Download presentation

Presentation is loading. Please wait.

1

Lecture 3: Financial Statements, Cash flow, and taxes Financial Management

2

Slide Symbols ARTICLES TEXTBOOKS NOTES ILLUSTRATION / EXCERCISE

3

History Financial Management Why is it Important? The economic system has grown enormously and has become quite complex

4

The objective of financial statements To provide a picture of the overall financial position and performance of the business. For this objective to be achieved, the accounting system normally produces three statements at regular intervals. 1. The cash flow statement (tracks cash movements (in/out) in a given period) 2. Profit and loss account (income statement) – information on how much wealth was generated or lost in a given period 3. Balance sheet ( shows the accumulated wealth or the status of an organisation at the end of a given period)

in a given period) 2. Profit and loss account (income statement) – information on how much wealth was generated or lost in a given period 3. Balance sheet ( shows the accumulated wealth or the status of an organisation at the end of a given period).")

5

Cash Flow Statement “ Summary of a company's cash receipts and cash disbursements over a period of time; Lists cash to and cash from operating, investing, and financing activities, along with the net increase or decrease in cash for the period”. Refer to the National Express statement

6

Net Cash Flow The actual net cash, as opposed to accounting profit (net income), that a firm generates during a specified period Net cash flow = Net Income + Depreciation and Amortization

, that a firm generates during a specified period Net cash flow = Net Income + Depreciation and Amortization")

7

Cash flow statement It is important that a manager understands what happened in his business over a period of time (i.e. trace the flow of cash during the period) The cash flow in a business organisation revolve around three key business activities. 1.Use assets and fund raised to operate the business 2.Investment in assets to conduct business 3.Raising funds to finance the assets Cash flow statement provides information on how a company's operations are running, where its money is coming from, and how it is being spent

The cash flow in a business organisation revolve around three key business activities. 1.Use assets and fund raised to operate the business 2.Investment in assets to conduct business 3.Raising funds to finance the assets Cash flow statement provides information on how a company s operations are running, where its money is coming from, and how it is being spent.")

8

Balance Sheet “A record of a company's financial structure, showing what a company owns (assets), what it owes (liabilities) and what is left over for the owners (shareholders) after what it owes is deducted from what it owns (the net worth, also commonly referred to as equity)”. For additional information please consult the following link: http://www.investopedia.com/articles/04/031004.asp

9

Balance Sheet Provides information on an organisation’s assets, liabilities and equity and their relationships to each other at a point in time. Assists in answering the following questions: Can the firm meet its financial obligations? How much money has already been invested in this company? Is the company overly indebted? What kind of assets has the company purchased with its financing? (Ameritrade, 2003)

.")

10

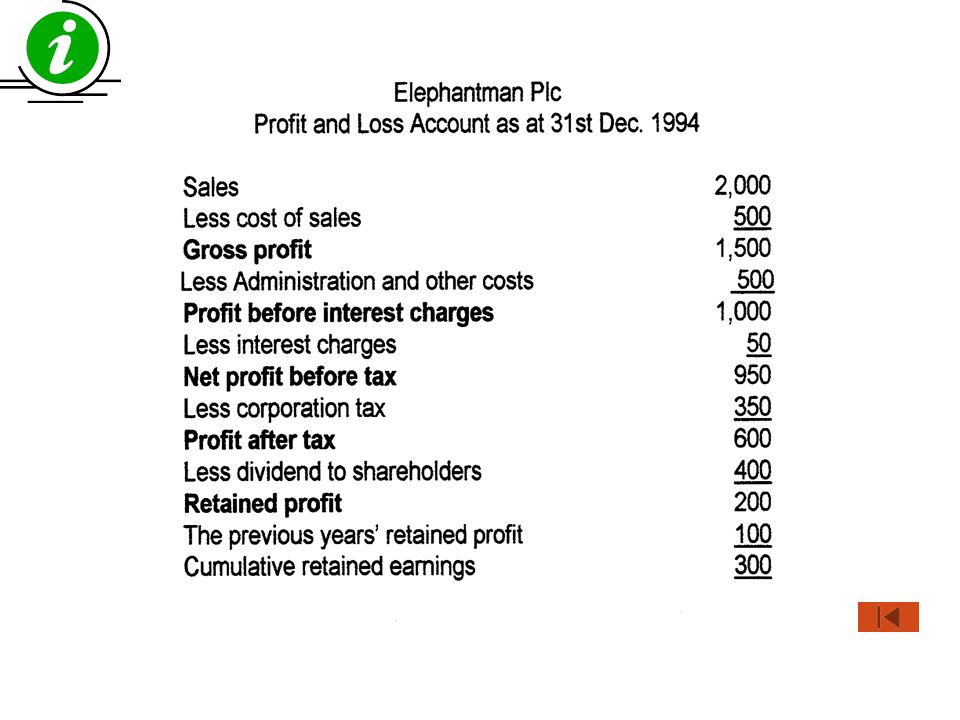

Trading Profit & Loss Account (Income Statement) “A financial statement that contains a summary of a business' financial operations for a specific period of time. It shows the net profit or loss for the period by stating the company's revenues and expenses”. GLOSARY DATA LOOK UP www.ncbuy.com/credit/glossary.html

11

Trading Profit & Loss Account (Income Statement) Provides information on: sales direct cost of sales gross profit administrative and other expenses corporation tax liability net profit dividends (declared and proposed) retained earnings.

