Download presentation

Presentation is loading. Please wait.

1

FIN 40153: Advanced Corporate Finance EVALUATING AN INVESTMENT OPPORTUNITY (BASED ON RWJ CHAPTER 5)

")

2

Capital Budgeting: Deciding what investments the company should make. Some Criteria that a good procedure for evaluating proposed investments should meet. –(1) Base the analysis on incremental costs and benefits, and don’t arbitrarily exclude any costs or benefits from the analysis. –(2) Allow for time value of money and for the risk involved. –(3) If forced to choose among proposals, select the one that does shareholders the most good.

Base the analysis on incremental costs and benefits, and don’t arbitrarily exclude any costs or benefits from the analysis. –(2) Allow for time value of money and for the risk involved. –(3) If forced to choose among proposals, select the one that does shareholders the most good..")

3

NPV Analysis Our recommended approach to evaluating proposed investments is Net Present Value (NPV) analysis. NPV = Present Value of the Incremental Benefits - Present Value of Incremental Costs. NPV-based decision rules: –When evaluating independent projects, take those with positive NPVs, reject those with negative NPVs. –When evaluating interdependent projects, take the combination with the highest combined NPV.

4

What About Approaches Other Than NPV? Other techniques are prevalent (or somewhat prevalent) in practice –Internal rate of return –Payback –Equivalent Annual Costs According to Graham and Harvey (2001), only the first two are used much in practice (see Table 6.5)

in practice –Internal rate of return –Payback –Equivalent Annual Costs According to Graham and Harvey (2001), only the first two are used much in practice (see Table 6.5).")

5

Mechanics of Each Technique Payback period –Payback period is number of years before cumulative cash flows equal the initial investment outlay Internal Rate of Return (IRR) is the discount rate that sets a project's NPV equal to zero NPV = Present Value of the Benefits - Present Value of the Costs EAA converts cash flows from projects into a similar annuity

is the discount rate that sets a project s NPV equal to zero NPV = Present Value of the Benefits - Present Value of the Costs EAA converts cash flows from projects into a similar annuity")

6

The Internal Rate of Return (IRR) Method IRR is a useful complement to NPV. The IRR is defined as the discount rate that causes the project’s computed NPV to equal zero. Note that the IRR computation starts with the same set of cash flow projections as the NPV analysis. The only way to compute an IRR is by trial and error.

7

The IRR Intuition The IRR can be interpreted as the answer to the following questions: –If the capital were placed in a bank account instead of the proposed project, what interest rate would that account have to pay, in order to generate the same future cash flows as this project? –Or, what rate of return can our shareholders expect to earn on the capital invested in this project?

