Download presentation

Presentation is loading. Please wait.

1

SmartGrids From a Vision for Intelligent Electrical Grids

Ronnie Belmans Katholieke Universiteit Leuven, Belgium 24 / 03 / 2010

2

Agenda New Energy Challenges Transition towards a SmartGrid

What value is created? Helping integration of renewables towards a CO2-lean society Consumer engagement Long term job growth Research, Development & Deployment

3

New grid challenges EU Energy Policy

“EU policy focuses on creating a competitive internal energy market offering quality service at low prices, on developing renewable energy sources, on reducing dependence on imported fuels, and on doing more with a lower consumption of energy.” In 1997 The European Commission proposed that the EU should aim to reach a 12% share of renewable energy by Directives were adopted in the electricity and transport sectors that set national sectoral targets. In 2006 the EU had reached a 7% share (of gross inland consumption) and the latest progress report indicates that the EU is unlikely to reach either the electricity or transport target for 2010.

and the latest progress report indicates that the EU is unlikely to reach either the electricity or transport target for")

4

EU Goals Reduction of greenhouse gases Energy consumption, Efficiency increase Share of renewable energy 100% -20% -20% I. Concept European Energy Policy (slide 2) Most of you will know the most important targets which the European Union has agreed to meet by 2020: A 20% reduction of greenhouse gas emissions compared to 1990; A 20% increase in energy efficiency; and A 20% share of renewables including a 10% share for transport. Notably, two of these targets are binding and are applicable at Member State level. Hence, we have clearly passed the stage of non-binding political declarations and we now have detailed and firm commitments all over Europe. This is where the European Union has made a difference. 20% 8.5%

Most of you will know the most important targets which the European Union has agreed to meet by 2020: A 20% reduction of greenhouse gas emissions compared to 1990; A 20% increase in energy efficiency; and. A 20% share of renewables including a 10% share for transport. Notably, two of these targets are binding and are applicable at Member State level. Hence, we have clearly passed the stage of non-binding political declarations and we now have detailed and firm commitments all over Europe. This is where the European Union has made a difference. 20% 8.5%")

5

IEA 2030

6

IEA 2030 Ref: IEA WEO 2009 6

7

Annual energy related CO2 worldwide emissions

450 ppm scenario Annual energy related CO2 worldwide emissions Ref: IEA WEO 2009

8

European Policy Ten point action plan

Use the new internal energy market better Make it easier for Member States to help one another in case an energy crisis arises Improve the EU Emissions Trading Scheme Energy efficiency Increase the use of renewable energy Technology Low carbon technology for fossil fuels Safety and security of nuclear power Agree to an international energy policy Improve understanding

9

Current European power system

430 million people served 2500 TWh used 560 GW installed 500€/kW = 280G€ km HV 0.4M€/km = 90G€ Approx km MV+LV network 1500€ investment per EU citizen Largest man-made system 2007 430 million people served 2602 TWh used (+1.1% 2007) 560 GW installed 500€/kW = 280G€ km HV 0.4M€/km = 90G€ Approx km MV+LV network 1500€ investment per EU citizen Largest man-made system 2008 Gegevens Entsoe nog slechts beperkt en niet in grafiek/kaart beschikbaar: UCTE gegevens wel geupdate: UCTE statistics Million people served/GW/km geen gegevens over gevonden Vraag is of U hier op deze slide dan entso-e mag laten staan? Data provided by UCTE

560 GW installed 500€/kW = 280G€ km HV 0.4M€/km = 90G€ Approx km MV+LV network. 1500€ investment per EU citizen. Largest man-made system Gegevens Entsoe nog slechts beperkt en niet in grafiek/kaart beschikbaar: id=27. UCTE gegevens wel geupdate: UCTE statistics Million people served/GW/km geen gegevens over gevonden. Vraag is of U hier op deze slide dan entso-e mag laten staan Data provided by UCTE.")

