Download presentation

Presentation is loading. Please wait.

1

chapter 24 Completing the Audit

2

Elaine describe what is meant by Interim Testing.

3

A B C D interim date report issued balance sheet end of field work

date on end of field work report date date report issued interim 12/31/14 A B C D 3

4

A B C D interim date report issued balance sheet end of field work

date on end of field work report date date report issued interim 12/31/14 A B C D 4

5

Contingent Liabilities / Attorney’s Letter

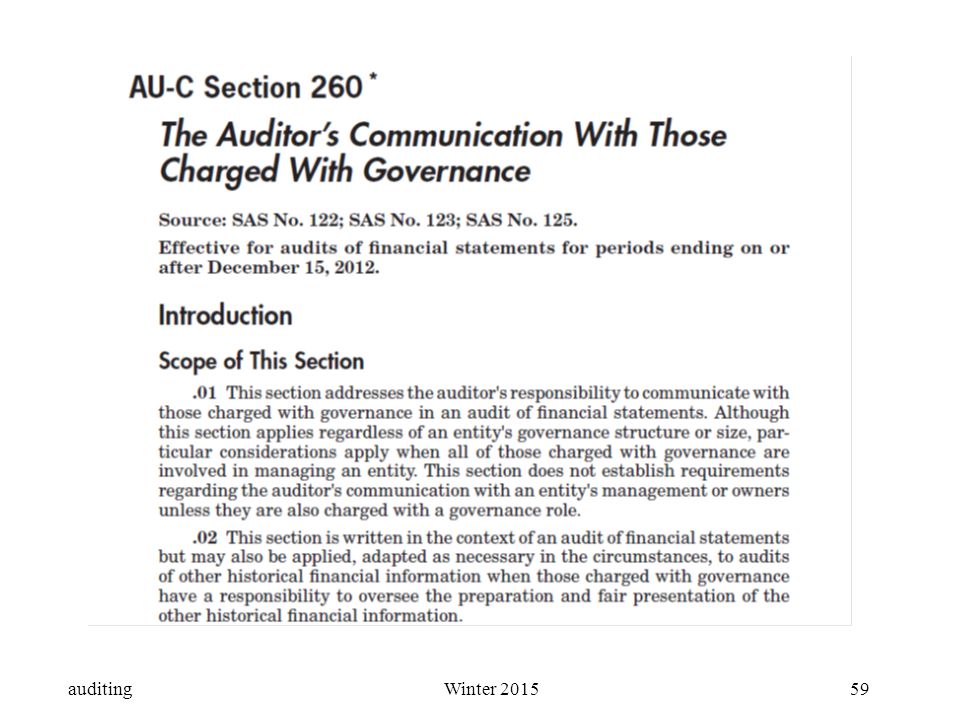

Subsequent Events Management Representations analytical procedures Final assessment of audit risk - opinion communications to audit comm or mgmt AU-c 260 Communication with Those Charged with Governance AU-c 265 Communicating Internal Control Related Matters Identified in an Audit subsequent discovery of facts

6

unrecorded liabilities

examining subsequent payments to suppliers and other creditors to ensure that they were correctly recorded. almost $5 million of purchases applicable to Dec. 31 audit period that had not been included as liabilities.

7

Contingent Liabilities / Losses

A potential future payment to an outside party from an existing condition Uncertainty about the amount Outcome will be resolved by future events

8

Contingent Liabilities / Losses

Lawsuits are an example of a contingency Income tax disputes Product warranties Guarantees of the debts of others

9

Steve what does SFAS No. 5 (ASC 450) teach us about

contingent losses or contingent liabilities

10

SFAS 5 (ASC 450) contingencies

probable estimable record loss probable not estimable disclose reasonably possible estimable or “ reasonably possible not estimable “ remote ignore ignore

11

SFAS 5 (ASC 450) contingencies

estimable can’t be estimated Probable accrue loss fn disclose Possible Remote do nothing

12

Contingencies – lawsuits audit procedures

Inquire of management Review minutes of BoD meetings Analyze legal expense Obtain a letter from each major attorney

13

Dan Management is our primary source of information about

Litigation, Claims and Assessments what is our most important source of evidence to corroborate managements’ representations regarding LCA ?

