Download presentation

Presentation is loading. Please wait.

1

Reform results and the structure of para-fiscal and non-tax charges in the budget of the Republic of Serbia and the local governments

2

Amendments to the Law on LG Finance adopted in September 2012 – one of the main manners of the conducted reform of para-fiscal charges in the previous phase The most significant changes – determining maximum amounts or total elimination of local signage fee (depending on concrete taxpayer and the legal entity size and scope of revenues) and limiting the maximum amount of utility fee for keeping motor vehicles The effects in the City of Belgrade are estimated at ca. RSD 3 billion a year The effects in all local government in total are estimated at ca. RSD 5 billion a year Law on local government finance – 2012 amendments

3

In the analysis of all non-tax charges in 2011, this fee was marked as the most fund-generating individual form in the system (its fiscal importance was nearly RSD 15 billion at that point) Starting from 1 st January 2014, the fee has been entirely abolished and it is not charged anymore On this ground, the local governments in Serbia will lose RSD 16 billion, which was the collected sum in 2013 The City of Belgrade will lose more than RSD 8 billion on this ground, which is more than 12% of total city budget revenues However, given its arbitrariness and discriminatory treatment for different taxpayers, and due to the cease of Constitution justification, its elimination is a significant step. Land use fee – deserved retirement

4

The Ministry of Finance formed a Working group for drafting the new law The foundations for LG finance need to be set up in a clear and transparent manner, as much as possible, and their funding sources and basic determining elements need to be precisely defined – the aim is to have as little high-amount forms as possible Property tax needs to become the most significant individual revenue source – application of the new Property Tax Law starting from 2014 also needs to allow taxation of construction, agriculture and forest land, in addition to facilities New Law on LG Finance – drafting and adoption planned for 2014

5

The LG budgets took the greatest burden of the reform of non-tax charges in 2012 The reform of some fees in 2012 did not bring the expected results – financial burden was concentrated on a lower number of taxpayers than before A joint assessment is that the following reform phase needs to focus on the national authorities, institutions and agencies and be subjected to change and reform LGs have further engaged in expanding the number of taxpayers and the scope of some fees (primarily the property tax) in order to compensate the lost revenues Land use fee – possibilities of revenue compensation? The conclusions from a round table with local government representatives

