Download presentation

Presentation is loading. Please wait.

1

Pensions and Other Postretirement Benefits Sid Glandon, DBA, CPA Associate Professor of Accounting University of Texas at El Paso

2

Qualified Pension Plans Must cover 70% of employees Can’t discriminate in favor of highly compensated employees Must be funded through contributions to an irrevocable trust Benefits must vest within specified period Compliance with restrictions regarding timing and amount of contributions and benefits.

3

Types of Pension Plans Defined Contribution Promise to pay fixed annual contributions to the pension fund Employee assumes risk of fund performance Defined Benefits Promise to pay fixed retirement benefit defined by a designated formula Employer assumes risk of fund performance

4

Defined Contribution Plans 401(k) Plans Permit voluntary contributions by employees (contributory plan) Money purchase plans Thrift plans Savings plans Profit-sharing plans

Plans Permit voluntary contributions by employees (contributory plan) Money purchase plans Thrift plans Savings plans Profit-sharing plans")

5

Components of Pension Expense + Service cost + Interest on pension liability - Return on plan assets Amortization of: + Prior service cost +/- Losses/gains resulting from a) revisions in estimates of pension liability b) investing plan assets

revisions in estimates of pension liability b) investing plan assets")

6

Pension Obligations Vested benefits obligation Present value of vested benefits at present pay levels Accumulated benefit obligation (ABO) Present value of vested and nonvested benefits at present pay levels Projected benefit obligation (PBO) Present value of vested, nonvested and additional benefits related to projected pay increases

Present value of vested and nonvested benefits at present pay levels Projected benefit obligation (PBO) Present value of vested, nonvested and additional benefits related to projected pay increases")

7

Projected Benefit Obligation Earned retirement benefits retirement annuity based on current data Present value of retirement annuity PV of retirement annuity at retirement date Projected benefit obligation PV of retirement annuity at current date

8

Example

12

Components that Cause Changes to Projected Benefit Obligation Service cost Current year of service Interest cost Beginning PBO * discount rate Prior service cost Result of plan amendments Gain or loss on the PBO Revision of estimates Payment of retirement benefits

13

Pension Plan Assets Pension plan assets are managed by a trustee Expected return on assets is included in periodic pension expense PBO > Plan Assets Underfunded pension plan Plan Assets > PBO Overfunded pension plan

14

Pension Expense + Service cost + Interest cost - Expected return on plan assets + Amortization of prior service cost + (-) Amortization of net loss or (gain)

Amortization of net loss or (gain)")

15

Recording Pension Expense and Pension Funding

16

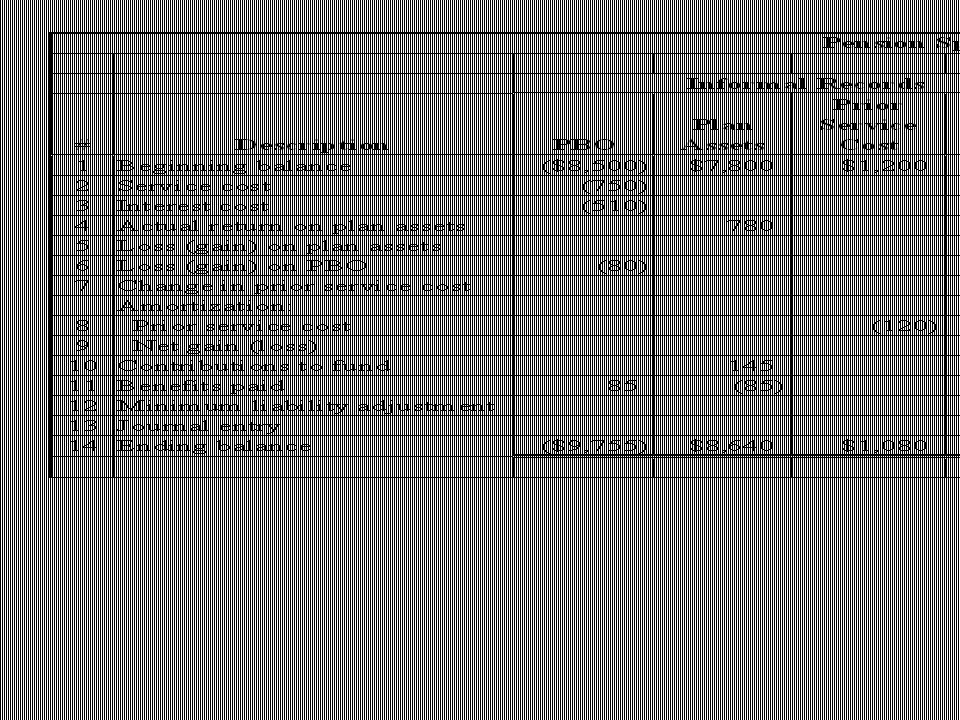

Pension Spreadsheet Informal Records PBO Plan assets Prior service cost Net loss (gain) Formal Records Pension expense Cash Prepaid (accrued) pension cost

Formal Records Pension expense Cash Prepaid (accrued) pension cost")

18

#1 Reconciliation Between Beginning Informal and Formal Records

19

#2 Service Cost Given by actuary as $750

20

#3 Interest Cost

22

#4 Actual Return on Plan Assets

23

#5 Loss (Gain) on Plan Assets

on Plan Assets")

25

#6 Loss (Gain) on PBO

on PBO")

27

#7 Change in Prior Service Cost In this case there is no change in prior service cost

28

#8 Amortization of Prior Service Cost

29

#9 Amortization of Net Gain (Loss) In this case there is no net gain (loss) on which amortization should be taken

In this case there is no net gain (loss) on which amortization should be taken")

30

#10 Contributions The employer made contributions to the plan in the amount of $145

31

#11 Benefits Paid The plan paid benefits to retirees in the amount of $85.

32

#12 Minimum Liability Adjustment None in this case

33

#13 Year-End Journal Entry to Record Pension Expense and Funding

34

#14 Reconciliation Between Beginning Informal and Formal Records

35

Postretirement Benefit Plans Medical insurance Dental insurance Life insurance Other postretirement benefits

36

Post Retirement Health Benefits Subject to the same assumptions as pension plans Additional assumptions Benefits are unrelated to service Benefits are based on medical need Costs are shared between employer and retiree Coverage is extended to spouses and qualified dependents

37

Net Cost of Benefits

38

Assumptions in addition to those applied to pension plans Estimated current cost of providing health benefits to retirees Demographic characteristics of potential retirees Benefits provided by Medicare Expected health care cost trends

39

Postretirement Benefit Obligation Expected postretirement benefit obligation (EPBO) Actuarial estimate of PV of future postretirement benefits Accumulated postretirement benefit obligation (APBO) Portion of EPBO attributed to employee service to date

Actuarial estimate of PV of future postretirement benefits Accumulated postretirement benefit obligation (APBO) Portion of EPBO attributed to employee service to date")

40

Example: Measuring the Obligation

41

APBO at 1/1/05

42

APBO at 12/31/05

43

Measuring APBO

44

Postretirement Benefit Expense Service cost Ending EPBO * one year of service Interest cost Beginning APBO * discount rate Amortization Prior service cost Liability resulting from plan amendment Net loss (Gain) Liability resulting in changes in assumptions Transition amount Liability at adoption of plan

Liability resulting in changes in assumptions Transition amount Liability at adoption of plan")

45

Required Disclosures Changes in APBO Components of net periodic postretirement benefit expense Weighted-average discount rate, rate of compensation used to compute postretirement benefit obligation Assumed health care cost trends

Similar presentations