14

Inquiry of Client’s Attorney

A list including (provided by client’s Senior Management) Pending litigation Asserted or unasserted claims Information about each item on list Likelihood of an unfavorable outcome Amount or range of potential loss A statement that the list is complete Page 348

Pending litigation. Asserted or unasserted claims. Information about each item on list. Likelihood of an unfavorable outcome. Amount or range of potential loss. A statement that the list is complete. Page 348.")

15

“Inquiry of a Client’s Attorney”

Catherine “Inquiry of a Client’s Attorney” this is an auditing procedure Who sends this letter to the attorney ? To whom does their attorney respond ?

16

“Inquiry of a Client’s Attorney”

Karli “Inquiry of a Client’s Attorney” what kind of problem do we have if their attorney refuses to respond ? what kind of report will we issue ?

17

Dev Do we modify the first paragraph?

Do we modify the Management’s Responsibility paragraph? Do we modify the Auditor’s Responsibility paragraph? Do we modify the Opinion paragraph? Is there a Basis for Opinion paragraph? Before or after?

20

A B C D interim date report issued end of field work report date

12/31/14 A B C D 20

21

Elizabeth T describe the two types of subsequent events

how do we decide whether to make an adjusting entry to include the effects of the subsequent event in the financial statement balances or just disclose the event in the footnotes

22

Type I - adjusting journal entry

subsequent events Type I - adjusting journal entry Those that provide evidence of conditions that existed at the date of the financial statements Type II - disclose b. Those that provide evidence of conditions that arose after the date of the financial statements

23

Type I - adjusting journal entry

Declaration of bankruptcy by a customer with a large account receivable Settlement of litigation for an amount greater than recorded Sale of investments for less than recorded amount

24

Type II - disclosure Issue bonds or equity securities

Merger or acquisition Loss due to fire or natural disaster

25

subsequent events – auditing procedures

inquire of management read internal financial statements read minutes of Bd of Directors’ meetings obtain a letter of representation page 353

27

Written Representations

AU-C Section 580* Written Representations Source: SAS No. 122. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope of This Section .01 This section addresses the auditor's responsibility to obtain written representations from management and, when appropriate, those charged with governance in an audit of financial statements. .02 Exhibit D, "List ofAU-C Sections Containing Requirements for Written Representations," lists other AU-C sections containing subject matter-specific requirements for written representations. The specific requirements for written representations of other AU-C sections do not limit the application of this

28

Letter of representation

Management is responsible for the financial statements Management believes the f/s conform to GAAP All financial records have been made available All minutes have been made available Information concerning fraud or illegal acts Information concerning related party transactions Unasserted claims that are probable have been disclosed Subsequent events Page 355

29

Brenda Who prepares and signs the letter of client representations?

30

Jeremy we must obtain certain representations from management in writing what kind of problem do we have if the client refuses? what kind of report will we issue ?

31

Elizabeth W Do we modify the first paragraph?

Do we modify the Management’s Responsibility paragraph? Do we modify the Auditor’s Responsibility paragraph? Do we modify the Opinion paragraph? Is there a Basis for Opinion paragraph? Before or after?