12

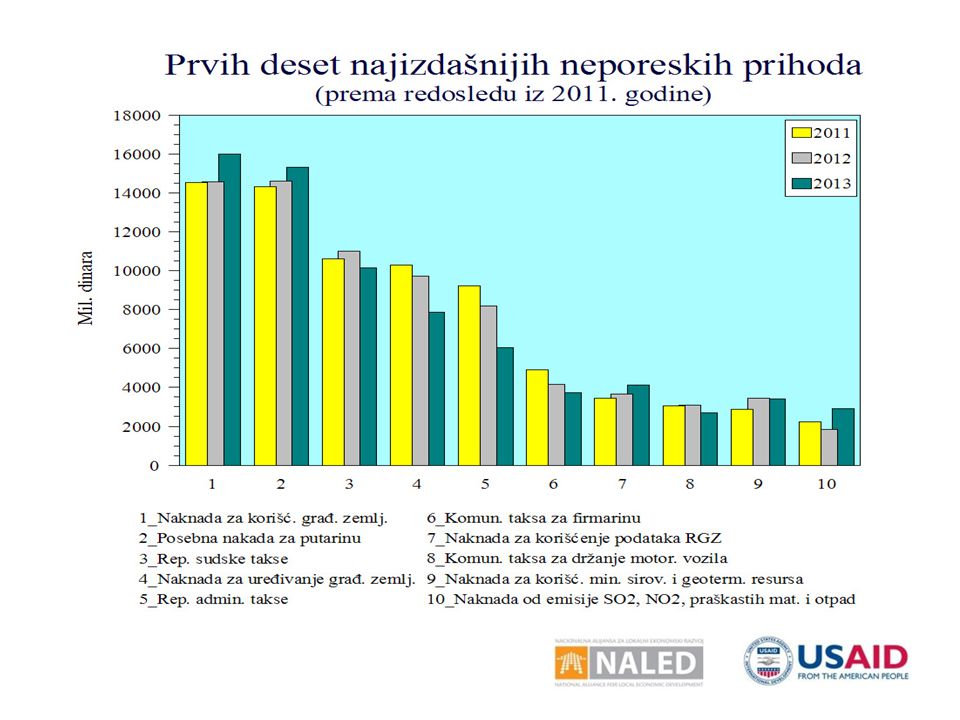

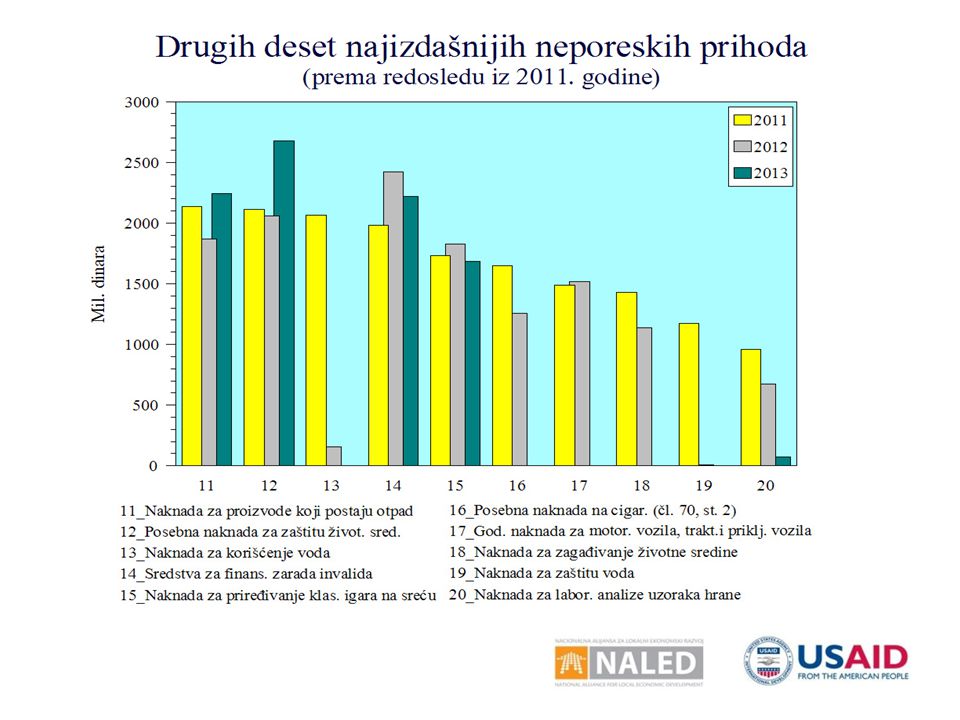

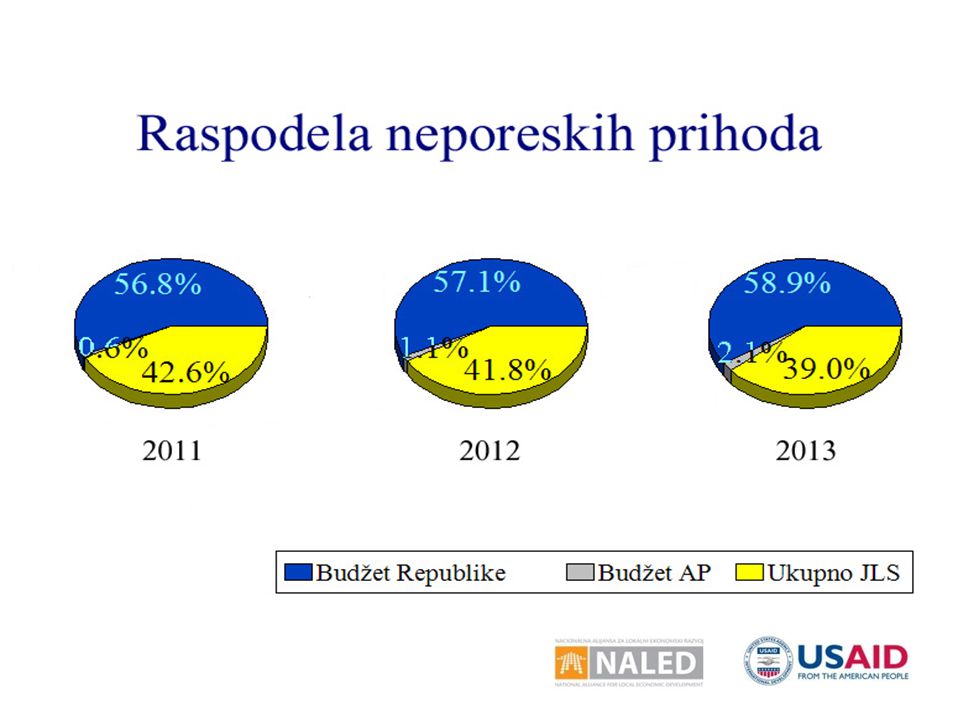

20 most fund-generating non-tax fees in 2013 and their distribution No. Account numberTitleDistributed revenuesNational budgetProvincial budgetTotal LGs 1234567 1741534Land use fee15,976,7685015,976,763 2714581Special fee for use of state road (road fee)15,316,043 0 3742271Republic court fees10,155,432 0 4742253Land development fee7,862,84800 5742221Republic administrative fees6,061,200 0 6742323Fee for use of Republic Geodetic Authority data4,134,284 0 7716111Utility fee for company name display (signage fee)3,716,93724903,716,689 8741511Fee for use of mineral resources...3,426,1701,814,661241,0411,370,468 9741562Fee for use of water resources2,917,2352,128,281788,954 10714549Fee for emission of SO2, NO2, particulate matter...2,916,5741,749,94501,166,629 11714513Utility fee for keeping motor and road vehicles2,683,66431002,683,354 12714562Special environment protection and improvement fee2,676,057402,676,053 13717512 Special fee for registration of motor vehicles 2,472,124 0 14741591Fee for products turning into special waste flows2,242,074 0 15745126Fees for funding the salaries of disabled persons...2,217,190 0 16742284Fee for organizing classic games of chance1,684,563 0 17741563Fee for