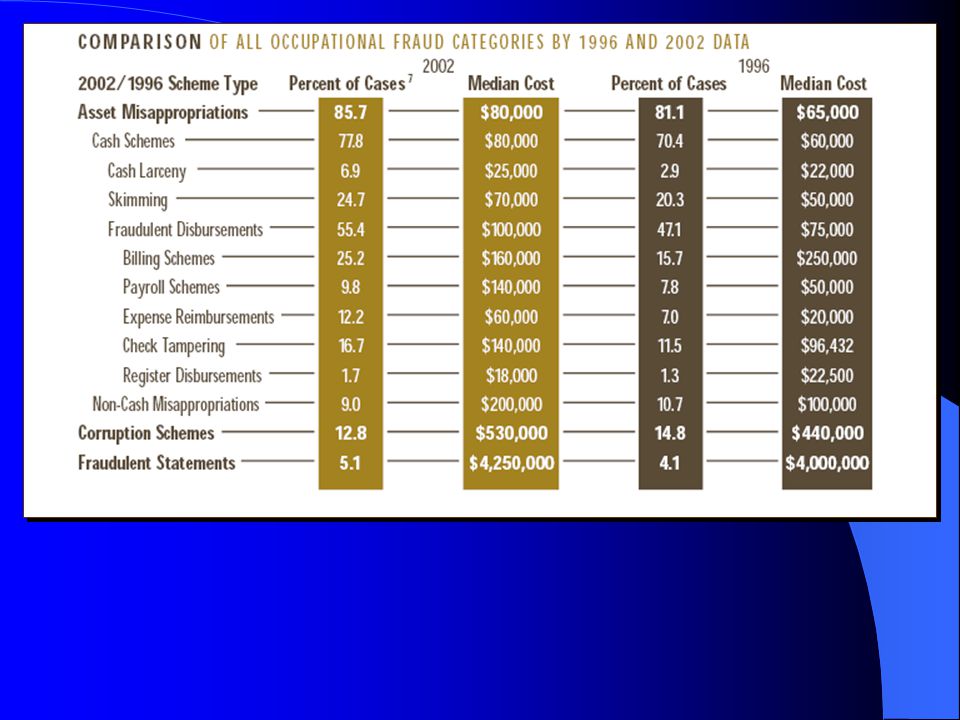

Billing Schemes 244 billing schemes were reported, with a median loss of $250,000. Billing schemes are the most common and most costly form of fraudulent disbursement.

10

Common Billing Schemes Shell company schemes Non-accomplice vendor schemes Personal purchases with company funds

11

Billing Schemes – Breakdown of Cases Of 244 billing schemes reported, over 90% were either personal purchases or shell company schemes. Billing schemes are the most common form of fraudulent disbursement.

12

Billing Schemes - Median Losses

13

Shell Company Schemes What is a shell company? Fictitious entity Created for purpose of committing fraud Only exist on paper Usually consist of bank account and mail drop Generally registered with state or county (perp needs registration to open bank account)

.")

14

Shell Company Schemes Usually invoice for services, not goods – Services not tangible, harder to verify How shell company invoices get paid: – Perp has authority to approve payment – Supervisor “rubber stamps” purchases – Perp prepares bogus support documents – Collusion among several employees

15

Shell Company Schemes Pass-through schemes: Variation of standard shell company scheme Perp assigned to purchase goods/services for company Uses shell company to buy the items on credit Shell company sells items to employer at inflated price Pays off shell’s credit, excess is profit

16

Shell Company Schemes – Countermeasures Question invoices that have residential address or mail drop for mailing address Look for invoices with lack of detail – Missing phone #, fax #, invoice #, tax id, etc. Investigate invoices with no sales tax Sort payments by vendor, look for: – Consecutive invoice numbers – Consistent payment amounts, round numbers

17

Shell Company Schemes – Countermeasures If suspicions about vendor arise: – Look up vendor in phone book – Contact others in industry – Visit address to verify existence – Independently verify delivery before paying Periodically run comparison reports between vendor/employee addresses Maintain up-to-date vendor list

18

Identifying the Perpetrator of a Shell Company Scheme Check articles of incorporation, dba Conduct surveillance on mail drop Review support: who requests, authorizes purchases? Review cancelled checks for bank acct info Don’t pay invoice, see who follows up Search workstation of suspect for evidence

19

Billing via Non-accomplice Vendors Perp overbills company on behalf of existing vendor Vendor not involved in the scheme Two common techniques: – Pay-and-return – Counterfeit invoices

20

Billing via Non-accomplice Vendors Pay-and-return scheme: Controls over returned checks may be more lax than outgoing checks Perp double-pays invoice, sends check to wrong address, etc. Tells recipient a mistake was made Asks for check back Steals the returned payment

21

Billing via Non-accomplice Vendors Counterfeit invoices: Perp generates bogus invoices, similar to existing vendor’s Easy to do with desktop publishing Company cuts check Perp steals check or has it delivered to mail drop

22

Non-Accomplice Vendors – Countermeasures Sort invoices by vendor, look for unusual invoice numbers, change in address or style Mail checks immediately after signing Restrict access to accounts payable records and addresses Investigate excessive purchases from particular vendor

23

Non-Accomplice Vendors – Countermeasures Independently spot-check purchases with vendors Install system to prevent duplicate payments Require all incoming mail to be opened by mailroom; all incoming checks logged (to prevent pay-and-return) Instruct bank not to cash checks payable to organization

Instruct bank not to cash checks payable to organization")

24

Personal Purchases with Company Funds Perp uses company checks to buy personal items. Common examples: – Home supplies/construction – Side business – Pay medical, utility, credit card bills, etc. Merchandise may be returned for cash

25

Personal Purchases with Company Funds Methods of payment: Perp has approval authority for invoices Altered or bogus support documentation Initiate fraudulent purchase requisitions Buy on running accounts/purchase orders Use company credit card

26

Personal Purchases – Countermeasures Require all purchases to be delivered to centralized receiving department Separate purchasing and receiving functions Investigate any purchases that are ordered drop- shipped to unusual location Question purchases that do not appear to have a business purpose Review any purchases made without management approval

27

General Billing Scheme Red Flags Invoices cannot be traced to shipments Multiple payments to single vendor on same date Pattern of purchases just below review level Unusually quick turnaround on invoices Departments/employees consistently over budget Payments to multiple vendors for same product

28

General Billing Scheme Red Flags Extreme inventory shortages Expenses increase dramatically Unexplained rise in cost of goods sold Unexplained decrease in gross/net profits Excessive materials orders Goods not purchased at optimal point High level approval of a low level transaction

29

Billing Schemes Controls Invoices, purchase orders and receiving reports must be matched before payment issued Purchasing department should be independent of: – Receiving – Shipping – Accounting

30

Billing Schemes Controls Purchases must have management approval Maintain a current approved vendor list Use competitive bids for major purchases Vendor purchases should be reviewed for abnormal levels Control methods should be implemented for duplicate invoices/purchase orders

Similar presentations

Runyon Kersteen Ouellette.>")