Download presentation

Presentation is loading. Please wait.

1

ADAPTED FOR THE SECOND CANADIAN EDITION BY: THEORY & PRACTICE JIMMY WANG LAURENTIAN UNIVERSITY FINANCIAL MANAGEMENT

2

CHAPTER 15 LEASE FINANCING

3

CHAPTER 15 OUTLINE Types of Leases Tax Effects Financial Statement Effects Evaluation by the Lessee Evaluation by the Lessor Other Issues in Lease Analysis Other Reasons for Leasing Copyright © 2014 by Nelson Education Ltd. 15-3

4

Nelson: Please replace with new Ch. 15 valuation box Copyright © 2014 by Nelson Education Ltd. 15-4

5

Who are the Two Parties to a Lease Transaction? The lessee, who uses the asset and makes the lease, or rental, payments The lessor, who owns the asset and receives the rental payments Note that the lease decision is a financing decision for the lessee and an investment decision for the lessor. Copyright © 2014 by Nelson Education Ltd. 15-5

6

Types of Leases Operating lease – Short-term and normally cancellable – Maintenance usually included – Not fully amortized Financial, or capital, lease – Long-term and normally not cancellable – Maintenance usually not included – Fully amortized Sale-and-leaseback arrangements Combination lease "Synthetic" lease Copyright © 2014 by Nelson Education Ltd. 15-6

7

Tax Effects Leases are reviewed by the Canada Revenue Agency (CRA) to determine if they are an actual lease or conditional sale. For an actual lease, the full lease payment is deductible. If the lease did not meet the CRA guidelines, then the lessee would treat the asset as a purchase and only deduct CCA and the interest portion of the lease payments. Copyright © 2014 by Nelson Education Ltd. 15-7

8

Financial Statement Effects For accounting purposes, leases are classified as either capital or operating. Capital leases must be shown directly on the lessee’s balance sheet. Operating leases, sometimes referred to as off-balance sheet financing, must be disclosed in the footnotes. Why are these rules in place? Copyright © 2014 by Nelson Education Ltd. 15-8

9

Please insert Figure 15-1 Copyright © 2014 by Nelson Education Ltd. 15-9

10

International Accounting Standards (IAS 17) Firms entering a financial lease contract are obligated to make lease payments as if they had signed a loan agreement. Failure to make lease payments is taken as a default on interest/principal and can bankrupt a firm. To capitalize a lease, the present value of the lease payments is shown as debt. The same amount is shown as a fixed asset. The leasing firm would have the same balance sheet as Firm B (a loan borrower) shown on the previous slide. Copyright © 2014 by Nelson Education Ltd. 15-10

shown on the previous slide. Copyright © 2014 by Nelson Education Ltd")

11

Impact on Capital Structure Leasing is a substitute for debt. As such, leasing uses up a firm’s debt capacity. Assume a firm has a 50/50 target capital structure. Half of its assets are leased. This has the effect of raising its true debt ratio, and thus its true capital structure is changed. Copyright © 2014 by Nelson Education Ltd. 15-11

12

Evaluation By the Lessee Based on regular capital budgeting procedures, the firm decides to acquire a certain capital asset. The next question is how to finance it: use internally generated cash flows, borrow to buy, or lease. As leasing is a substitute for debt financing, the appropriate comparison would be with debt financing. Copyright © 2014 by Nelson Education Ltd. 15-12