releasing water1,272,8551,172,830100,025 18742287Fee for organizing special games of chance - betting1,142,900 0 19742286Fee for organizing special games of chance – slot machines1,018,982 0 20741566Drainage fee for legal entities999,799204,360795,440 21 Total90,893,69953,515,4371,925,46035,452,804 22 %100.0058.882.1239.00

15,316, Republic court fees10,155, Land development fee7,862, Republic administrative fees6,061, Fee for use of Republic Geodetic Authority data4,134, Utility fee for company name display (signage fee)3,716, ,716, Fee for use of mineral resources...3,426,1701,814,661241,0411,370, Fee for use of water resources2,917,2352,128,281788, Fee for emission of SO2, NO2, particulate matter...2,916,5741,749,94501,166, Utility fee for keeping motor and road vehicles2,683, ,683, Special environment protection and improvement fee2,676,057402,676, Special fee for registration of motor vehicles 2,472, Fee for products turning into special waste flows2,242, Fees for funding the salaries of disabled persons...2,217, Fee for organizing classic games of chance1,684, Fee for releasing water1,272,8551,172,830100, Fee for organizing special games of chance - betting1,142, Fee for organizing special games of chance – slot machines1,018, Drainage fee for legal entities999,799204,360795, Total90,893,69953,515,4371,925,46035,452, %")