Provides information on: sales direct cost of sales gross profit administrative and other expenses corporation tax liability net profit dividends (declared and proposed) retained earnings.")

12

Modified Accounting and Data for Investor and Managerial Decision Prepared by accountants and presented in annually report (mostly) Helpful for corporate decision making and stock valuation purposes If company obtains more assets than it actually needs, it will have raised too much capital and can impact to unnecessarily high capital cost

Helpful for corporate decision making and stock valuation purposes If company obtains more assets than it actually needs, it will have raised too much capital and can impact to unnecessarily high capital cost")

13

Cont’ Operating Assets and Operating Capital – When evaluating a company’s overall position and value, analyst often focus on net operating working capital (NOWC) – NOWC

– NOWC")

14

Cont’ NOWC – Operating working capital less accounts payable and accruals. It is the working capital acquired with investor supplied funds Total operating capital = NOWC + Fixed assets

15

Cont’ Net Operating Profit After Taxes (NOPAT) the profit a company would generate if it had no debt and held only operating assets. Free cash flow which is available for distribution to all investors ( stockholders and debt holders ) after company made all the investments in fixed asset, new product and working capital

after company made all the investments in fixed asset, new product and working capital.")

16

The Federal Income Tax System and terms Corporate Taxes Personal Taxes Interest Paid Interest Earned Dividends Paid Dividends Received Depreciation

17

Principal financial statements These are the principal means through which the management communicates information about the organisation to the stakeholders. – Stakeholders would want to know about the company resources and how the resources have been funded. They need the answer to the question, “where is this company?”– The Balance Sheet – They will also wish to satisfy themselves on the business performance of the company in terms of profit and trading activities – The Profit and Loss Account or Income Statement.. – They will want to understand the origins of cash inflow into the business as well as where cash outflows were directed at. In other words they wish to have good understanding of how the company business is being conducted. – The Cash flow statement These statements are backward looking (lagging metrics) because they report on past events and transactions. They are useful for evaluating past performance and monitoring trends for forecasting future performance. For internal decision making, these statements can be prepared using projected data so that future cash flows, profit and financial position can be assessed.

because they report on past events and transactions. They are useful for evaluating past performance and monitoring trends for forecasting future performance. For internal decision making, these statements can be prepared using projected data so that future cash flows, profit and financial position can be assessed..")

18

Cash Generated From business Asset sold and purchased Cash from bank loan & shares Bank balance at the end of the period

19

Original & written down values of company assets Investment in Other companies Cash in the office and bank, outstand- ing debtors and the value of closing stock. A breakdown of how much the Company owes The shareholders’ Interest in the company Dr. E. Davidson Assets Claims (creditors) Reading: See M-cLaney & Atril, p28-57 Claims (business owners)

Reading: See M-cLaney & Atril, p28-57 Claims (business owners).")

21

Readings McLaney and Atril (2005) Accounting: An Introduction. FT Prentice Hall, 3 th edition, p28-57; p62-84) Bringham and Houston (2007) Essential Financial Management

Bringham and Houston (2007) Essential Financial Management.")

22

Articles 1.Public Sector Cash flow Statement http://www.abs.gov.au/Ausstats/abs@.nsf/Lookup/4B1D272B99895D89CA256C320 0241891 http://www.abs.gov.au/Ausstats/abs@.nsf/Lookup/4B1D272B99895D89CA256C320 0241891 2.Private Sector Cash flow Statement – National Express http://www.nationalexpressgroup.com/nx/ic/kfd/cashflow http://www.nationalexpressgroup.com/nx/ic/kfd/cashflow 3.Rey (2005) How to read an Income Statement http://management.about.com/cs/adminaccounting/ht/readincomestmt.htm

How to read an Income Statement")

23

Cash Flow Statement “A cash flow statement is a financial report that shows incoming and outgoing money during a particular period (often monthly or quarterly). It does not include non-cash items such as depreciation. This makes it useful for determining the short-term viability of a company, particularly its ability to pay bills.financial report moneycashdepreciationpay bills People and groups interested in cash flow statements include: Accounting personnel, who need to know whether the organization will be able to cover payroll and other immediate expenses Accounting Potential lenders/creditors, who want a clear picture of a company's ability to repaylenderscreditorsability to repay Potential investors who need to judge whether the company is financially soundinvestors Potential employees or contractors who need to know whether the company will be able to afford compensation Cash flow statements are particularly important for start-up companies with limited liquid assets. These companies are vulnerable to devastating cash shortages, even when Accounts Receivable balances point to long-term financial health. “financial health (http://www.mywiseowl.com/articles/Cash_flow_statement )http://www.mywiseowl.com/articles/Cash_flow_statement

")

Similar presentations

and what a firm owes (liabilities) Asset = Liability.>")

![17-1 Learning Objectives After studying this chapter, you should be able to: [1] Indicate the usefulness of the statement of cash flows. [2] Distinguish.](/20/5984334/big_thumb.jpg "17-1 Learning Objectives After studying this chapter, you should be able to: [1] Indicate the usefulness of the statement of cash flows. [2] Distinguish.>")