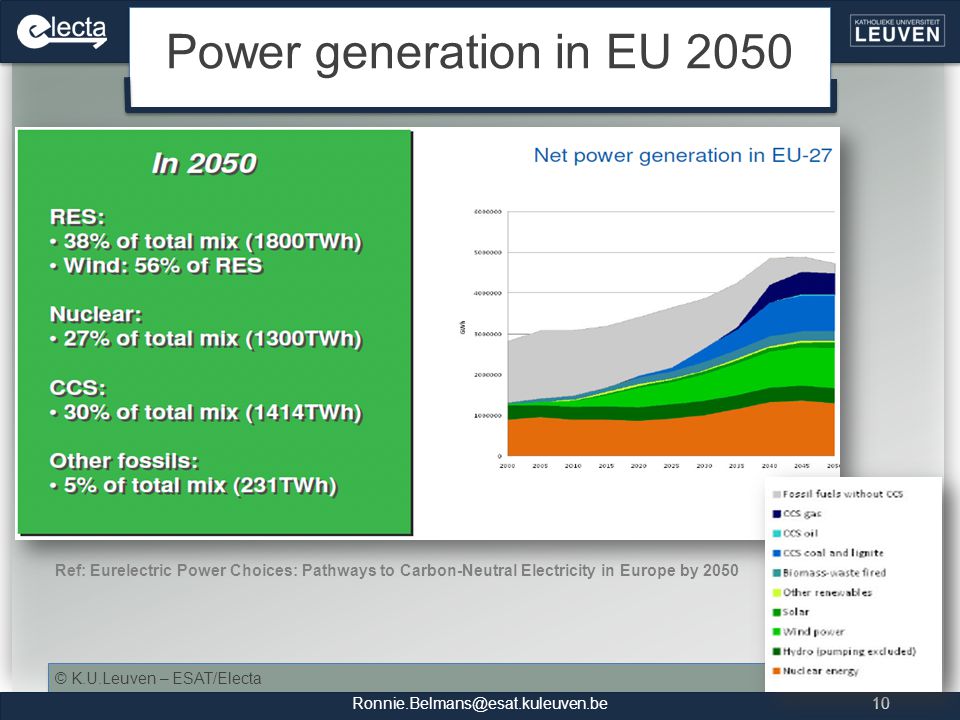

10

Power generation in EU 2050 Ref: Eurelectric Power Choices: Pathways to Carbon-Neutral Electricity in Europe by 2050

11

New grid challenges Overview

Future of energy demand Generation paradigm shift Ageing assets Markets and regulation

12

New grid challenges 1. Future of electricity demand

Rise of consumption at 2% a year 1250 TWh/year extra by 2030 Dependence on imported fuels? Plug-in Hybrid Electric Vehicles?

13

New grid challenges 2. New generation paradigm

Current grid = hierarchical One-way pipeline Source has no realtime info on termination points Peak demand reserve => inefficient use of grid Demand Traditional one-way supply system Supply G Generation Transmission Distribution

14

New grid challenges 2. New generation paradigm

Increasing wind generation & CHP units in Denmark

15

New grid challenges 2. New generation paradigm

Western Danish power system 400 kV Interconnections 150 kV 60 kV 10-20 kV 400 V 4 central units: 1,488 MW 5 central units: 1,939 MW 80 wind power units: 160 MW 15 local CHP plants: 24 wind power units: 578 MW 18 MW Range of central control Non-dispatchable and beyond central control 543 local CHP plants: 1,104 MW 4.057 wind power units: 2,201 MW

16

New grid challenges 2. New generation paradigm

Importance of wind forecasting Wind speed change of 1 m/s = variation of 320MW on a capacity of MW. Control systems needed to avoid excessive backup capacity “Fresh breeze” means somewhere between 200 and 1,600 MW

17

Technical miracles of the 20th century

Electrification Automobile Airplane Safe and Abundant Water Electronics Radio and Television Agricultural Mechanization Computers Telephone Air Conditioning and Refrigeration Interstate Highways Space Exploration Internet Imaging Technologies Household Appliances Health Technologies Petroleum and Gas Technologies Laser and Fiber Optics Nuclear Technologies High Performance Materials Still… new generation paradigms & ageing assets pose a serious challenge… (Source: National Academy of Engineering)

")

18

New grid challenges 2. New generation paradigm

Future grid = distributed Wind and solar “farms” Home PV + CHP+ PHEV G Generation G Supply Transmission Traditional one-way supply system Bi-directional supply system G G Distribution Generation Demand Generation

19

New grid challenges 2. New generation paradigm

Evolution in renewable energy production & Trend in PRIMES base scenario

20

New grid challenges 2. New generation paradigm

Wind generation cost Demand-pull CO2-lean energy supply needs renewable energy resources Dependency on primary energy sources Rising/fluctuating (?) fuel prices Liberalized market opportunities Energy efficiency: CHPs Subsidies, e.g. ROC PV cost Source: IEA Technology-push Experience curves of PV and wind Break-even point? Although not entirely true for wind due to bottlenecks in supply chain… Electrical energy storage? Source: PhD G. Nemet

fuel prices. Liberalized market opportunities. Energy efficiency: CHPs. Subsidies, e.g. ROC. PV cost. Source: IEA. Technology-push. Experience curves of PV and wind. Break-even point Although not entirely true for wind due to bottlenecks in supply chain… Electrical energy storage Source: PhD G. Nemet.")

