Download presentation

Presentation is loading. Please wait.

1

Medical Care Markets Ty Borders, Ph.D. Assistant Professor Health Services Research & Management Texas Tech School of Medicine

2

Objectives Describe the evolution of the medical profession and medical practices Discuss the supply of physicians in the United States Discuss the other major health care professionals Describe methods of assessing the supply of health care providers

3

Objectives (continued) Discuss the supply of physicians in rural areas Describe the factors associated with establishing practice in a rural area Describe rural physician recruitment and retention mechanisms Describe the role of competition in affecting supply in rural areas

Discuss the supply of physicians in rural areas Describe the factors associated with establishing practice in a rural area Describe rural physician recruitment and retention mechanisms Describe the role of competition in affecting supply in rural areas")

4

Rise of the medical profession (from Starr) Romans –Physicians frequently slaves, freedmen, or foreigners 18th c. England –Only persons beneath physicians were surgeons and apothecaries 19th c. America –Surgeons in same social class as barbers

5

What about the rest of the world? Medical profession not as powerful in other highly developed nations Former Soviet Union - $ comparable to factory workers Japan - managers make more $ United Kingdom - $ salaries much lower than U.S. docs

6

Rise of the Medical Profession General characteristics of a profession: Self-regulating Unique body of knowledge High level of training Service orientation Code of ethics

7

Authority of medical profession (from Starr) The authority of MDs differentiates them from other professions Authority is the ability to control others’ behaviors 2 roots of authority –Dependence –Legitimacy

The authority of MDs differentiates them from other professions Authority is the ability to control others’ behaviors 2 roots of authority –Dependence –Legitimacy")

8

Derivations of dependence Knowledge, competence of a professional Belief that bad consequences will occur if one does not obey professional Unique reasons we are dependent upon medical profession –They have scientific knowledge –They make decisions for us

9

Derivations of legitimacy Acceptance that you should obey Based on... –Rational, scientific grounds –Affirmation by peer group –Judgement/advice is meant to do good When legitimacy is in doubt, dependence almost usually still exists

10

Cultural and social authority Social authority: Giving of commands (e.g. when parent tells you what to do; when boss tells you what to do) Cultural authority: Our views of reality which affect our reactions to commands from others.

Cultural authority: Our views of reality which affect our reactions to commands from others..")

11

Consolidation of medical authority Greater cohesion Referrals to specialists Changes in pre-industrial America Better transportation Telephones Differentiation of labor

12

Consolidation (continued) Standardization of medial education –In mid to late 19th c., a lot of sects within medicine –Homeopaths: thought disease could be cured/caused by drugs; thought that disease caused by a suppressed itch. –Eclectics: thought herbal medicine was best treatment.

13

Consolidation (continued) First medical school at Univ. of Pennsylvania in 1765 –Doctors only went to school for four years Abraham Flexner’s report –Recommended closure of many medical schools Now, over 100 medical schools in U.S. –Doctors have 8 years of undergraduate education

14

Medical authority and conversion into economic power AMA: established in 1846 Hospitals and drug companies dependent upon physicians as gatekeepers Doctors against national health insurance, prepaid group practices, and company employment

15

Measuring supply No. of physicians per 100,000 enrollees No. of physicians per 10,000 residents Supply/pop. ratios do not account for.. –Physician productivity –Health of the population –Physicians who travel around to provide care

16

Allopathic vs. Osteopathic Medicine Osteopathy (O.D.) is similar to allopathic medicine (M.D.) –Reimbursed by Medicaid, Medicare, & most private insurance Osteopathy tends to stress joint manipulation and diet more than allopathic O.D.s more common in rural than urban areas

is similar to allopathic medicine (M.D.) –Reimbursed by Medicaid, Medicare, & most private insurance Osteopathy tends to stress joint manipulation and diet more than allopathic O.D.s more common in rural than urban areas.")

17

Full-Time Equivalent Phys. Needed per 10,000 Pop. in HMOs Primary Care5.0 OB/GYN1.1 General Surgery0.6 Ortho0.5 Emergency Med.0.5 Anesthesiology0.6 Radiology0.6 Psychiatry0.4 Urology0.3 (Kronick et al. as cited in Rohrer 2000)

.")