32

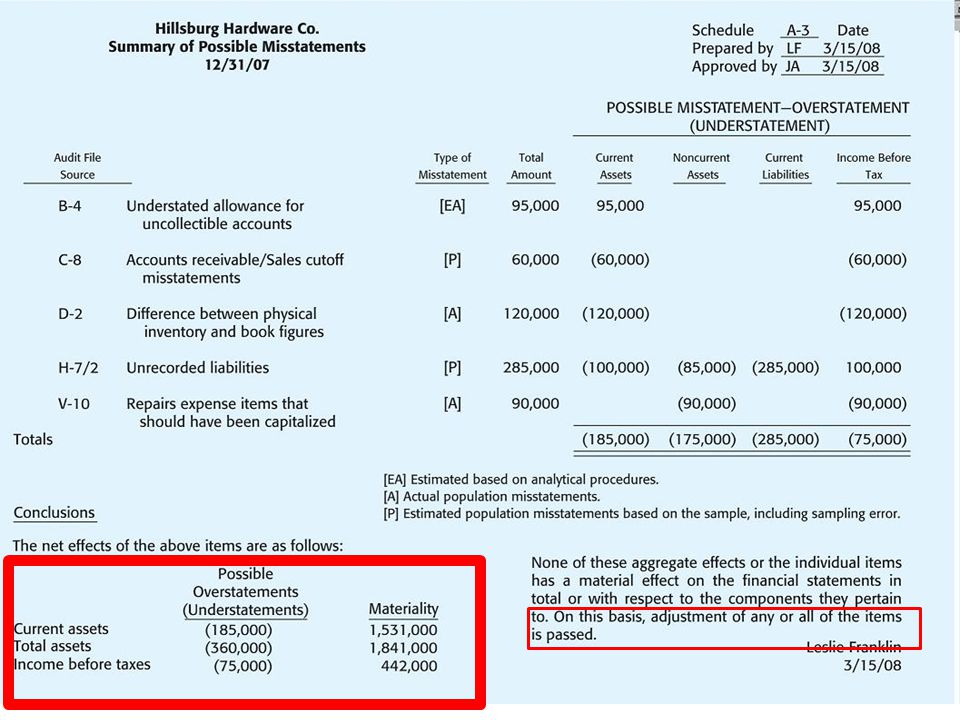

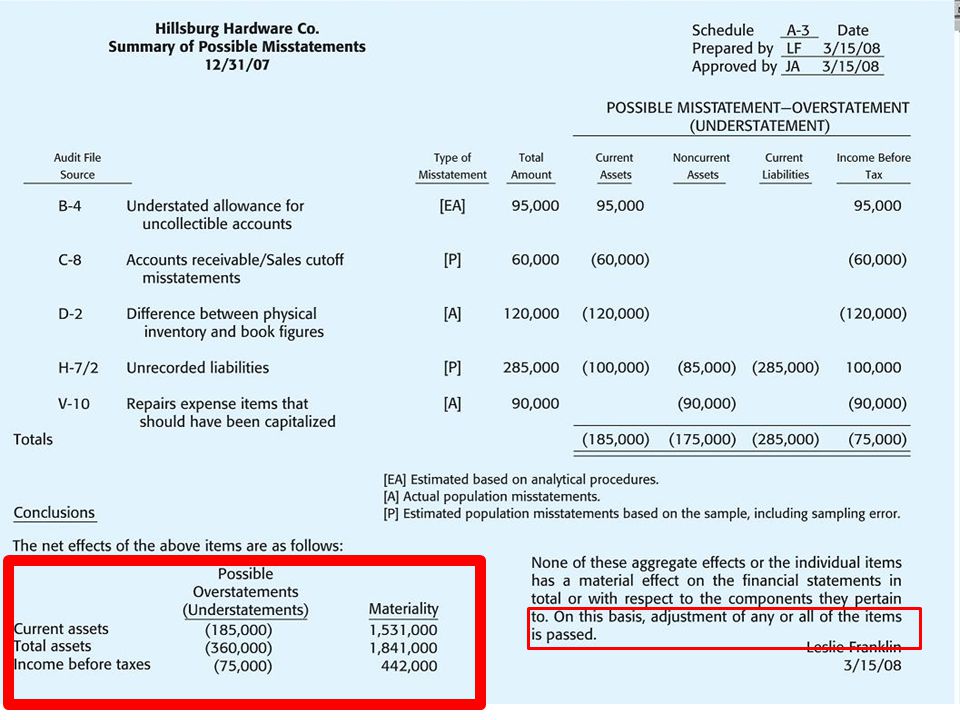

Ellen what is a “waived” or “passed” adjustment? on page 360

“unadjusted misstatement audit schedule” “summary of possible misstatements”

34

Materiality page 122

35

Ellen at what three stages of the audit MAY we perform Analytical Procedures ? at what stages of the audit are we required to perform Analytical Procedures?

