Download presentation

Presentation is loading. Please wait.

1

Insurance Institutions

2

I. Introduction A. Type of Insurance 1. Social Insurance 2. Private Insurance American System –Life Insurance –Property/Casualty Insurance European System

3

B. Risk 1. Outcome Pure Risk The outcome can only be a loss or no loss with no possibility for gain. Speculative Risk Uncertainty about an event could result in either a gain or a loss.

4

2. Insurability Statistical Concepts –Law of Large Numbers –Measurable Objective Risk Objective risk is the deviation of actual losses from expected losses and can be measured statistically.

5

Commercial Insurability –Homogeneous exposure units There is a large number of homogeneous exposure units so that losses can be predicted on the law of large numbers. –Accidental and unintentional occurrence The law of large numbers is based on randomness.

6

–Identifiable circumstances of loss The time, location, cause, and amount should be identifiable. –Calculable probability of loss The is required for the purpose of calculating premium.

7

–Non-catastrophic loss A large portion of the exposure units should not experience a loss at the same time. –Affordable premium This is to ensure a sizable market.

8

II. Life Insurance Companies A. Industry Structure 1. Insurers By Organizational Form –Stock Life Insurance Companies –Mutual Life Insurance Companies –Fraternal Life Insurance Companies –Government Agencies –Mutual Savings Banks

9

By Reserve Requirement –Legal Reserve Companies –Assessment Insurance Companies By Reinsurance –Primary Companies (Ceding Companies) –Reinsurance Companies

–Reinsurance Companies")

10

2. Distribution Network Branch Offices General Agencies Direct Mail

11

B. Financial Operations 1. Life Insurance Policies By Purpose –Risk

12

–Term Insurance Duration 1-year, 3-year, 5-year, 10-year Face Amount Constant term, decreasing term, increasing term Expiration Protection Renewable term, convertible term