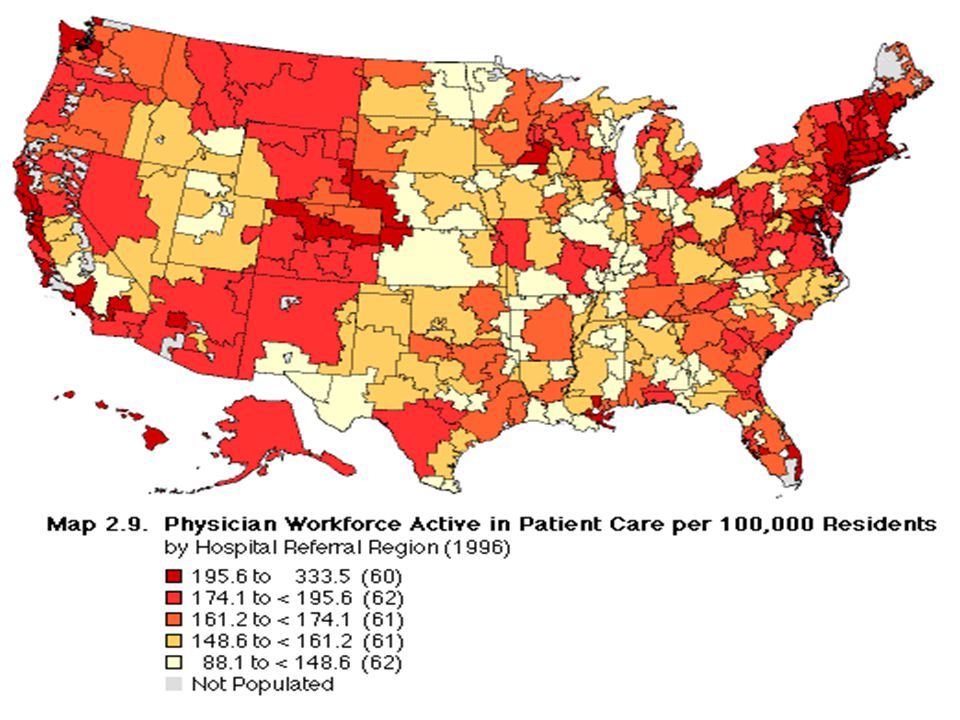

19

Phys/100,000 relative to HMO requirements

20

No. of excess physicians (from Wennberg)

")

21

Consequences of increased supply (nationally) Increased competition, shift in employment –Solo practice, fee for service to group practice, capitation Supply-induced demand Which has contributed to managed care

Increased competition, shift in employment –Solo practice, fee for service to group practice, capitation Supply-induced demand Which has contributed to managed care")

22

Consequences of increased supply (nationally) Increased competition, shift in employment –Solo practice, fee for service to group practice, capitation Supply-induced demand Which has contributed to managed care

Increased competition, shift in employment –Solo practice, fee for service to group practice, capitation Supply-induced demand Which has contributed to managed care")

23

Physician supply in rural areas Smallest number of physicians per 100,000 population in rural areas non- adjacent to a metro area

24

International Medical Graduates Supply has increased in 1990s Teaching hospitals receive subsidies for medical education Most practice in urban areas Do have an impact on supply in Health Professional Shortage Areas (HPSAs), –18.7% of PCPs are IMGs (nation) –23.2% of PCPs are IMGs (Texas) Overall, IMGs increasing oversupply

, –18.7% of PCPs are IMGs (nation) –23.2% of PCPs are IMGs (Texas) Overall, IMGs increasing oversupply")

25

Physician Assistants (PAs) and Nurse Practitioners (NPs) PAs work under supervision of physicians –can diagnose, manage, treat common diseases NPs have a similar role –Midwives, family NPs, psych. NPs –Emphasize prevention, counseling

26

Rise of nursing Early 1900’s, –Nurses tended to be social derelicts, past prostitutes (Rosenberg’s The Care of Strangers) Today, a respected and large (the largest) health care profession

Today, a respected and large (the largest) health care profession")

27

Professionalization of nursing Led by Florence Nightingale –Argued that only women are caring enough to be nurses –Physicians agreed with this they didn’t want nurses involved in technical aspects

28

Nurse training in early 20 c. Nurse training was a good deal –Free room and board –Usually sponsored by hospitals (as is still the case in Japan) –Hospitals got cheap labor in return

–Hospitals got cheap labor in return.")