13

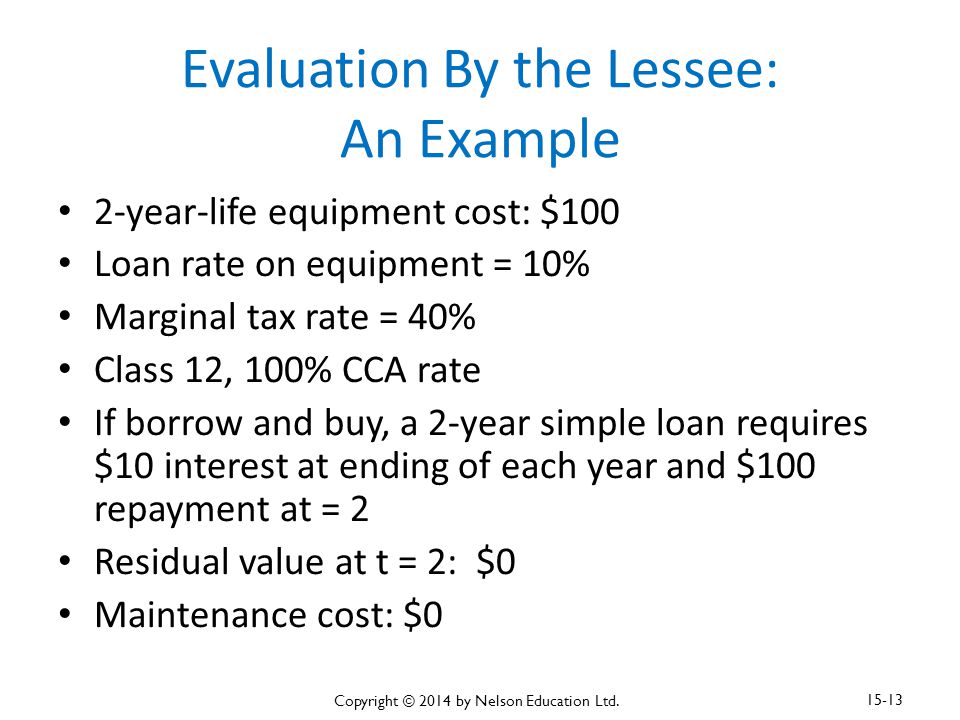

Evaluation By the Lessee: An Example 2-year-life equipment cost: $100 Loan rate on equipment = 10% Marginal tax rate = 40% Class 12, 100% CCA rate If borrow and buy, a 2-year simple loan requires $10 interest at ending of each year and $100 repayment at = 2 Residual value at t = 2: $0 Maintenance cost: $0 Copyright © 2014 by Nelson Education Ltd. 15-13

14

Other Information for Lease If the equipment is leased: – Lease contract runs for 2 years – Lease meets CRA guidelines to deduct lease payments for tax purposes – Lease payment will be $55 at the end of each year Copyright © 2014 by Nelson Education Ltd. 15-14