13

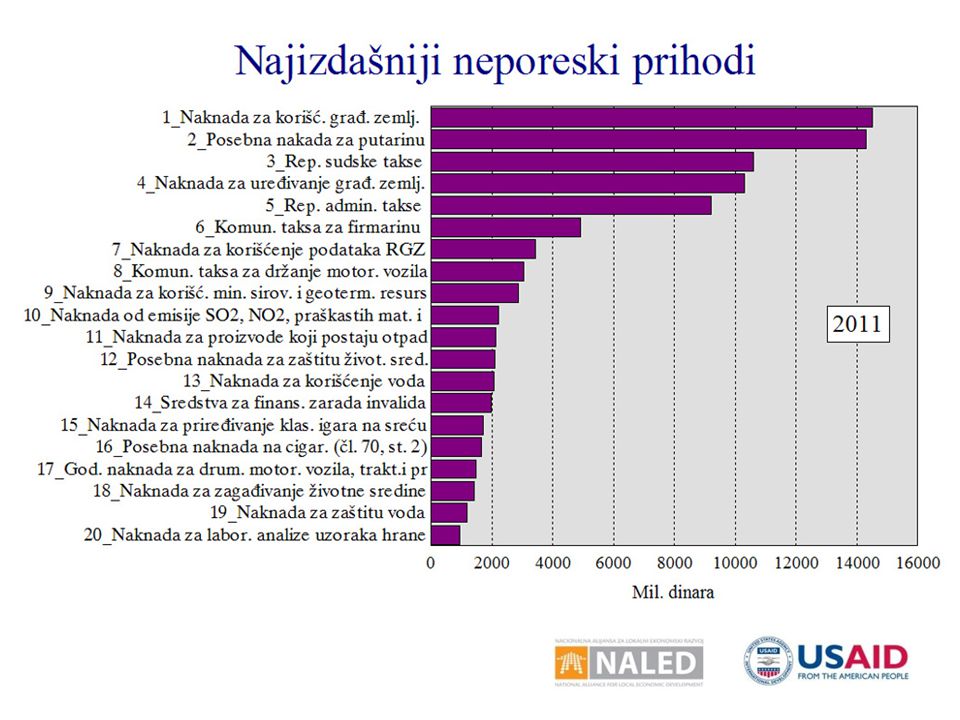

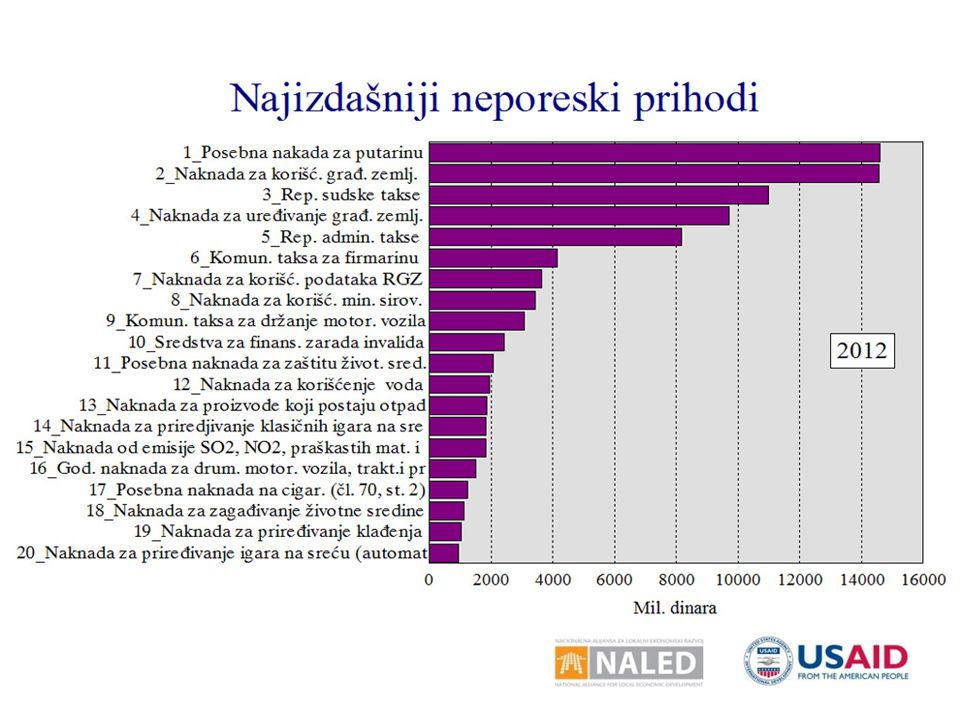

20 most fund-generating non-tax fees from 2011 to 2013 and the rank changes Amount in 000 RSDRank No Account numberTitle201120122013201120122013 123456789 1741534Land use fee14,519,07314,580,32315,976,768121 2714581Special fee for use of state road (road fee)14,309,77114,595,08415,316,043212 3742271Republic court fees10,609,93210,984,90610,155,432333 4742253Land development fee10,289,5099,705,4227,862,848454 5742221Republic administrative fees9,220,0688,172,5326,061,200545 6716111Utility fee for company name display (signage fee)4,913,1314,154,9463,716,937667 7742323Fee for use of Republic Geodetic Authority data3,427,5093,642,8064,134,284776 8714513Utility fee for keeping motor and road vehicles3,042,5883,082,6482,683,6648911 9741511Fee for use of mineral resources2,857,6083,434,5003,426,170988 10714549Fee for emission of SO2, NO2, particulate matter...2,231,3381,828,2622,916,574101510 11741591Fee for products turning into special waste flows2,137,4431,865,4932,242,0741113 12714562Special environment protection and improvement fee2,114,1902,058,9552,676,057121112 13714541Fee for use of water resources2,064,651159,05792713>20 14745126Funds for financing the salaries of disabled persons1,980,5042,422,0102,217,190141014 15742284Fee for organizing classic games of chance1,728,8701,828,5961,684,563151415 16714536Special cigarette fee from Article 70 of the Law on Tobacco1,648,0271,255,09201617>20 17714514Annual fee for road motor vehicles,...1,487,5511,519,8646831716>20 18714547Pollution fee1,430,4181,136,4043,5141819>20 19714542Water protection fee1,173,1579,9983,80119>20 20742124Fee for laboratory analysis of food samples...957,215672,62172,64820>20 Total92,142,55387,109,51981,151,377 Source: Ministry of Finance, Treasury

