Download presentation

Presentation is loading. Please wait.

2

Fiscal and Monetary Policy Effects CHAPTER 16

3

When you have completed your study of this chapter, you will be able to C H A P T E R C H E C K L I S T Describe the federal budget process and explain the effects of fiscal policy. 1 Describe the Federal Reserve’s monetary policy process and explain the effects of monetary policy. 2

4

16.1 THE BUDGET AND FISCAL POLICY Fiscal policy is the use of the federal budget to sustain economic growth and smooth the business cycle. The Federal Budget The federal budget is an annual statement of the expenditures and tax receipts of the government of the United States.

5

16.1 THE BUDGET AND FISCAL POLICY The government has a budget surplus if tax receipts exceed expenditures. The government has a budget deficit if expenditures exceeds tax receipts. The government has a balanced budget if tax receipts equal expenditures. Budget surplus (+)/deficit (–) = Tax receipts – Expenditures The government’s surplus or deficit is equal to tax receipts minus expenditures.

/deficit (–) = Tax receipts – Expenditures The government’s surplus or deficit is equal to tax receipts minus expenditures..")

6

16.1 THE BUDGET AND FISCAL POLICY The government borrows to finance a budget deficit and repays its debt when it has a budget surplus. The amount of debt outstanding that arises from past budget deficits is called national debt.

7

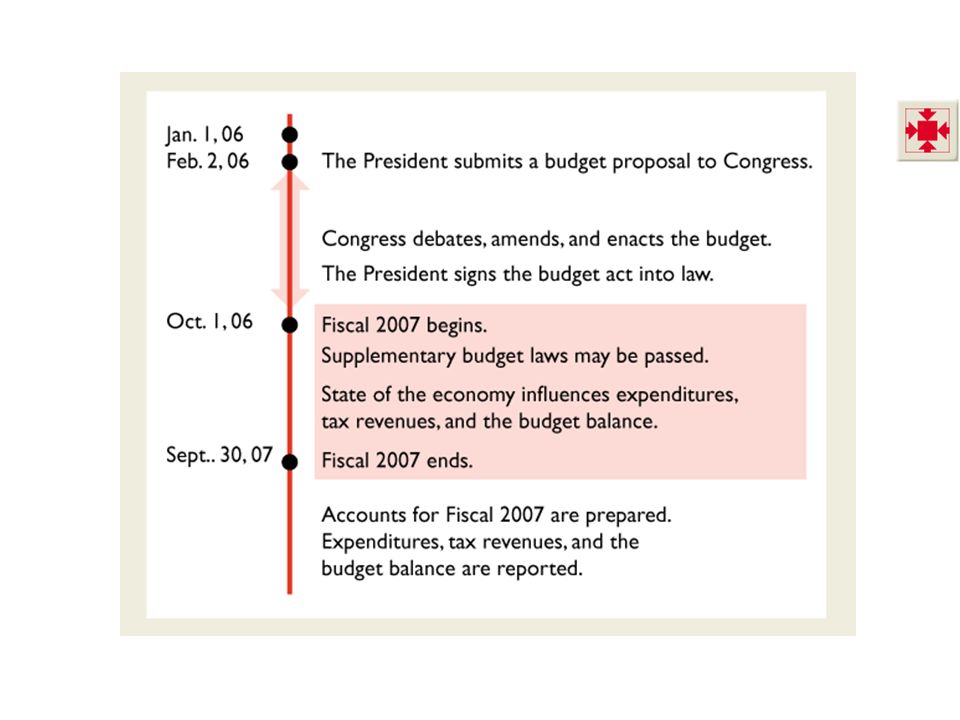

16.1 THE BUDGET AND FISCAL POLICY Figure 16.1 shows the federal budget time line for Fiscal year 2007. Budget Time Line The President and Congress make the federal budget on the annual time line.

9

16.1 THE BUDGET AND FISCAL POLICY Types of Fiscal Policy Fiscal policy can be either Discretionary or Automatic

10

16.1 THE BUDGET AND FISCAL POLICY Discretionary fiscal policy A fiscal policy action that is initiated by an act of Congress. Automatic fiscal policy A fiscal policy action that is triggered by the state of the economy For example, an increase in unemployment induces an increase in payments to the unemployed or in a recession tax receipts decrease as incomes fall.