36

req’d planning phase substantive tests req’d at conclusion as an overall review

37

Analytical Procedures

AU-C Section 520* Analytical Procedures Source: SAS No. 122. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope of This Section .01 This section addresses the auditor's use of analytical procedures as substantive procedures (substantive analytical procedures). It also addresses the auditor's responsibility to perform analytical procedures near the end of the audit that assist the auditor when forming an overall conclusion on the financial statements. Section 315, Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement, addresses the use of analytical procedures as risk assessment procedures (which may be referred to as analytical procedures used to plan the audit).1 Section 330, Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained, addresses the nature, timing, and extent of audit procedures in response to assessed risks; these audit procedures may include substantive analytical procedures

. It also addresses the auditor s responsibility to perform analytical procedures near the end of the audit that assist the auditor when forming an overall conclusion on the financial statements. Section 315, Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement, addresses the use of analytical procedures as risk assessment procedures (which may be referred to as analytical procedures used to plan the audit).1 Section 330, Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained, addresses the nature, timing, and extent of audit procedures in response to assessed risks; these audit procedures may include substantive analytical procedures.")

38

A B C D interim end of field work date report issued report date

12/31/14 A B C D 38

39

Contingent Liabilities / Attorney’s Letter

Subsequent Events Management Representations analytical procedures Final assessment of audit risk - opinion communications to audit comm or mgmt AU-c 260 Communication with Those Charged with Governance AU-c 265 Communicating Internal Control Related Matters Identified in an Audit subsequent discovery of facts

40

Ryan M what is the definition of audit risk?

42

material known misstatement from samples projected uncorrected

.05 known misstatement from samples projected uncorrected misstatements

43

final review of workpapers

all accounting and auditing questions have been resolved support the auditor’s opinion provide evidence the audit complied with GAAS means of coordinating and supervising the audit

44

Eric who is an “independent reviewer?”

45

dual dating events that occur between the end of field work (the report date) and the date the report is issued extend field work or dual date page 353

46

dual dating p. 353 Hewlett-Packard has an October 31 year end

Ernst & Young completed field work on November 13th On Dec. 6, 2001, Hewlett-Packard made a $1 billion dollar debt offering, which it disclosed in Note 19 in its financial statements. This is how Ernst & Young dated its auditor’s report November 13, 2001, except for Note 19, as to which the date is December 6, 2001.

47

A B C D interim end of field work date report issued report date

12/31/14 A B C D 47

49

AU-C Section 265* Communicating Internal Control Related Matters Identified in an Audit Source: SAS No. 122; SAS No. 125. Effective for audits of financial statements for periods ending on or after December 15, 2012. Introduction Scope of This Section .01 This section addresses the auditor's responsibility to appropriately communicate to those charged with governance and management deficiencies in internal control that the auditor has identified in an audit of financial statements. This section does not impose additional responsibilities on the auditor regarding obtaining an understanding of internal control or designing and performing tests of controls over and above the requirements of section 315, Understanding the Entity and Its Environment and Assessing the Risks of Material Misstatement, and section 330, Performing Audit Procedures in Response to Assessed Risks and Evaluating the Audit Evidence Obtained. Section 260, The Auditor's Communication With Those Charged With Governance, establishes further requirements and provides guidance regarding the auditor's responsibility to communicate with those charged with governance regarding the audit.

50

Deficiency in internal control

Deficiency in internal control. A deficiency in internal control exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent, or detect and correct, misstatements on a timely basis. A deficiency in design exists when a control necessary to meet the control objective is missing, or an existing control is not properly designed so that, even if the control operates as designed, the control objective would not be met. A deficiency in operation exists when a properly designed control does not operate as designed or when the person performing the control does not possess the necessary authority or competence to perform the control effectively. Material weakness. A deficiency, or a combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity's financial statements will not be prevented, or detected and corrected, on a timely basis. Significant deficiency. A deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness yet important enough to merit attention by those charged with governance.