13

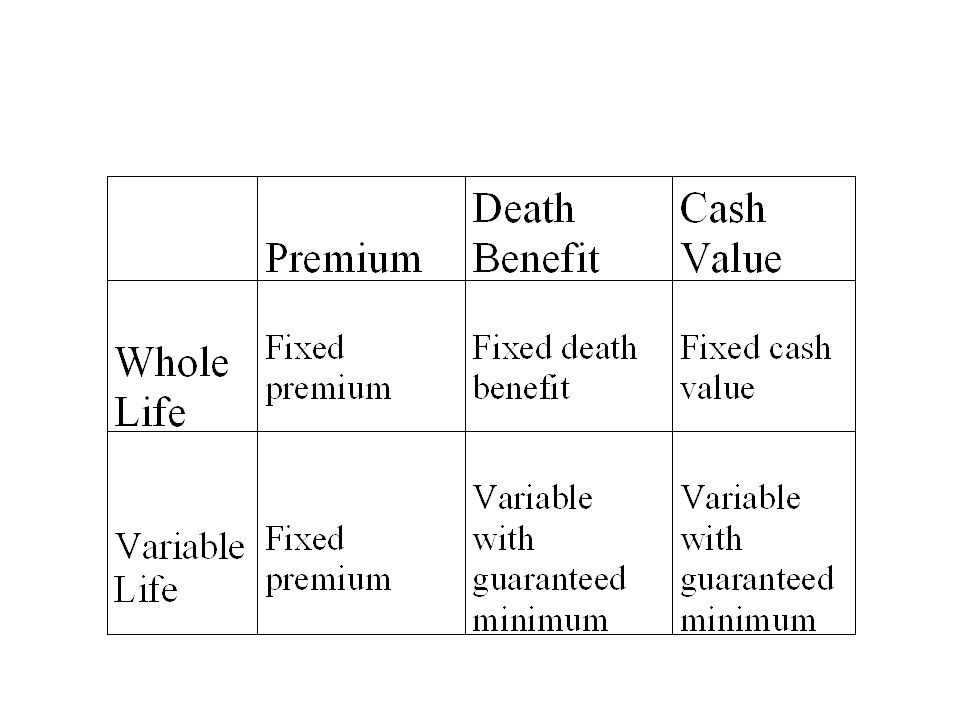

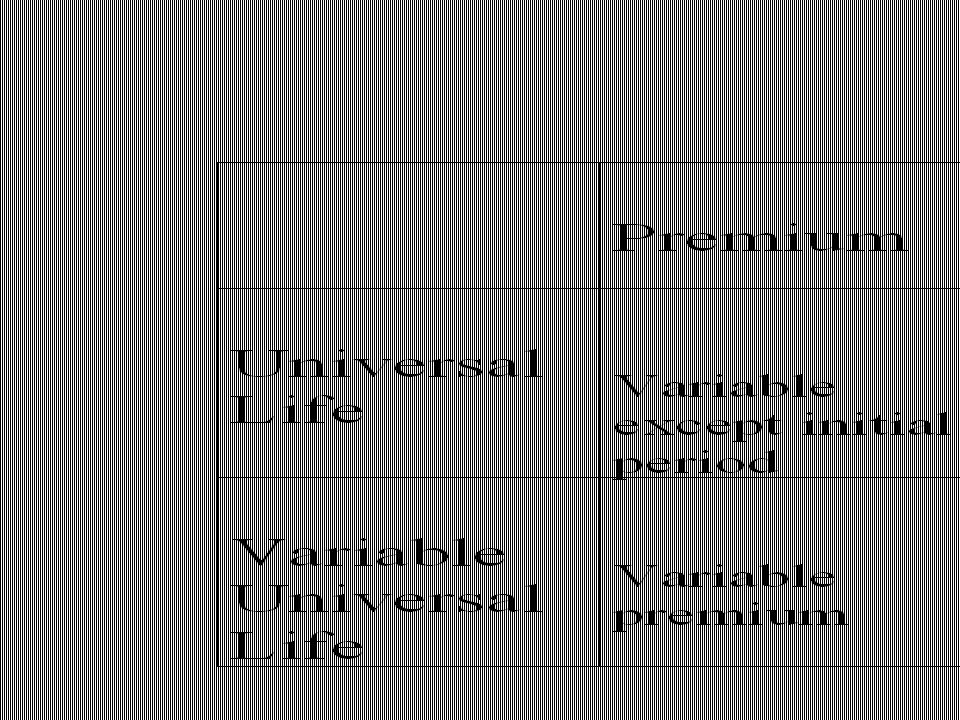

–Risk/Investment Endowment Life Whole Life (Straight Life) Variable Life Universal Life Variable Universal Life (Universal Life II) Single Premium Life

Variable Life Universal Life Variable Universal Life (Universal Life II) Single Premium Life")

16

By Market Segment –Individual Life (Ordinary Life) –Business Life –Group Life –Credit Life –Industrial Life (Home Service Life)

–Business Life –Group Life –Credit Life –Industrial Life (Home Service Life)")

17

By Dividend Received –Participating Contract (rec. dividends) –Non-Participating Contract (no dividend)

–Non-Participating Contract (no dividend).")

18

2. Annuity 3. Health Insurance 4. Investments Corporate Bonds Mortgages Government Securities

19

C. Regulations National Association of Insurance Commissioners (NAIC) Insurance Regulatory Information System

Insurance Regulatory Information System.")

20

III. Property/Casualty Insurance Companies A. Industry Structure 1. Insurers By Ownership –Stock Companies –Mutual Companies –Reciprocals (Interinsurance Exchanges) –Domestic Lloyd

–Domestic Lloyd.")

21

By Corporate Control –Independent Companies –Captive Companies

22

By Premium Assessment –Assessment Companies –Non-Assessment Companies

23

By Reinsurance –Primary Companies (Ceding Companies) –Reinsurance Companies

–Reinsurance Companies")

24

2. Distribution Network Branch Offices General Agencies Direct Mail

25

B. Financial Operations 1. Property/Liability Policies By Parties Covered – First Person Insurance –Third Party Liability Insurance

26

By Pattern of Loss Payments –Short-Tailed Insurance Lines –Long-Tailed Insurance Lines

27

By Risk Category –Property Insurance Named Peril Policies A named peril policy cover perils that are specifically named, such as lightning, flood, theft, etc.

28

All-Risk Policies (Open Perils) An all risk policy protect the insured against loss from all perils except those specifically excluded.

An all risk policy protect the insured against loss from all perils except those specifically excluded.")

29

–Liability Insurance –Marine Insurance Ocean Marine Insurance Inland Marine Insurance –Multiline Policies A multiline policy contain both property and liability insurance coverages. Examples include homeowner’s policies and personal auto policies.

30

–Surety Insurance –Fidelity Insurance

31

2. Health Insurance 3. Investments Corporate stocks Revenue bonds Corporate bonds U. S. government securities C. Regulations

32

IV. Trends A. Bancassurance Cross-Sectoral Investing (i.e., crossing industry lines) Interpenetration of Markets (i.e., merges and acquisitions) Cooperative Arrangement (i.e., cooperating between independent banks and insurance companies)

Interpenetration of Markets (i.e., merges and acquisitions) Cooperative Arrangement (i.e., cooperating between independent banks and insurance companies).")

33

B. Cross-Border Activities Mergers and Acquisitions Branching

34

V. Social Insurance A. Institutions Social Security Administration, Department of Health and Human Services Bureau of Employment Security, Department of Labor Bureau of Employees’ Compensation, Department of Labor

35

B. Financial Operations Old-Age, Survivor, Disability, and Health Insurance (OASDHI) Unemployment Insurance Worker’s Compensation

Unemployment Insurance Worker’s Compensation.")

Similar presentations

as implemented by the U.S. Department.>")

life and health and 2) property and casualty n Describe.>")