15

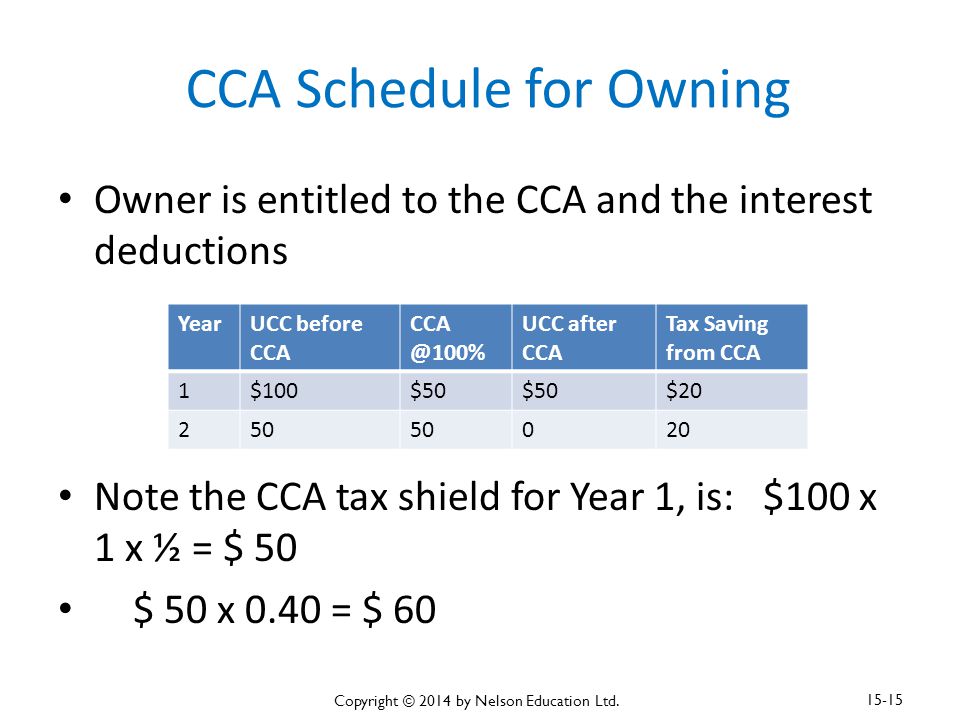

CCA Schedule for Owning Owner is entitled to the CCA and the interest deductions Note the CCA tax shield for Year 1, is: $100 x 1 x ½ = $ 50 $ 50 x 0.40 = $ 60 YearUCC before CCA CCA @100% UCC after CCA Tax Saving from CCA 1$100$50 $20 250 020 Copyright © 2014 by Nelson Education Ltd. 15-15

16

Cash Flow Time Line: Borrow-To-Buy 012 Equipment cost($100) Inflow from loan100 Interest expense($10) Interest tax savings44 Principal repayment($100) CCA tax savings20 NCF0$14($86) PV@6% cost of buying=$63.33 Copyright © 2014 by Nelson Education Ltd. 15-16

17

Why Use 6% as the Discount Rate? Leasing is similar to debt financing. – The cash flows have relatively low risk; most are fixed by contract. – Therefore, the firm’s 10% cost of debt is a good candidate. The tax shield of interest payments must be recognized, so the discount rate is: 10%(1 – T) = 10%(1 – 0.4) = 6.0% Copyright © 2014 by Nelson Education Ltd. 15-17

= 10%(1 – 0.4) = 6.0% Copyright © 2014 by Nelson Education Ltd")