51

Nico what is the definition of control risk?

52

control risk the risk that a misstatement in an assertion about a class of transaction, account balance, or disclosure and that could be material, either individually or when aggregated with other misstatements, will not be prevented, or detected and corrected, on a timely basis by the entity’s internal control.

53

Lauren what is a material weakness?

54

material weakness (page 177 )

a significant deficiency that results in a reasonable possibility that a material misstatement would not be prevented, or detected and corrected on a timely basis

55

Ryan H what two types of control deficiencies do we report ?

56

Steffan to whom do we report deficiencies in the internal controls ?

57

communication of internal control matters

communicate what significant deficiency material weaknesses communicate to who the audit committee board of directors owners or senior management those charged with governance

60

communication with audit committees

The auditor’s responsibilities An overview of the scope of the audit Approach to address significant risks Corrected misstatements Accounting practices & estimates Difficulties & disagreements with management page 362

61

management letter

62

A B C D interim end of field work date report issued report date

12/31/14 A B C D 62

63

Contingent Liabilities / Attorney’s Letter

Subsequent Events Management Representations analytical procedures Final assessment of audit risk - opinion communications to audit comm or mgmt AU-c 260 Communication with Those Charged with Governance AU-c 265Communicating Internal Control Related Matters Identified in an Audit subsequent discovery of facts

66

Fischer vs. Kletz, 266 F. Supp. 180 (SDNY 1967),

the auditor did not disclose errors in a previously issued audit report when (s)he discovered the errors three months later during a consulting engagement an auditor has a duty to anyone still relying on his report to disclose subsequently discovered errors in the report

he discovered the errors three months later during a consulting engagement. an auditor has a duty to anyone still relying on his report to disclose subsequently discovered errors in the report.")

67

subsequent discovery of facts existing at the date of the audit report

the auditor should a. discuss the matter with management and, when appropriate, those charged with governance. b. determine whether the financial statements need revision and, if so, inquire how management intends to address the matter in the financial statements.

68

subsequent discovery of facts existing at the date of the audit report

.16 If management revises the financial statements, the auditor should a. apply the requirements of paragraph . b. if the audited financial statements have been made available to third parties, assess whether the steps taken …. ensure that anyone in receipt of those financial statements is informed of the situation,

69

subsequent discovery of facts existing at the date of the audit report

.17 If management does not revise the financial statements in circumstances when the auditor believes they need to be revised, then a. if the audited financial statements have not been made available to third parties, the auditor should notify management and those charged with governance—unless all of those charged with governance are involved in managing the entity4—not to make the audited financial statements available to third parties before the necessary revisions have been made and a new auditor's report on the revised financial statements has been provided. If the audited financial statements are, nevertheless, subsequently made available to third parties without the necessary revisions, the auditor should apply the requirements of paragraph .17b. b. if the audited financial statements have been made available to third parties, the auditor should assess whether the steps taken by management are timely and appropriate to ensure that anyone in receipt of the audited financial statements is informed of the situation, including that the audited financial statements are not to be relied upon. .18 If management does not take the necessary steps to ensure that anyone in receipt of the audited financial statements is informed of the situation, as provided by paragraphs .16b or .17b, the auditor should notify management and those charged with governance—unless all of those charged with governance are involved in managing the entity5—that the auditor will seek to prevent future reliance on the auditor's report. If, despite such notification, management or those charged with governance do not take the necessary steps, the auditor should take appropriate action to seek to prevent reliance on the auditor's report. (Ref: par. .A23–.A26)

")

70

subsequent discovery of facts existing at the date of the audit report

71

end of audit party

72

great quarter You made it very enjoyable for me to come to work every day

73

congratulations to our March 2015 grads

Similar presentations