14,309,77114,595,08415,316, Republic court fees10,609,93210,984,90610,155, Land development fee10,289,5099,705,4227,862, Republic administrative fees9,220,0688,172,5326,061, Utility fee for company name display (signage fee)4,913,1314,154,9463,716, Fee for use of Republic Geodetic Authority data3,427,5093,642,8064,134, Utility fee for keeping motor and road vehicles3,042,5883,082,6482,683, Fee for use of mineral resources2,857,6083,434,5003,426, Fee for emission of SO2, NO2, particulate matter...2,231,3381,828,2622,916, Fee for products turning into special waste flows2,137,4431,865,4932,242, Special environment protection and improvement fee2,114,1902,058,9552,676, Fee for use of water resources2,064,651159, > Funds for financing the salaries of disabled persons1,980,5042,422,0102,217, Fee for organizing classic games of chance1,728,8701,828,5961,684, Special cigarette fee from Article 70 of the Law on Tobacco1,648,0271,255, > Annual fee for road motor vehicles,...1,487,5511,519, > Pollution fee1,430,4181,136,4043, > Water protection fee1,173,1579,9983,80119> Fee for laboratory analysis of food samples...957,215672,62172,64820>20 Total92,142,55387,109,51981,151,377 Source: Ministry of Finance, Treasury")

14

THANK YOU FOR YOUR ATTENTION!

Similar presentations

+61 (0)2 6252 5758.>")

1,339,662 Total area 45,227 km 2 Average salary (2010)792 EUR (2011 IV quarter)865 EUR Currency.>")