18

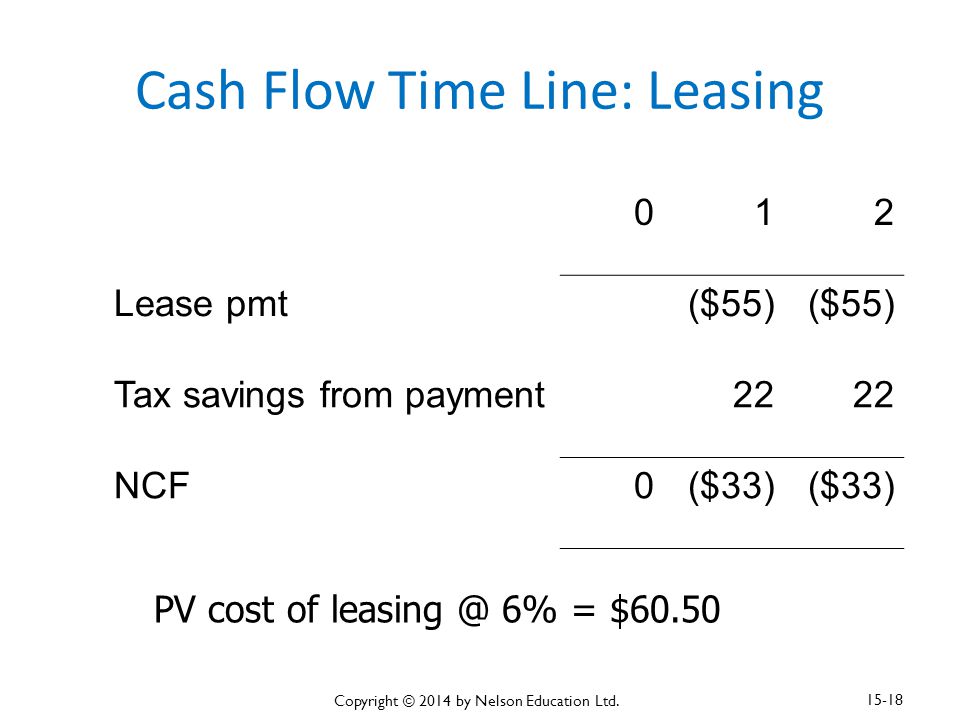

Cash Flow Time Line: Leasing PV cost of leasing @ 6% = $60.50 012 Lease pmt($55) Tax savings from payment22 NCF0($33) Copyright © 2014 by Nelson Education Ltd. 15-18

19

What is the Net Advantage to Leasing (NAL)? NAL = PV cost of owning – PV cost of leasing = $63.33 - $60.50 = $2.83 > 0 Should the firm lease or buy the equipment? Why? Lease because NAL > 0 implying leasing is cheaper than buying. Copyright © 2014 by Nelson Education Ltd. 15-19

20

Alternative Lease/Buy Analysis Instead of separately calculating the present values of the cost of borrowing to buy and of the cost of leasing and then comparing the two financing methods, we may calculate NAL directly with these cash flows: 1.the purchase price is an advantage to leasing and may be treated as inflows; 2.the CCA tax shields and the residual value are opportunity costs and thus are outflows; and 3.the same as those in calculating the cost of leasing. Copyright © 2014 by Nelson Education Ltd. 15-20

21

Alternative Lease/Buy Analysis: An Illustration NAL = Purchase Price – PV of Cash Flows = $100 – $53/(1 + 6%) – $53/(1 + 6%) 2 = $100 – $50 – $47.17 = $2.83 > 0 Copyright © 2014 by Nelson Education Ltd. 15-21

22

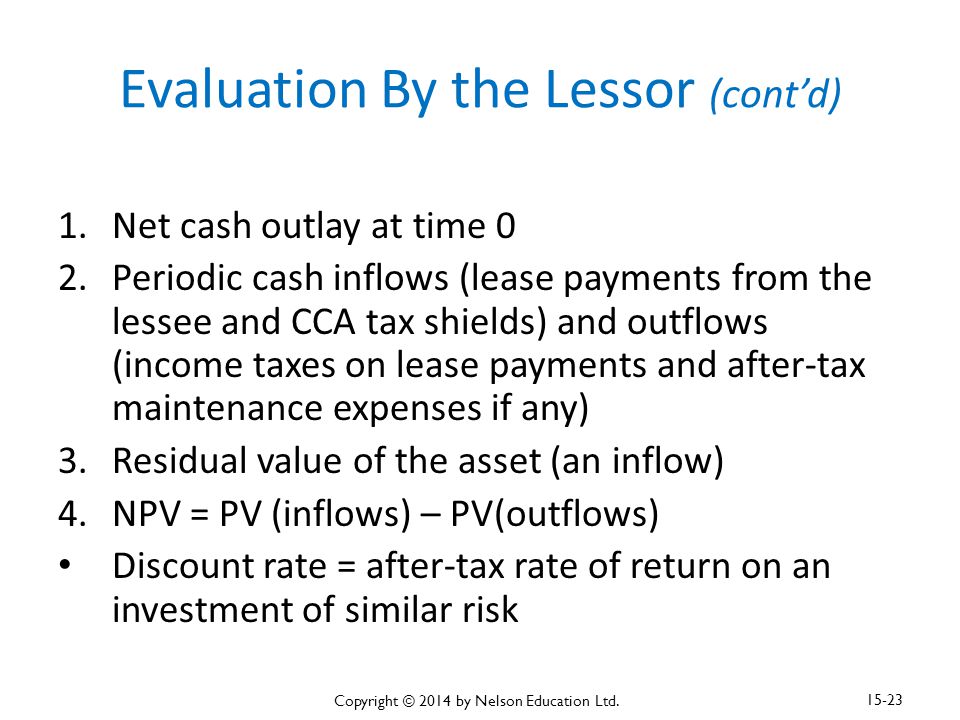

Evaluation By the Lessor To the lessor, writing the lease is an investment. Therefore, the lessor must compare the return on the lease investment with the return available on alternative investments of similar risk. Copyright © 2014 by Nelson Education Ltd. 15-22