29

Financing health services: Objectives Describe problems with competition in medical care markets Explain the origins of health insurance Differentiate types of insurance Describe major reimbursement mechanisms Explain service use incentives Identify provider incentives

30

Assumptions for optimal competition Market competition –No negative externalities of consumption –No positive externalities of consumption –Consumer tastes predetermined Demand theory –Person is the best judge of his/her welfare –Consumers have sufficient information to make good choices –Consumers know with certainty the results of their consumption decisions –Individuals are rational –Individuals reveal their preference through their actions

31

Assumptions for optimal competition Supply theory –Supply and demand are independently determined (no supply- induced demand) –Firms do not have any monopoly power (there is a sufficient number of suppliers) –No barriers to entry *from Thomas Rice, The Economics of Health Revisited

–Firms do not have any monopoly power (there is a sufficient number of suppliers) –No barriers to entry *from Thomas Rice, The Economics of Health Revisited")

32

What is insurance? A method of distributing risk Traditional insurance for expensive potential losses –car accidents, hospitalization Today’ health insurance covers fairly non-risky events –routine physician care

33

Origins of health insurance European industries –Germany’s sickness fund, 1840 United States –Blue Cross: Baylor teachers in Dallas, 1929 –American Medical Association opposed –Blue Cross: expanded during depression –Blue Shield: California Medical Society, 1939

34

Health insurance types Voluntary –Individuals, employers purchases Social health insurance –Government sponsored (e.g. Medicare in the U.S.; health insurance in Canada) Public welfare –For low income persons (e.g. Medicaid)

Public welfare –For low income persons (e.g. Medicaid).")

35

Health insurance coverage in U.S. 41.7 million Americans (15.6 % of population) uninsured in 1996 (Carrasquillo et al. 1999; from Current Population Survey) Texas has the higher proportion of uninsured of all of the states –4,680,000 Texans (24.3 %) uninsured –a significant increase from 1989

uninsured in 1996 (Carrasquillo et al. 1999; from Current Population Survey) Texas has the higher proportion of uninsured of all of the states –4,680,000 Texans (24.3 %) uninsured –a significant increase from")

36

Health insurance coverage in U.S. 187.9 million (70.4%) covered by private 31.9 million (11.8%) covered by Medicaid 34.7 million (13.2%) covered by Medicare (13.2%)

covered by private 31.9 million (11.8%) covered by Medicaid 34.7 million (13.2%) covered by Medicare (13.2%).")

37

Health insurance coverage in U.S. by Age Category

38

Health insurance coverage in U.S. by Gender

39

Voluntary health insurance Most people in U.S. covered by private, voluntary insurance –Employer purchased –Self-employed –Medigap

40

Social health insurance Worker’s compensation Medicare Department of Defense VA health system (not simply an insurance system, but a health system)

")

41

Source of expenditures

42

Worker’s compensation Covers employed persons Pays cash replacement of a portion of wages Pays for medical care resulting from work-related injury or sickness

43

Medicare An entitlement program passed in 1965 The major social health insurance program in the U.S. Covers individuals 65 and older –Also covers disabled individuals and those with end-stage renal disease

44

Medicare Part A Compulsory Covers hospital costs Paid for by Social Health Insurance Trust Fund Indirect payment –Gov’t. does not own provider organizations and does not hire providers

45

Medicare Part A Benefits 90 inpatient days in a benefit period –Deductibles for days 1-60 –Coinsurance for days 61-90 100 days in Skilled Nursing Facility –Coinsurance