21

New grid challenges 3. Ageing assets

Lagging investments in infrastructure Rising demand = decreasing safety margins Installation wave in European distribution systems in the 60s & 70s Replacement wave expected with business-as-usual approach Opportunity for new system architecture and operation schemes

22

New grid challenges 3. Ageing assets

More complex role and increased responsibilities of network operators for planning and asset management. Comprehensive integrated system solutions required from suppliers A stable and predictable regulatory framework is required Lack of EU-wide standards for integrated asset management and network planning Long term vision

23

New grid challenges 4. Markets and regulation

Energy market Data + information need > 20G€ investment (based on 100€ per connection) GenCo DistCo Retail TransCo REGULATED

GenCo. DistCo. Retail. TransCo. REGULATED.")

24

Drivers towards a smart grid

Regulation of Monopolies Innovation and Competitiveness Low Prices And Efficiency Primary Energy Sources Reliability and Quality Capacity Nature Preservation Climate Change Kyoto and Post-Kyoto Internal Market Security of Supply Environment

25

SmartGrids Vision User-centric Stakeholder ownership Networks renewal

Distributed and central generation Demand response Interoperable European Electricity Networks Liberalised markets Environmental policy

26

Challenges for 2020 and beyond

Micro- generation in millions of homes ? 50GW of wind power in the North ? Smart Grids will be needed to ensure supply security, connect and operate clean and sustainable energy, and give value for money Customer Interaction and Intelligent Appliances plus wind variation / cloud cover / customer choice… Ackgt TechFreep 30GW of solar power in the South ? New DC Links and Interconnections

27

SmartGrids Vision Multi-directional ‘flows’ End user real time

Information & participation Seamless integration of new applications Central & dispersed intelligence Smart materials and power electronics Central & dispersed sources

28

SmartGrids Vision Enable active customer participation

Provide power quality for the 21st Century Operate resiliently against attack and natural disaster Enable new products services and markets Anticipate and respond to system disturbances (self-heal) Accommo-date all generation and storage options Optimise assets and operate efficiently Enable fundamental changes in Transport and Buildings (Source: SmartGridNews.com)

Accommo-date all generation and storage options. Optimise assets and operate efficiently. Enable fundamental changes in Transport and Buildings. (Source: SmartGridNews.com)")

29

SmartGrids Vision 20th Century Grid 21st Century Smart Grid

Electromechanical Digital Very limited or one-way communications Two-way communications every where Few, if any, sensors – “Blind” Operation Monitors and sensors throughout – usage, system status, equipment condition Limited control over power flows Pervasive control systems - substation, distribution & feeder automation Reliability concerns – Manual restoration Adaptive protection, Semi-automated restoration and, eventually, selfhealing Sub-optimal asset utilization Asset life and system capacity extensions through condition monitoring and dynamic limits Stand-alone information systems and applications Enterprise Level Information Integration, inter-operability and coordinated automation Very limited, if any, distributed resources Large penetrations of distributed, Intermittent and demand-side resources Carbon based generation Carbon Limits and Green Power Credits Emergency decisions by committee and phone Decision support systems, predictive reliability Limited price information, static tariff Full price information, dynamic tariff, demand response Few customer choices Many customer choices, value adder services, integrated demand-side automation

30

SmartGrids Vision a smart metering revolution? a networks perspective

losses management & rewards “an RTU at every service head” intelligent demand control in emergencies the portal to demand & micro-gen services local network also the comms channel ? operational visibility of local networks new services to delight customers…. Load-limiting & remote disconnection

31

SmartGrids Vision How will the future grid look like?

