Download presentation

Presentation is loading. Please wait.

1

Understanding Indirect Costs

REC Infrastructure Retreat April 7, 2015 Nancy L. Wilkinson, Office of the Dean for Research (IFAS)

")

2

Understanding Indirect Costs– Today’s Agenda

Definition Key Concepts – Facilities & Administrative Facilities & Administrative Cost Pool Elements F&A Formula Examples with and without Cost Sharing UF Rate Agreement – comparisons to Peer Institutions UF/IFAS Distribution of IDC annually On vs. Off Campus Your Questions Next TOPIC ---- Capacity Funds

3

What are Indirect Costs? – Definition

Costs that cannot be specifically identified to a sponsored activity Typically this cost is known as “Facilities & Administrative (F&A) Costs” UF uses different lingo – IDC Formula is used to determine the F&A “rate” at UF Prepared by Cost Analysis UF calculations are submitted to Federal government (so called cognizant agency) for negotiations Our “approved” F&A Rate Agreement is less than actual costs incurred DHHS negotiates down Even if we are paid the “full” federally negotiated rate - it is less than UF’s actual costs

Costs UF uses different lingo – IDC. Formula is used to determine the F&A rate at UF. Prepared by Cost Analysis. UF calculations are submitted to Federal government (so called cognizant agency) for negotiations. Our approved F&A Rate Agreement is less than actual costs incurred. DHHS negotiates down. Even if we are paid the full federally negotiated rate - it is less than UF’s actual costs.")

4

Key Concept for F&A Rate

Facilities (examples) Building Depreciation PO&M Interest Expense on Capital Items Bond Payments Administrative (examples) General Administration Department and College Administration Sponsored Project Administration There are both allowable and unallowable activities and charges in Section J; it is important to note that if a particular item was not on the list, it does not imply that it is either allowable or unallowable; if you are uncertain, review the agency terms and conditions as well as the approved budget to see it the charge is allowed. ***Note that just because the agency approved the purchase does not mean it is allowable.*** Allowable charges : Travel, Lab Supplies, Approved and allowable equipment Now that we have determine the cost to be reasonable and allowable, lets now look at the allocability of an expense Strategies: Fully depreciated buildings used for Administrative purposes Building divided into components (building shell, service systems, fixed equipment, etc.) with various depreciation schedules Limited

Building Depreciation. PO&M. Interest Expense on Capital Items. Bond Payments. Administrative (examples) General Administration. Department and College Administration. Sponsored Project Administration. There are both allowable and unallowable activities and charges in Section J; it is important to note that if a particular item was not on the list, it does not imply that it is either allowable or unallowable; if you are uncertain, review the agency terms and conditions as well as the approved budget to see it the charge is allowed. ***Note that just because the agency approved the purchase does not mean it is allowable.*** Allowable charges : Travel, Lab Supplies, Approved and allowable equipment. Now that we have determine the cost to be reasonable and allowable, lets now look at the allocability of an expense. Strategies: Fully depreciated buildings used for Administrative purposes. Building divided into components (building shell, service systems, fixed equipment, etc.) with various depreciation schedules. Limited.")

5

What are Indirect Costs? – Facilities Cost Pool

Determination of Cost Pools and Distribution Base all governed by federal regulations “Facilities” cost pools are typically: Building Depreciation Equipment Depreciation Capital Improvements to Land and Buildings at UF Plant Operation and Maintenance costs Interest expense on capital expenditures Library costs (building)

")

6

What are Indirect Costs? – Administrative Cost Pools

“Administrative” cost pools are typically: General University Administration UF President; VP’s; CFO; HR; Development; Department/College Administration Deans; Departments; Centers Sponsored Projects Administration Division of Sponsored Programs; Contracts & Grants; Cost Analysis Interest expense on capital expenditures Library costs for administration Limited – cannot exceed 26%

7

What are Indirect Costs? – Formula

1 year of Facilities Pools (Building & Equipment Depreciation + PO&M + Interest Expense + Library costs) PLUS + 1 year of Administrative Pools (University Administration + Sponsored Programs Admin. + Colleges/Departments) 1 year of Expenditures on Research Grants (Funds 201 and 209) Cost Sharing Numerator Denominator

PLUS + 1 year of Administrative Pools (University Administration + Sponsored Programs Admin. + Colleges/Departments) 1 year of Expenditures on Research Grants (Funds 201 and 209) Cost Sharing. Numerator. Denominator.")