8

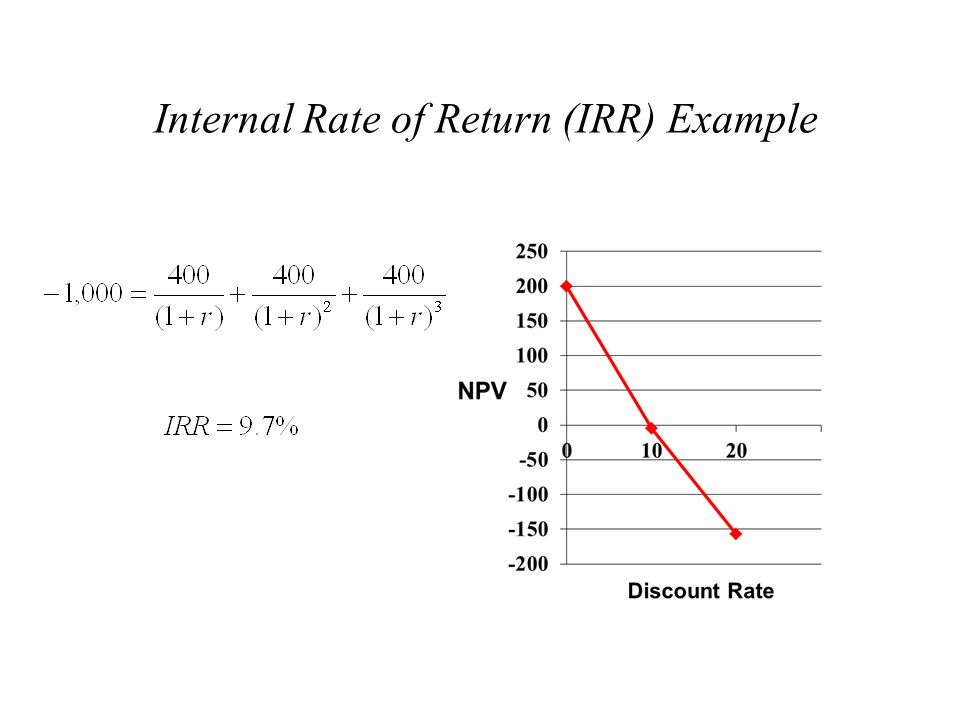

Consider the following stream of cash flows: Calculate the NPV at different discount rates until you find the discount rate where NPV equals zero. 0123 -1,000 400 Internal Rate of Return (IRR) Example

Example.")

10

Two Mutually Exclusive Projects: EAA Ignoring the difference in lives, project L should be accepted. But what if we can replicate project S?

11

Equivalent Annual Annuity Approach The EAA is the value of the level annuity payment that would be equivalent in present value terms to the projects original NPV. For Project S: EAA S = 4,132/1.7355 = $2,381 For Project L: EAA L = 6,190/3.1699 = $1,953 The EAA method says accept project S. –Be careful if you are working with costs rather than revenues.

12

Profitability Index Ratio of the total PV of future cash flows to the value of the initial costs Example: Two investment opportunities Project Cash Flow PV of C 1 and C 2 PI PV@12% C 0 C 1 C 2 1-20 70 10$70.5$3.53$50.5 2-101540 $45.3$4.53$35.3 Project 2 has the highest profitability index but Project 1 has the highest NPV. What should you do?

13

Use of PI: Capital Rationing Example: Suppose that you face a capital constraint of $20. Consider the previous example with an additional project. Project Cash Flow PV of C 1 and C 2 PI NPV@12% C 0 C 1 C 2 1 -20 70 10 $70.53.53$50.5 2 -10 15 40 $45.34.53$35.3 3 -10 -5 60 $43.44.34$33.4

14

Some Issues with IRR Multiple IRRs Scale effects Timing effects Mutually exclusive projects

15

Multiple IRRs There can be as many solutions to the IRR definition as there are changes of sign in the time-ordered cash flow series. Consider the stream: Can (and does) have two IRR’s. 012 -100-132 230

have two IRR’s")

16

Calculate NPV at different rates: The project is desirable if the discount rate is between 10.00% and 20.00%. But you don't know this until you calculate NPVs. This curve could be inverted!

17

Another IRR pitfall: Mutually Exclusive Projects: IRR can lead to incorrect conclusions about different projects' relative worth. Ralph owns a warehouse he wants to fix up and use for one of two purposes. –A:Store toxic waste containers –B:Store electronic equipment. Let's look at the cash flows, IRR’s and NPV’s:

18

There are also limitations in using IRR to choose between Projects. Example:

19

At low discount rates, B is better. At high discount rates, A is better. But A always has the higher IRR. An easy mistake would be to choose A regardless of discount rate.

20

Additional Cautions about IRR The IRR is stated as a percent per period (like an interest rate), so it is insensitive to the size of the project and to how many periods the project lasts. Would you rather earn, over the next 24 hours, a 200% return on a $1 investment, or a 100% return on a $1000 investment? Would you rather earn 25% for one year (with no unusual opportunities to follow) or 24% per year until you retire? Is NPV sensitive to these considerations? Simply choosing the project with the larger IRR would be justified only if cash flows could always be reinvested at the IRR instead of the actual capital market rate, r.

or 24% per year until you retire. Is NPV sensitive to these considerations. Simply choosing the project with the larger IRR would be justified only if cash flows could always be reinvested at the IRR instead of the actual capital market rate, r..")

Similar presentations