11

16.1 THE BUDGET AND FISCAL POLICY Discretionary Fiscal Policy: Demand-Side Effects The Government Expenditure Multiplier The government expenditure multiplier is magnification effect of a change in government expenditure on goods and services on aggregate demand. It works like the investment multiplier.

12

16.1 THE BUDGET AND FISCAL POLICY The Tax Multiplier The tax multiplier magnification effect of a change in taxes on aggregate demand. A decrease in taxes increases disposable income. And an increase in disposable income increases consumption expenditure. With increased consumption expenditure, employment and incomes rise and consumption expenditure increases yet further.

13

16.1 THE BUDGET AND FISCAL POLICY So a decrease in taxes works like an increase in government expenditure. Both actions increase aggregate demand and have a multiplier effect. The magnitude of the tax multiplier is smaller than the government expenditure multiplier.

14

16.1 THE BUDGET AND FISCAL POLICY The Balanced Budget Multiplier The balanced budget multiplier is the magnification effect on aggregate demand of a simultaneous change in government expenditure and taxes that leaves the budget balance unchanged. The balanced budget multiplier is not zero—it is positive—because the government expenditure multiplier is larger than the tax multiplier.

15

16.1 THE BUDGET AND FISCAL POLICY Discretionary Fiscal Stabilization If real GDP is below potential GDP, the government might use discretionary fiscal policy in an attempt to restore full employment. Expansionary fiscal policy is a discretionary fiscal policy designed to increase aggregate demand—a discretionary increase in government expenditure or a discretionary tax cut.

16

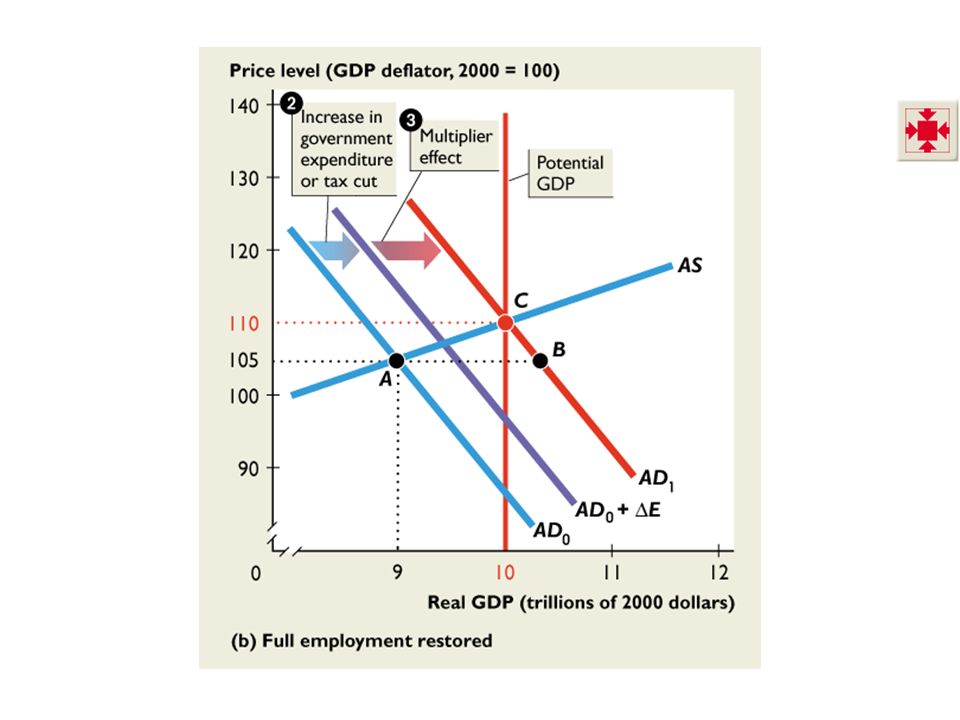

16.1 THE BUDGET AND FISCAL POLICY Potential GDP is $10 trillion, real GDP is $9 trillion, and 1. There is a $1 trillion recessionary gap. 2. An increase in government expenditure or a tax cut increases expenditure by ∆E. Figure 16.2 illustrates an expansionary fiscal policy.

17

16.1 THE BUDGET AND FISCAL POLICY 3. The multiplier increases induced expenditure. The AD curve shifts rightward to AD 1. The price level rises to 110, real GDP increases to $10 trillion, and the recessionary gap is eliminated.