8

What are Indirect Costs? – Example

Facilities Pools - $150,000,000 + +Administrative Pools $250,000,000 =$400,000,000 Expenses on Sponsored Programs = $800,000,000 Rate = 50% Numerator Denominator

9

What are Indirect Costs? – Example including C/S

Facilities Pools - $150,000,000 + +Administrative Pools $250,000,000 =$400,000,000 Expenses on Sponsored Programs = $800,000,000 + Cost Sharing =$200,000,000 =$1,000,000,000 Rate = 40% Cost Sharing impact is to reduce F&A Rate Numerator Denominator

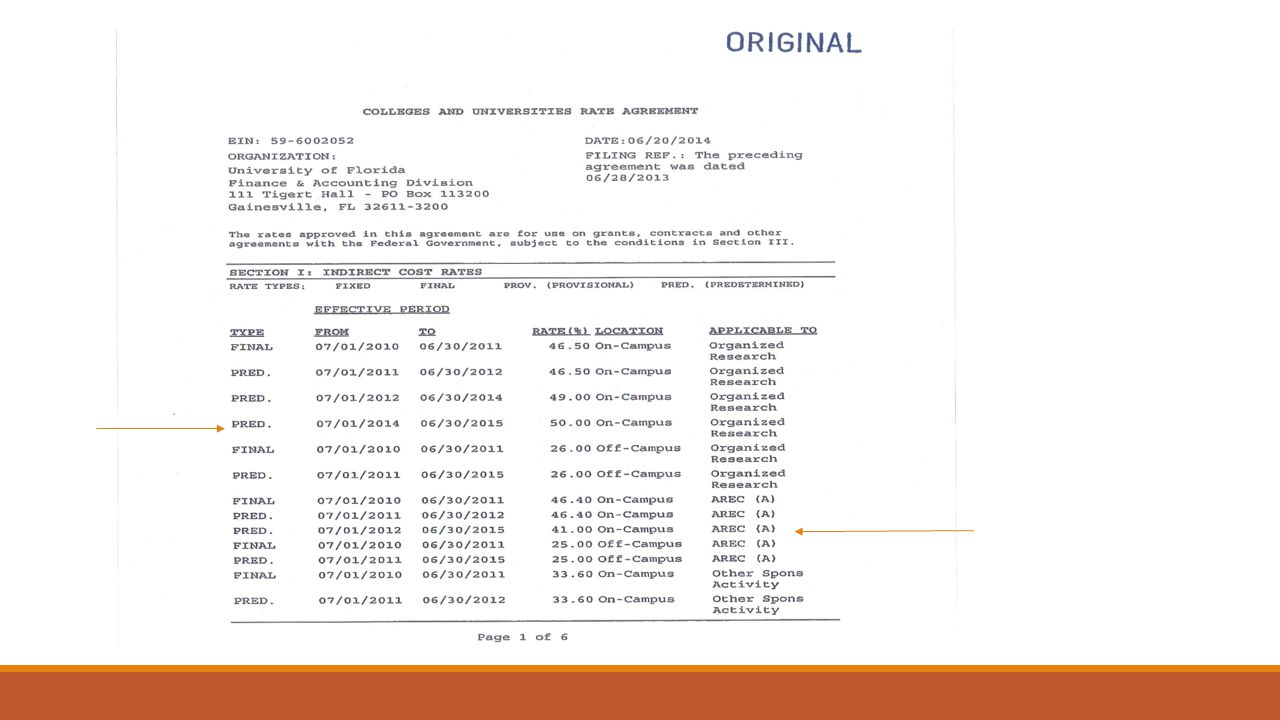

11

What are Indirect Costs? – Comparison to Peers

F&A Rates Research (on campus) University of Minnesota 52 University of Florida 50 Ohio State University 54 Penn State University 50.7 U California - Davis 55.5

University of Minnesota. 52. University of Florida. 50. Ohio State University. 54. Penn State University U California - Davis")

12

Indirect Costs Distribution – Within IFAS

IDC Expenses in Fund 201 (Federal) & 209 (non-Federal) accumulated by Contracts & Grants (CnG) Total is “earned” IDC to IFAS 2014 IDC Earnings $10,904,855 RCM $5,099,298 Net to IFAS $5,805,557 47% of earnings to RCM

& 209 (non-Federal) accumulated by Contracts & Grants (CnG) Total is earned IDC to IFAS IDC Earnings. $10,904,855. RCM. $5,099,298. Net to IFAS. $5,805, % of earnings to RCM.")

13

Indirect Costs Distribution – IFAS Distribution Percentages

IFAS Approved Centers 2/3 from Sr. VP 1/3 from Dean 50% Sr. VP 25% Dean(s) 15% Unit Leader(s) 10% PI

15% Unit Leader(s) 10% PI.")