23

Evaluation By the Lessor (cont’d) 1.Net cash outlay at time 0 2.Periodic cash inflows (lease payments from the lessee and CCA tax shields) and outflows (income taxes on lease payments and after-tax maintenance expenses if any) 3.Residual value of the asset (an inflow) 4.NPV = PV (inflows) – PV(outflows) Discount rate = after-tax rate of return on an investment of similar risk Copyright © 2014 by Nelson Education Ltd. 15-23

24

Lessor’s Evaluation: An Example Lease payment = $320,000 at the beginning of each year Cost of equipment = $1,000,000 Loan rate on equipment = 10% Marginal tax rate = 40% Class 43, 30% CCA rate 4- year maintenance contract costs $20,000 at the beginning of each year Residual value at t = 4: $200,000 Copyright © 2014 by Nelson Education Ltd. 15-24

25

Time Line: Lessor’s Analysis (In Thousands) 01234 Cost-1,000 CCA tax shield6010271.449.98 Maint-20 Tax sav8888 Lse pmt320 Tax-128 RV200 RV tax-80 NCF-804240282251.4169.98 Copyright © 2014 by Nelson Education Ltd. 15-25

26

Time Line: Lessor’s Analysis (In Thousands) (cont’d) The NPV of the net cash flows, when discounted at 6%, is $19,114. Should the lessor write the lease? Why? Yes! If the lease’s NPV is greater than zero, then the lease should be written. Copyright © 2014 by Nelson Education Ltd. 15-26

27

Setting the Lease Payment The lessor may set the size of the lease payments on its own or by negotiation with the lessee. The lease payments are set so as to provide the lessor with some specific rate of return. The NPV is set to zero with the target rate of return as the discount rate and then solve the equation for the lease payment. Copyright © 2014 by Nelson Education Ltd. 15-27

28

Remarks If all inputs for leasing analysis are symmetrical between lessee and lessor, leasing is a zero-sum game. The lessor’s cash flows would be equal, but opposite in sign, to the lessee’s NAL. What are the implications? Differences between lessees and lessors must exist to support a lease. Copyright © 2014 by Nelson Education Ltd. 15-28

29

Other Issues in Lease Analysis Do higher residual values make leasing less attractive to the lessee? Is lease financing more available or “better” than debt financing? Is the lease analysis presented here applicable to real estate leases? To auto leases? Vehicle leases Copyright © 2014 by Nelson Education Ltd. 15-29

30

Other Reasons for Leasing Leasing is driven by various differences between lessees and lessors. The top three motivations are: – tax rate differentials – that lessors are often better to bear the residual value risk than lessees – that lessors can maintain the leased asset more efficiently than lessees Copyright © 2014 by Nelson Education Ltd. 15-30

31

Other Reasons for Leasing (cont’d) Leasing provides operating flexibility (airlines lease their aircraft). Leasing can reduce the risk of technological obsolescence (hospitals lease high-technology items). Leasing especially with a cancellation clause can also be attractive when a firm is uncertain about the demand for its products or services. Copyright © 2014 by Nelson Education Ltd. 15-31

. Leasing especially with a cancellation clause can also be attractive when a firm is uncertain about the demand for its products or services. Copyright © 2014 by Nelson Education Ltd")

32

Issues of Cancellation Clause A cancellation clause would lower the risk of the lease to the lessee but raise the lessor’s risk. To account for this, the lessor would increase the annual lease payment or else impose a penalty for early cancellation. Copyright © 2014 by Nelson Education Ltd. 15-32

Similar presentations

Analyze the various sources of borrowing available to a client and.>")