19

16.1 THE BUDGET AND FISCAL POLICY Figure 16.3 illustrates contractionary fiscal policy. Potential GDP is $10 trillion, real GDP is $11 trillion, and 1. There is a $1 trillion inflationary gap. 2. A decrease in government expenditure or a tax rise decreases expenditure by ∆E.

20

16.1 THE BUDGET AND FISCAL POLICY 3. The multiplier decreases induced expenditure. The AD curve shifts leftward to AD 1. The price level falls to 110, real GDP decreases to $10 trillion, and the inflationary gap is eliminated.

22

16.1 THE BUDGET AND FISCAL POLICY Discretionary Fiscal Policy: Supply-Side Effects An increase in government expenditure that increase the quantities of productive services and capital increases aggregate supply.

23

16.1 THE BUDGET AND FISCAL POLICY Supply-Side Effects of Taxes Taxes decrease the supply of labor and saving. A decrease in the supply of labor increases the equilibrium real wage rate and decreases the equilibrium quantity of labor employed. Similarly, a decrease in the supply of saving increases the equilibrium real interest rate and decreases the equilibrium quantity of investment and capital employed.

24

16.1 THE BUDGET AND FISCAL POLICY With smaller quantities of labor and capital, potential GDP decreases, and so does aggregate supply. So an increase in taxes decreases aggregate supply.

25

16.1 THE BUDGET AND FISCAL POLICY Scale of Government Supply-Side Effects If both government expenditure and taxes increase, the scale of government increases. More productive government expenditure increases potential GDP, but higher taxes to pay for the expenditure decreases potential GDP. Economists disagree on which of these effects is stronger.

26

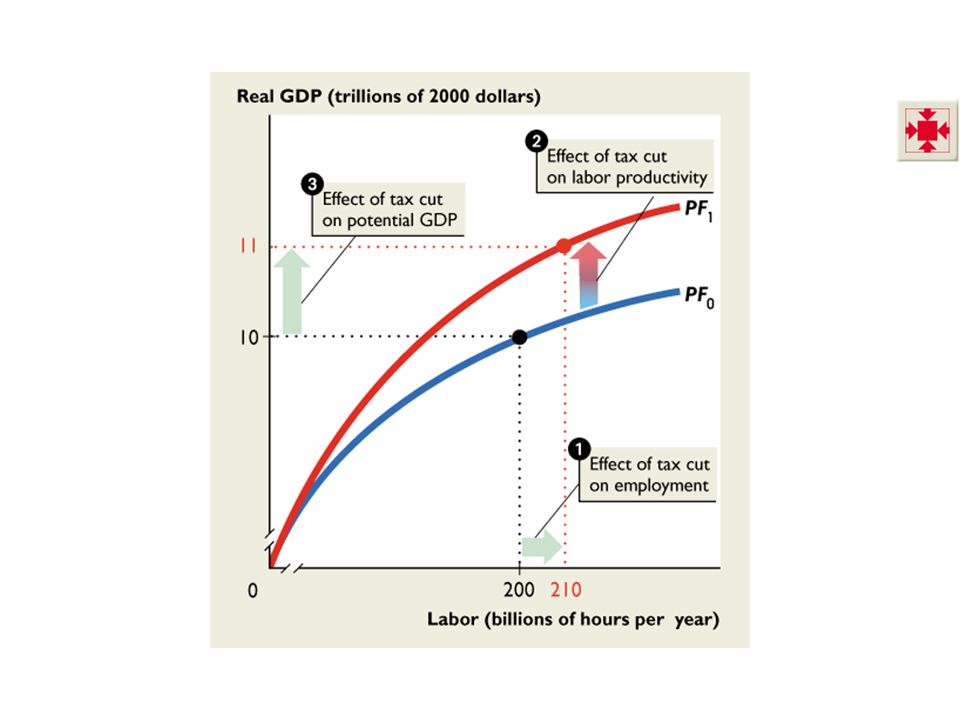

16.1 THE BUDGET AND FISCAL POLICY 1. A tax cut strengthens the incentive to work, increases the supply of labor, and increases employment. 2. A tax cut strengthens the incentive to save and invest, which increases the quantity of capital and increases labor productivity. Figure 16.4 illustrates the effects of fiscal policy on potential GDP.

27

16.1 THE BUDGET AND FISCAL POLICY 3. The combined effects of a tax cut on employment and labor productivity increases potential GDP.