14

Key Concept for On/Off Campus

On Campus (criteria) UF Owned Facility Does not have to be the Gainesville campus Off Campus (criteria) Non UF Facility Budget includes– rental costs Remember - there is no “facility” cost in the IDC It is not about geography!!! There are both allowable and unallowable activities and charges in Section J; it is important to note that if a particular item was not on the list, it does not imply that it is either allowable or unallowable; if you are uncertain, review the agency terms and conditions as well as the approved budget to see it the charge is allowed. ***Note that just because the agency approved the purchase does not mean it is allowable.*** Allowable charges : Travel, Lab Supplies, Approved and allowable equipment Now that we have determine the cost to be reasonable and allowable, lets now look at the allocability of an expense

UF Owned Facility. Does not have to be the Gainesville campus. Off Campus (criteria) Non UF Facility. Budget includes– rental costs. Remember - there is no facility cost in the IDC. It is not about geography!!! There are both allowable and unallowable activities and charges in Section J; it is important to note that if a particular item was not on the list, it does not imply that it is either allowable or unallowable; if you are uncertain, review the agency terms and conditions as well as the approved budget to see it the charge is allowed. ***Note that just because the agency approved the purchase does not mean it is allowable.*** Allowable charges : Travel, Lab Supplies, Approved and allowable equipment. Now that we have determine the cost to be reasonable and allowable, lets now look at the allocability of an expense.")

15

Questions & Comments?

16

Capacity (Formula)Funds in Fund 221/222

REC Infrastructure Retreat April 7, 2015 Nancy L. Wilkinson, Office of the Dean for Research (IFAS)

")

17

Capacity Funds– Today’s Agenda

Definition Submission and Award Process New Uniform Guidance regulations (A-81) Specific restrictions Cost Principles Allowable, Reasonable & Necessary, Allocable IFAS Management Your Questions

Specific restrictions. Cost Principles. Allowable, Reasonable & Necessary, Allocable. IFAS Management. Your Questions.")

18

Capacity Funds–Definition

Capacity Funds (used to called Formula Funds) are VERY RESTRICTIVE. More than the typical USDA NIFA award. Fund 221 – Research based capacity funds Hatch Regular Hatch Multistate McIntire-Stennis Animal Health Fund 222 – Extension based capacity funds Smith-Lever Expanded Food & Nutrition Education Program (EFNEP) Renewable Resources Extension Act (RREA) Civil Service Retirement System (CSRS)

are VERY RESTRICTIVE. More than the typical USDA NIFA award. Fund 221 – Research based capacity funds. Hatch Regular. Hatch Multistate. McIntire-Stennis. Animal Health. Fund 222 – Extension based capacity funds. Smith-Lever. Expanded Food & Nutrition Education Program (EFNEP) Renewable Resources Extension Act (RREA) Civil Service Retirement System (CSRS)")

19

(FGO) Issued with deadline to submit application

Funding Grant Opportunity Submit Application (via Cayuse) to Grants.Gov Award Face Sheet is issued to UF

to Grants.Gov. Award Face Sheet is issued to UF.")

20

Capacity Funds– new Uniform Guidance (A-81)

2 CFR Part 200 – Uniform Guidance Subpart A – Acronyms and Definitions Subpart B – General Provisions (200.1xx) Subpart C – Pre Award Requirements (200.2xx) Subpart D – Post Award Requirements (200.3xx) This was OMB Circular A-110 Administrative Requirements Subpart E – Cost Principles (200.4xx) This was OMB Circular A-21 Cost Principles Subpart F– Audit Requirements (200.5xx) This was OMB Circular A-133 Audit Requirements

Subpart C – Pre Award Requirements (200.2xx) Subpart D – Post Award Requirements (200.3xx) This was OMB Circular A-110 Administrative Requirements. Subpart E – Cost Principles (200.4xx) This was OMB Circular A-21 Cost Principles. Subpart F– Audit Requirements (200.5xx) This was OMB Circular A-133 Audit Requirements.")