Can we manage by stretching the current 380 kV grid to its limits? Or do we need a new overlay grid? “Stretching” was successful for trains Be aware of the “sailing ship syndrome”… We must accept the limits of today’s situation

32

? SmartGrids Vision A renewed grid vision? 1956 2020-2050 1948 1974

2008

33

SmartGrids Vision New roles for Network Co’s SS Integrator Optimiser

Energy Storage Grid Infeed SS Integrator Optimiser Aggregator Energy efficiency Customer overall participation Customer micro-gen types Heat networks Carrier communications Manage constraints and minimise losses Utilise smart meter data Manage asset condition / predict failure events Intelligent demand management in emergencies Aggregator and manager of dispersed power sources Aggregator and manager of ancillary services for local network and the grid (Source: EON Central Networks)

")

34

sustainable, economic and secure electricity supply

SmartGrids Vision Security of supply DSO’s SmartGrid Consumers Generators TSO’s Actions sustainable, economic and secure electricity supply Technology Standards Small scale generation Market considerations Consumer choice Regulations Reduced environmental impact What is a SmartGrid? A SmartGrid is an electricity network that can intelligently integrate the actions of all users connected to it - generators, consumers and those that do both – in order to efficiently deliver sustainable, economic and secure electricity supplies. A SmartGrid employs innovative products and services together with intelligent monitoring, control, communication, and self-healing technologies to: better facilitate the connection and operation of generators of all sizes and technologies; allow consumers to play a part in optimizing the operation of the system; provide consumers with greater information and choice of supply; => Energy awareness significantly reduce the environmental impact of the whole electricity supply system; deliver enhanced levels of reliability and security of supply. SmartGrids deployment must include not only technology, market and commercial considerations, environmental impact, regulatory framework, standardization usage, ICT (Information & Communication Technology) and migration strategy but also societal requirements and governmental edicts. Communication Energy Awareness Innovation Self-healing

and migration strategy but also societal. requirements and governmental edicts. Communication. Energy Awareness. Innovation. Self-healing.")

35

SmartGrids Vision Key Challenges

Strengthening the grid ensuring sufficient transmission capacity to interconnect energy resources, especially RES, across Europe Moving offshore Integrating intermittent generation Preparing for electric vehicles Enhancing intelligence of generation, demand and most notably in the grid Communication between millions of parties in a single market Developing decentralized architectures to enable smaller scale electricity supply systems to operate harmoniously Activating consumers, with or without their own generation, to play an active role in the operation of the system Moving offshore – developing the most efficient connections for offshore wind farms and for other marine technologies; Integrating intermittent generation – finding the best ways of integrating intermittent generation including residential microgeneration; Preparing for electric vehicles – whereas SmartGrids must accommodate the needs of all consumers, electric vehicles are particularly emphasized due to their mobile and highly dispersed character and possible massive deployment in the next years, what would yield a major challenge for the future electricity networks. Enhancing intelligence of generation, demand and most notably in the grid; Communications – delivering the communications infrastructure to allow potentially millions of parties to operate and trade in the single market; Developing decentralized architectures – enabling smaller scale electricity supply systems to operate harmoniously with the total system; Activation consumers– enabling all consumers, with or without their own generation, to play an active role in the operation of the system;

36

SmartGrids Vision Stakeholders Energy service providers

Technology providers Researchers Users Traders Regulators Governmental agencies Network companies Generators

37

From passive towards active grids

Integration of decentralized generation? Passive grids = Fit and Forget Fault Detection: power can come from any direction Power Quality: responsibility? Voltage Control: responsibility? Grid Planning: deterministic peak planning, cfr ER P2/5 in UK Significant grid problems at low levels of decentralized generation Active grids Normal operation Curtailment of generation Local power balance Coordinated voltage control Voltage regulators in-line Fault situations

38

From passive towards active grids

Active distribution system has three layers Copper based energy infrastructure (electricity) Communications layer Software layer Copper based energy infrastructure (electricity) Optimized topology Power electronic devices Communications layer requirements of speed, quality, reliability, dependability with costs different communication technologies at the same time Software layer multiple software functions for normal operation: doing locally and independently the maximum number of functions, reporting/requesting from the upper level the minimum possible information necessary network reconfiguration self-healing procedures fault management forecasting, modeling and planning.

Communications layer. Software layer. Copper based energy infrastructure (electricity) Optimized topology. Power electronic devices. Communications layer. requirements of speed, quality, reliability, dependability with costs. different communication technologies at the same time. Software layer. multiple software functions for normal operation: doing locally and independently the maximum number of functions, reporting/requesting from the upper level the minimum possible information necessary. network reconfiguration. self-healing procedures. fault management. forecasting, modeling and planning.")