29

16.1 THE BUDGET AND FISCAL POLICY Combined Demand and Supply Effects An increase in government expenditure or a tax cut increases equilibrium real GDP but might raise, lower, or have no effect on the price level. Figure 16.5 on the next slides shows the supply-side effects of fiscal policy when fiscal policy has no effect on the price level.

30

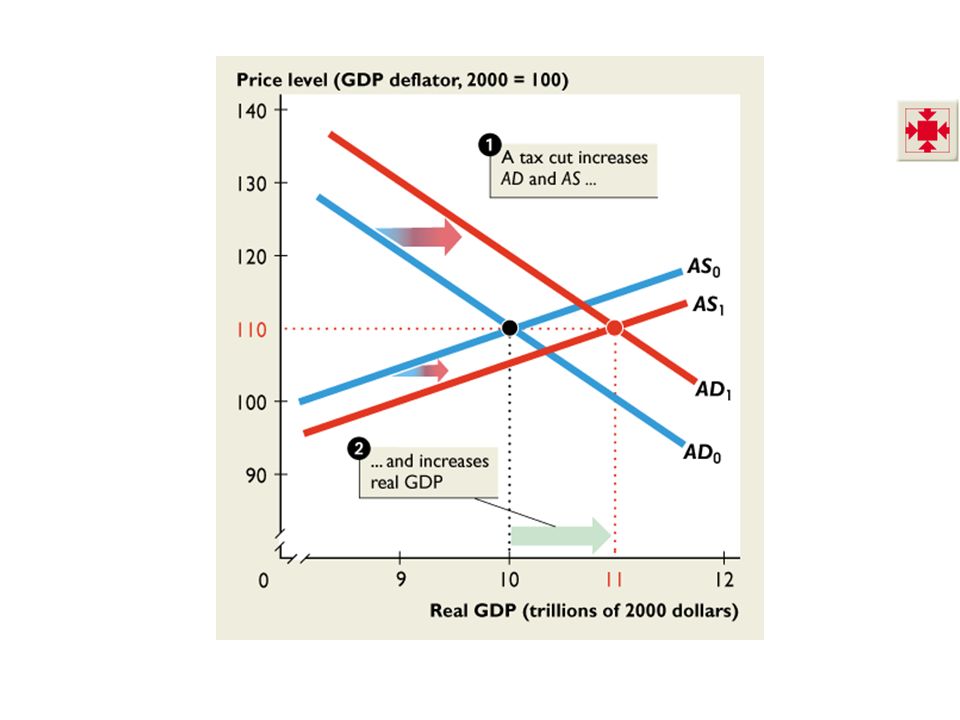

16.1 THE BUDGET AND FISCAL POLICY 1. A tax cut increases disposable income, which increases aggregate demand from AD 0 to AD 1. A tax cut also strengthens the incentive to work, save, and invest, which increases aggregate supply from AS 0 to AS 1. 2. Real GDP increases.

32

16.1 THE BUDGET AND FISCAL POLICY Limitations of Discretionary Fiscal Policy The use of discretionary fiscal policy is seriously hampered by three factors: Law-making time lag Estimating potential GDP Economic forecasting

33

16.1 THE BUDGET AND FISCAL POLICY Law-Making Time Lag The amount of time it takes Congress to pass the laws needed to change taxes or spending. This process takes time because each member of Congress has a different idea about what is the best tax or spending program to change, so long debates and committee meetings are needed to reconcile conflicting views.

34

16.1 THE BUDGET AND FISCAL POLICY Estimating Potential GDP It is not easy to tell whether real GDP is below, above, or at potential GDP. So a discretionary fiscal action might move real GDP away from potential GDP instead of toward it. This problem is a serious one because too much fiscal stimulation brings inflation and too little might bring recession.

35

16.1 THE BUDGET AND FISCAL POLICY Economic Forecasting Fiscal policy changes take a long time to enact in Congress and yet more time to become effective. So fiscal policy must target forecasts of where the economy will be in the future. Economic forecasting has improved enormously in recent years, but it remains inexact and subject to error. So for a second reason, discretionary fiscal action might move real GDP away from potential GDP and create the very problems it seeks to correct.

36

16.1 THE BUDGET AND FISCAL POLICY Automatic Fiscal Policy A consequence of tax receipts and expenditures that fluctuate with real GDP. Automatic stabilizers are features of fiscal policy that stabilize real GDP without explicit action by the government. Induced Taxes Induced taxes are taxes that vary with real GDP.