46

Medigap 70 % of Medicare enrollees have supplemental insurance –Covers deductibles, coinsurance

47

Medicare Part B Not compulsory Covers physician services Most $ from general treasury Some $ from Social Security check deductions for Part B

48

Medicare Part B Benefits Physician services –Yearly deductible –Monthly premium Outpatient hospital care No pharmaceuticals No eye examinations

49

Medicaid (Title XIX) A welfare or charity program Most $ comes from U.S. General Treasury State treasuries pick up rest of tab

50

Medicaid (Title XIX) Eligibility requirements –Receiving Aid to Families with Dependent Children (AFDC) –Pregnant and postpartum women with children < 6 yrs. and income < 133% of poverty level –Aged, blind, and disabled receiving supplemental security income

51

Medicaid Benefits Hospital inpatient care Home health care Physician services Family planning Other services as shown in text

52

VA Health Care System For retired, disabled, and other “deserving” veterans –approximately 170 hospitals in U.S. –provide mostly acute hospital care –some specialized outpatient care –mental health care –long term care

53

Moral hazard When have insurance, want to reap the benefits of it Can lead to excess use of health services To control effects of moral hazard, multiple techniques used

54

TEFRA Tax Equity and Fiscal Responsibility Act (1982) Encouraged Medicare HMOs Prospective payment for Medicare (DRGs)

Encouraged Medicare HMOs Prospective payment for Medicare (DRGs)")

55

RBRVS Resource-based relative-value scale (1992) –for Medicare Part B –Based on physician work, practice expense, and malpractice insurance

–for Medicare Part B –Based on physician work, practice expense, and malpractice insurance")

56

Controlling excess use In the U.S., we tend to rely on risk distribution and market incentives –Patient incentives (cost sharing) –Provider incentives (reimbursement) –Utilization review –Health plan competition

–Provider incentives (reimbursement) –Utilization review –Health plan competition")

57

Patient incentives: Deductibles Money that must be paid by the individual before insurance benefits kick in –e.g. the patient must pay for $500 of medical charges before insurance begins to pay –Criticized for contributing to delays in treatment

58

Other patient incentives Copayment –Fixed amount paid for each service consumed –e.g. a patient has to pay $15 every time he/she visits a physician Coinsurance –A percentage of money paid by individual for each service –e.g. the insurer pays 80% of surgery charges; the patient pays 20%

59

Physician reimbursement Fee-for-service (FFS) Prepayment Salary

Prepayment Salary")

60

Utilization review Prospective Retrospective Concurrent

61

What is managed care? FFS managed care PPOs POS plans HMOs

62

Fee for service (FFS) Reimbursement on a per diem, per case, per procedure basis Incentives for overutilization Managed FFS –Utilization review –Preauthorization

Reimbursement on a per diem, per case, per procedure basis Incentives for overutilization Managed FFS –Utilization review –Preauthorization")

63

Preferred Provider Organizations Organization contracts with group of providers in exchange for discount Managed care techniques –Utilization review –Per diem hospital reimbursement –Gatekeeping (rarely)

")

64

HMOs Utilization review Preauthorization Gatekeeping Capitation

65

IPA model HMO HMO contracts with an independent practice association or solo practitioners HMO may capitate IPA –IPA decides how to reimburse physicians HMO may capitate individual doctors

66

Network model HMO HMO contracts with multiple medical groups to provide care Contract is non-exclusive. HMO typically capitates the group

67

Prepaid Group Practice HMO HMO contracts with single or multiple group practices Relationship often exclusive –Group practice agrees to treat only the HMO’s enrollees Kaiser Permanente

68

Staff model HMO HMO employs physicians Physicians receive a salary HMO has more influence over the physicians’ behavior Group Health Cooperative of Puget Sound

69

Efficiency and quality HMOs appear to achieve efficiency through lower hospital admissions Staff and prepaid group models most efficient Quality just as good in staff and prepaid group models as FFS plans –Clinical quality –Patient satisfaction

Similar presentations

Name the basic types of medical insurance policies and describe their features Describe the different types.>")