21

Terms and Conditions Office of Management and Budget

This Award incorporates the following: 1. Application in response to FY 2015 RFA. 2. Formula Grants Terms and Conditions, 3. General Provisions, 2 CFR Part 400, Uniform Administrative Requirements, Cost Principles, and Audit Requirements adopts 2 CFR Part incorporated by reference. 2 CFR Part adopts subparts A through F of 2 CFR Part 200; and 2 CFR Part includes USDA department-wide conflict of interest policy in compliance with 2 CFR Part 4. Administrative Manual for Hatch Act Funds 5. Administrative Guidance for Multistate Extension and Integrated Activities 6. Guidelines for State Plans of Work 7. Stakeholder Input Regulation (7 CFR 3418) 8. This award will reach the statutory time limitation on 09/30/2016, the end date of this project. No-cost extensions of time will not be possible. 9. One hundred percent matching is required for this award. All matching must directly benefit and be specifically identifiable with approved project objectives. The awardee is required to maintain complete, accurate, up-to-date records to support all matching activities under the award. Matching requirements may not be satisfied with Federal funds or with property or services provided under another Federal assistance award. Terms and Conditions Office of Management and Budget 2 CFR Chapter I, Chapter II, Part 200, et al. Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards; Final Rule

8. This award will reach the statutory time limitation on 09/30/2016, the end date of this project. No-cost extensions of time will not be possible. 9. One hundred percent matching is required for this award. All matching must directly benefit and be specifically identifiable with approved project objectives. The awardee is required to maintain complete, accurate, up-to-date records to support all matching activities under the award. Matching requirements may not be satisfied with Federal funds or with property or services provided under another Federal assistance award. Terms and Conditions. Office of Management and Budget. 2 CFR Chapter I, Chapter II, Part 200, et al. Uniform Administrative Requirements, Cost Principles, and Audit. Requirements for Federal Awards; Final Rule.")

23

Big Picture – Key Concepts for Spending

Expense must be: Allowability ( ) Reasonable and Necessary for the performance of the project ( ) Allocable to the project ( )

Reasonable and Necessary for the performance of the project ( ) Allocable to the project ( )")

24

Big Picture – Key Concepts for Spending

What is Allowable? Must be necessary and reasonable for the performance Consistently treated expense in like circumstance Cannot be included as a cost to meet cost sharing or matching of any other federal award For RESEARCH capacity funds – must have an active REEport project too!

25

Big Picture – Key Concepts for Spending

What is Reasonable & Necessary? Regulations tell us that a cost is reasonable and necessary if the expense doesn’t exceed that cost incurred by a “prudent person under the circumstances prevailing at the time the decision was made to incur the cost.” Generally recognized as ordinary and necessary Use “market prices for comparable goods or services in the geographic area”

26

Big Picture – Key Concepts for Spending

Is the expense Allocable? Is the expense assignable to this award in accordance with the relative benefits received? (c) Any cost allocable to a particular Federal award under the principles provided for in this part may not be charged to other Federal awards to overcome fund deficiencies, to avoid restrictions imposed by Federal statutes, regulations, or terms and conditions of the Federal awards, or for other reasons (d) Direct cost allocation principles. If a cost benefits two or more projects or activities in proportions that can be determined without undue effort or cost, the cost must be allocated to the projects based on the proportional benefit. If a cost benefits two or more projects or activities in proportions that cannot be determined because of the interrelationship of the work involved, then, notwithstanding paragraph (c) of this section, the costs may be allocated or transferred to benefitted projects on any reasonable documented basis. Determining that methodology is the key!

Any cost allocable to a particular Federal award under the principles provided for in this part may not be charged to other Federal awards to overcome fund deficiencies, to avoid restrictions imposed by Federal statutes, regulations, or terms and conditions of the Federal awards, or for other reasons (d) Direct cost allocation principles. If a cost benefits two or more projects or activities in proportions that can be determined without undue effort or cost, the cost must be allocated to the projects based on the proportional benefit. If a cost benefits two or more projects or activities in proportions that cannot be determined because of the interrelationship of the work involved, then, notwithstanding paragraph (c) of this section, the costs may be allocated or transferred to benefitted projects on any reasonable documented basis. Determining that methodology is the key!")

27

Capacity Funds– Management within IFAS

Block Tuition Remission – prohibited Require REEport project (CRIS) value for each expense in the Research Capacity Funds CAS Exemptions will not be requested from the Division of Sponsored Programs (DSP) Effort reported is aligned to salary charged on Capacity Funds Working on fine tuning Cost Sharing to ensure detailed tracking

value for each expense in the Research Capacity Funds. CAS Exemptions will not be requested from the Division of Sponsored Programs (DSP) Effort reported is aligned to salary charged on Capacity Funds. Working on fine tuning Cost Sharing to ensure detailed tracking.")

28

Questions & Comments?

Similar presentations

Presented by Beverly Blakeney, Diane Cummings and Julie Macy.>")

>")

Cost Recovery Report April 22, 2009 Carol Hollingsworth, Director, Grants & Contracts Financial Services & Janet Parker,>")

Cost Recovery March 5, 2009.>")