37

16.1 THE BUDGET AND FISCAL POLICY Needs-Tested Spending Needs-tested spending is spending on programs that entitle suitably qualified people and businesses to receive benefits— benefits that vary with need and with the state of the economy.

38

16. 2 THE FED AND MONETARY POLICY The Monetary Policy Process The Fed makes monetary policy in a process that has three main elements: Monitoring economic conditions Making policy decisions Reporting to Congress

39

Monitoring Economic Conditions Beige Book A report that summarizes current economic conditions in each Federal Reserve district and each sector of the economy. The Beige Book is a good source of current information about the state of the economy. 16. 2 THE FED AND MONETARY POLICY

40

Meetings of the Federal Open Market Committee (FOMC) The FOMC, which meets eight times a year, makes the monetary policy decisions. After each meeting, the FOMC announces its decisions and describes its view of the likelihood that its goals of price stability and sustainable economic growth will be achieved. 16. 2 THE FED AND MONETARY POLICY

41

The Monetary Policy Report to Congress Twice a year, in February and July, the Fed prepares a Monetary Policy Report to Congress, and the Fed chairman testifies before the House of Representatives Committee on Financial Services. 16. 2 THE FED AND MONETARY POLICY

42

Influencing the Interest Rate When the FOMC announces a policy change, its press release talks about the federal funds interest rate or the discount rate. The press release does not talk about the quantity of money or the size of the open market operations it plans to conduct. This impression that the Fed determines interest rates rather than the quantity of money is misleading to two reason: a long-run reason and a short-run reason. 16. 2 THE FED AND MONETARY POLICY

43

In the Long Run In the long run, the real interest rate is determined in global financial markets and the inflation rate is determined by the growth rate of the quantity of money. So in the long run, the Fed influences the nominal interest rate by the effects of its policies on the inflation rate. The Fed does not directly control the nominal interest rate, and it has no control over the real interest rate. 16. 2 THE FED AND MONETARY POLICY

44

In the Short Run In the short run, the Fed can determine the nominal interest rate and take actions to set the federal funds rate. But to do so, the Fed must undertake open market operations that change the quantity of money. Also, in the short run, the expected inflation rate is determined by recent monetary policy and inflation experience. So when the Fed changes the nominal interest rate, the real interest rate also changes, temporarily. 16. 2 THE FED AND MONETARY POLICY

45

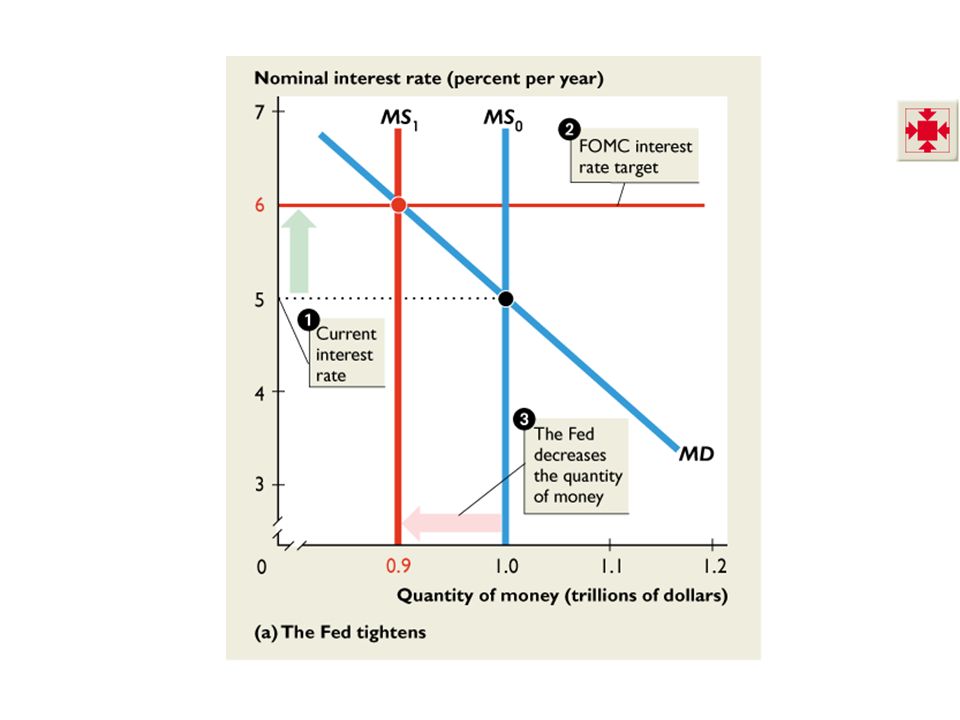

The Fed Raises the Interest Rate Suppose the Fed fears inflation and decides it must take action. The FOMC instructs the New York Fed to sell securities in the open market. This action mops up bank reserves. Some banks are short of reserves and they seek to borrow reserves from other banks. The federal funds interest rate rises. 16. 2 THE FED AND MONETARY POLICY