39

From passive towards active grids New grid hierarchies

Cell concept (Denmark) Hierarchical structure in the power system in which each cell coordinates local balance (market for DG), clears fault situations and communicates with other cells in energy trading Virtual Power Plants (VPP) Flexible representation of load & generation, acting as 1 entity towards DSO/TSO (Source: (Source: Risö)

Hierarchical structure in the power system in which each cell coordinates local balance (market for DG), clears fault situations and communicates with other cells in energy trading. Virtual Power Plants (VPP) Flexible representation of load & generation, acting as 1 entity towards DSO/TSO. (Source: (Source: Risö)")

40

Transmission system changes

CORESO Central Western Europe Development of market mechanisms Strengthening security of supply Efficient and safe management of the electricity system requires means of coordination and organizational structures at this scale

41

Ancillary services of small generation units

Voltage support Feeder/transformer congestion Impact on T&D reinforcement deferral Black start capability of local grids? By means of Generation curtailment, Generation dispatch, e.g. CHPs Reactive power control Demand control? Storage?

42

Standardisation and interoperability

Lots of different standards exist Overlapping scope and functionality: Protocols for metering aspects, control-related or interaction Information models for data exchange Varying status: De jure standards from established organizations (ISO, IEC, …) De facto standards from alliances or user groups Fully proprietary protocols EC has acknowledged the need for harmonization Mandate M/441 on smart metering assigned to CEN, CENELEC and ETSI Speedy market acceptance demands standardization e.g. Unified European electric vehicle plug

De facto standards from alliances or user groups. Fully proprietary protocols. EC has acknowledged the need for harmonization. Mandate M/441 on smart metering assigned to CEN, CENELEC and ETSI. Speedy market acceptance demands standardization. e.g. Unified European electric vehicle plug.")

43

Public Acceptance much more than technology…

Smart Grids extend beyond networks and will embrace transport, the built environment, the behaviours and engagement of customers, and will need societal acceptance.

44

Public Acceptance much more than technology…

Smart Grids will require Customer Acceptance and Participation in: ...Intelligent Appliances & Demand Response ...Smart metering with 2-way communications ...Micro-generation providing grid services

45

Public Acceptance Consumer values

Services more fit to consumer’s expectations More information about consumption More awareness Energy savings Faster and more adequate metering and billing Smarter appliances / homes

46

Public Acceptance Privacy Issues Security Unknown privacy implications

Who can access which data? cfr. April 2009: smart meter proposal in The Netherlands rejected due to privacy concerns Need for regulations and contractual arrangements Security Cyberattacks on the grid Meter fraud Dependability Design enables self-healing and resilience Self-healing and resilience: Vinden van fouten in het net door digitale meters Meter fraud Vb: Meters Italie betalen zichzelf terug door minder diefstal

47

Jobs Direct In the electricity sector: Direct utility SmartGrid

New ESCOs Contractors Installation accelerators Service providers SmartGrid equipment providers Ref. KEMA New jobs at classical energy companies New jobs at new energy service companies Contractors for the roll-out of smart grids Smart grid equipment providers

48

Jobs Indirect Technologies dependent on SmartGrids

Renewable energy technology manufacturers Distributed generation CHP heat and electricity demand matching PHEV Charging cheaper when coordinated Telecommunication sector Renewables otherwise only limited penetration possible DG ie CHP heat and electricity demand coupling PHEV charging power flows need to be controlled to avoid grid problems, billing systems necessary for charging at tertiary locations

49

Jobs Both high and lower skilled workers necessary

Installing smart meters Keeping the lights on Long term job growth Classical energy companies New business models Rollout is a huge effort Every home needs a meter Each windmill must be connected

50

Current Status Global recognition of the benefits towards implementation of Smart Grids for all actors Widespread rollout of “Smart” is technically possible during the next decade Complex and not fully clear how this evolution is going to take place in practice

51

Current Status Large-scale deployment not yet happened, why not? Some reasons: Limited pilot experiences so far Limited statistical significance of the quantification of benefits achieved in these experiences Uncertainties regarding the global investments Key challenges for the Smart Grid deployment: Largely of regulatory nature To a lesser extent influenced by research and development issues and by a lack of suitable demonstration pilot projects

52

What are the Elements for Success?

Action Now! and beyond 2050 targets 2020 targets REQUIRES research for tomorrow’s technologies REQUIRE development of today’s technologies REQUIRE application of today’s technologies These actions must be put in hand NOW

53

SmartGrids From a Vision for Intelligent Electrical Grids

Thank you for your attention ! Ronnie Belmans Katholieke Universiteit Leuven, Belgium

Similar presentations

>")

Dr Samuel Jupe (Parsons Brinckerhoff) UK Member.>")