46

With fewer reserves, the banks make a smaller quantity of new loans each day until the quantity of loans outstanding has fallen to a level that is consistent with the new lower level of reserves. The quantity of money decreases. Figure 16.6(a) on the next slide illustrates these events. 16. 2 THE FED AND MONETARY POLICY

on the next slide illustrates these events THE FED AND MONETARY POLICY.")

47

1. The current interest rate is 5 percent a year. 2. The FOMC’s target interest rate is 6 percent a year. 3. To raise the interest rate to the target, the Fed must sell securities in the open market and decrease the quantity of money to $0.9 trillion. 16. 2 THE FED AND MONETARY POLICY

49

The Fed Lowers the Interest Rate If the Fed fears recession, it acts to increase aggregate demand. The FOMC announces that it will lower the short-term interest rates. To achieve this goal, the FOMC instructs the New York Fed to buy securities in the open market. 16. 2 THE FED AND MONETARY POLICY

50

This action increases bank reserves. Flush with reserves, banks now seek to lend reserves to other banks. The federal funds rate falls. With more reserves, the banks increase their lending and the quantity of money increases. Figure 16.6(b) on the next slide illustrates these events. 16. 2 THE FED AND MONETARY POLICY

on the next slide illustrates these events THE FED AND MONETARY POLICY.")

51

1. The current interest rate is 5 percent a year. 2. The FOMC’s interest rate target is 4 percent a year. 3. To lower the interest rate to the target, the Fed must buy securities in the open market and increase the quantity of money to $1.1 trillion. 16. 2 THE FED AND MONETARY POLICY

53

The Ripple Effects of the Fed’s Actions Suppose that the Fed increases the interest rate. Three main events follow: Investment and consumption expenditure decrease. The dollar rises, and net exports decrease. A multiplier process induces a further decrease in consumption expenditure and aggregate demand. 16. 2 THE FED AND MONETARY POLICY

54

Investment and Consumption Expenditure The interest rate influences investment and consumption expenditure. When the Fed increases the nominal interest rate, the real interest rate rises temporarily, and investment and expenditure on consumer durables decrease. 16. 2 THE FED AND MONETARY POLICY

55

The Dollar and Net Exports The higher price of the dollar means that foreigners must now pay more for U.S.-made goods and services. So the quantity demanded and the expenditure on U.S.- made items decrease. U.S. exports decrease. 16. 2 THE FED AND MONETARY POLICY

56

Similarly, the higher price of the dollar means that Americans now pay less for foreign-made goods and services. So the quantity demanded and the expenditure on foreign-made items increase. U.S. imports increase. 16. 2 THE FED AND MONETARY POLICY

57

The Multiplier Process Taking these effects together, investment, consumption expenditure, and net exports are all interest-sensitive components of expenditure. So a rise in the interest rate brings a decrease in aggregate expenditure. 16. 2 THE FED AND MONETARY POLICY

58

The decrease in expenditure decreases incomes, and the decrease in income induces a decrease in consumption expenditure. The decreased consumption expenditure lowers aggregate expenditure. Real GDP and disposable income decrease further, and so does consumption expenditure. Real GDP growth slows, and the inflation rate slows. 16. 2 THE FED AND MONETARY POLICY

59

Figure 16.7(a) shows ripple effects of the Fed’s actions when the Fed raises the interest rate. 16. 2 THE FED AND MONETARY POLICY

61

Figure 16.7(a) shows ripple effects of the Fed’s actions when the Fed lowers the interest rate.

shows ripple effects of the Fed’s actions when the Fed lowers the interest rate.")

63

16. 2 THE FED AND MONETARY POLICY Monetary Stabilization in the AS-AD Model The Fed Tightens to Fight Inflation Real GDP exceeds potential GDP and the Fed Fears inflation. Figure 16.8 illustrates how the Fed’s policy works.

64

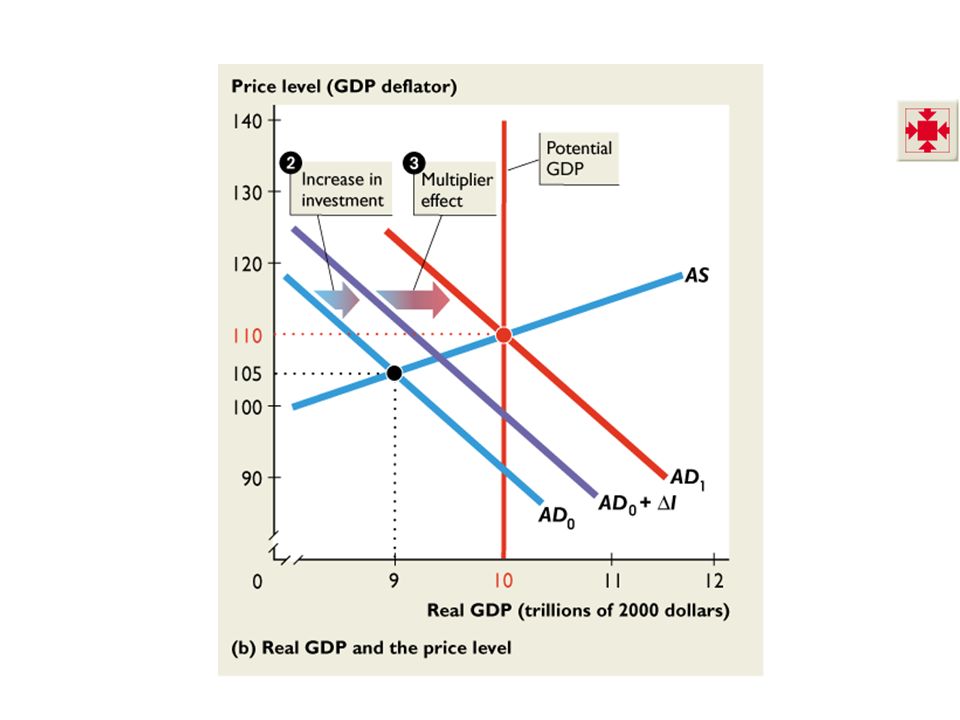

1. The Fed raises the interest rate and the quantity of investment decreases. 16. 2 THE FED AND MONETARY POLICY The curve ID is the investment demand curve. The interest rate is 5 percent a year and investment is $2 trillion.

66

2. Expenditure decreases by ∆I. 3. The multiplier induces additional expenditure cuts. The aggregate demand curve shifts to AD 1. 16. 2 THE FED AND MONETARY POLICY Real GDP decreases to potential GDP, and inflation is avoided.

68

The Fed Eases to Fight Recession Real GDP is below potential GDP and the Fed fears recession. Figure 16.9 illustrates how the Fed’s policy works. 16. 2 THE FED AND MONETARY POLICY

69

1. The Fed lowers the interest rate and the quantity of investment increases. The curve ID is the investment demand curve. The interest rate is 5 percent a year and investment is $2 trillion.

71

2. Expenditure increases by ∆I. 3. The multiplier induces additional expenditure. The aggregate demand curve shifts to AD 1. 16. 2 THE FED AND MONETARY POLICY Real GDP increases to potential GDP, and recession is avoided.

73

The Size of the Multiplier Effect The size of the multiplier effect of monetary policy depends on the sensitivity of expenditure plans to the interest rate. The larger the effect of a change in the interest rate on aggregate expenditure, The greater is the multiplier effect and The smaller is the change in the interest rate that achieves the Fed’s objective. 16. 2 THE FED AND MONETARY POLICY

74

Limitations of Monetary Stabilization Policy Monetary policy has an advantage over fiscal policy because it cuts out the law-making time lags. But monetary policy shares the other two limitations of fiscal policy: Estimating potential GDP is hard. Economic forecasting is error-prone. 16. 2 THE FED AND MONETARY POLICY

75

Fiscal Policy and Monetary Policy in YOUR Life Consider the U.S. economy right now. Is the U.S. economy at full employment or is there a recessionary gap or an inflationary gap? What type of fiscal policy or monetary policy would you recommend? What do recent changes in policy say about the government’s and the Fed’s view of the state of the economy? How do you think recent changes in fiscal policy and monetary policy will affect you?

Similar presentations